|

市场调查报告书

商品编码

1536979

汽车工程服务外包:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Automotive Engineering Services Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

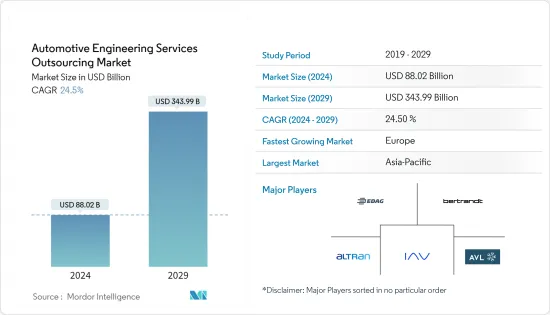

汽车工程服务外包市场规模预计到2024年为880.2亿美元,预计到2029年将达到3,439.9亿美元,在预测期内(2024-2029年)复合年增长率为24.5%。

从长远来看,工程公司正在迅速转向外包,以降低成本、提高效率和增加产能。公司出于多种原因外包工程服务,包括需要快速週转时间、灵活性、缺乏内部专业知识以及预算限制。此外,对电动车的需求不断增长、电动车的日益普及、自动驾驶汽车的创新技术(例如提高车辆和乘客安全的 ADAS)、轻型汽车等将对未来几年的市场成长产生积极影响。引起

鑑于电动车销量的成长,供应链中的多家公司正在合作加强汽车零件的设计。世界各地政府推出了各种计划和倡议,鼓励买家倾向于购买电动车而不是传统汽车。

主要亮点

- 加州ZEV计划就是其中一项鼓励购买电动车的计划,该计划的目标是到2025年让150万辆电动车上路。

- 2023年11月,Capgemini SA将利用其在软体开发和产品工程方面的关键专业知识,在自动驾驶、联网汽车、电动和共享汽车领域开发可持续、永续的连网型解决方案。Capgemini SA在 Everest Group ACES 汽车工程服务 PEAK Matrix 评估 2023 中获得了最高的「愿景和能力」评级,并被评为顶级领导者。

由于OEM的存在以及消费者对电动车偏好的变化,预计欧洲目标市场将显着成长。德国和英国等国家的存在也对市场成长产生了积极影响,因为其政府实施了排放气体政策和鼓励使用绿色技术的政策。预计北美市场在预测期内也将出现可观的成长。

汽车工程服务外包市场趋势

乘用车占有率第一

近年来,乘用车以其时尚的设计、紧凑的尺寸和经济的价值等特点受到了驾驶者的广泛欢迎。乘用车已成为许多已开发国家最常见的交通途径。在全球范围内,由于生活方式的改善、购买力的提高、可支配收入的增加、品牌知名度的提高和经济的改善,客户偏好正在发生变化,乘用车销量也在增加。

印度汽车工业协会的数据显示,2022-2023年乘用车销量从14,67,039辆增加到17,47,376辆。

亚太地区对电动车的需求不断增长也带动了市场的成长。 2023年第一季,印度电动车销量与2022年同期相比翻了一番。

运动型多用途车(SUV)的需求不断增长,为市场参与者创造了利润丰厚的机会,也是全球乘用车市场成长的主要动力。 SUV 在乘用车 (PV) 总销量中的份额从 2016 年的 18% 上升到 2023 年的 41%。

两家公司致力于开发汽车工程领域令人兴奋的能力,并共用对未来移动出行的愿景。我们也专注于在全球范围内扩展这些能力和创新的协议。业务领域包括电气和电子、软体、咨询服务、测试和车辆开发。

例如,2022 年 10 月,数位转型、咨询和业务再造服务及解决方案的领先供应商 Tech Mahindra 宣布将加入富士康主导的Mobility in Harmony)联盟。

因此,预计上述因素将对市场产生正面影响。

亚太地区预计将占据汽车工程服务外包市场的主要份额

预计亚太地区将占据目标市场的很大份额。这是由于主要汽车製造商由于劳动力成本低廉而将生产和相关业务外包给印度、韩国和中国等国家。因此,汽车 ESO 提供者正在将其业务迁往该地区。

印度约占低成本国家可用劳动力的30%。与欧洲、拉丁美洲和北美国家相比,我们具有15-26%的成本优势。印度为全球OEM提供了一个竞争激烈的市场,以满足世界各个领域的需求。起亚和名爵是印度市场的两家新OEM。

印度低成本、受过良好教育的半技术纯熟劳工使其成为寻求外包的国际OEM的有吸引力的选择。多家公司专注于合作开发永续行动解决方案,并建立下一代电动车、自动驾驶解决方案和行动服务应用,为行动产业的消费者带来价值。例如

- 2022年8月,总部位于印度的L&T Technology Services获得了宝马集团一份为期五年的资讯娱乐合同,为其资讯娱乐套件提供高端工程服务。由于靠近宝马集团园区,LTTS 工程师能够开发各种解决方案并即时提供服务。

因此,上述因素预计将对市场成长产生正面影响。

汽车工程服务外包产业概况

汽车工程服务外包市场由全球和地区知名公司整合和主导。这些公司采用新产品发布、联盟和合併等策略来维持其市场地位。例如

- 2023年9月,HCLTech以2.76亿美元收购德国汽车工程服务供应商ASAP集团100%股权。该交易预计将于 2023 年 9 月完成。 ASAP 专注于自动驾驶、电动车和连网领域的面向未来的汽车技术。

主导市场的一些主要企业包括 AVL List GmbH、Bertrandt AG、EDAG Engineering GmbH、IAV GmbH 和 Altran。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 汽车工业快速成长

- 市场限制因素

- 汽车领域研发业务数位化

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 按服务类型

- 设计

- 原型製作

- 系统整合

- 测试

- 按位置类型

- 陆上

- 离岸

- 车辆类型

- 客车

- 商用车

- 推进类型

- 内燃机

- 电动发动机

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东/非洲

- 北美洲

第六章 竞争状况

- 公司简介

- AVL List GmbH

- Bertrandt AG

- EDAG Engineering GmbH

- IAV GmbH

- HORIBA Ltd

- Altran(Capgemini Engineering)

- FEV Group GmbH

- MBtech Group GmbH(A subsidiary of AKKA Technologies)

- Alten GmbH

- P3 Automotive GmbH

- Altair Engineering Inc.

- ITK Engineering GmbH(Robert Bosch GmbH)

- ESG Elektroniksystem-und Logistik-GmbH

- RLE International Group

- ASAP Holding GmbH

- Kistler Holding AG

第七章 市场机会及未来趋势

The Automotive Engineering Services Outsourcing Market size is estimated at USD 88.02 billion in 2024, and is expected to reach USD 343.99 billion by 2029, growing at a CAGR of 24.5% during the forecast period (2024-2029).

Over the long term, engineering firms are rapidly shifting to outsourcing to save costs, boost efficiency, or increase competence. Companies outsource engineering services for various reasons, including the need for fast delivery, flexibility, a lack of in-house specialists, and a constrained budget. Additionally, increasing demand for electric vehicles, as well as increasing adoption of electric vehicles, autonomous vehicle innovative technologies such as ADAS for vehicle and passenger safety, and lightweight vehicles, are key factors that may positively impact market growth in the coming years.

Considering the growth in electric vehicle sales, several companies from the supply chain are entering into partnerships to enhance the design of vehicle components. Governments have launched various plans and efforts worldwide to encourage buyers to lean toward electric vehicles over conventional automobiles.

Key Highlights

- One such plan that encourages the purchase of electric vehicles is the California ZEV program, which intends to have 1.5 million electric vehicles on the road by 2025.

- In November 2023, Capgemini offered sustainable, safe, secure, and connected solutions with key expertise such as software development and product engineering in the Autonomous, Connected, Electric, and Shared vehicles domains. It received the highest "Vision and Capability" rating and was designated the top Leader by the Everest Group ACES Automotive Engineering Services PEAK Matrix Assessment 2023.

Europe is expected to grow significantly in the target market, owing to the presence of OEMs and changing consumer preference toward electric vehicles. The presence of countries such as Germany and the United Kingdom also positively impacts the market's growth due to the policies and regulations implemented by their governments related to emissions and encouraging the usage of green technology. North America is also expected to witness considerable market growth during the forecast period.

Automotive Engineering Services Outsourcing Market Trends

Passenger Cars Hold the Highest Share

Passenger cars have gained immense popularity among drivers over the past few years due to features such as stylish design, compact size, and economic value. Passenger cars are the most common mode of transportation in numerous advanced countries. The improving lifestyles, increasing purchasing power, rising disposable incomes, growing brand awareness, and improving economy are leading to a shift in customer preferences worldwide globe, resulting in high sales of passenger cars.

According to the Society of Indian Automobile Manufacturers, sales of passenger cars increased from 14,67,039 to 17,47,376 units during 2022-2023.

The increased demand for electric vehicles in Asia-Pacific also resulted in market growth. In the first quarter of 2023, electric car sales in India doubled compared to the same period in 2022.

The rising demand for sport utility vehicles (SUVs) creates profitable opportunities for market players and acts as a major driving factor for the global passenger car market's growth. The share of SUVs in overall passenger vehicle (PV) sales rose from 18% in 2016 to 41% in 2023.

Companies are focusing on developing some exciting capabilities in automotive engineering and sharing their vision for the future of mobility. They are also focusing on agreements to scale these capabilities and innovations globally. The segments include electric/electronics, software, consulting and service, testing, and vehicle development.

For instance, in October 2022, Tech Mahindra, a leading provider of digital transformation, consulting, and business re-engineering services and solutions, announced a partnership with Foxconn-initiated MIH (Mobility in Harmony) Consortium, an open EV alliance that promotes collaboration in the mobility industry.

Thus, the abovementioned factors are expected to have a positive impact on the market.

Asia-Pacific is Expected to Hold a Major Share in the Automotive Engineering Service Outsourcing Market

Asia-Pacific is likely to have a large share of the target market, attributed to the presence of significant automobile OEMs and the outsourcing of production and associated operations to countries such as India, South Korea, and China due to the availability of low-cost labor. As a result, automotive ESO providers are transferring their operations to this region.

India accounts for roughly 30% of all available manpower among low-cost countries. The country has a 15-26% cost advantage over European, Latin American, and North American countries. India has provided a highly competitive market for global OEMs catering to the needs of various segments worldwide. Kia and MG are two new OEMs in the Indian market.

The availability of low-cost, educated, and semi-skilled labor in India makes it an attractive option for international OEMs seeking to outsource their operations. Several firms focus on partnerships to develop sustainable mobility solutions and build the next generation of electric vehicles, autonomous driving solutions, and mobility service applications that can deliver value for consumers in the mobility industry. For instance,

- In August 2022, L&T Technology Services, headquartered in India, bagged a 5-year infotainment deal from BMW Group to provide high-end engineering services for the company's suite of infotainment. The proximity to BMW Group's campus will enable LTTS' engineers to work on a variety of solutions and offer services in real-time.

Thus, the abovementioned factors are expected to positively impact the market's growth.

Automotive Engineering Services Outsourcing Industry Overview

The automotive engineering services outsourcing market is consolidated and led by globally and regionally established players. These companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions. For instance,

- In September 2023, HCLTech acquired a 100% stake in the German automotive engineering services provider ASAP Group for USD 276 million. The transaction was expected to close by September 2023. ASAP is focused on future-oriented automotive technologies in areas such as autonomous driving, e-mobility, and connectivity.

Some major players dominating the market include AVL List GmbH, Bertrandt AG, EDAG Engineering GmbH, IAV GmbH, and Altran.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Exponential Increase in Automotive Sector

- 4.2 Market Restraints

- 4.2.1 Digitization of R&D Operations in Automotive Sector

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Designing

- 5.1.2 Prototyping

- 5.1.3 System Integration

- 5.1.4 Testing

- 5.2 By Location Type

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Commercial Vehicles

- 5.4 Propulsion Type

- 5.4.1 IC Engine

- 5.4.2 Electric Engine

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE*

- 6.1 Company Profiles

- 6.1.1 AVL List GmbH

- 6.1.2 Bertrandt AG

- 6.1.3 EDAG Engineering GmbH

- 6.1.4 IAV GmbH

- 6.1.5 HORIBA Ltd

- 6.1.6 Altran (Capgemini Engineering)

- 6.1.7 FEV Group GmbH

- 6.1.8 MBtech Group GmbH (A subsidiary of AKKA Technologies)

- 6.1.9 Alten GmbH

- 6.1.10 P3 Automotive GmbH

- 6.1.11 Altair Engineering Inc.

- 6.1.12 ITK Engineering GmbH (Robert Bosch GmbH)

- 6.1.13 ESG Elektroniksystem- und Logistik-GmbH

- 6.1.14 RLE International Group

- 6.1.15 ASAP Holding GmbH

- 6.1.16 Kistler Holding AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

汽车工程服务外包(ESO)全球市场规模、份额、趋势和成长分析报告(2026-2034)

汽车工程服务外包(ESO)全球市场规模、份额、趋势和成长分析报告(2026-2034) 汽车工程服务外包市场规模、份额、趋势及预测(按服务、车辆类型、地点、应用和地区划分),2026-2034年

汽车工程服务外包市场规模、份额、趋势及预测(按服务、车辆类型、地点、应用和地区划分),2026-2034年 数位双胞胎汽车工程市场预测至2032年:按组件、部署模式、车辆类型、应用、最终用户和地区分類的全球分析汽车工程服务外包市场预测至 2032 年:按服务类型、车辆类型、推进类型、地区和应用进行全球分析

数位双胞胎汽车工程市场预测至2032年:按组件、部署模式、车辆类型、应用、最终用户和地区分類的全球分析汽车工程服务外包市场预测至 2032 年:按服务类型、车辆类型、推进类型、地区和应用进行全球分析 汽车工程服务外包市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测汽车工程服务外包市场规模:依服务、地点类型、车辆类型、应用、区域覆盖范围、预测

汽车工程服务外包市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测汽车工程服务外包市场规模:依服务、地点类型、车辆类型、应用、区域覆盖范围、预测 汽车工程服务外包市场规模、份额及成长分析(按服务、车辆类型、地点类型、性质类型、推进力、应用和地区)-2025 年至 2032 年产业预测

汽车工程服务外包市场规模、份额及成长分析(按服务、车辆类型、地点类型、性质类型、推进力、应用和地区)-2025 年至 2032 年产业预测 汽车工程服务外包市场:全球产业分析、市场规模、占有率、成长、趋势与未来预测(2025-2032年)

汽车工程服务外包市场:全球产业分析、市场规模、占有率、成长、趋势与未来预测(2025-2032年) 汽车工程服务外包市场 - 2024-2034 年全球产业分析、规模、份额、成长、趋势与预测

汽车工程服务外包市场 - 2024-2034 年全球产业分析、规模、份额、成长、趋势与预测