|

市场调查报告书

商品编码

1636233

电动车镍氢电池应用:市场占有率分析、产业趋势、成长预测(2025-2030)Nickel Metal Hydride Battery For Electric Vehicle Application - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

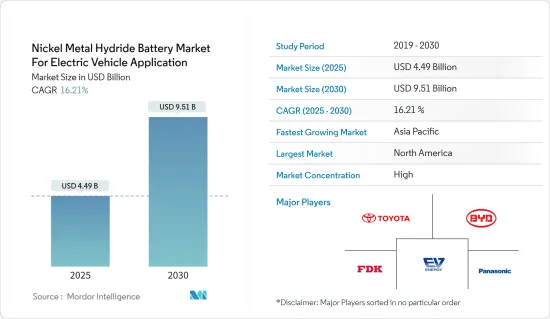

电动车镍氢电池应用市场预计将从2025年的44.9亿美元成长到2030年的95.1亿美元,预测期内(2025-2030年)复合年增长率为16.21%。

主要亮点

- 从中期来看,电动车需求增加和成本效益等因素预计将在预测期内推动市场发展。

- 另一方面,来自替代技术的竞争预计将阻碍预测期内的市场成长。

- 然而,技术进步预计将在未来几年为市场带来重大机会。

- 由于电动车在该地区各国的渗透率不断提高,预计亚太地区将主导市场。

镍氢电池市场趋势

预计电池驱动的电动车将占据主导地位

- 纯电动车(BEV)是一种没有内燃机、仅由可充电电池提供动力的电动车。推进依靠马达,该电动机储存在大容量电池组中。

- 镍氢电池由于其相对较高的能量密度、较长的使用寿命以及在各种温度范围内有效运行的能力,长期以来一直在各种电动车应用中广受欢迎。儘管锂离子电池近年来在市场上占据主导地位,但镍氢电池仍然发挥着重要作用,特别是在混合动力汽车和一些纯电动车中。

- 全球对纯电动车的需求正在迅速增长,销量预计将从 2019 年的 150 万辆增至 2023 年的 950 万辆。这一增长的推动因素包括日益增长的环境问题、旨在减少排放气体的政府法规以及电池技术的进步。

- 2023年,纯电动车成为最受买家欢迎的第三大选择。 12 月市场占有率上升至 18.5%,全年整体占有率达 14.6%,领先柴油引擎的 13.6%。汽油车以35.3%位居第一,混合动力车以25.8%位居第二。

- 然而,2023年12月新纯电动车销量自2020年4月以来首次下降,下降16.9%至16.07万辆。这一下降是由于2022年12月的强劲表现以及纯电动车最大市场德国的显着下降,下降了47.6%。儘管出现下滑,全年总销量仍超过150万辆,较2022年大幅成长37%,纯电动车市场占有率达14.6%。

- 相反,12 月欧盟混合动力电动车新註册量激增 26%,其中四个最大市场中的三个成长强劲:德国(+38%)、法国(+32.6%)、西班牙(+24.3%)。这一趋势促成2023年整体成长29.5%,导致混合动力电动车销量超过270万辆,占欧盟市场占有率的四分之一。

- 随着产业的发展,对镍氢技术的持续投资可能会导致镍氢技术在纯电动车市场的復兴,特别是在镍氢独特优势最有利的某些细分领域。总体而言,随着电动车需求的增加和电池技术的不断进步,镍氢电池市场的纯电动车领域有望成长。

预计北美将占据主导地位

- 在混合动力电动车 (HEV) 的普及和绿色交通解决方案的推动下,北美电动车 (EV) 应用的镍氢 (NiMH) 电池市场正在经历变革时期。镍氢电池以其耐用性、热稳定性和成本效益而闻名,由于其能够储存能量并有效支援再生煞车系统,因此广泛应用于混合动力汽车。

- 近年来,北美对电动车的需求大幅增加。光是美国的电动车销量就从 2019 年的 32.5 万辆增长到 2023 年的约 139 万辆,反映出消费者强烈转向更永续的交通途径。这一趋势得到了鼓励电动车采用和减少温室气体排放的政府奖励和政策的补充。

- 例如,2024 年 1 月,财政部和能源部宣布,《通货膨胀削减法案》的电动车充电税额扣抵30C 将适用于约三分之二的美国人,并将允许低收入地区和非都市区电动车充电基础设施成本最高可享 30% 的折扣,从而降低安装电动车充电基础设施的成本,并增加服务欠缺地区的电动车充电服务。

- 主要汽车製造商,尤其是丰田,透过将镍氢电池融入混合动力车型,引领了镍氢电池市场。丰田完善的混合动力汽车产品线严重依赖镍氢技术,对整体市场需求做出了巨大贡献。此外,汽车产业对提高燃油效率和减少对石化燃料的依赖的关注进一步巩固了镍氢电池在混合动力应用中的作用。

- 儘管面临来自锂离子电池的竞争,锂离子电池具有更高的能量密度和更快的充电时间,但镍氢电池由于其低成本和成熟的製造工艺,仍然是许多混合动力汽车的可行选择。此外,电池技术的进步正在提高镍氢电池的性能,使其在不断发展的市场中更具竞争力。

- 总之,在混合动力汽车的普及、技术进步和政府支持政策的推动下,北美电动车镍氢电池市场预计将成长。随着该地区继续优先考虑永续交通,镍氢电池将在向更清洁、更有效率的行动解决方案过渡中发挥关键作用。

镍氢电池产业概况

用于电动车应用的镍氢电池市场正在整合。主要参与者包括Panasonic控股公司、比亚迪公司、EV Energy、FDK和丰田汽车公司(排名不分先后)。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 至2029年市场规模及需求预测(单位:十亿美元)

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 电动车需求增加

- 成本效益

- 抑制因素

- 来自替代技术的竞争

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 依推进类型

- 电池电动车

- 油电混合车

- 插电式混合动力电动车

- 燃料电池电动车

- 按车型分类

- 客车

- 商用车

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 北欧的

- 俄罗斯

- 土耳其

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 印尼

- 泰国

- 越南

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 卡达

- 埃及

- 奈及利亚

- 其他中东和非洲

- 北美洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Panasonic Holdings Corporation

- BYD Company

- Toyota Motor Corp

- FDK Corporation

- EV Energy Co. Ltd

- Saft Group

- 市场排名/份额分析

- 其他知名企业名单

第七章 市场机会及未来趋势

- 技术进步

简介目录

Product Code: 50003501

The Nickel Metal Hydride Battery Market For Electric Vehicle Application Industry is expected to grow from USD 4.49 billion in 2025 to USD 9.51 billion by 2030, at a CAGR of 16.21% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing demand for electric vehicles and cost-effectiveness are expected to drive the market during the forecast period.

- On the other hand, competition from alternative technologies is expected to hinder market growth during the forecast period.

- However, technological advancements are expected to provide significant opportunities for the market in the coming years.

- Asia-Pacific is estimated to dominate the market due to the increasing adoption rate of electric vehicles across the various countries in the region.

Nickel Metal Hydride Battery Market Trends

Battery Electric Vehicles are Expected to Dominate

- Battery electric vehicles (BEVs) are electric vehicles powered entirely by rechargeable batteries with no internal combustion engine. They rely on electric motors for propulsion and store electricity in high-capacity battery packs.

- NiMH batteries have long been a popular choice for various electric vehicle applications due to their relatively high energy density, longevity, and ability to operate effectively in a range of temperatures. While lithium-ion batteries have dominated the market in recent years, NiMH batteries continue to play a significant role, especially in hybrid vehicles and some BEVs.

- The demand for BEVs has surged globally, with sales growing from 1.5 million units in 2019 to 9.5 million units in 2023. This growth is driven by increasing environmental concerns, government regulations aimed at reducing emissions, and advancements in battery technologies.

- Battery-electric cars were the third most popular choice among buyers in 2023. In December, their market share rose to 18.5%, contributing to an overall annual share of 14.6%, which surpassed diesel's steady 13.6%. Petrol vehicles maintained the top spot at 35.3%, while hybrid-electric cars held the second position with a 25.8% market share.

- However, in December 2023, new battery-electric car sales fell for the first time since April 2020, decreasing by 16.9% to 160,700 units. This decline was attributed to a strong performance in December 2022 and a notable drop in Germany, which saw a 47.6% decrease, as it is the largest market for battery-electric cars. Despite this dip, the total sales volume for the year exceeded 1.5 million units, marking a significant 37% increase compared to 2022, with the battery-electric car market share reaching 14.6%.

- Conversely, new EU registrations of hybrid-electric cars saw a 26% surge in December, driven by strong gains in three of the four largest markets: Germany (+38%), France (+32.6%), and Spain (+24.3%). This trend contributed to an overall increase of 29.5% in 2023, resulting in more than 2.7 million hybrid-electric vehicles sold, which accounted for a quarter of the EU market share.

- As the industry evolves, the continued investment in NiMH technology could lead to its resurgence in the BEV market, particularly in specific segments where its unique advantages are most beneficial. Overall, the BEV segment of the NiMH battery market is poised for growth as demand for electric vehicles rises and battery technology continues to advance.

North America is Expected to Dominate

- The North American nickel-metal hydride (NiMH) battery market for electric vehicle (EV) applications is witnessing a transformative phase driven by the increasing adoption of hybrid electric vehicles (HEVs) and the push for greener transportation solutions. NiMH batteries, known for their durability, thermal stability, and cost-effectiveness, are widely utilized in HEVs due to their ability to store energy and efficiently support regenerative braking systems.

- In recent years, the demand for electric vehicles in North America has surged significantly. The growth of electric vehicle sales, which increased from 325,000 units in 2019 to approximately 1.39 million units in 2023 in the United States alone, reflects a strong consumer shift toward more sustainable transportation options. This trend is complemented by government incentives and policies promoting EV adoption and reducing greenhouse gas emissions.

- For instance, in January 2024, the Department of Treasury and the Department of Energy confirmed that the Inflation Reduction Act's 30C for EV charging tax credit will be available to approximately two-thirds of American citizens and will provide up to 30% off the cost of the charger to individuals and businesses in low-income communities and non-urban areas, making it more affordable to install EV charging infrastructure and increasing access to EV charging in underserved communities.

- Major automotive manufacturers, particularly Toyota, have driven the NiMH battery market by integrating them into their hybrid models. Toyota's well-established HEV lineup, which relies heavily on NiMH technology, has contributed significantly to the overall market demand. Additionally, the automotive industry's focus on improving fuel efficiency and reducing dependence on fossil fuels has further solidified the role of NiMH batteries in hybrid applications.

- Despite competition from lithium-ion batteries, which offer higher energy densities and faster charging times, NiMH batteries remain a viable option for many HEVs due to their lower costs and established manufacturing processes. Moreover, ongoing advancements in battery technology are enhancing the performance of NiMH batteries, making them more competitive in the evolving market.

- In conclusion, the North American nickel-metal hydride battery market for electric vehicle applications is positioned for growth, driven by the increasing adoption of hybrid vehicles, technological advancements, and supportive government policies. As the region continues to prioritize sustainable transportation, NiMH batteries will play a crucial role in the transition to cleaner and more efficient mobility solutions.

Nickel Metal Hydride Battery Industry Overview

The nickel metal hydride battery market for electric vehicle applications is consolidated. Some of the major players include (not in particular order) Panasonic Holdings Corporation, BYD Company, EV Energy Co. Ltd, FDK Corporation, and Toyota Motor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand of Electric Vehicles

- 4.5.1.2 Cost-effectiveness

- 4.5.2 Restraints

- 4.5.2.1 Competition from Alternative Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Propulsion Type

- 5.1.1 Battery Electric Vehicles

- 5.1.2 Hybrid Electric Vehicles

- 5.1.3 Plug-in Hybrid Electric Vehicles

- 5.1.4 Fuel Cell Electric Vehicles

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 NORDIC

- 5.3.2.7 Russia

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Indonesia

- 5.3.3.7 Thailand

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 Nigeria

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Holdings Corporation

- 6.3.2 BYD Company

- 6.3.3 Toyota Motor Corp

- 6.3.4 FDK Corporation

- 6.3.5 EV Energy Co. Ltd

- 6.3.6 Saft Group

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements

02-2729-4219

+886-2-2729-4219

小型镍氢电池:全球市场份额和排名、总收入和需求预测(2025-2031 年)

小型镍氢电池:全球市场份额和排名、总收入和需求预测(2025-2031 年) 镍氢电池市场机会、成长动力、产业趋势分析及2025-2034年预测

镍氢电池市场机会、成长动力、产业趋势分析及2025-2034年预测 全球镍氢电池市场

全球镍氢电池市场 镍氢电池市场:按产品类型、应用、最终用户产业和地区划分

镍氢电池市场:按产品类型、应用、最终用户产业和地区划分 镍氢电池市场:全球产业分析、市场规模、市场占有率、成长、趋势与未来预测(2025-2032 年)

镍氢电池市场:全球产业分析、市场规模、市场占有率、成长、趋势与未来预测(2025-2032 年) 东协电动车镍氢电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)义大利电动车用镍氢电池:市场占有率分析、产业趋势、成长预测(2025-2030)亚太地区电动车镍氢电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)欧洲电动车镍氢电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)法国电动车用镍氢电池:市场占有率分析、产业趋势、成长预测(2025-2030)

东协电动车镍氢电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)义大利电动车用镍氢电池:市场占有率分析、产业趋势、成长预测(2025-2030)亚太地区电动车镍氢电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)欧洲电动车镍氢电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)法国电动车用镍氢电池:市场占有率分析、产业趋势、成长预测(2025-2030)

▼