|

市场调查报告书

商品编码

1636563

欧洲电动车(EV)充电设备 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)Europe Electric Vehicle (EV) Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

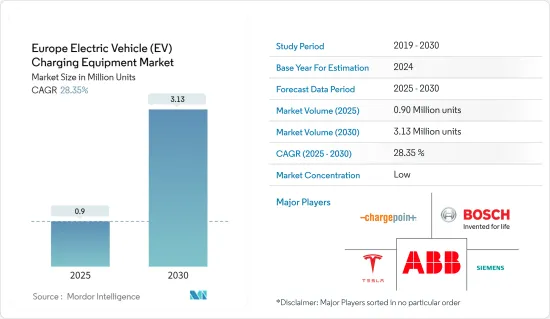

预计2025年欧洲电动车充电设备市场规模为90万台,2030年预计达313万台,预测期间(2025-2030年)复合年增长率为28.35%。

主要亮点

- 从中期来看,电动车普及率的提高以及政府倡议支持的加强电动车充电基础设施等因素预计将在预测期内推动电动车充电设备市场的发展。

- 相反,与安装充电站相关的高安装和维护成本也可能阻碍预测期内的市场成长。

- 然而,快速成长的欧洲市场对全面的电动车充电网路的需求,加上电动车充电设备的技术进步,在预测期内为欧洲电动车充电设备市场创造了重大机会。

- 德国积极采取倡议促进电动车的普及,并有望在欧洲市场取得显着成长。

欧洲电动车(EV)充电设备市场趋势

电池电动车领域占据市场主导地位

- 电池式电动车(BEV),通常称为电动车,利用大型牵引电池组为马达提供动力。为了充电,这些车辆连接到电动车供电设备(EVSE)。

- 作为全电动汽车,纯电动车通常没有内燃机 (ICE)、燃料箱或排气管。它从在电网上充电的电池组获取能量。作为零排放车辆,纯电动车可以减少空气污染,因为它们不会排放与传统汽油动力车辆相关的有害废气排放气体。

- 欧洲汽车产业正在经历重大转型,电池式电动车(BEV) 越来越受欢迎。在技术进步、政府支持和环保意识不断增强的推动下,纯电动车正在成为应对气候变迁和减少对石化燃料依赖的可行解决方案。

- 根据国际能源总署(IEA)的资料,2023年欧盟纯电动车销量将达到约160万辆,比2022年的120万辆成长33%。此外,欧盟的纯电动车库存总数已增加至约 460 万辆。随着纯电动车销量飙升,欧洲对充电基础设施的需求不断增加

- 此外,一些欧洲政府正在製定策略,以在未来几年增加电动车的采用。例如,2024 年 5 月,法国政府为其汽车製造商设定了一个雄心勃勃的目标,在未来 10 年内生产 200 万辆电动或混合动力汽车。作为与政府新中期协议的一部分,汽车业的中期目标是到 2027 年销售 80 万辆电动车,比 2022 年的 20 万辆大幅成长。此外,汽车製造商的目标是到 2022 年将电动车 (EV) 的年销量从 16,500 辆增加到 100,000 辆。这些雄心勃勃的目标将显着增加该地区对电动车充电设备的需求。

- 根据欧洲汽车工业协会(ACEA)预测,2023年欧盟将安装约15万个公共充电点(平均每週不到3,000个),使总合超过63万个。作为回应,欧盟委员会设定了到 2030 年拥有约 350 万个充电站的目标。为了实现这一目标,每年需要安装约 41 万个公共充电点(每週约 8,000 个)。

- 相反,ACEA 预测到 2030 年将需要 880 万个充电点。满足这项需求需要每年安装 120 万个充电站(每週超过 22,000 个),是目前数量的八倍。这些雄心勃勃的目标凸显了欧洲纯电动车市场的成长以及相关的电动车充电设备需求的激增。

- 近年来,多家中国知名汽车製造商表示有兴趣在欧洲建立製造和组装工厂,旨在扩大具有价格竞争力的汽车的销售,并与欧洲汽车製造商竞争。例如,2024 年 4 月,中国最大的出口商奇瑞汽车宣布,将与西班牙 EV Motors 合资,在加泰隆尼亚地区建立欧洲首个生产工厂。此外,有关未来十年内在英国建立汽车工厂的可能性的讨论正在进行中。

- 2023年,全球领先的电动车製造商之一比亚迪宣布计划在匈牙利建立第一个欧洲生产基地,三年后投产。该工厂将服务于欧洲市场,并将生产电池电动车和插电式混合动力车。这些发展预计将加强纯电动车製造业并增加对电动车充电基础设施的需求。

- 在这些发展中,纯电动车领域预计将在未来几年引领欧洲电动车充电设备市场。

德国正在经历显着的成长

- 德国正在迅速扩大其电动车(EV)设备和基础设施,反映出该国对电动车产业的加速承诺。据国际能源总署 (IEA) 称,到 2023年终,德国将拥有约 108,000 个公共电动车充电站。其中包括约 21,000 个快速充电设施和约 87,000 个慢速充电设施。具体来说,2023年将新增慢充点16,000多个、快充点6000个以上。

- 德国政府制定了雄心勃勃的计划,目标是到 2030年终在全国安装 100 万个公共充电站。然而,截至2023年下半年,这一目标仅实现了约11%。为了填补这一空白,预计未来几年公共电动车充电站将大幅增加,这表明电动车充电设备市场将快速成长。

- 各国政府正在积极核准在从公共场所到住宅和商业设施的各种地点安装电动车充电设施。这项倡议是为了应对道路上电动车数量的不断增加以及对电动车充电设备的需求成长。扩大电动车充电基础设施对德国至关重要,旨在透过消除续航里程问题和提高可及性来鼓励更多消费者转向电动车。

- 2024 年 2 月,欧洲着名电动车充电公司 Fastned 获得批准,可在德国高速公路沿线安装 34 个快速充电站。该倡议是「Deutschlandnets」竞标的一部分,强调了德国加强其电动车充电基础设施的承诺。 Fastned 的这项倡议是朝着 2030 年在欧洲安装 1,000 个快速充电站的雄心勃勃的目标迈出的一步。

- 在德国,越来越多的公司正在安装自己的电动车充电中心,作为加强其电动车基础设施并应对快速增长的充电设备需求的策略。这些枢纽不仅推动电动车的普及,还有助于减少碳排放并支持永续交通解决方案。

- 2023 年 11 月,梅赛德斯-奔驰在德国曼海姆开设了第一个内部充电中心。此专案符合梅赛德斯-宾士未来10年在全球安装超过2,000个充电站和10,000个快速充电点的目标。

- 德国也推动在加油站安装电动车充电设备,以加强对永续交通的承诺。这项任务不仅促进清洁能源汽车,还应对更广泛的气候变迁挑战。

- 2023 年 9 月,德国总理奥拉夫·肖尔茨宣布,他将很快颁布立法,要求 80% 的加油站提供至少 150 千瓦的快速充电选项。

- 鑑于这些发展,在电动车渗透率上升、强劲投资以及政府支持措施和目标的推动下,德国电动车(EV)充电设备市场预计将显着成长。

欧洲电动车(EV)充电设备产业概况

欧洲电动车(EV)充电设备市场已缩减一半。市场主要企业包括(排名不分先后)ABB Ltd、Robert Bosch GmbH、ChargePoint Inc.、Siemens AG 和 Tesla Inc.。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 至2029年市场规模及需求预测(单位:台)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车普及及相关投资扩大

- 政府措施支持加强电动车充电基础设施

- 抑制因素

- 与安装充电站相关的高安装和维护成本

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 车型

- 纯电动车(BEV)

- 插电式混合动力汽车(PHEV)

- 混合动力电动车(HEV)

- 应用

- 家庭充电

- 职场充电

- 公共充电

- 充电类型

- 交流充电(1 级和 2 级)

- 直流充电

- 地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧的

- 欧洲其他地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- ABB Ltd

- Robert Bosch GmbH

- Delta Electronics Inc.

- Siemens AG

- Tesla Inc.

- ChargePoint Inc.

- Enphase Energy, Inc.

- Powercharge

- Ampure

- Exicom Tele-Systems Ltd

- Schneider Electric SE

- Eaton Corporation

- 其他知名公司名单

- 市场排名分析

第七章 市场机会及未来趋势

- 电动车充电设备的技术进步

- 新兴欧洲市场需要强大的电动车充电网络

简介目录

Product Code: 50004069

The Europe Electric Vehicle Charging Equipment Market size is estimated at 0.90 million units in 2025, and is expected to reach 3.13 million units by 2030, at a CAGR of 28.35% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing adoption of electric vehicles and the efforts to enhance EV charging infrastructure supported by government initiatives are expected to drive the EV charging equipment market during the forecast period.

- Conversely, the market's growth during the forecast period may be stunted by the high installation and maintenance costs tied to setting up charging stations.

- However, the burgeoning European markets' demand for a comprehensive EV charging network, coupled with technological strides in EV charging equipment, presents substantial opportunities for the Europe EV charging equipment market during the forecast period.

- Germany, with its proactive initiatives promoting electric vehicle adoption, is poised for notable growth in the European landscape.

Europe Electric Vehicle (EV) Charging Equipment Market Trends

Battery Electric Vehicles Segment to Dominate the Market

- Battery electric vehicles (BEVs), commonly known as electric vehicles, utilize a sizable traction battery pack to power their electric motors. To recharge, these vehicles connect to electric vehicle supply equipment (EVSE).

- BEVs, being entirely electric, typically lack an internal combustion engine (ICE), fuel tank, or exhaust pipe. They derive their energy from a grid-recharged battery pack. As zero-emission vehicles, BEVs do not produce the harmful tailpipe emissions associated with traditional gasoline-powered cars, thus mitigating air pollution.

- Europe's automotive industry is undergoing a significant shift, with battery electric vehicles (BEVs) gaining traction and popularity. Driven by technological advancements, governmental backing, and heightened environmental awareness, BEVs are emerging as a viable solution to combat climate change and lessen dependence on fossil fuels.

- Data from the International Energy Agency (IEA) reveals that BEV sales in the European Union reached approximately 1.6 million units in 2023, marking a 33% increase from 1.2 million units in 2022. Furthermore, the total BEV stock in the EU has climbed to around 4.6 million units. As BEV sales surge, the demand for charging infrastructure in Europe intensifies.

- Moreover, several European governments are strategizing to amplify EV adoption in the upcoming years. For instance, in May 2024, the French government set an ambitious target for its automakers: to produce two million electric or hybrid vehicles by the decade's end. As part of a new medium-term agreement with the government, the industry aims for an interim target of 800,000 electric vehicle sales by 2027, a significant jump from 200,000 in 2022. Additionally, carmakers are setting their sights on boosting electric light utility vehicle sales to 100,000 annually, up from 16,500 in 2022. Such ambitious goals are poised to drive a substantial demand for EV charging equipment in the region.

- According to the European Automobile Manufacturers' Association (ACEA), the EU saw the installation of only about 150,000 public charging points in 2023 (averaging less than 3,000 weekly), bringing the total to over 630,000. In contrast, the European Commission aims for a target of around 3.5 million charging points by 2030. Achieving this would necessitate an installation rate of approximately 410,000 public charging points annually (or nearly 8,000 weekly), nearly three times the current rate.

- Conversely, ACEA projects a need for 8.8 million charging points by 2030. Meeting this demand would require an annual installation of 1.2 million chargers (or over 22,000 weekly), which is eight times the current rate. Such ambitious targets underscore the growing BEV market in Europe and the corresponding surge in demand for EV charging equipment.

- In recent years, several prominent Chinese automakers have expressed interest in establishing manufacturing and assembly plants in Europe, aiming to boost sales of competitively priced vehicles and challenge their European counterparts. For instance, in April 2024, Chery Auto, China's leading automaker by export volume, announced a joint venture with Spain's EV Motors to inaugurate its inaugural European manufacturing facility in Catalonia, with production slated to commence later in 2024. Furthermore, discussions are underway for potential car factories in Britain this decade.

- In 2023, BYD, the world's foremost EV manufacturer, declared plans for its maiden European production base in Hungary, set to commence operations in three years. This facility will cater to the European market, producing both battery EVs and plug-in hybrids. Such developments are anticipated to bolster the BEV manufacturing sector, subsequently amplifying the demand for a robust EV charging infrastructure.

- Given these dynamics, the BEV segment is poised to lead the European EV charging equipment market in the coming years.

Germany to Witness a Significant Growth

- Germany has been rapidly expanding its electric vehicle (EV) equipment and infrastructure, mirroring the nation's increasing embrace of the EV industry. According to the International Energy Agency (IEA), by the close of 2023, Germany boasted approximately 108,000 publicly available EV charging points. This tally comprised around 21,000 fast chargers and 87,000 slow chargers. Notably, in 2023, Germany added over 16,000 public slow charging points and 6,000 public fast charging points.

- The German government has ambitious plans, targeting the installation of 1 million public charging points nationwide by the end of 2030. Yet, as of late 2023, only about 11% of this target has been met. To bridge this gap, a substantial increase in public EV charging points is anticipated in the coming years, signaling a burgeoning market for EV charging equipment.

- The government is actively approving EV charging installations in diverse locales, from public spaces to residential and commercial properties. This initiative has spurred demand for EV charging equipment, catering to the rising number of electric vehicles on the roads. Expanding the EV charging infrastructure is pivotal for Germany, as it aims to alleviate range anxiety and enhance accessibility, thereby encouraging more consumers to transition to electric vehicles.

- In February 2024, Fastned, a prominent European EV charging firm, received approval to establish 34 fast-charging sites along Germany's highways. This initiative, part of the "Deutschlandnetz" tender, underscores Germany's commitment to bolstering its EV charging infrastructure. Fastned's move is a stride towards its ambitious goal of 1,000 fast charging stations across Europe by 2030.

- Companies in Germany are increasingly setting up their own EV charging hubs, a strategy to bolster the nation's EV infrastructure and cater to the surging demand for charging equipment. These hubs not only promote EV adoption but also play a role in curbing carbon emissions and championing sustainable transport solutions.

- In November 2023, Mercedes-Benz inaugurated its inaugural proprietary charging hub in Mannheim, Germany. This venture aligns with the company's global ambition of establishing over 2,000 charging stations by decade's end, featuring upwards of 10,000 fast-charging points.

- Germany is also pushing for EV chargers at gas stations, reinforcing its commitment to sustainable transport. This mandate not only promotes clean energy vehicles but also addresses broader climate change challenges.

- In September 2023, German Chancellor Olaf Scholz announced a forthcoming law stipulating that 80% of all service stations must offer fast-charging options, with a minimum capacity of 150 kilowatts.

- Given these developments, the EV charging equipment market in Germany is poised for significant growth, buoyed by rising EV adoption, robust investments, and supportive government policies and targets.

Europe Electric Vehicle (EV) Charging Equipment Industry Overview

The Europe electric vehicle (EV) charging equipment market is semi-fragmented. Some of the key players in the market (not in any particular order) include ABB Ltd, Robert Bosch GmbH, ChargePoint Inc., Siemens AG, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in Units, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles and Related Investments

- 4.5.1.2 Efforts to Boost EV Charging Infrastructure Supported by Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Installation Costs Associated With Setting Up Charging Stations And Maintenance Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Battery Electric Vehicle (BEV)

- 5.1.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.1.3 Hybrid Electric Vehicle (HEV)

- 5.2 Application

- 5.2.1 Home Charging

- 5.2.2 Workplace Charging

- 5.2.3 Public Charging

- 5.3 Charging Type

- 5.3.1 AC Charging (Level 1 and Level 2)

- 5.3.2 DC Charging

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Nordic

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Robert Bosch GmbH

- 6.3.3 Delta Electronics Inc.

- 6.3.4 Siemens AG

- 6.3.5 Tesla Inc.

- 6.3.6 ChargePoint Inc.

- 6.3.7 Enphase Energy, Inc.

- 6.3.8 Powercharge

- 6.3.9 Ampure

- 6.3.10 Exicom Tele-Systems Ltd

- 6.3.11 Schneider Electric SE

- 6.3.12 Eaton Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technology Advancement in the EV Charging Equipment

- 7.2 Need for a Robust EV Charging Network in the Emerging European Markets

02-2729-4219

+886-2-2729-4219

电动车充电站市场(含广告看板):依广告形式、充电器类型、安装位置、网路类型和最终用户划分,全球预测,2026-2032年电动车充电主动滤波器按充电站类型、滤波器配置、额定输出功率和最终用户划分,全球预测,2026-2032年电动车充电滤波器市场按滤波器类型、滤波器拓扑结构、额定电流、应用和最终用户划分-全球预测,2026-2032年电动车智慧充电控制器市场:按充电等级、模式、通讯技术、交付方式、车辆类型、应用和最终用户划分-2026-2032年全球预测

电动车充电站市场(含广告看板):依广告形式、充电器类型、安装位置、网路类型和最终用户划分,全球预测,2026-2032年电动车充电主动滤波器按充电站类型、滤波器配置、额定输出功率和最终用户划分,全球预测,2026-2032年电动车充电滤波器市场按滤波器类型、滤波器拓扑结构、额定电流、应用和最终用户划分-全球预测,2026-2032年电动车智慧充电控制器市场:按充电等级、模式、通讯技术、交付方式、车辆类型、应用和最终用户划分-2026-2032年全球预测 日本电动车充电设备市场占有率分析、产业趋势及统计、成长预测(2026-2031)

日本电动车充电设备市场占有率分析、产业趋势及统计、成长预测(2026-2031) 日本电动车充电设备市场规模、份额、趋势及预测(按充电站、最终用途和地区划分,2026-2034年)

日本电动车充电设备市场规模、份额、趋势及预测(按充电站、最终用途和地区划分,2026-2034年) 电动汽车家用充电套件市场预测至2032年:按充电器类型、连接器类型、车辆类型、安装类型、分销管道、应用和地区分類的全球分析

电动汽车家用充电套件市场预测至2032年:按充电器类型、连接器类型、车辆类型、安装类型、分销管道、应用和地区分類的全球分析 智慧电动汽车充电网路市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)超快速电动车充电(350kW+)系统市场机会、成长驱动因素、产业趋势分析及2025-2034年预测美国电动车 (EV) 充电:市场占有率分析、行业趋势和成长预测(2025-2030 年)

智慧电动汽车充电网路市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)超快速电动车充电(350kW+)系统市场机会、成长驱动因素、产业趋势分析及2025-2034年预测美国电动车 (EV) 充电:市场占有率分析、行业趋势和成长预测(2025-2030 年)

▼