|

市场调查报告书

商品编码

1640449

高可见度包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Highly Visible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

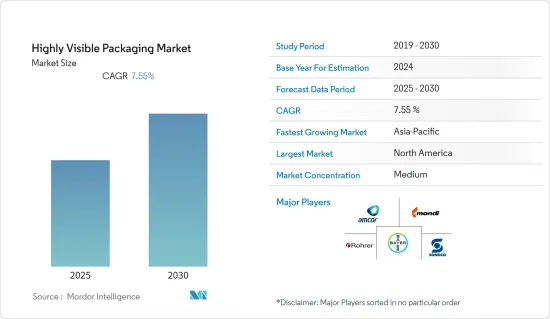

预计预测期内高能见度包装市场复合年增长率将达到 7.55%。

主要亮点

- > 高可见度包装具有高水准的保护性覆盖和防篡改功能,经久耐用,对产品製造商而言是一种有益的选择,并间接对消费者而言是一种有益的选择。在新冠肺炎疫情期间,餐厅专注于外带和送餐服务,并增加了显眼的一次性塑胶食品容器的使用。

- 高可见度包装对于製造业务而言是一种资产,因为快速识别产品可以带来更高的销售转换率。此外,它还可以让消费者在购买产品之前评估产品的视觉吸引力,帮助他们做出明智的决定。

- 方便食品的需求促使製造商使用更多高可见度的包装,因为易用性在客户的购买决策中起着关键作用。然而,随着所有包装需求中塑胶的使用量不断增加,包括 PE、HDPE、LLDPE、PP 和 LDPE,正逐渐迫使製造商选择可回收的替代品,从而提高其产品的知名度。

- 在为减缓电子商务成长而实施的封锁期间,电子商务的成长导致全球电子商务包装中使用的塑胶数量增加。对改善消费者开箱体验的关注导致了用于主要产品包装的高视觉性包装技术的兴起。

高可见度包装市场趋势

快速消费品占据很大市场占有率

- 快速消费品包装在饰面、尺寸、原材料和外观方面都具有创新性。

- 电子商务行业日益增长的需求正在塑造快速消费品包装设计市场。

- 这一类别的成长归因于对实用且可行的包装的需求不断增长,用于运送单一到小份产品以及便捷的快速消费品包装替代品。

- 消费者偏好的变化推动了包装材料的进步,包括产品可见度的提升。

- 食品包装变得如此重要,以至于消费者行销宣传活动经常将其作为产品的主要特征之一来强调,最终促进了高知名度包装市场的成长。

- 然而,快速变化的成本压力和更本地化的供应需求导致对高能见度包装的投资以塑胶和纸质包装类型为主。德国快速消费品企业汉高最近也报告了类似的趋势。

北美占据市场主导地位

- 食品和饮料行业的强劲成长迎合了时间紧迫的消费者的需求,便利商店和折扣店在该全部区域盛行,推动了快速消费品包装的成长。过去几年,美国对牛奶、起司和优格等乳製品的需求强劲。

- 为了减少包装废弃物,北美的製造商和客户越来越倾向于使用可生物降解、透明的包装,以便以环保的方式处理。这促使供应商进行创新并提供与传统包装技术相比产生更少废弃物的永续包装解决方案。

- 该地区的供应商可能会参与併购和创新包装发布,这可能会改变市场格局。

- 政府政策提高了营商规则和准则的透明度,食品加工产业已经成熟,包括生物基塑胶和热塑性塑胶在内的永续食品包装解决方案正在推出。

- 消费者意识到保持食品新鲜和健康的健康益处,而高度可见的包装有助于消费者的认知。该地区的工业研究和开发将带来创新的新产品和製造新产品的技术。

高能见度包装产业概况

预计高可见度包装市场的竞争格局将保持适中。然而,由于消费者意识的提高和对高可见度包装的需求,市场竞争预计将会加剧。公司正在投资开发透明和永续的包装。

- 2021 年 10 月—加拿大塑胶包装公司 Printex Transparent Packaging 推出了一系列全 PCR 聚对苯二甲酸乙二醇酯 (PET) 透明盒子。 Eco-PET 100 盒子可重复回收,并设计为原生 PET 的「合适」替代品。

- 2021 年 8 月 - Amcor 在亚洲和欧洲破土动工建设两个新工厂并启动了新计划,以扩大其全球网络,补充其现有的北美研发中心。

- 2021 年 11 月 - 安姆科硬包装 (ARP) 宣布技术进步,将能够在美国回收日之前回收数十亿个小瓶子。 ARP 以其可回收设计的包装而闻名,并不断寻找增加回收过程中所用材料数量的方法。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 市场驱动因素

- 确保安全的同时实现差异化

- 市场限制

- 增加占用空间和资源的密封工艺

第五章 市场区隔

- 按类型

- 翻盖包装

- 泡壳包装

- 收缩包装

- 开窗包装

- 塑胶容器和包装

- 玻璃容器

- 瓦楞纸箱

- 按最终用户产业

- 饮食

- 卫生保健

- 製造业

- 农业

- 服装与时尚

- 电子产品

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 新加坡

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲国家

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 科威特

- 卡达

- 南非

- 以色列

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 公司简介

- Amcor Limited

- Mondi Group

- Reynolds Group Holdings Limited

- Rohrer Corporation

- Bayer AG

- Sonoco Corporation

- Bemis Corporation

- Anchor Packaging

- Drug Package Inc.

- Imex Packaging

第七章投资分析

第 8 章:未来展望

简介目录

Product Code: 53084

The Highly Visible Packaging Market is expected to register a CAGR of 7.55% during the forecast period.

Key Highlights

- >

- Moreover, the capability to be durable, such as highly protective covering and tamper-proof, makes it a profitable option for product manufacturers and indirectly for consumers. During the COVID-19 pandemic, restaurants focused on take-away and food deliveries during lockdowns, increasing the use of high visibility single-use plastic food containers. This affected the studied market and led to an increase in sales.

- High-visibility packaging acts as an asset to manufacturing operations where quick product identification results in high sale conversion numbers. Moreover, it allows the consumer to assess the product's visual appeal before purchasing the product and helps them make an informed decision.

- The demand for convenience foods drives manufacturers toward using more high visibility packaging as ease of use plays a vital role in customer purchase decisions.

- High visibility packaging offers clarity to improve product identification and protection from damage and contamination. In the case of pharmaceutical packaging, it facilitates patient compliance with drug regimens and improves inventory control, distribution, and recordkeeping for health care providers and institutions.

- However, increasing the use of plastics like PE, HDPE, LLDPE, PP, LDPE, and others for all packaging needs is gradually compelling manufacturers to opt for recyclable alternatives, reducing product visibility.

- During the lockdowns that were imposed to slow down the spread of COVID-19, the increase in e-commerce increased the volume of plastics used in e-commerce packaging across the world. With an emphasis on better consumer unpacking experience, high visibility packaging techniques for primary packaging of products witnessed a rise.

Highly Visible Packaging Market Trends

FMCG Holds a Major Market Share

- FMCG packaging is innovative in terms of finishing, size, raw materials, and looks.

- Increasing demand for the e-commerce industry is creating a market for FMCG packaging design.

- The category section growth is attributed to the rising demand for practical and feasible packaging for delivering single-serve to small serve products along with the convenient FMCG packaging alternatives.

- Changing preferences of consumers are leading to advances in packaging materials, such as the visibility of the product.

- Food packaging has become so vital that it is often highlighted in consumer marketing campaigns as one of a product's essential features, which ultimately leads to the growth of the highly visible packaging market.

- However, with quickly changing cost pressures and more regional supply needs, the investment for high visibility packaging is centered on plastic and paper packaging types. Henkel, a player in the German FMCG sector, reported a similar trend recently.

The North American Region Dominates the Market

- The strong growth rate in the food and beverage industry toward time-pressed consumers and the prevalence of convenience and discount retailers throughout the region are attributed to the growth of FMCG packaging. In the past few years, the United States witnessed strong demand for dairy products, including milk, cheese, and yogurt.

- To reduce the waste from packaging materials, manufacturers and customers in North America increasingly prefer the use of bio-degradable see-through packaging materials that can be disposed of in an eco-friendly way. This will induce vendors to innovate and provide sustainable packaging solutions that result in less waste compared to the conventional packaging techniques.

- Vendors in the region are involved in M&As and innovative packaging launches, which are likely to change the market landscape.

- Government policies increase transparency in rules and guidelines for business, the presence of a well-established food processing industry, and the deployment of sustainable food packaging solutions, including bio-based plastics and thermoplastics.

- Consumer awareness about the health benefits of keeping food fresh and healthy, and highly visible packaging help consumers recognize it. More research and development in the region within Industry leads to innovative new products and technology to manufacture new products.

Highly Visible Packaging Industry Overview

The competitive landscape for the highly visible packaging market is expected to be moderate. However, with the rising consumer awareness and the need to have a highly visible package, the market competition is expected to rise. Companies are investing in developing clear and sustainable packages.

- October 2021 - The Canadian plastic packaging company Printex Transparent Packaging introduced a range of fully PCR polyethylene terephthalate (PET) clear boxes. The Eco-PET 100 boxes can be recycled repeatedly and are designed to serve as a 'suitable' replacement for virgin PET.

- August 2021 - Amcor started a new project, building two new sites in Asia and Europe to expand the global network complement existing innovation centers in North America.

- November 2021 - Amcor Rigid Packaging (ARP), in conjunction with America Recycles Day, announced a technological advancement that makes it possible for billions of small bottles to be recycled. ARP, known for its designed-to-be-recycled packaging, is always looking for ways to increase the amount of material that makes it to - and through - the recycling process.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Facilitate Differentiation While Maintaining Security

- 4.5 Market Restraints

- 4.5.1 Addition of Sealing Process that Consumes Space and Resources

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Clamshell Packaging

- 5.1.2 Blister Pack

- 5.1.3 Shrink Wrap

- 5.1.4 Windowed Packaging

- 5.1.5 Plastic Container Packaging

- 5.1.6 Glass Container

- 5.1.7 Corrugated Box

- 5.2 By End-user Industry

- 5.2.1 Food and Beverage

- 5.2.2 Healthcare

- 5.2.3 Manufacturing

- 5.2.4 Agriculture

- 5.2.5 Fashion and Apparels

- 5.2.6 Electronics and Appliances

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Singapore

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Kuwait

- 5.3.5.4 Qatar

- 5.3.5.5 South Africa

- 5.3.5.6 Israel

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor Limited

- 6.1.2 Mondi Group

- 6.1.3 Reynolds Group Holdings Limited

- 6.1.4 Rohrer Corporation

- 6.1.5 Bayer AG

- 6.1.6 Sonoco Corporation

- 6.1.7 Bemis Corporation

- 6.1.8 Anchor Packaging

- 6.1.9 Drug Package Inc.

- 6.1.10 Imex Packaging

7 INVESTMENT ANALYSIS

8 FUTURE OUTLOOK

02-2729-4219

+886-2-2729-4219

2025-2033 年复合包装市场规模、份额、趋势和预测(按材料、最终用途和地区)

2025-2033 年复合包装市场规模、份额、趋势和预测(按材料、最终用途和地区) 中国玻璃包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中国玻璃包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 包装帮浦和分配器:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

包装帮浦和分配器:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 德国包装产业:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

德国包装产业:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 法国包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)

法国包装:市场占有率分析、行业趋势和成长预测(2025-2030 年) 西班牙包装产业:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

西班牙包装产业:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 2030年防腐包装市场预测:按产品类型、材料、技术、应用和地区分類的全球分析

2030年防腐包装市场预测:按产品类型、材料、技术、应用和地区分類的全球分析 2024 年包装世界市场报告

2024 年包装世界市场报告 全球包装市场2025-2029

全球包装市场2025-2029 人口和人口结构对包装的影响:长期展望(至2050年)

人口和人口结构对包装的影响:长期展望(至2050年)

▼