|

市场调查报告书

商品编码

1642184

欧洲託管服务:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Europe Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

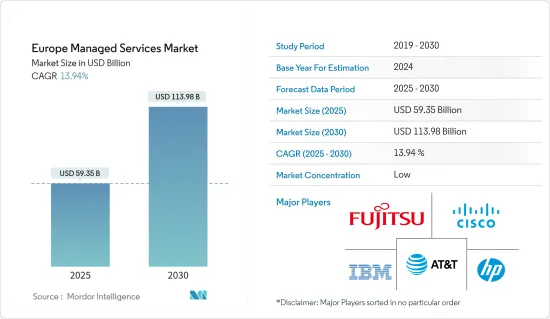

欧洲託管服务市场规模预计在 2025 年为 593.5 亿美元,预计到 2030 年将达到 1139.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 13.94%。

主要亮点

- 云端服务的日益普及、云端的多样化以及 IT 组织对最小化资本支出和最大化 IT 预算的追求等因素继续推动着所调查市场的成长。

- 人工智慧和云端管理满足各种功能业务需求和託管服务,帮助组织以较低的成本高效运行,而不会牺牲工作品质。主要市场参与企业正在投资创造新产品并实现产品多样化。我们也进行研究和开发,以提供可靠且实惠的服务。例如,2022年8月,野村综合研究所(NRI)公布了「NRI对产品开发的投资」。 NRI 在其丹麦分店开设了一个专用的託管服务室,以加强其在欧洲的託管服务。

- 欧洲是主要的汽车製造市场之一。近年来,汽车产业经历了剧烈变革,生产的汽车有望实现网联化、自动驾驶、按需化、共用和电动化。自动驾驶的出现带来了挑战,包括训练人工智慧和即时决策系统所需的大量资料。富士通等服务提供者提供的解决方案可以减少资料量并以分散的方式进行管理,仅收集相关资料。

- 此外,领先的公司正在欧洲建立公有云来支援他们的业务。例如,微软最近宣布计划在德国开设两个新的云端区域,使欧洲乃至世界各地的更多组织和公司能够利用公共云端解决方案实现数位转型。这些新区域提供 Microsoft Azure、Office 365 和 Dynamics 365 的全部功能、企业级安全性和其他功能,以协助客户满足其合规性和监管要求。

- 此外,物联网迫使企业重新评估客户获取资讯的方式并制定最能为他们服务的策略。每年都有数以百万计的新设备连接到互联网,这使得人们几乎不可能了解本已复杂的情况以及众多渠道带来的整合挑战和网路威胁。因此,託管服务供应商可以在此时提高物联网生态系统每一层的安全性,使企业能够利用物联网进行创新,并透过提供合格的资源和全天候支援服务来保持技术领先地位。

- 然而,儘管託管服务提供了显着的好处,但它们也伴随着固有的挑战,例如可靠性问题可能会阻碍预测期内的市场成长。聘请 MSP 来託管关键业务基础设施的过程需要有信心,即提供者的业务能够维持这种关係。如果供应商无法在市场上保持竞争力,依赖他们的企业可能会被迫更换整个网站寄存、电子邮件、日历和其他关键基础设施。

- 此外,此次疫情也暴露了各组织的灾害復原计画(DRP)和业务永续营运计画(BCP)中的缺陷。大多数计划都未能预见疫情,迫使各组织争相转移IT基础设施,以适应分散式远端劳动力。此次疫情凸显了监控技术和服务的重要性,以便在安全事件造成营运风险之前发现它们。因此,预计后疫情时期将为欧洲託管服务市场带来成长机会。

欧洲託管服务市场的趋势

云端领域预计将高速成长

- 随着该地区数位转型的进展,企业越来越依赖 IT 提供的创造性应用和增强功能来取得成功。这已成为大多数组织的关键竞争优势。此外,IT外包已不仅是一种削减成本的策略,还包括云端迁移和云端服务选项。因此,这种新形式是由业务成长、客户体验和竞争颠覆等组织动机所驱动的。

- 云端外包需求的不断增长表明欧洲公司更倾向于使用开源云端平台来储存资料。此外,在云端上营运的公司可能会担心安全威胁,并透过外包IT安全服务来消除任何威胁。这样,就需要供应商的专业知识,并且可以更容易委派责任。

- 据欧盟统计局称,近年来欧盟企业对云端处理的使用大幅增加。业内消息进一步表示,该地区对 IaaS 和 SaaS 的采用正在增长,从而推动了对混合云的需求。此外,欧盟的「数位十年」等多项区域措施也在推动市场的成长。 「数位十年」旨在到 2030 年将欧洲企业对云端运算技术的采用率提高到 75%。

- 自带设备 (BYOD) 和物联网 (IoT) 正在推动云端运算采用的成长。云端基础的解决方案主要被用来从物联网产生的资料中获取价值。这是由公有、私有和混合云模型支撑的。此外,公司的传统IT基础设施可能必须依靠云端来连接物联网设备。此外,企业也意识到公有和私有云端服务的一些缺点。公司正在寻找混合方法,以提供两种架构的优势,同时最大限度地减少每种模型的缺点。因此,出现了一种新趋势,即将在私有和公有系统上运行的两个或多个应用程式整合在一起 - 混合云託管服务。

- 此外,欧洲各国僱用 ICT 专业人员的公司比例不断增长,证明了欧洲对云端和混合IT基础设施的采用日益广泛。例如,根据丹麦统计局的数据,在丹麦,僱用 ICT 专业人员的公司比例将从 2016 年的 25% 增长到 2022 年的 34%。

託管安全占据主要市场占有率

- 为了保持竞争力,欧洲各地各种规模的企业越来越多地转向託管服务提供者。託管安全服务提供者透过提供正确的专业知识、解决方案和定价模式来增加其产品组合的价值。託管安全服务是该地区充满活力的商业领域中的新兴产业。服务提供者正在建立託管安全营运中心 (SOC) 来提供安全和支援服务。大多数服务提供者为其客户部署自己的整合安全管理平台,提供安全资讯和事件管理 (SIEM) 和其他监控解决方案。

- 由于技术发展导致网路安全威胁日益增加,各国政府正在对网路安全和 MSSP 进行投资。例如,根据 AAG IT Services & CyberSecurity 的数据,约有 39% 的欧洲公司将报告在 2022 年遭受网路攻击。

- 完全託管的託管服务包括伺服器安装和设定、根据客户要求安装已通过核准的软体、安全监控、软体更新和管理、资料备份和保护以及许多其他服务。德国许多公司,尤其是新兴企业和中小型企业,正在寻找这样的解决方案。这些服务为需要大量资金来维护和管理现场伺服器、需要合适的 IT 团队或因业务需求而时间紧迫的中小型企业提供了商业机会。

- 该地区资料外洩的增加预计将推动託管安全服务,并允许託管安全供应商开发新产品以获得市场占有率。例如,根据 TourShark 的数据,今年第三季度,俄罗斯在资料外洩方面居中欧和东欧 (CEE) 国家之首,洩漏记录超过 2,230 万条。乌克兰位居第二,黑山位居第三。

- 达梭系统等多家法国大型公司正在透过提供易于部署的打包解决方案(SaaS、PaaS、IaaS)并为新兴企业提供客製化服务,加强该国的新兴企业生态系统。法国政府决定利用 Orange Business Services 将非关键资料外包给外部云端。这是因为他们已经意识到使用云端运算的好处,云端运算非常适合容量波动(为政府提供了更快推出新服务所需的灵活性)。

欧洲管理服务业概况

欧洲託管服务市场较为分散,主要由拥有强大基本客群的国际公司主导。此外,随着公司采取强有力的竞争策略来维持市场地位并留住客户,竞争对手之间的竞争正在加剧。主要参与者包括富士通、IBM 和Cisco。

- 2024 年 1 月 - 商业 ISP 和託管服务提供商 Evolve 成为加入 MS3 位于英格兰北部的全新 10Gbps 光纤到户宽频网路的最新供应商,目标是到 2025年终连接英国各地的 535,000 户居民。 Asterion 的一项未指定的投资正在支持 MS3,它现在涵盖 158,779 个站点(119,139 RFS)并且正在迅速成长。透过与 MS3 的新合作,Evolve 将利用 MS3 的 XGS-PON 网络,率先酵母约克郡和剪切机地区的企业提供新解决方案。

- 2023 年 12 月 BT 和安全存取服务边缘 (SASE) 参与者 Netskope 宣布建立合作伙伴关係,向 BT 的全球客户提供 Netskope 市场领先的安全服务边缘 (SSE) 功能。此次伙伴关係是在几家大型客户部署之后达成的,两家公司曾共同努力满足大型企业的安全和存取需求。根据英国电信的资料,目前全球 76% 的劳动力青睐混合工作方式,需要更灵活、更安全的连接。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场动态

- 市场驱动因素

- 向混合 IT 的转变日益加剧

- 降低成本,提高业务效率

- 市场限制

- 整合和监管问题以及可靠性问题

第六章 市场细分

- 按部署

- 本地

- 云

- 按类型

- 託管资料中心

- 託管安全

- 管理通讯

- 主机网路

- 託管基础设施

- 管理行动性

- 按公司规模

- 中小型企业

- 大型企业

- 按行业

- BFSI

- 製造业

- 卫生保健

- 零售

- 其他行业

- 按国家

- 英国

- 德国

- 法国

- 其他欧洲国家

第七章 竞争格局

- 公司简介

- Fujitsu Ltd

- Cisco Systems Inc.

- IBM Corporation

- AT&T Inc.

- HP Development Company LP

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Nokia Solutions and Networks

- Deutsche Telekom AG

- Tata Consultancy Services Limited

- Citrix Systems Inc.

- Wipro Ltd

- NSC Global Ltd

- Telefonica Europe PLC

第八章投资分析

第九章 市场机会与未来趋势

The Europe Managed Services Market size is estimated at USD 59.35 billion in 2025, and is expected to reach USD 113.98 billion by 2030, at a CAGR of 13.94% during the forecast period (2025-2030).

Key Highlights

- Factors such as the growing adoption of cloud services, growth in cloud diversification, and the willingness of IT companies to minimize capital expenditure and make the most of their IT budgets continue to drive the growth of the studied market.

- Artificial technology and cloud management address various functional business requirements and managed services and assist with the efficient operation of the organization at a low cost without sacrificing the caliber of the work produced. The key market participants are making investments in the creation of new items and the diversification of their product offerings. They are also conducting research and development efforts to provide dependable and affordable services. For instance, in August 2022, Nomura Research Institute, Ltd. (NRI), a leading provider of system solutions and consulting services and system solutions, launched a dedicated managed services room at the NRI Europe Denmark Branch in order to enhance its system for providing managed services in Europe.

- The European region is among the leading automotive manufacturing markets. In recent years, the automotive industry has entered into a period of radical change, with the vehicles being produced expected to be connected, autonomous, shared on-demand, and electric. The emergence of autonomous driving will have challenges, including huge data volumes required for training AI and real-time decision-making systems. Service providers, like Fujitsu, offer solutions that will decrease data volumes and manage them in a distributed fashion, where only the relevant data is collected.

- Furthermore, major players are setting up public cloud setups in Europe to empower businesses. For instance, Microsoft recently announced its plans to deliver two new cloud regions in Germany to equip more organizations and companies in Europe and worldwide to transform them digitally with public cloud solutions. These new regions will offer Microsoft Azure, Office 365, and Dynamics 365 full functionality features, enterprise-grade security, and other features to help customers meet compliance and regulatory requirements.

- Additionally, IoT has forced companies to re-evaluate how customers access information and develop a strategy to best reach them. Millions of new gadgets connect to the Internet every year, making it practically impossible to understand the already complex landscape and the integration challenges and cyber threats provided by many channels. Hence, managed service providers can improve security for each tier of the IoT ecosystem at this point, enabling firms to harness IoT for innovation and stay on the cutting edge of technology by providing qualified resources and round-the-clock support services.

- However, despite the managed services providing excellent benefits, the specific challenges, like reliability concerns, may obstruct the market's growth over the forecast period. The process of hiring an MSP to host critical business infrastructure involves the belief that the providers' business may endure the relationship with them. In case of any failure by the providers to sustain the competition in the market, the enterprises relying upon them may have to entirely replace web hosting, emails, calendars, and other critical pieces of infrastructure, without which it is not possible to conduct business.

- Moreover, the pandemic has also revealed gaps in organizations' disaster recovery plans (DRP) and business continuity plans (BCP). Most of these plans could not address the pandemic, forcing organizations to scramble to transition their IT infrastructure to accommodate a distributed and remote workforce. The pandemic highlighted the importance of monitoring technology and services in detecting security incidents before they cause operational risk. Hence, the post-COVID period is anticipated to drive growth opportunities in the European managed services market.

Europe Managed Services Market Trends

Cloud segment is expected to grow at a higher pace

- With digital transformation in the region, organizations have become dependent on the success of creative applications and extensions that IT could provide. It has become a critical competitive edge for most organizations. Moreover, IT outsourcing has become more than a simple cost-reduction technique with cloud migrations and cloud service options. Therefore, this new form is driven by organizational motivations regarding business growth, customer experience, and competitive disruption.

- The increasing demand for cloud outsourcing indicates that European companies prefer cloud platforms from public sources for data storage purposes. Also, businesses operating over the cloud will likely be concerned about security threats and will eliminate all possible threats by outsourcing IT security services. This way, the demand for expert knowledge of the vendor will be required, along with an easy delegation of responsibilities.

- According to Eurostat, the use of cloud computing among EU enterprises increased significantly in recent years. Industry sources further suggest the increasing adoption of IaaS and SaaS in the European region, which in turn would increase the demand for hybrid cloud in the market. Furthermore, several regional initiatives such as EU's Digital Decade which to expand the use fo cloud-edge technologies among European businesses to 75% by 2030 also favors the studied market's growth.

- Bring-your-own-device (BYOD) and the Internet of things (IoT) have pushed the growth of cloud adoption, as cloud-based solutions are being leveraged primarily to derive value from the data generated by IoT. This is supported by the public, private, and hybrid cloud models. In addition, the legacy IT infrastructure of enterprises may have to rely on the cloud to connect with IoT devices. Besides, organizations realize several drawbacks of public and private cloud services. They are looking for a hybrid approach that provides advantages of both architectures, minimizing the drawbacks in each model. As a result, there is an emerging trend of integrating two or more applications running on private and public systems, i.e., hybrid cloud hosting services.

- Furthermore, the growing adoption of cloud and hybrid IT infrastructure in the European is also evident from the fact that the share of enterprises employing ICT specialists has been growing across various European countries. For instance, according to Statistics Denmark, in Denmark, the share of enterprises employing ICT specialists increased to 34% in 2022, compared to 25% in 2016.

Managed Security Account for Significant Market Share

- To maintain a competitive edge, organizations across Europe, irrespective of their sizes, increasingly rely on managed service providers to ensure technology usage to transform and scale businesses. Managed security service providers are adding value to their portfolio of offerings by providing the right expertise, solutions, and pricing models. Managed security service is an emerging field in the dynamic business space of the region. Service providers are setting up managed security operations centers (SOC) to deliver security and support services. Most service providers deploy their own unified security management platform for customers to provide security information and event management) and other monitoring solutions (SIEM).

- The growing cyber security threats due to the increase in the development of technologies have led the government to invest in cyber security and MSSP. For instance, according to AAG IT Services & Cyber Security, in 2022, about 39% of enterprises in Europe reported suffering a cyberattack.

- Fully managed to host services, including server installations and setup, approved software installations according to customer requirements, security monitoring, software updates and management, data backup and protection, and a slew of other services. Many enterprises in Germany, especially startups and SMEs, are looking for such solutions. These services offer the opportunity for SMEs that need more capital to keep and maintain their servers on-site, need an appropriate IT team, or are time-constrained due to the demands of their business operations.

- The rise in data breaches in the region is expected to drive the managed security services and enable managed security vendors to develop new products to capture the market share. For instance, according to tour shark, with over 22.3 million data breaches in the third quarter of the current year, Russia led all of Central and Eastern Europe (CEE) countries. Ukraine and Montenegro came in second and third, respectively.

- To empower the thriving startup ecosystem in the country, many French majors, like Dassault Systems, are offering packaged solutions (software-as-a-service (SaaS), platform-as-a-service, PaaS, and infrastructure-as-a-service (Iaas)) that can be easily deployed with tailored offerings for startups to augment growth. The French government decided to use the services of outsourcing non-critical data to an external cloud provided by Orange Business Services after realizing the benefits of using the cloud, which is perfectly suited to capacity fluctuations (thereby empowering the government with the flexibility required to implement new services more quickly).

Europe Managed Services Industry Overview

The Europe managed services market is fragmented as the market studied is dominated by international players with a strong client base. Additionally, companies are employing powerful competitive strategies to sustain themselves in the market and retain their clients, intensifying competitive rivalry. Key players are Fujitsu Ltd, IBM Corporation, Cisco Systems, etc.

- January 2024: Business ISP and managed service provider Evolve has become the latest provider to hop onto MS3's new 10Gbps capable Fibre-to-the-Premises broadband network in the North of England, aiming to reach 535,000 UK premises by the end of 2025. An unspecified investment from Asterion is backing MS3 and has covered 158,779 premises passed (119,139 RFS) and is rising fast. Evolve's new partnership with MS3 allows them to leverage MS3's XGS-PON network to bring new solutions to businesses in the East Riding and Lincolnshire regions for the first time.

- December 2023: BT and Netskope, a player in Secure Access Service Edge (SASE), announced a partnership to bring Netskope's market-leading Security Service Edge (SSE) capabilities to BT's global customers. The partnership follows several large customer implementations where the two companies have collaborated to meet the security and access needs of large enterprises successfully. BT's data shows that hybrid working is now a requirement for 76% of global workers, driving a requirement for more agile, secure connectivity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Restraints

- 5.2.1 Integration and Regulatory Issues and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small and Medium Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 Manufacturing

- 6.4.3 Healthcare

- 6.4.4 Retail

- 6.4.5 Other End-user Verticals

- 6.5 By Country

- 6.5.1 United Kingdom

- 6.5.2 Germany

- 6.5.3 France

- 6.5.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Development Company LP

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Nokia Solutions and Networks

- 7.1.10 Deutsche Telekom AG

- 7.1.11 Tata Consultancy Services Limited

- 7.1.12 Citrix Systems Inc.

- 7.1.13 Wipro Ltd

- 7.1.14 NSC Global Ltd

- 7.1.15 Telefonica Europe PLC

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2026年全球託管资讯服务市场报告

2026年全球託管资讯服务市场报告 託管服务市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和交付类型划分

託管服务市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和交付类型划分 DevOps转型服务市场:2026-2032年全球预测(按服务类型、组织规模、解决方案类型、部署类型、最终用户产业和通路划分)永续发展管理服务市场:依服务类型、服务模式、实施类型、永续发展重点领域和最终用户划分-2026-2032年全球预测

DevOps转型服务市场:2026-2032年全球预测(按服务类型、组织规模、解决方案类型、部署类型、最终用户产业和通路划分)永续发展管理服务市场:依服务类型、服务模式、实施类型、永续发展重点领域和最终用户划分-2026-2032年全球预测 託管服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)

託管服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年) 託管服务市场规模、份额和趋势分析报告:按解决方案、託管资讯服务、部署类型、企业规模、最终用途、地区和细分市场预测(2026-2033 年)

託管服务市场规模、份额和趋势分析报告:按解决方案、託管资讯服务、部署类型、企业规模、最终用途、地区和细分市场预测(2026-2033 年) 全球託管服务市场-产业规模、份额、趋势、机会和预测,按部署方式、类型、最终用户产业、地区和竞争格局划分(2021-2031 年预测)

全球託管服务市场-产业规模、份额、趋势、机会和预测,按部署方式、类型、最终用户产业、地区和竞争格局划分(2021-2031 年预测) 日本託管服务市场规模、份额、趋势及预测(按类型、部署模式、企业规模、最终用途和地区划分,2026-2034 年)

日本託管服务市场规模、份额、趋势及预测(按类型、部署模式、企业规模、最终用途和地区划分,2026-2034 年) 管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测

管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测 全球管理资讯服务市场

全球管理资讯服务市场