|

市场调查报告书

商品编码

1644284

日本低温运输物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Japan Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

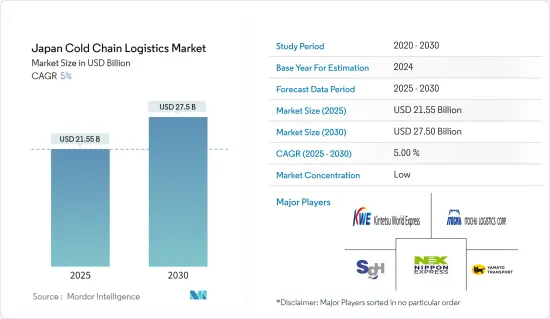

日本低温运输物流市场规模预计在2025年为215.5亿美元,预计到2030年将达到275亿美元,预测期内(2025-2030年)的复合年增长率为5%。

受新冠疫情影响,日本贸易工业部报告称,2020 年 3 月药局销售额较去年同期成长了 7.5%。对此,日本超级市场协会表示,为满足自我隔离和居家烹饪需求,2020年3月超级市场食品需求和销售额与去年同期相比成长了7.4%。这些因素都对日本低温运输物流市场产生了负面影响。新冠疫情对日本的低温运输业务产生了影响,包括人们对食品安全的担忧加剧。

日本被认为是低温运输物流的成熟市场,由多家参与企业主导。由于生物製药和再生医学的快速发展,日本近年来对药品冷链的需求不断增加。随着 COVID-19 疫苗和其他治疗方法的采用,预计这一趋势将持续下去。日本的低温运输物流最初是针对生鲜、冷藏和冷冻食品产业而建立的。低温运输物流注重始终在温度和湿度受控的环境中及时分销产品。

日本的冷藏仓库大多由大型低温运输公司拥有并经营,只有少数设施可供租赁。随着利用电子商务销售冷冻冷藏产品的不断进步,有潜在需求的地区将会加速建造冷藏仓库。

冷藏仓库数量的增加和医药行业的成长等因素预计将推动日本低温运输物流市场的成长。市场挑战包括冷藏能力分布不均、缺乏适当的物流连接支援以及需要高额的资本投入。

日本低温运输物流市场趋势

现代家庭推动冷冻食品需求

作为现代家庭的解决方案,随着老年人变得更加独立,双收入家庭和单人家庭的增加,对冷藏/冷冻食品的需求不断增加,同时也带来了食品浪费的风险以及食品和饮料行业劳动力短缺的日益加剧。

2021年日本冷冻食品消费量量约290万吨。日本生产的受欢迎的冷冻食品包括饺子、炸丸子和小麦粉麵条(乌龙麵)。近年来,日本食品特别是农产品在世界各地热销。

日本人口老化和向更健康寿命的转变正在推动冷冻食品的销售。超级市场、大卖场和药局的销售量也大幅增加。由于冷冻技术的进步和新冠疫情期间对居家食品的需求增加,日本的冷冻食品变得更加多样化。

名店的高价位家常小菜、道地的外国菜复製品等迅速占领市场,迫使百货商场、超级市场加速扩大销售面积。

日本製药业的成长

日本是世界上最大的医药市场之一,主要原因是其老化社会。在政府大力推广学名药的倡议下,该国也是先进医疗设备的主要生产国和进口国之一。

该国的生技药品领域仅次于美国。再加上政府重点支持低成本假冒产品,生物相似药存在着巨大的机会。日本为创新製药公司提供了慷慨的独占期,但在学名药的采用方面,该国正在赶上其他成熟市场。

国内药厂越来越多地在全球分销其产品,这也反映出人们对该体系的信心。随着主要企业海外销售比重稳定上升,对低温运输储运设施的需求也日益增加。人们对日本製药业兴趣日益浓厚的另一个关键驱动因素是需要加强日本的药物研发生态系统。

日本新冠肺炎感染人数不断上升,处方药和疫苗的需求也随之增加。这影响了药品需求。新冠疫苗进口增加推动了药品需求。例如,2021年5月,日本政府与辉瑞-BioNTech签署合同,将在2021年终进口1.94亿剂(133万美元)疫苗。据 IQVIA 称,2021 年日本处方药市场价值约为 10.6 兆日圆(800 亿美元),高于 2020 年的约 10.4 兆日圆(790 亿美元)。

日本低温运输物流产业概况

市场相对分散,拥有众多国内外参与企业,包括日本通运、大和号、佐川急便、伊藤忠物流公司和近铁世界快捷。市场竞争与成本、仓储费、空间和包装材料价格的上涨有关。服务供应商仍在努力发展其提供流程标准化的能力。缺乏有关储存温度和工作流程的标准化是该行业面临的另一个主要挑战。可用冷藏空间的品质和灵活性是一个值得关注的问题。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态与洞察

- 当前市场状况

- 市场动态

- 驱动程式

- 医疗领域的重要性

- 消费者对生鲜食品的需求不断增加

- 限制因素

- 包装不当或损坏的产品

- 温控混乱

- 机会

- 技术创新

- 驱动程式

- 技术趋势和自动化

- 政府法规和倡议

- 产业价值链/供应链分析

- 环境/温度控制储存亮点

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 排放标准和法规对低温运输产业的影响

- COVID-19 对市场的影响

第五章 市场区隔

- 按服务

- 贮存

- 运输

- 附加价值服务(速冻、标籤、库存管理等)

- 按温度类型

- 冷藏

- 冷冻

- 按应用

- 园艺(新鲜水果和蔬菜)

- 乳製品(牛奶、冰淇淋、奶油等)

- 肉类、鱼类、家禽

- 加工食品

- 製药、生命科学、化学

- 其他的

第六章 竞争格局

- 市场集中度概览

- 公司简介

- Nippon Express

- Yamato Holdings

- Sagawa

- Kintetsu World Express

- Itochu Logistics Corp.

- DHL

- Kuehne Nagel

- K line Logistics

- Nichirei Logistics Group, Inc.

- Sojitz Corporation

- CEVA Logistics

- Kokubu Goup

- Agility

- SF Express*

第七章 日本低温运输物流市场的未来

第 8 章 附录

The Japan Cold Chain Logistics Market size is estimated at USD 21.55 billion in 2025, and is expected to reach USD 27.50 billion by 2030, at a CAGR of 5% during the forecast period (2025-2030).

With COVID-19 in effect, the Japanese Trade Ministry reported a 7.5% Y-o-Y increase in the sale of drugstores in March 2020. Along with this, the Japan Supermarkets Association, in response to the self-imposed quarantines and the need to cook at home, reflected a 7.4% Y-o-Y increase in the demand and sales of groceries at the supermarkets in March 2020. All these factors led to a negative impact on the cold chain logistics market in Japan. COVID-19 impacted Japan's cold chain operations, including increased food safety concerns.

Japan is regarded as a mature market for cold chain logistics and is dominated by several players. Rapid advancements in biopharmaceuticals and regenerative medicine recently increased the demand for the cold pharmaceutical chain in Japan. This trend is expected to continue with the COVID-19 vaccines introduction and other treatments. Cold chain logistics in Japan was initially established for the fresh, refrigerated, and frozen food industries. Cold chain logistics focuses on the timely distribution of products within a constantly controlled temperature and humidity environment.

Most cold storage facilities in Japan are owned and operated by major cold chain corporations, with only a small number available for lease. Advances in using e-commerce to sell frozen and chilled goods will accelerate cold storage development in areas with latent needs.

Factors such as an increase in the number of refrigerated warehouses and growth in the pharmaceutical sector are expected to drive the growth of Japan's cold chain logistics market. Some of the challenges in the market are the irregular distribution of cold storage capacity, lack of proper logistical connectivity support, and the need for high capital investment.

Japan Cold Chain Logistics Market Trends

Modern Households Leading to Demand for Frozen Foods

The demand for chilled/frozen foods is increasing as a solution for modern-age families, such as independent elderly citizens, increase in dual-income households and single people, along with the danger of food loss and increasing overall labor shortages in the food and beverage industry.

In 2021, the consumption volume of frozen food in Japan amounted to about 2.9 million tons (USD 0.020 million tons). Popular frozen food products manufactured in Japan include dumplings (gyoza), croquettes, and wheat-flour noodles (udon). In recent years, Japanese food also exploded worldwide, especially agricultural products.

As the Japanese population ages, the shift to healthy life expectancy is a common desire of the people aiding the sale of frozen products. It also significantly increased in supermarkets, hypermarkets, and drugstores. Frozen food items in Japan became more diverse due to advances in refrigeration technology and growing demand for eat-at-home products amid the COVID-19 pandemic.

High-priced delicacies from well-known restaurants and authentic reproductions of food from abroad grew across the market, prompting department stores and supermarkets to speed up efforts to expand sales spaces.

Growth of Pharmaceutical Sector in Japan

Japan is one of the largest pharmaceutical markets in the world, primarily due to its aging population. It is also among the major producers and importers of advanced medical facilities backed by active government initiatives to promote generic drugs.

The country's native biologics sector is second after the USA. Coupled with the government's focus on supporting lower-cost copycat products, this entails a massive opportunity for bio-similars. While innovative drugmakers long benefited from generous exclusivity periods in Japan, the country is catching up with other mature markets regarding generics penetration.

The confidence in the system is reflected by the fact that domestic drugmakers are increasingly going global with their products. With the share of top Japanese companies' overseas sales rising steadily, the demand for cold chain storage and transportation facilities is also increasing. Another critical factor for increased interest in Japan's pharmaceuticals sector is the need to enhance Japan's drug discovery ecosystem.

The increased COVID-19 infection cases in the country increased the demand for prescription drugs and vaccines. It impacted the pharmaceutical product demand. The increasing import of COVID-19 vaccines increased the pharmaceutical product demand. For instance, in May 2021, the Japanese government signed a contract with Pfizer-BioNTech to import 194 million (USD 1.33 million)vaccine doses by the end of 2021. In 2021, the Japanese prescription drug market was valued at approximately JPY 10.6 trillion (USD 0.080 Trillion), up from about JPY 10.4 trillion (USD 0.079 Trillion) in 2020, according to IQVIA.

Japan Cold Chain Logistics Industry Overview

The market is relatively fragmented, with many local and international players, including Nippon Express, Yamato, Sagawa Express Co., Ltd, Itochu Logistics Corp., and Kintetsu World Express. The competition in the market pertains to costs, storage fees, and space, along with the rising prices of packing and packaging materials. The service providers are still working on developing the ability to provide standardization in the processes. Lack of standardization related to storage temperature and operating procedures are a few more significant challenges the industry faces. The quality and flexibility of available cold warehousing space are a considerable concern.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Criticality of the healthcare sector

- 4.2.1.2 Increased consumer demand for fresh foods

- 4.2.2 Restraints

- 4.2.2.1 Inadequate packaging or damaged products

- 4.2.2.2 Disrupted temperature control

- 4.2.3 Opportunities

- 4.2.3.1 Technological Innovations

- 4.2.1 Drivers

- 4.3 Technological Trends and Automation

- 4.4 Government Regulations and Initiatives

- 4.5 Industry Value Chain/Supply Chain Analysis

- 4.6 Spotlight on Ambient/Temperature-controlled Storage

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Emission Standards and Regulations on Cold Chain Industry

- 4.9 Impact of COVID - 19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.2 By Temperature Type

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.3 By Application

- 5.3.1 Horticulture (Fresh Fruits & Vegetables)

- 5.3.2 Dairy Products (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Meats, Fish, Poultry

- 5.3.4 Processed Food Products

- 5.3.5 Pharma, Life Sciences, and Chemicals

- 5.3.6 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Nippon Express

- 6.2.2 Yamato Holdings

- 6.2.3 Sagawa

- 6.2.4 Kintetsu World Express

- 6.2.5 Itochu Logistics Corp.

- 6.2.6 DHL

- 6.2.7 Kuehne Nagel

- 6.2.8 K line Logistics

- 6.2.9 Nichirei Logistics Group, Inc.

- 6.2.10 Sojitz Corporation

- 6.2.11 CEVA Logistics

- 6.2.12 Kokubu Goup

- 6.2.13 Agility

- 6.2.14 SF Express*

7 FUTURE OF JAPAN COLD CHAIN LOGISTICS MARKET

8 APPENDIX

全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年)

全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年) 冷链物流设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

冷链物流设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032

低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032 全球低温运输物流自动化市场:2032 年预测 - 按组件、温度范围、应用、最终用户和地区分析

全球低温运输物流自动化市场:2032 年预测 - 按组件、温度范围、应用、最终用户和地区分析 电动车、电气化与冷链运输:机会在哪里?

电动车、电气化与冷链运输:机会在哪里? 2025年低温运输全球市场报告2032 年低温运输物流市场预测:按类型、温度类型、应用和地区进行的全球分析2032 年水产品和生鲜产品农产品低温运输市场预测:按组件、温度类型、技术、应用、最终用户和地区进行的全球分析

2025年低温运输全球市场报告2032 年低温运输物流市场预测:按类型、温度类型、应用和地区进行的全球分析2032 年水产品和生鲜产品农产品低温运输市场预测:按组件、温度类型、技术、应用、最终用户和地区进行的全球分析 低温运输市场规模、份额、趋势分析报告:按类型、温度范围、应用、地区、细分市场预测,2025-2033 年

低温运输市场规模、份额、趋势分析报告:按类型、温度范围、应用、地区、细分市场预测,2025-2033 年