|

市场调查报告书

商品编码

1683536

欧洲电动车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)Europe EV Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

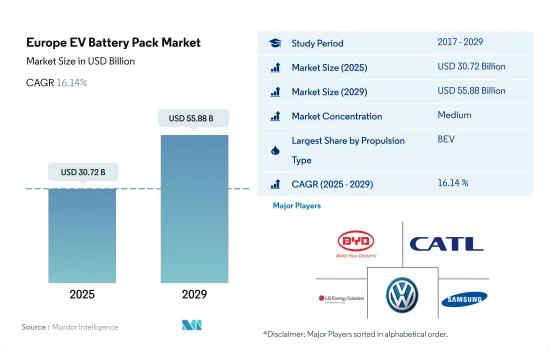

预计 2025 年欧洲电动车电池组市场规模将达到 307.2 亿美元,到 2029 年将达到 558.8 亿美元,预测期内(2025-2029 年)的复合年增长率为 16.14%。

受电动车需求成长推动,欧洲电动车电池组市场预计将实现 16.5% 的复合年增长率

- 在欧洲,政府奖励、更严格的排放法规和电池技术的进步正在推动纯电动车(BEV)和电动公车的采用强劲成长。根据欧洲替代燃料观察站的报告,2020年欧洲电动车数量将达到140万辆,其中纯电动车将占74%。欧洲电动公车市场也在成长,2017 年至 2022 年的复合年增长率为 16.2%。

- 电动车市场对电池组的需求不断增长,主要是由于电池密度和续航里程的增加以及电池成本的下降。电池技术正在迅速发展,锂离子电池的能量密度在过去十年中已经翻了一番,使得汽车一次充电就可以行驶更长的距离。电池成本也大幅下降,2010年至2020年,电动车锂离子电池的平均成本下降了89%,预计2030年将进一步降至58美元/度。固态电池也正在获得发展势头,丰田、福斯等公司都在大力投资这项技术。

- 预计预测期内(2023-2029 年),欧洲电动车电池组市场将大幅扩张。由于对电动车的需求不断增长,预计预测期内复合年增长率将达到 16.5%。更高的能量密度、更长的行驶里程以及更短的充电时间只是预计将推动行业成长的一些电池技术发展。未来电池组的回收和再利用机会预计也将非常丰富,进一步推动欧洲电池组市场的发展。

受政府激励措施和消费者意识增强的推动,法国和义大利的欧洲电动车电池组市场出现成长

- 欧洲电动车电池组市场是一个充满活力且不断成长的市场。随着电动车普及率的提高和电池组成本的下降,市场预计将继续成长。预计上述因素以及许多其他因素将在未来几年推动欧洲电动车电池组市场的成长。

- 德国是市场主要企业,多年来金额成长显着。这种增长归因于多种因素,包括政府对电动车的支持、消费者对电动车的需求不断增长以及电池技术的进步。德国强劲的汽车工业,加上主要汽车製造商对电动车生产的大量投资,是电池组需求激增的主要原因。

- 另一个欧洲主要国家法国的电池组市场也正在经历显着的成长。法国透过优惠政策和奖励鼓励电动车的应用的努力在推动电池组市场的成长方面发挥了重要作用。虽然义大利的成长速度与德国、法国相比有所放缓,但电池组市场仍处于上升趋势。消费者对电动车认识的不断提高、政府激励措施和技术进步等因素推动了义大利市场的成长。随着对电动车的需求不断增长,电池组预计将在支持义大利向永续交通转型方面发挥关键作用。

欧洲电动车电池组市场趋势

丰田集团引领欧洲电动车市场,其次是雷诺、特斯拉、起亚和宝马

- 欧洲电动车市场成长显着,参与者众多,但主要由五大公司推动,到2022年这五大公司将占据50%以上的市场份额,包括丰田集团、起亚汽车、雷诺、特斯拉、起亚汽车和大众。丰田集团是欧洲最大的电动车经销商,市占率约14.84%。该公司拥有强大的供应和分销网络,可满足其整个欧洲客户的需求和供应。雷诺在电动车市场提供了广泛的产品系列。

- 雷诺的市场占有率约为 7.47%,是欧洲第二大电动车销售商。雷诺拥有强大的品牌形象和强劲的财务状况。我们与日产等领先品牌建立了联盟和策略伙伴关係。特斯拉以6.71%的销量位居电动车第三名。特斯拉致力于尖端技术创新,与包括电池在内的电动车零件製造商建立了强大的策略合作伙伴关係。

- 起亚是欧洲第四大电动车销售商,市场占有率约 6.26%。该公司为不同类型的客户提供广泛的产品类型,并且与其他品牌相比,为每种预算提供多种选择。在欧洲电动车市场中排名第五的是BMW,市场占有率约为6.14%。其他在欧洲国家销售电动车的公司包括现代、宾士、宝马、奥迪和福特。

由于电动车在欧洲的广泛销售,特斯拉和雷诺将成为 2022 年电池组需求的最大贡献者。

- 过去几年,整个欧洲对电动车的需求急剧增长。电动车如今在欧洲道路上更为普遍。消费者对购买电动车的兴趣因地区和国家而异,但在德国和英国这两个最大的电动车市场,SUV 是最受欢迎的电动车类型。由于人们对舒适交通的兴趣日益浓厚,而且 SUV 比轿车拥有更大的内部空间,欧洲国家对电动 SUV 的需求超过了轿车。

- 欧洲各地消费者对紧凑型SUV的购买量正在急剧增加。特斯拉 Model Y 配备全马达、五星级 NCAP 安全认证、可容纳多达七名乘客的宽敞座位以及远距续航里程等特点。 2022年,它成为英国、德国等几个欧洲主要市场最受欢迎的车型之一。雷诺Arkana配备全混合动力发动机,由于其燃油效率和有竞争力的价格,获得了包括法国在内的多个欧洲国家客户的强烈销售反响。

- Captur 是雷诺 2022 年在欧洲国家最畅销的汽车之一,因为它提供混合动力和插电式混合动力传动系统,并配备了一系列吸引买家的功能。欧洲电动车市场还拥有一系列国际品牌的电动 SUV 和轿车。常见的汽车包括丰田雅力士和福特 Kuga,这两款车在 2022 年的销量强劲。欧洲电动车市场的其他竞争对手包括菲亚特 500 和丰田雅力士 Cross。

欧洲电动车电池组产业概况

欧洲电动车电池组市场正缓慢整合,前五大公司占据51.61%的市场。该市场的主要企业为:比亚迪股份有限公司、宁德时代新能源科技股份有限公司(CATL)、LG能源解决方案有限公司、上汽大众动力电池和三星SDI(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 电动汽车销售

- 电动车销量(按OEM)

- 最畅销的电动车车型

- 具有首选电池化学成分的OEM

- 电池组价格

- 电池材料成本

- 每种电池化学成分的价格表

- 谁供给谁?

- 电动车电池容量和效率

- 发布的电动车车型数量

- 法律规范

- 比利时

- 法国

- 德国

- 匈牙利

- 波兰

- 英国

- 价值链与通路分析

第五章 市场区隔

- 体型

- 公车

- LCV

- M&HDT

- 搭乘用车

- 推进类型

- BEV

- PHEV

- 电池化学

- LFP

- NCA

- NCM

- NMC

- 其他的

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 超过80度

- 少于15千瓦时

- 电池形状

- 圆柱形

- 包包

- 方块

- 方法

- 雷射

- 金属丝

- 成分

- 阳极

- 阴极

- 电解

- 分隔符

- 材料类型

- 钴

- 锂

- 锰

- 天然石墨

- 镍

- 其他材料

- 国家

- 法国

- 德国

- 匈牙利

- 义大利

- 波兰

- 瑞典

- 英国

- 其他欧洲国家

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 业务状况

- 公司简介

- BMZ Batterien-Montage-Zentrum GmbH

- BYD Company Ltd.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- Deutsche ACCUmotive GmbH & Co. KG

- Groupe Renault

- LG Energy Solution Ltd.

- Ningbo Tuopu Group Co. Ltd.

- NorthVolt AB

- Panasonic Holdings Corporation

- SAIC Volkswagen Power Battery Co. Ltd.

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- SVOLT Energy Technology Co. Ltd.(SVOLT)

- TOSHIBA Corp.

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

The Europe EV Battery Pack Market size is estimated at 30.72 billion USD in 2025, and is expected to reach 55.88 billion USD by 2029, growing at a CAGR of 16.14% during the forecast period (2025-2029).

The European electric vehicle battery pack market poised to record 16.5% CAGR, fueled by increasing BEV demand

- Europe has seen significant growth in the adoption of pure battery electric vehicles (BEVs) and electric buses driven by government incentives, stricter emissions regulations, and advancements in battery technology. According to a report by the European Alternative Fuels Observatory, the number of electric vehicles in Europe reached 1.4 million in 2020, with BEVs accounting for 74% of the total. The electric bus market in Europe also experienced growth, recording a CAGR of 16.2% from 2017 to 2022.

- The growing demand for battery packs in the electric vehicle market is driven by the increasing battery density and range and the declining battery costs. Battery technology has been evolving rapidly, and the energy density of lithium-ion batteries has already doubled over the past decade, allowing for longer ranges on a single charge. Battery costs have also declined significantly, with the average cost of lithium-ion batteries for electric vehicles declining by 89% from 2010 to 2020. The cost is expected to further decline to USD 58/kWh by 2030. The trend of solid-state batteries is also increasing, with companies such as Toyota and Volkswagen investing heavily in the technology.

- In the forecast period (2023-2029), the European market for electric vehicle battery packs is anticipated to expand significantly. It is anticipated to register a CAGR of 16.5% over the forecast period as a result of the rising demand for electric cars. Higher energy density, longer ranges, and quicker charging times are just a few of the battery technology developments that are anticipated to help the industry grow. Opportunities for recycling and reusing battery packs are also expected to abound in the future, further driving the battery pack market in Europe.

France and Italy experience growth in European electric vehicle battery pack market, fueled by government incentives and rising consumer awareness

- The European electric vehicle battery pack market is a dynamic and growing market. The market is expected to continue to grow in the coming years, driven by the increasing adoption of EVs and the declining cost of battery packs. In addition to the factors mentioned above, a number of other factors are expected to drive the growth of the European electric vehicle battery pack market in the coming years.

- Germany is a leading player in the market, having registered a remarkable increase in value over the years. This growth can be attributed to various factors, such as government support for electric vehicles, rising consumer demand for EVs, and advancements in battery technology. Germany's robust automotive industry, combined with substantial investments by major automakers in electric vehicle production, has significantly contributed to the surge in demand for battery packs.

- France, another prominent European country, has also witnessed notable growth in the battery pack market. France's commitment to promoting the adoption of electric vehicles through favorable policies and incentives has played a significant role in driving the growth of the battery pack market. While exhibiting slower growth compared to Germany and France, Italy has still experienced an upward trend in the battery pack market. Factors such as increasing consumer awareness of electric vehicles, government incentives, and technological advancements have contributed to the market's growth in Italy. As the demand for electric vehicles continues to rise, battery packs are expected to play a crucial role in supporting the transition toward sustainable mobility in Italy.

Europe EV Battery Pack Market Trends

TOYOTA GROUP LEADS THE EUROPEAN EV MARKET, FOLLOWED BY RENAULT, TESLA, KIA, AND BMW

- The market for electric vehicles in various European countries is growing significantly, with numerous players operating, but it is largely driven by five major companies, which held more than 50% of the market in 2022. These companies include Toyota Group, Kia, Renault, Tesla, Kia, and Volkswagen. Toyota Group is the largest seller of electric vehicles in Europe, accounting for around 14.84% share of the electric car market. The company has a strong supply and distribution network catering to the demand and supply of customers in various European countries. The company has a wide product portfolio offering in the EV market.

- Renault holds a market share of around 7.47%, making it the second-largest seller of electric vehicles across Europe. The company has a good brand image and a strong financial position. The company has alliances and strategic partnerships with good brands such as Nissan. The 3rd highest market share, 6.71%, for electric vehicle sales was recorded by Tesla. The business focuses on cutting-edge innovations and has solid strategic alliances with producers of several EV parts, including batteries.

- The 4th largest place in European EV sales is Kia, accounting for around 6.26% of the market share. The company has wide product offerings for various types of customers with various budget-friendly options compared to other brands. The 5th largest player operating in the European EV market is BMW, maintaining its market share at around 6.14%. Some of the other players selling EVs in various European countries include Hyundai, Mercedes-Benz, BMW, Audi, and Ford.

Tesla and Renault are the largest contributors to the demand for battery packs, as a result of the widespread sale of EVs in Europe in 2022

- The demand for electric vehicles has dramatically increased during the past several years in every part of Europe. Electric vehicles are now more prevalent on European roadways. Although consumer interest in buying electric vehicles varies by area and by country, SUVs are the most popular type of electric vehicle in Germany and the United Kingdom, the region's two biggest markets for electric vehicles. The demand for electric SUVs is outpacing that for sedans in various European countries due to the increased interest in comfortable transportation and the fact that SUVs are roomier than sedans.

- The number of compact SUVs purchased by consumers has increased dramatically across Europe. The Tesla Model Y offers a fully electric motor, a 5-star NCAP safety certification, spacious seating for up to 7 passengers, a long-range, and other features. It became one of the most popular models in several major European markets, including the United Kingdom and Germany, in 2022. The Renault Arkana provides a full hybrid engine, which has received a strong sales reaction from customers in several European nations like France due to its fuel efficiency and competitive pricing.

- Captur was one of the best sellers from Renault in the European countries in 2022, owing to its offering of a hybrid and a plug-in hybrid powertrain, and is packed with lots of features attracting buyers. The European EV market also features a variety of electric SUVs and sedans from various international brands. One of the common cars is the Toyota Yaris and Ford Kuga, which recorded good sales in 2022. Other cars in the European EV market that are in the competition include the Fiat 500 and Toyota Yaris Cross.

Europe EV Battery Pack Industry Overview

The Europe EV Battery Pack Market is moderately consolidated, with the top five companies occupying 51.61%. The major players in this market are BYD Company Ltd., Contemporary Amperex Technology Co. Ltd. (CATL), LG Energy Solution Ltd., SAIC Volkswagen Power Battery Co. Ltd. and Samsung SDI Co. Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 France

- 4.11.3 Germany

- 4.11.4 Hungary

- 4.11.5 Poland

- 4.11.6 UK

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Battery Chemistry

- 5.3.1 LFP

- 5.3.2 NCA

- 5.3.3 NCM

- 5.3.4 NMC

- 5.3.5 Others

- 5.4 Capacity

- 5.4.1 15 kWh to 40 kWh

- 5.4.2 40 kWh to 80 kWh

- 5.4.3 Above 80 kWh

- 5.4.4 Less than 15 kWh

- 5.5 Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 Method

- 5.6.1 Laser

- 5.6.2 Wire

- 5.7 Component

- 5.7.1 Anode

- 5.7.2 Cathode

- 5.7.3 Electrolyte

- 5.7.4 Separator

- 5.8 Material Type

- 5.8.1 Cobalt

- 5.8.2 Lithium

- 5.8.3 Manganese

- 5.8.4 Natural Graphite

- 5.8.5 Nickel

- 5.8.6 Other Materials

- 5.9 Country

- 5.9.1 France

- 5.9.2 Germany

- 5.9.3 Hungary

- 5.9.4 Italy

- 5.9.5 Poland

- 5.9.6 Sweden

- 5.9.7 UK

- 5.9.8 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BMZ Batterien-Montage-Zentrum GmbH

- 6.4.2 BYD Company Ltd.

- 6.4.3 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.4 Deutsche ACCUmotive GmbH & Co. KG

- 6.4.5 Groupe Renault

- 6.4.6 LG Energy Solution Ltd.

- 6.4.7 Ningbo Tuopu Group Co. Ltd.

- 6.4.8 NorthVolt AB

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 SAIC Volkswagen Power Battery Co. Ltd.

- 6.4.11 Samsung SDI Co. Ltd.

- 6.4.12 SK Innovation Co. Ltd.

- 6.4.13 SVOLT Energy Technology Co. Ltd. (SVOLT)

- 6.4.14 TOSHIBA Corp.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

高密度电动车电池组设计市场-策略洞察与预测(2026-2031年)

高密度电动车电池组设计市场-策略洞察与预测(2026-2031年) 电动汽车电池组市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

电动汽车电池组市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 东协电动车电池组:市场占有率分析、产业趋势与成长预测(2025-2030 年)中国电动车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)亚太地区电动汽车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)北美电动车电池组:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)印度电动车电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)德国电动车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)日本电动车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)法国电动车电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)

东协电动车电池组:市场占有率分析、产业趋势与成长预测(2025-2030 年)中国电动车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)亚太地区电动汽车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)北美电动车电池组:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)印度电动车电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)德国电动车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)日本电动车电池组:市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)法国电动车电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)