|

市场调查报告书

商品编码

1683991

印度除草剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030)India Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

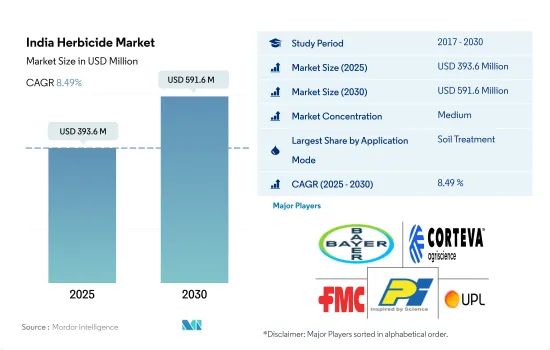

印度除草剂市场规模预计在 2025 年为 3.936 亿美元,预计到 2030 年将达到 5.916 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.49%。

除草剂应用最重要的主要方式是土壤处理应用。

- 杂草对印度农业部门构成重大威胁,每年造成约 45.0% 的作物损失。农民实施各种策略来控制杂草,包括轮作、耕作、人工除草和使用化学除草剂。

- 然而,替代方案带来的生产成本上升,导致更多农民采用化学除草剂来对抗作物中的杂草。透过使用除草剂,农民可以有效地控制杂草的生长,并最大限度地减少其对农业产量的负面影响。

- 除草的喷洒方法多种多样。使用除草剂进行土壤处理占据了很大的市场份额,因为它能够有效地在杂草生长的早期阶段进行控制。这种施用方法因其在抽穗前控制杂草的优势而受到种植谷类的农民的欢迎。

- 土壤处理包括将除草剂直接施用于土壤,有效地针对杂草种子和新生的幼苗,抑制它们的生长和建立。土壤处理使农民能够主动解决杂草问题并在关键的早期阶段促进作物健康生长。

- 除土壤处理外,叶面喷布喷洒和化学喷雾等其他除草方法也在该国迅速流行起来。这些模式已证明了其有效性,并在提高作物产量方面提供了多重益处。 2022 年,叶面喷布的市场占有率显着上升,为 33.2%,化学喷剂的市占率为 18.7%。

印度除草剂市场趋势

预计除草剂消耗量的增加将用于应对因作物损失增加而带来的杂草问题。

- 机械化和基于化学方法的除草方法正在迅速取代传统的手工除草方法。农民使用除草剂是一种经济有效的方式来控制小型和大型农业作业中的杂草。

- 在印度,农民实行作物集约化种植,即一年内多次重复作物週期,以提高作物产量。作物集约化种植往往会导致杂草压力增加,因此需要使用除草剂来维持作物的生产力。每公顷除草剂消费量平均为49.7公克/公顷。

- 每公顷除草剂的消费量取决于许多方面,例如作物类型、杂草侵染程度、农业实践和杂草管理策略。 2017 年至 2022 年,印度每公顷除草剂消费量增加了 6.0%。印度人均除草剂使用量增加,从而提高了每公顷平均农业产量。农民对除草剂益处的认识不断提高,加上市场上除草剂种类繁多,导致了除草剂使用量的增加。

- 具有耐除草剂特性的基因改造作物(如耐除草剂棉花(Bt棉))的出现,以及使用「Burnase/Burstar」技术进行基因改造的杂交芥菜(如DMH-11)的开发,使农民能够使用更广泛的除草剂来控制杂草。这些改良作物经过基因改造,能够耐受特定的除草剂,使农民能够更有效地控制杂草。

Atrazine、Paraquat和Glyphosate是印度使用的主要除草剂。

- 印度拥有多种多样的农业气候和土壤。不同的农业和耕作系统受到多种类型的杂草问题的困扰。杂草不仅影响产品品质、对健康和环境造成危害,还会造成作物产量损失10%至80%。Atrazine、Paraquat和Glyphosate是该国使用的主要除草剂。

- Atrazine是一种广泛用于印度玉米和水稻作物的除草剂,以控制稗草、刺苋属植物和苋菜等阔叶杂草和禾本科杂草。 2022年,该除草剂的价值为13,500美元。印度是世界上最大的莠Atrazine技术进口国,主要来自中国、义大利和以色列。

- Paraquat是一种广谱接触性除草剂,2022 年的市场价值为 4,600 美元。在印度,Paraquat二氯化物总合14 个商品名。它用于大约 25 种作物,包括谷物、豆类、油籽、蔬菜和经济作物。然而,中央杀虫剂委员会和登记委员会(CIBRC)仅核准在 9 种作物上使用该产品。

- Glyphosate是一种非选择性除草剂,用于控制狗牙根、白茅和野古草等杂草。根据印度政府2022年9月发布的通知,Glyphosate只能用于茶园和非农业用地。 2022 年其价值为 1,100 美元。

- 印度政府一直提供持续的预算支持,以促进农村经济发展并增加农民收入。 2022 财政年度预算提案并宣布了多项旨在改善农业部门和农村经济的政策和措施。预计这将对该国的除草剂价格产生进一步影响。

印度除草剂产业概况

印度除草剂市场适度整合,前五大公司占61.28%的市占率。市场的主要企业是:拜耳股份公司、科迪华农业科技、FMC 公司、PI Industries 和 UPL 有限公司(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 印度

- 价值炼和通路分析

第五章 市场区隔

- 执行模式

- 化学灌溉

- 叶面喷布

- 熏蒸

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

第六章竞争格局

- 主要策略趋势

- 市场占有率分析

- 商业状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Gharda Chemicals Ltd

- PI Industries

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001693

The India Herbicide Market size is estimated at 393.6 million USD in 2025, and is expected to reach 591.6 million USD by 2030, growing at a CAGR of 8.49% during the forecast period (2025-2030).

The primary mode of herbicide application of utmost significance is the soil treatment application

- Weeds pose a significant threat to the agricultural sector in India, resulting in substantial annual crop losses of around 45.0%. Farmers are implementing various strategies, including crop rotation, cultural practices, manual weeding, and spraying chemical herbicides to control weeds.

- However, due to rising production costs associated with alternative methods, more farmers are adopting chemical herbicides to tackle weeds in their crops. Farmers can efficiently control weed growth and minimize the detrimental effects on their agricultural yield by spraying herbicides.

- There are various application modes for weed control. Soil treatment using herbicides holds a prominent share due to its effectiveness in managing weeds during their early growth stages. This application method has gained popularity among farmers cultivating grain and cereal crops due to its advantageous effects in controlling pre-emergence weeds.

- Soil treatment involves applying herbicides directly to the soil, where they can effectively target weed seeds and emerging seedlings, inhibiting their growth and establishment. By employing soil treatment applications, farmers can proactively address weed issues and promote healthier crop growth in the crucial early stages.

- Following the soil treatment mode, other application modes such as foliar and chemigation have witnessed a surge in popularity for weed control in the country. These modes have demonstrated their effectiveness and offered various benefits in enhancing crop productivity. In 2022, foliar and chemigation registered a significant market share of 33.2% and 18.7%, respectively.

India Herbicide Market Trends

Herbicide consumption is anticipated to expand to manage the weed challenges due to growing losses of crops

- Mechanized and chemical-based weed control approaches are rapidly replacing traditional manual weeding methods. Farmers use herbicides as a cost-effective and efficient way to manage weeds in small-scale and large-scale farming operations.

- With the aim of increasing crop productivity, farmers in India have been practicing crop intensification, which involves repeated cropping cycles within a year. This intensification frequently results in increased weed pressure, necessitating the application of herbicides to maintain crop productivity. The average herbicide consumption per hectare accounted for 49.7 g/ha.

- Herbicide consumption per hectare can vary based on numerous aspects such as crop type, weed infestation level, agricultural practices, and weed management strategies. The consumption of herbicides in India per hectare increased by 6.0% from 2017 to 2022. Herbicide usage per capita in India increased to boost the average agricultural output per hectare. Farmers' growing awareness of the advantages of herbicides, along with the availability of a wide range of herbicides on the market, has contributed to their increased usage.

- The utilization of genetically modified (GM) crops that possess herbicide-tolerant characteristics, like herbicide-tolerant cotton (Bt cotton), and the development of hybridized mustard such as DMH-11 using the "barnase/barstar" technique for genetic modification has enabled farmers to employ herbicides more extensively in weed management. These modified crops are designed to endure specific herbicides, empowering farmers to utilize herbicides to a greater extent for effective weed control.

Atrazine, paraquat, and glyphosate are major herbicides used in the country

- India has a wide range of agroclimates and soil types. The highly diverse agriculture and farming systems are beset with different types of weed problems. Weeds cause 10% to 80% crop yield losses, besides impairing product quality and causing health and environmental hazards. Atrazine, paraquat, and glyphosate are major herbicides used in the country.

- Atrazine is an herbicide widely used to control broadleaf and grassy weeds like Echinocloa, Elusine spp, and Amaranthus viridis in maize and rice crops in India. The herbicide was valued at USD 13.5 thousand in 2022. India is the world's largest importer of Atrazine technical and imports majorly from China, Italy, and Israel.

- Paraquat is a broad-spectrum contact herbicide, accounting for USD 4.6 thousand in 2022. A total of 14 commercial names of paraquat dichloride are sold in India. It is used in about 25 crops, including cereals, pulses, oil seeds, vegetables, and cash crops. However, the Central Insecticide Board & Registration Committee (CIBRC) has approved its use in only nine crops.

- Glyphosate is a non-selective herbicide used to control weeds like Cynodon dactylon, Imperata cylindrica, and Arundinella bengalensis. As per the notice issued by the Government of India in September 2022, glyphosate can be used only in tea gardens and non-crop areas. It was valued at USD 1.1 thousand in 2022.

- The Government of India has continuously provided budgetary support to revive the rural economy and increase farmers' income. A number of measures and initiatives were proposed and announced during the FY22 budget for the improvement of the agriculture sector and the rural economy. This is expected to influence the prices of herbicides in the country further.

India Herbicide Industry Overview

The India Herbicide Market is moderately consolidated, with the top five companies occupying 61.28%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, PI Industries and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Gharda Chemicals Ltd

- 6.4.7 PI Industries

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2025年全球不织布除草布市场报告

2025年全球不织布除草布市场报告 2032 年Paraquat市场预测:按产品类型、作物类型、应用、最终用户和地区进行的全球分析2032 年除草剂市场预测:按产品类型、应用、最终用户和地区进行的全球分析

2032 年Paraquat市场预测:按产品类型、作物类型、应用、最终用户和地区进行的全球分析2032 年除草剂市场预测:按产品类型、应用、最终用户和地区进行的全球分析 2025 年至 2033 年除草剂市场规模、份额、趋势及预测(按类型、作用方式、应用和地区)2025年全球智慧除草市场报告2025年除草剂全球市场报告

2025 年至 2033 年除草剂市场规模、份额、趋势及预测(按类型、作用方式、应用和地区)2025年全球智慧除草市场报告2025年除草剂全球市场报告 磺酸盐市场分析与预测(至2034年):类型、产品、应用、技术、最终用户、形式、部署、材料类型、功能杂草控制市场:按控制方法、按应用领域、按杂草类型、按最终用户、按地区

磺酸盐市场分析与预测(至2034年):类型、产品、应用、技术、最终用户、形式、部署、材料类型、功能杂草控制市场:按控制方法、按应用领域、按杂草类型、按最终用户、按地区 磺酸盐市场报告:趋势、预测与竞争分析(至 2031 年)

磺酸盐市场报告:趋势、预测与竞争分析(至 2031 年) 中国除草剂市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

中国除草剂市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

▼