|

市场调查报告书

商品编码

1684055

美国MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)United States MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

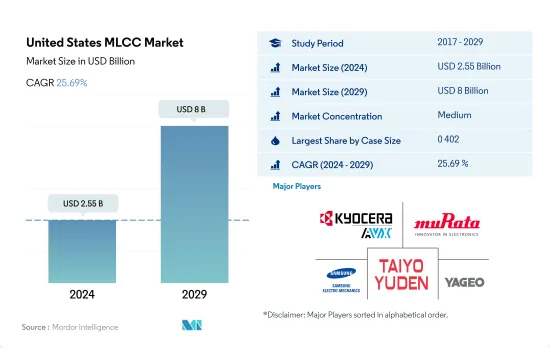

预计2024年美国MLCC市场规模为25.5亿美元,2029年将达到80亿美元,预测期内(2024-2029年)的复合年增长率为25.69%。

0201型MLCC的主要成长要素之一是消费者对新技术的认识不断提高。

- 0201 外壳尺寸领域将成为领跑者,到 2022 年将占据最大的市场占有率,达到 22.29%,其次是 0402,占 22.22%,0603,占 21.94%。

- 持续的小型化趋势加上对更高组件密度的需求正在推动对这些组件的需求。可携式和连网型设备的日益普及也推动了对 0201 MLCC 元件的需求。美国有几家着名的笔记型电脑製造商和跨国公司在该市场上占有重要地位。对视讯会议、虚拟协作工具和线上教育日益增长的需求正在刺激笔记型电脑的销售。

- 01005 MLCC 具有广泛的应用,尤其是在智慧型手机、穿戴式装置和物联网装置等小型电子设备中,使製造商能够在不影响效能的情况下实现时尚紧凑的设计。在美国,5G网路的快速推出正在推动对智慧型手机的需求。

- 0402 外壳类型是表面黏着技术陶瓷电容器广泛采用的外形规格。汽车产业在各种应用中都依赖 0402 MLCC,包括引擎控制单元、资讯娱乐系统和 ADAS。这些电容器在恶劣的汽车环境中提供可靠的性能。在北美,由于人们越来越关注车辆安全、对车辆舒适性的需求不断增长,以及车主越来越希望在发生事故时减少人为错误,自动驾驶汽车的需求正在增长。

美国MLCC市场趋势

第三方物流供应商的发展可能会刺激轻型商用车的需求

- 轻型商用车(LCV)市场主要受电子商务和物流行业推动。随着越来越多的人可以使用网路和智慧型手机,网路零售和电子商务正在兴起。预计轻型商用车的购买量将会增加,有利于更快地向客户交付货物。 2019年该国产量为803万辆。

- 新冠疫情和俄乌战争导致行动和运输限制的程度和类型空前,导致产量与前一年同期比较下降了17.17%。封锁和其他限制措施为商用车产业的供应链带来了前所未有的挑战。排放法规的收紧、车辆安全性的提高、汽车驾驶辅助系统以及零售和电子商务领域物流的爆炸性增长都刺激了对新型创新商用车的需求。

- FedEx、UPS、DHL等第三方物流供应商使用各种轻型货车将产品运送到最近的产品配送站。小型轻型商用车在城市通勤时比大型商用车消费量更少的燃料,这就是这些公司增加轻型商用车持有的原因。为了应对气候变迁和城市污染,大型物流营运商开始用电动和低排放气体汽车取代持有内燃机车队。例如,联邦快递于2021年12月宣布了一项全球目标,即到2025年实现其新购车辆50%为电动车,到2030年实现100%的电动车化。联邦快递致力于透过其配送车队的电气化,到2040年实现全球碳中和,这是其投资的重点领域。

美国消费者对安全性的要求越来越高,这推动了乘用车的需求。

- 美国是全球最大的汽车市场之一,乘用车产量位居全球第八,2019年产量为250万辆。

- 受新冠疫情影响,产量大幅下降,与前一年同期比较去年同期下降24%。乘用车维修活动也大幅下降。车辆限行措施的放鬆,有望带动私家车使用量激增,带动乘用车消费復苏。

- 美国乘用车产量达到 172 万辆,因为一些OEM表示有兴趣增加生产能力以满足日益增长的电动车需求。政府禁止内燃机汽车的政策也促进了电动车的销售。此外,由于各种原因,全球汽油和柴油价格上涨也使电动车製造商更容易增加销售量。第三大市场美国的电动车销售量预计将在2022年成长55%,销售份额达8%。

- ICE车型的销量一直在稳步下降。 2022 年美国可用的 ICE 选项数量将比 2016 年减少 3% 至 4%。美国电动车销量的成长归因于多种因素。除了OEM提供的型号之外,还有更多型号可供选择,这将有助于填补供应缺口。

- 美国是第二大 FCEV 保有量国家,持有超过 15,000 辆 FCEV。其中大部分是燃料电池汽车。 2022年美国FCEV保有量将成长20%以上。这些关键因素正在推动乘用车生产的需求,并预计其需求将持续成长。

美国MLCC产业概况

美国MLCC市场适度整合,前五大企业占41.51%。市场的主要企业有:京瓷AVX元件株式会社(京瓷株式会社)、村田製作所、三星电机、太阳诱电和国巨株式会社。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 价格趋势

- 铜价走势

- 镍价趋势

- 油价趋势

- 锌价趋势

- 家电销量

- 空调销售

- 桌上型电脑销量

- 游戏机销售

- 笔记型电脑销售

- 冰箱销售

- 智慧型手机销量

- 仓储设备销售

- 平板电脑销量

- 电视销售

- 汽车製造

- 重型卡车生产

- 轻型商用车生产

- 乘用车生产

- 汽车产量

- 电动汽车生产

- BEV(纯电动车)生产

- PHEV(插电式混合动力汽车)产量

- 工业自动化销售

- 工业机器人销售

- 服务机器人销售

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 介电类型

- 1级

- 2级

- 錶壳尺寸

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- 其他的

- 电压

- 500V~1000V

- 小于500V

- 1000V以上

- 电容

- 100uF~1,000uF

- 小于100uF

- 超过 1,000uF

- Mlcc安装类型

- 金属盖

- 径向引线

- 表面黏着技术

- 最终用户

- 航太和国防

- 车

- 家用电子电器

- 工业设备

- 医疗设备

- 电力和公共产业

- 通讯设备

- 其他的

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第 7 章 CEO 的关键策略问题CEO 的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50002001

The United States MLCC Market size is estimated at 2.55 billion USD in 2024, and is expected to reach 8 billion USD by 2029, growing at a CAGR of 25.69% during the forecast period (2024-2029).

Increasing awareness among consumers about the emergence of novel technologies among the primary growth drivers of 0201 MLCCs

- The case size 0201 segment emerged as the frontrunner, capturing the largest market share of 22.29%, followed by 0402, with 22.22%, and 0603, with 21.94%, in terms of volume in 2022.

- The ongoing trend of miniaturization, coupled with the need for higher component density, drives the demand for these components. The increasing popularity of portable and connected devices further contributes to the demand for 0201 MLCC components, enabling manufacturers to achieve compact designs without compromising performance. The United States is home to several prominent laptop manufacturers and multinational companies with a significant presence in the market. The increased need for video conferencing, virtual collaboration tools, and online education has accelerated laptop sales.

- The usage of 01005 MLCCs spans diverse applications, particularly in compact electronic devices such as smartphones, wearables, and IoT devices, enabling manufacturers to achieve sleek and compact designs without compromising performance. Smartphones are in high demand in the United States due to the rapid adoption of the 5G network.

- The 0402 case type is widely adopted as a form factor for surface-mount ceramic capacitors. The automotive industry relies on 0402 MLCCs for various applications, including engine control units, infotainment systems, and ADAS. These capacitors provide reliable performance in harsh automotive environments. The demand for autonomous vehicles is rising in North America due to the increased focus on automotive safety, the rise in demand for comfort features in a vehicle, and a growing desire of vehicle owners to reduce the amount of human error in case of accidents.

United States MLCC Market Trends

The development of third-party logistic providers may propel the demand for light commercial vehicles

- The market for light commercial vehicles (LCVs) is primarily driven by the e-commerce and logistics industries. As more people have access to the Internet and smartphones, online retail sales and e-commerce have been increasing. Purchases of LCVs are anticipated to increase, thereby facilitating quick delivery of items to customers. The country produced 8.03 million units in 2019.

- The COVID-19 pandemic and the Russia-Ukraine War resulted in unprecedented levels and types of mobility and transportation restrictions, resulting in a 17.17% Y-o-Y drop in production. Lockdowns and other restrictions caused previously unheard-of problems in the commercial vehicle industry's supply chain. Tightening emissions regulations, vehicle safety improvements, driver-assist systems in cars, and the explosive growth of logistics in the retail and e-commerce sectors have all fueled demand for new and innovative commercial vehicles.

- Third-party logistic providers, such as FedEx, UPS, and DHL, use a variety of LCVs to transport products to the nearest product delivery station. These businesses have a larger fleet of LCVs because smaller LCVs use less fuel than heavy commercial vehicles when commuting within a city. To combat climate change and city pollution, big logistics operators have started replacing their fleets of combustion engines with electric or low-emission vehicles. For instance, in December 2021, FedEx announced a global target to make 50% of all newly purchased vehicles electric by 2025, rising to 100% for the new fleet by 2030. By 2040, FedEx wants to achieve global carbon neutrality through the electrification of pickups and delivery vehicles as a significant investment area.

Customers in the United States are demanding higher safety, which is propelling the demand for passenger vehicles

- The United States has one of the largest automotive markets in the world and ranks 8th in the production of passenger cars, producing 2.5 million units in 2019.

- Post the COVID-19 outbreak, there has been a major decline in production, registering a Y-o-Y drop of 24%, along with a decline in the usage of personal vehicles for commuting. Maintenance activities of passenger vehicles have significantly declined. With the ease of lockdown measures, there has been a surge in the usage of personal vehicles, which may drive the recovery of passenger vehicle consumption.

- The production of passenger vehicles in the United States reached 1.72 million units as several OEMs became interested in increasing their production capacity to meet the growing demand for electric vehicles. The government policy of banning ICE engines helped boost the sales of electric vehicles. The increase in the price of gasoline and diesel due to various global reasons has also made it easy for EV companies to boost their sales. Electric car sales in the United States, the third largest market, increased by 55% in 2022, reaching a sales share of 8%.

- Sales of ICE models have been steadily decreasing. The number of available ICE options was 3% to 4% lower in the United States in 2022 than in 2016. Several factors help increase sales of electric cars in the United States. More available models beyond those offered by OEMs help close the supply gap.

- The United States holds the second largest FCEV stock, with over 15,000 FCEVs. Most of these are fuel-cell cars. In 2022, the stock of FCEVs in the United States increased by more than 20%. These key elements fuel production demand for passenger vehicles and are expected to increase in the future.

United States MLCC Industry Overview

The United States MLCC Market is moderately consolidated, with the top five companies occupying 41.51%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Price Trend

- 4.1.1 Copper Price Trend

- 4.1.2 Nickel Price Trend

- 4.1.3 Oil Price Trend

- 4.1.4 Zinc Price Trend

- 4.2 Consumer Electronics Sales

- 4.2.1 Air Conditioner Sales

- 4.2.2 Desktop PC's Sales

- 4.2.3 Gaming Console Sales

- 4.2.4 Laptops Sales

- 4.2.5 Refrigerator Sales

- 4.2.6 Smartphones Sales

- 4.2.7 Storage Unit Sales

- 4.2.8 Tablets Sales

- 4.2.9 Television Sales

- 4.3 Automotive Production

- 4.3.1 Heavy Trucks Production

- 4.3.2 Light Commercial Vehicles Production

- 4.3.3 Passenger Vehicles Production

- 4.3.4 Total Motor Production

- 4.4 Ev Production

- 4.4.1 BEV (Battery Electric Vehicle) Production

- 4.4.2 PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.5 Industrial Automation Sales

- 4.5.1 Industrial Robots Sales

- 4.5.2 Service Robots Sales

- 4.6 Regulatory Framework

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 500V to 1000V

- 5.3.2 Less than 500V

- 5.3.3 More than 1000V

- 5.4 Capacitance

- 5.4.1 100µF to 1000µF

- 5.4.2 Less than 100µF

- 5.4.3 More than 1000µF

- 5.5 Mlcc Mounting Type

- 5.5.1 Metal Cap

- 5.5.2 Radial Lead

- 5.5.3 Surface Mount

- 5.6 End User

- 5.6.1 Aerospace and Defence

- 5.6.2 Automotive

- 5.6.3 Consumer Electronics

- 5.6.4 Industrial

- 5.6.5 Medical Devices

- 5.6.6 Power and Utilities

- 5.6.7 Telecommunication

- 5.6.8 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

用于MLCC电极的镍浆(<200nm)—全球市场份额和排名、总收入和需求预测(2025-2031年)MLCC镍内电极膏:2025-2031年全球市占率排名、总销售额及需求预测

用于MLCC电极的镍浆(<200nm)—全球市场份额和排名、总收入和需求预测(2025-2031年)MLCC镍内电极膏:2025-2031年全球市占率排名、总销售额及需求预测 MLCC-市场占有率分析、产业趋势与统计、成长预测(2024-2029)个人电脑和笔记型电脑用 MLCC——市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中压MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)中国MLCC市场占有率分析、产业趋势与统计、成长预测(2025-2030年)亚太地区MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)北美MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)印度MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)工业MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

MLCC-市场占有率分析、产业趋势与统计、成长预测(2024-2029)个人电脑和笔记型电脑用 MLCC——市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中压MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)中国MLCC市场占有率分析、产业趋势与统计、成长预测(2025-2030年)亚太地区MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)北美MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)印度MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)工业MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

▼