|

市场调查报告书

商品编码

1686521

託管服务 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

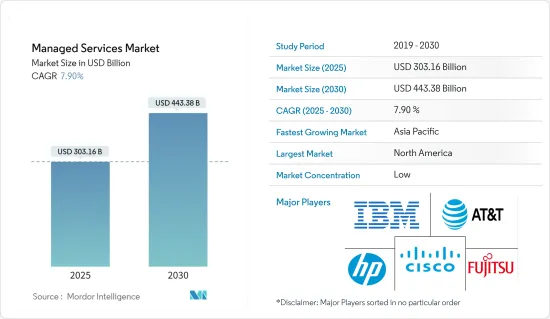

託管服务市场规模预计在 2025 年达到 3,031.6 亿美元,预计到 2030 年将达到 4,433.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.9%。

随着越来越多的中小型企业考虑外包非核心业务,中小型企业(SMB)有望成为对市场成长产生正面影响的驱动力。据 Datto 称,平均每个 MSP 有 122 个客户,大约 60% 的 MSP 客户拥有 1 至 150 名员工。此外,只有 5% 的 MSP 拥有员工人数超过 500 人的客户。

主要亮点

- 託管服务提供了一系列好处,并被证明可以透过让组织专注于其核心专业知识对发展产生积极影响。据估计,成功实施託管服务可以降低25-45%的IT成本,并提高45-65%的业务效率。此外,根据智慧技术解决方案的调查,25% 的公司表示,停机平均每小时造成 301,000 美元至 40 万美元的损失。

- 此外,预测到2022年,开发与发展速度相符的应用程式将变得非常重要。应用程式维护和支援服务是 IT 託管服务的重要组成部分。应用程式效能监控(APM)有望为开发人员提供快速回馈机制。前端监控(使用者行为调查)、ADTD(应用程式发现、追踪和诊断)和 AIOps 分析(应用程式生命週期模式和异常检测)都是 APM 的一部分。这些解决方案可协助 DevOps 团队更好地分析业务问题。这减少了平均修復时间(MTTR)。

- 随着行业要求、标准和消费者需求每天都在变化,企业要求以结果为导向的成果。这些公司要求预先定义或预期的标准能够被清楚地记录下来并即时交付。 MSP 将使用进阶分析和彙报来描述部署技术的影响并提供基于事实的资料。

- 此外,区块链和物联网技术将为託管服务提供者创造更好的机会。为了抓住这些机会、保持相关性并跟上竞争的步伐,託管服务供应商正在越来越多地掌握这些技术所需的技能,以及 AR、VR 和 AI 等其他颠覆性技术。

- 自新冠疫情爆发以来,企业采用的远距工作模式导致云端基础的解决方案的需求激增。随着越来越多的 IT 决策者希望利用现代云端环境,计划耗时更长,所需的预算也更大。据 Wanclouds 称,美国和英国近一半(48%)的 IT 决策者表示,成功迁移单一多重云端应用程式的平均时间为一到两个月。

託管服务市场趋势

製造业预计将占据较大的市场占有率

- 在当今科技主导的商业环境中,巨量资料已成为提高製造业生产力和效率的关键驱动力之一。感测器和连网型设备的广泛采用,实现了 M2M通讯,导致製造业产生的资料点数量显着增加。

- 各行各业正在快速转型为智慧产业,资料可以即时产生和视觉化。从说明到预测性的分析技术的进步使业界能够从这些丰富的资料中获得利益。製造业的座右铭正在转向基于指标的领域,在该领域中,可以基于资料驱动的统计数据利用来改善决策。

- 随着工业 4.0 概念影响製造生产设施,製造业产生的资料量正在滚雪球般增长,因为现在可以从各个製程点(例如温度、压力、湿度、应力、应变、品质等)建立资料。

- 一些应用范例是在半导体、消费性电子和汽车行业,这些行业製造商需要监控大量变数以确保最终产品的品质。巨量资料分析已成为传统方法的有效解决方案。

- 许多中小型製造企业将这些巨量资料分析解决方案外包,因为他们专注于硬体设备,缺乏软体解决方案的专业知识。外包软体服务正在进一步减少开支。预计在预测期内,现场服务管理和 ERP 等其他软体服务的外包将促进託管服务的发展。

亚太地区可望成为成长最快的市场

- 数位转型已成为中国的首要任务,随着越来越多的公司製定正式策略来支持这项工作,数位转型正在迅速加速。 2021年1月,中国国务院发布了「十四五」规划(2021-2025年)期间推动数位经济蓬勃发展的建议。根据规划,2025年,我国产业数位转型将迈上新台阶,数位公共服务更加完善,数位经济管治结构明显改善。

- 中国的託管服务供应商致力于跟上最新技术,以降低安全风险并优化最终用户的业务。该国的电信业者主要服务託管服务市场。这些公司也策略性地收购託管服务公司,以占领更多的市场占有率。

- 此外,由于产业技术的快速发展,印度银行业正经历巨大的变化,导致各组织采用云端处理服务来应对挑战。此外,印度託管储存供应商正在投资开发专门针对 BFSI 领域的整合式云端储存平台。

- 此外,印度政府继续对智慧城市等实体基础设施进行大量投资,预计这将为资料储存、安全性和网路管理等託管服务的部署创造机会。目前,印度的智慧城市计画专注于改造100座城市。

- 2022 年 1 月,毕马威印度公司和 Qualys 宣布建立合作伙伴关係,将 Qualys 解决方案加入毕马威的託管安全服务。毕马威在印度业界领先且全球认可的网路安全服务,与 Qualys 世界一流的网路安全创新相结合,将使企业能够保护其网路、应用程式、端点和云端工作负载免受安全漏洞的侵害,提供可见性并确保合规性。

- 而服务业在GDP中所占比重最大的日本,在服务业管理方面也共用。日本一直是市场经济,是世界第二已开发经济体。目前,日本正专注于发展混合动力汽车、机器人、光学设备等製造业。

託管服务业概览

全球託管服务市场竞争激烈,有几家大型企业参与。市场的主要企业包括Cisco、IBM、微软、富士通和 Wipro。随着市场竞争不断加剧,企业正在形成策略联盟和伙伴关係。

2022 年 5 月,安永和 IBM Expand Alliance 宣布决定透过数位创新和更强的弹性来帮助全球企业。安永和 IBM 正在建立一个新的人才卓越中心 (COE),该中心将建立资料驱动的人工智慧和混合云端解决方案,并提供全方位的人才、人力资源、流动性和薪资核算转型服务,以帮助客户转变其人力资源职能,同时克服吸引、留住和提升员工技能的迫切需求。

2022 年 5 月,IBM 宣布与亚马逊网路服务 (AWS) 达成策略合作协议 (SCA),透露计划在 AWS 上广泛提供其软体目录作为软体即服务 (SaaS)。企业将能够在 AWS 上将广泛的 IBM 软体组合作为云端原生服务运行,使推出和运行以实现业务价值。

2022 年 1 月,Rackspace Technology 与 BT 宣布达成伙伴关係协议,为 BT 的跨国客户转型云端服务。根据协议,英国电信的混合云服务将基于 Rackspace 技术解决方案,该公司将透过 Rackspace Fabric 管理层将其部署在英国电信的资料中心。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 转向混合IT的转变日益加剧

- 提高成本和业务效率

- 市场挑战

- 整合和监管问题、可靠性问题

第六章市场区隔

- 扩张

- 本地

- 云

- 类型

- 託管资料中心

- 託管安全

- 託管通讯

- 主机网路

- 託管基础设施

- 託管行动性

- 公司规模

- 中小企业

- 大型企业

- 按最终用户产业

- BFSI

- 资讯科技/通讯

- 卫生保健

- 娱乐和媒体

- 零售

- 製造业

- 政府

- 其他最终用户产业

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第七章竞争格局

- 公司简介

- Fujitsu Ltd

- Cisco Systems Inc.

- IBM Corporation

- AT&T Inc.

- HP Development Company LP

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Nokia Solutions and Networks

- Deutsche Telekom AG

- Rackspace Inc.

- Tata Consultancy Services Limited

- Citrix Systems Inc.

- Wipro Ltd

- NSC Global Ltd

- Telefonaktiebolaget LM Ericsson

第八章投资分析

第九章 市场机会与未来趋势

The Managed Services Market size is estimated at USD 303.16 billion in 2025, and is expected to reach USD 443.38 billion by 2030, at a CAGR of 7.9% during the forecast period (2025-2030).

Small and midsize Businesses (SMB) are expected to be the driving factors that positively impact the market's growth, as more and more SMBs are looking to outsource non-core activities. According to Datto, on average, MSPs report a client base of 122 clients, and about 60% of the MSP's clients have between 1-150 employees. Additionally, only 5% of the MSPs reported clients with over 500 employees.

Key Highlights

- Managed services offer various benefits that are proven to positively impact the development of the organization that adopts such services as they can focus on their core expertise. It is estimated that successfully deploying managed services will help reduce IT cost by 25-45% and increase operational efficiency by 45-65%. In addition, according to Intelligent Technical Solutions, 25% of organizations said downtime costs averaged between USD 301,000 and USD 400,000 per hour.

- Moreover, 2022 was expected to be all about application deployments matched to the development speed. The application maintenance and support services will be pivotal to the managed services in IT. Application performance monitoring (APM) will imbibe a quick feedback mechanism for developers. Front-end monitoring (for studying user behavior), ADTD (for application discovery, tracing, and diagnostics), and AIOps analytics (for detecting application lifecycle patterns and anomalies) will all be parts of APM. These solutions will help the DevOps team to analyze business problems better. It will cut down on their mean time to repair (MTTR).

- With industry requirements, standards, and consumer needs changing daily, businesses are seeking result-based outcomes. They require possession of pre-defined or expected criteria documented clearly, and in real time. The MSP will now be seen using advanced analytics and reporting to state the implemented technologies' impact and present factual data.

- Further, the Blockchain and IoT technologies are set to create better opportunities for managed services providers, as these organizations require expertise to implement these technologies. To get a hold of these opportunities, stay relevant, and keep up with the competition, managed services providers increasingly acquire essential skill sets for these, among other innovative technologies, like AR, VR, and AI.

- Since the outbreak of COVID-19, the demand for cloud-based solutions saw significant growth due to remote working models being adopted by enterprises. As more IT decision-makers look to take advantage of modern cloud environments, they are increasingly running into longer project runways and the need for bigger budgets. According to Wanclouds, nearly half (48%) of the US and the UK IT decision-makers say the average time it takes them to complete a single multi-cloud application migration successfully is 1-2 months.

Managed Services Market Trends

Manufacturing is Expected to Hold a Significant Market Share

- In the current technology-driven business environment, Big Data is one of the manufacturers' primary drivers of productivity and efficiency. With the high rate of adoption of sensors and connected devices and the enabling of M2M communication, there has been a massive increase in the data points that are generated in the manufacturing industry.

- Industries are pitching hard and fast to switch to a smart industry, where data generation and visualization can become real-time. From descriptive to predictive, the evolution of analytics has made the industry aware of the benefits it can reap from this volume of data. The motto of the manufacturing industry is moving toward a metrics-based sector, which can improve decision-making based on the data-driven use of statistics.

- With the concept of Industry 4.0 influencing production establishments in the manufacturing industry, the amount of data produced from the manufacturing industry has snowballed, as they have been able to create data from each process point, varying from temperature, pressure, humidity, stress, strain, and quality, among numerous others.

- There are several applications in the semiconductors, consumer electronics, and the automotive industry, where manufacturers have to monitor numerous variables to ensure the quality of end products. Big Data analytics has emerged as an effective solution to traditional methods.

- As most small and medium manufacturing industries are more concentrated on hardware equipment and lack expertise in software solutions, they are outsourcing these Big Data analytic solutions. Outsourcing software services are further reducing their expenditure. Outsourcing other software services, such as field service management and ERP, is expected to boost managed services during the forecast period.

Asia-Pacific is Expected to be the Fastest Growing Market

- Digital transformation has become a top priority in the country and is moving rapidly as more companies are implementing formal strategies to support their efforts. In January 2021, China's State Council released a proposal to help the digital economy flourish throughout the 14th Five-Year Plan period (2021-2025). According to the plan, China's digital transformation of industries will reach a new level by 2025, while digital public services will become more inclusive, and the digital economy governance structure will visibly improve.

- The managed service providers in China focus on reducing security risks and optimizing operations for the end users by keeping up with the latest technologies. The telecommunication companies in the country majorly offer the managed services market. These companies are also strategically acquiring companies offering managed services to gain more market share.

- Furthermore, the banking sector in India is experiencing a colossal change due to the rapid evolution of technology in its verticals, which led to the adoption of cloud computing services by organizations to address their issues. Additionally, the managed storage providers in the country are investing in developing an integrated cloud storage platform dedicated to the BFSI sector.

- Moreover, the ongoing extensive investments by the Indian government toward physical infrastructures, like smart cities, are expected to create more opportunities for deploying managed services, like data storage, security, and network management, in the country. Currently, the Indian smart cities program is focused on transforming 100 cities.

- In January 2022, KPMG India and Qualys announced a partnership to add Qualys solutions to KPMG's Managed Security service. KPMG's industry-leading and globally recognized cybersecurity services in India will be combined with Qualys' world-class cybersecurity innovations to enable enterprises to protect their network, applications, endpoints, and cloud workloads from security vulnerabilities, provide visibility, and ensure compliance.

- Whereas, with the service industry taking up the largest portion of its GDP, Japan has much to share in managing the service industry. Japan has always been a market-oriented economy and represents the second-most developed economy in the world. Currently, the country is focusing on the manufacturing sectors, including the production of hybrid vehicles, robotics, and optical instruments.

Managed Services Industry Overview

The global managed services market is very competitive because of the presence of several major players. Some major players in the market are Cisco Systems Inc., IBM Corporation, Microsoft Corporation, Fujitsu Ltd, and Wipro Ltd. The market players are forming strategic collaborations and partnerships to sustain the intense competition in the market.

In May 2022, EY and IBM Expand Alliance announced their decision to help businesses around the world through digital innovation and greater resilience.EY and IBM have established a new Talent Center of Excellence (COE) that will create data-driven AI and hybrid cloud solutions to provide broad talent, HR, mobility, and payroll transformation services helping clients in overcoming the urgent need to attract, retain and upskill their workforce while transforming their HR function.

In May 2022, IBM announced a Strategic Collaboration Agreement (SCA) with Amazon Web Services Inc. (AWS), with plans to offer a broad array of its software catalog as Software-as-a-Service (SaaS) on AWS that will help customers build and deploy modern, secure, and more intelligent workflows with IBM Software on AWS. Organizations will be able to run a broad array of the IBM Software catalog as cloud-native services on AWS so they can get up and running quickly to deliver business value.

In January 2022, Rackspace Technology and BT announced a partnership agreement to transform BT's multinational customers' cloud services. Under the terms of the agreement, BT's hybrid cloud services will be based on Rackspace Technology's solutions, which the company will deploy in BT data centers along with its Rackspace Fabric management layer.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Challenges

- 5.2.1 Integration and Regulatory Issues and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 Enterprise Size

- 6.3.1 Small and Medium Enterprises

- 6.3.2 Large Enterprises

- 6.4 End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecommunication

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-User Verticals

- 6.5 Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 India

- 6.5.3.3 Japan

- 6.5.3.4 Rest of Asia-Pacific

- 6.5.4 Latin America

- 6.5.4.1 Brazil

- 6.5.4.2 Argentina

- 6.5.4.3 Mexico

- 6.5.4.4 Rest of Latin America

- 6.5.5 Middle East and Africa

- 6.5.5.1 United Arab Emirates

- 6.5.5.2 Saudi Arabia

- 6.5.5.3 South Africa

- 6.5.5.4 Rest of Middle East and Africa

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Development Company LP

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Nokia Solutions and Networks

- 7.1.10 Deutsche Telekom AG

- 7.1.11 Rackspace Inc.

- 7.1.12 Tata Consultancy Services Limited

- 7.1.13 Citrix Systems Inc.

- 7.1.14 Wipro Ltd

- 7.1.15 NSC Global Ltd

- 7.1.16 Telefonaktiebolaget LM Ericsson

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测

管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测 2025年全球託管服务市场报告全球託管通讯服务市场:2032 年预测 - 按服务类型、部署方式、组织规模、最终用户和地区进行分析2025年电信託管服务全球市场报告

2025年全球託管服务市场报告全球託管通讯服务市场:2032 年预测 - 按服务类型、部署方式、组织规模、最终用户和地区进行分析2025年电信託管服务全球市场报告 託管服务市场:2025-2030 年全球预测(按服务类型、合约类型、组织规模、最终用户和部署类型)

託管服务市场:2025-2030 年全球预测(按服务类型、合约类型、组织规模、最终用户和部署类型) 全球管理资讯服务市场全球託管基础设施服务市场

全球管理资讯服务市场全球託管基础设施服务市场 託管IT基础设施服务市场规模、份额、成长分析(按类型、最终用户、企业规模、服务类别和地区)- 产业预测,2025 年至 2032 年

託管IT基础设施服务市场规模、份额、成长分析(按类型、最终用户、企业规模、服务类别和地区)- 产业预测,2025 年至 2032 年 2025-2029年全球託管IT基础设施服务市场2032 年託管服务市场预测:按服务类型、组织规模、部署模式、最终用户和地区进行的全球分析

2025-2029年全球託管IT基础设施服务市场2032 年託管服务市场预测:按服务类型、组织规模、部署模式、最终用户和地区进行的全球分析