|

市场调查报告书

商品编码

1687065

英国货运和物流:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)United Kingdom Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

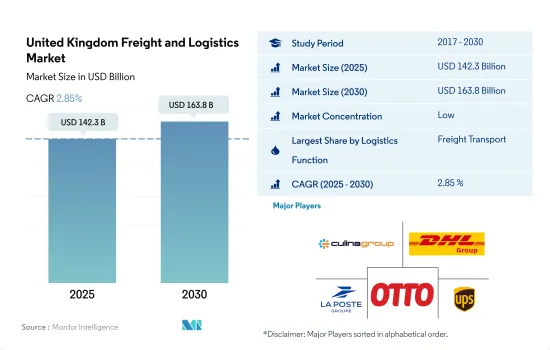

英国货运和物流市场规模预计在 2025 年达到 1,423 亿美元,预计到 2030 年将达到 1,638 亿美元,预测期内(2025-2030 年)的复合年增长率为 2.85%。

电子商务的推出、基础设施的发展以及促进技术采用的策略正在推动市场需求。

- 英国的目标是到2040年实现所有新型重型货车零排放。据预测,英国电动卡车市场预计将在2020年至2026年期间以约70%的复合年增长率强劲增长,预计2026年的销量将达到2167辆。其中,预计25辆中有22辆将是中型电动卡车。一个值得注意的进展是,亚马逊宣布计划在 2022 年将五辆电动重型货车 (HGV) 引入其配送车队,每年行驶 10 万英里。这项措施预计将减少二氧化碳排放170多吨。英国正积极建立国家架空导线网络,为远距电动卡车提供动力,以实现2050年交通脱碳的目标。

- 电子商务的快速成长是英国运输业发展的一大催化剂。预测显示,2025年,英国电子商务收益将达到1,795亿美元。 2023年,服装和箱包等时尚产品的电子商务销售额预计将大幅成长,增加53.8亿美元以上,达到约438.9亿美元。预计这一上升趋势将持续下去,到 2025 年时尚市场电子商务销售收益预计将达到约 543.6 亿美元。

英国货运和物流市场趋势

随着消费者履约中心需求的增长,预计到 2027 年英国仓库数量将达到 214,000 个

- 2024 年 5 月,杜拜环球港务集团在考文垂开设了迄今为止最大的仓库,占地 598,000 平方英尺,这是 5,000 万英镑(6,092 万美元)投资的一部分,旨在增强客户竞争力。此前,英国政府于 2023 年 9 月在比斯特开设了一座占地 270,000 平方英尺的音乐和视讯分销仓库,该仓库将处理英国70% 的实体音乐和 35% 的家庭娱乐产品。 DP World 先前已在特伦特河畔伯顿开设了一个 75,000 平方英尺的仓库,并在伦敦门户物流中心开设了一个 230,000 平方英尺的多用户仓库。杜拜环球港务集团在南安普敦和伦敦门户设有枢纽,业务遍及 78 个国家,控制全球 10% 的贸易。预计这些倡议将提高该产业对 GDP 的贡献。

- 英国大型仓库的数量正在快速成长。到 2027 年,预计全球整体将有约 214,000 个面积超过 50,000 平方英尺的仓库。许多仓库将作为电子商务履约中心,到 2027 年,大约 18% 的仓库将用于消费者履约。这一增长表明,随着电子商务的扩张,作为贸易物流中心的仓库比例开始转向消费者履约中心。

英国政府对燃油价格有很大影响,燃油税和增值税(标准税率为 20%)构成了汽油和柴油价格的大部分。

- 2022年8月,原油价格跌破100美元,月末收在每桶90.63美元。 2023年油价进一步下跌,5月跌至每桶72.50美元的低点。 2024年3月,英国汽油价格平均为每公升150.1披索,为2023年11月以来的最高水准。这是由于油价上涨以及中东局势恶化导致英镑兑美元走弱。虽然整体通膨有所缓和,但 3 月汽油和柴油价格上涨。 2024 年 4 月以色列对伊朗发动报復性攻击后,油价飙升,随后开始下跌。

- 2024 年 6 月,英国政府确认计画在 2030 年强制要求喷射机燃料中至少含有 10% 的永续航空燃料 (SAF)。目前,SAF 比传统燃料稀缺且昂贵,因此很难增加其在航空领域的使用。 SAF 占世界喷射机燃料的份额不到 0.1%。政府对 SAF 的授权将于 2025 年 1 月开始,但需获得立法核准。这是 2022 年「Jet Zero」策略的延续,该策略的目标是到 2050 年实现航空业净零排放。

英国货运及物流业概况

英国货运和物流市场较为分散,主要有主要企业(按字母顺序排列):Culina Group、DHL Group、La Poste Group(包括 DPD Group、CitySprint (UK) Ltd.)、Otto Group(包括 Evri Limited)和美国联合包裹服务公司 - UPS(包括 Coyote Logistics)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 人口统计

- 按经济活动分類的GDP分布

- 经济活动GDP成长

- 通货膨胀率

- 经济表现及概况

- 电子商务产业趋势

- 製造业趋势

- 交通运输仓储业GDP

- 出口趋势

- 进口趋势

- 燃油价格

- 卡车运输成本

- 卡车持有量(按类型)

- 物流绩效

- 主要卡车供应商

- 模态共享

- 海运能力

- 班轮连结性

- 停靠港和演出

- 货运趋势

- 货物吨位趋势

- 基础设施

- 法律规范(公路和铁路)

- 英国

- 法律规范(海运和空运)

- 英国

- 价值炼和通路分析

第五章市场区隔

- 最终用户产业

- 农业、渔业和林业

- 建设业

- 製造业

- 石油和天然气、采矿和采石

- 批发和零售

- 其他的

- 物流功能

- 快递、快递和小包裹(CEP)

- 目的地

- 国内的

- 国际的

- 货物

- 按交通方式

- 航空

- 海上和内陆水道

- 其他的

- 货物

- 交通方式

- 航空

- 管道

- 铁路

- 路

- 海上和内陆水道

- 仓库存放

- 温度管理

- 无温度控制

- 温度管理

- 其他服务

- 快递、快递和小包裹(CEP)

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介.

- Advanced Supply Chain Group

- Americold(including Americold Whitchurch)

- Ballyvesey Holdings Limited(including Montgomery Transport)

- CMA CGM Group(including CEVA Logistics)

- Culina Group

- DACHSER

- Delamode Group(formerly Xpediator PLC)

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DP World(including P&O Ferrymasters)

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Europa Worldwide Group

- Expeditors International of Washington, Inc.

- FedEx

- GBA Logistics

- Gregory Distribution Ltd.

- Hellmann Worldwide Logistics

- Hoyer Group(including Hoyer UK Ltd)

- Huboo

- Kinaxia Logistics Limited(including Mark Thompson Transport)

- Kuehne+Nagel

- La Poste Group(including DPD Group, and CitySprint(UK)Ltd.)

- Lineage, Inc.

- Maritime Group Ltd.

- Meachers Global Logistics

- Otto Group(including Evri Limited)

- Owens Group

- Pall-Ex Group

- PD Ports(owned by Brookfield Asset Management)

- Peel Ports Group

- Rhenus Group

- Samskip

- SITRA Group(including Abbey Logistics Group)

- Solstor UK Limited

- Swain Group

- Turners(Soham)Ltd.

- United Parcel Service of America, Inc.-UPS(including Coyote Logistics)

- WH Malcolm Ltd.

- Walden Group(including Moviantio)

- Whistl UK Ltd.

- Wincanton PLC

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(市场驱动因素、限制因素、机会)

- 技术进步

- 资讯来源及延伸阅读

- 图表清单

- 关键见解

- 资料包

- 词彙表

- 外汇

The United Kingdom Freight and Logistics Market size is estimated at 142.3 billion USD in 2025, and is expected to reach 163.8 billion USD by 2030, growing at a CAGR of 2.85% during the forecast period (2025-2030).

E-commerce, infrastructure development, and strategy launches will boost technology adoption are leading the market demand

- The UK aims to achieve zero-emission status for new heavy goods vehicles by 2040. Projections indicate a robust CAGR of nearly 70% for the UK's electric truck market from 2020 to 2026, with sales forecasted to hit 2,167 units in 2026. Of these, approximately 22 out of every 25 vehicles are expected to be medium-duty electric trucks. In a notable development, Amazon announced plans in 2022 to introduce five electric heavy goods vehicles (HGVs) into its delivery fleet, covering a distance of 100,000 miles annually. This initiative is anticipated to reduce carbon emissions by over 170 tonnes. The UK is actively working on establishing a nationwide network of overhead wires to power long-distance electric trucks, aligning with its 2050 goal of decarbonizing transportation.

- The rapid growth of e-commerce is a major catalyst for the UK's transportation sector. Projections indicate that e-commerce revenue in the UK will reach USD 179.5 billion by 2025. In 2023, revenue from e-commerce sales of fashion products, including apparel and bags, saw a significant surge, rising by over USD 5.38 billion to approximately USD 43.89 billion. This upward trend is expected to continue, with revenue from e-commerce sales in the fashion market projected to reach around USD 54.36 billion by 2025.

United Kingdom Freight and Logistics Market Trends

The UK's warehouse count is expected to reach 214,000 by 2027 due to a rise in demand for consumer fulfillment centers

- In May 2024, DP World opened its largest warehouse yet, a 598,000 sq ft facility in Coventry, as part of a GBP 50 million (USD 60.92 million) investment to boost customer competitiveness. This follows the September 2023 opening of a 270,000 sq ft music and video distribution warehouse in Bicester, handling 70% of the UK's physical music and 35% of home entertainment products. Previously, DP World opened a 75,000 sq ft site in Burton upon Trent and a 230,000 sq ft multi-user warehouse at London Gateway's logistics hub. Alongside its hubs at Southampton and London Gateway, operating in 78 countries, DP World manages 10% of global trade. Such initiaves are expected to boost the GDP contribution from the sector.

- The number of large warehouses in the United Kingdom is rapidly increasing. By 2027, there are expected to be around 214,000 warehouses larger than 50,000 square feet globally. Many of these warehouses are to serve as e-commerce fulfillment centers, and approximately 18% of all warehouses will be for consumer fulfillment by 2027. This increase suggests the global expansion of e-commerce as the proportion of warehouses operating as trade distribution hubs begins to shift in favor of consumer fulfillment centers.

UK government has a major influence on fuel prices, and both fuel duty and VAT (standard 20% rate) make up majority of the petrol and diesel prices

- In August 2022, the oil price dropped under USD 100 and finished the month at USD 90.63 a barrel. Prices dropped further in 2023, and by May, a barrel of oil was down to USD 72.50. In March 2024, petrol prices in the UK averaged 150.1p per litre, the highest since November 2023. This is due to rising oil prices due to Middle East tensions and a weaker pound against the dollar. Although overall inflation has eased, petrol and diesel prices increased in March. Oil prices have since dropped after spiking following Israel's retaliatory attack on Iran in April 2024.

- In June 2024, the UK government confirmed it plans to require at least 10% sustainable aviation fuel (SAF) in jet fuel by 2030. Currently, SAF is scarce and more expensive than traditional fuels, making it challenging to increase its use in aviation. SAF represents less than 0.1% of jet fuel globally. The government's SAF mandate, pending legislative approval, is set to start in January 2025. This follows the 2022 "Jet Zero" strategy aiming for net-zero emissions in aviation by 2050.

United Kingdom Freight and Logistics Industry Overview

The United Kingdom Freight and Logistics Market is fragmented, with the major five players in this market being Culina Group, DHL Group, La Poste Group (including DPD Group, and CitySprint (UK) Ltd.), Otto Group (including Evri Limited) and United Parcel Service of America, Inc. - UPS (including Coyote Logistics) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 United Kingdom

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 United Kingdom

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Advanced Supply Chain Group

- 6.4.2 Americold (including Americold Whitchurch)

- 6.4.3 Ballyvesey Holdings Limited (including Montgomery Transport)

- 6.4.4 CMA CGM Group (including CEVA Logistics)

- 6.4.5 Culina Group

- 6.4.6 DACHSER

- 6.4.7 Delamode Group (formerly Xpediator PLC)

- 6.4.8 Deutsche Bahn AG (including DB Schenker)

- 6.4.9 DHL Group

- 6.4.10 DP World (including P&O Ferrymasters)

- 6.4.11 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.12 Europa Worldwide Group

- 6.4.13 Expeditors International of Washington, Inc.

- 6.4.14 FedEx

- 6.4.15 GBA Logistics

- 6.4.16 Gregory Distribution Ltd.

- 6.4.17 Hellmann Worldwide Logistics

- 6.4.18 Hoyer Group (including Hoyer UK Ltd)

- 6.4.19 Huboo

- 6.4.20 Kinaxia Logistics Limited (including Mark Thompson Transport)

- 6.4.21 Kuehne+Nagel

- 6.4.22 La Poste Group (including DPD Group, and CitySprint (UK) Ltd.)

- 6.4.23 Lineage, Inc.

- 6.4.24 Maritime Group Ltd.

- 6.4.25 Meachers Global Logistics

- 6.4.26 Otto Group (including Evri Limited)

- 6.4.27 Owens Group

- 6.4.28 Pall-Ex Group

- 6.4.29 PD Ports (owned by Brookfield Asset Management)

- 6.4.30 Peel Ports Group

- 6.4.31 Rhenus Group

- 6.4.32 Samskip

- 6.4.33 SITRA Group (including Abbey Logistics Group)

- 6.4.34 Solstor UK Limited

- 6.4.35 Swain Group

- 6.4.36 Turners (Soham) Ltd.

- 6.4.37 United Parcel Service of America, Inc. - UPS (including Coyote Logistics)

- 6.4.38 W H Malcolm Ltd.

- 6.4.39 Walden Group (including Moviantio)

- 6.4.40 Whistl UK Ltd.

- 6.4.41 Wincanton PLC

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

全球货物审核与结算市场预测(2025-2030)

全球货物审核与结算市场预测(2025-2030) 2032 年碳中和解决方案市场预测:按类型、组件、部署模式、组织规模、技术、最终用户和地区进行的全球分析

2032 年碳中和解决方案市场预测:按类型、组件、部署模式、组织规模、技术、最终用户和地区进行的全球分析 2025年货运和物流全球市场报告

2025年货运和物流全球市场报告 货运审核与结算市场规模、份额及成长分析(依公司规模、最终用户、应用及地区)-2025 年至 2032 年产业预测

货运审核与结算市场规模、份额及成长分析(依公司规模、最终用户、应用及地区)-2025 年至 2032 年产业预测 2034 年货运与物流市场分析与预测:类型、产品、服务、技术、组件、应用、流程、模式、最终用户2025年全球货运车辆市场报告

2034 年货运与物流市场分析与预测:类型、产品、服务、技术、组件、应用、流程、模式、最终用户2025年全球货运车辆市场报告 东协货运与物流:市场占有率分析、产业趋势与成长预测(2025-2030 年)中国货运与物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030)义大利货运和物流:市场占有率分析、行业趋势和成长预测(2025-2030 年)亚太货运与物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

东协货运与物流:市场占有率分析、产业趋势与成长预测(2025-2030 年)中国货运与物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030)义大利货运和物流:市场占有率分析、行业趋势和成长预测(2025-2030 年)亚太货运与物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)