|

市场调查报告书

商品编码

1851460

美国个人护理包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)US Personal Care Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

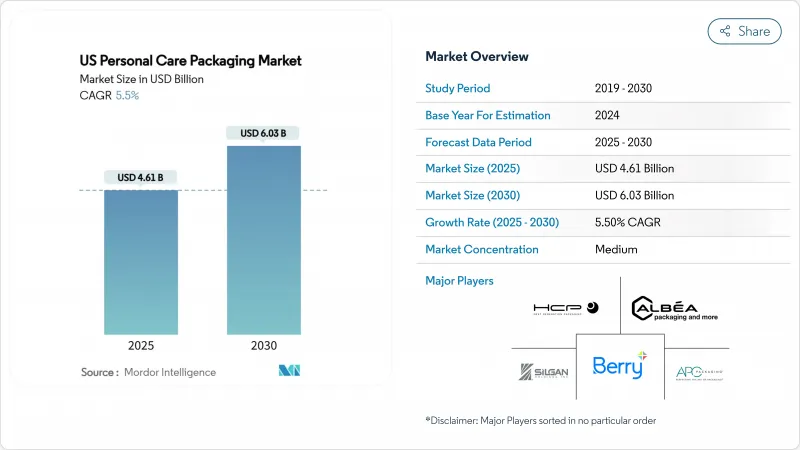

据估计,2025 年美国个人护理包装市场规模为 46.1 亿美元,预计到 2030 年将达到 60.3 亿美元,预测期(2025-2030 年)复合年增长率为 5.5%。

全氟烷基和多氟烷基物质(PFAS)的持续淘汰、永续性指令以及社交媒体主导的对吸睛包装的追求,正在重塑材料选择和设计理念。明尼苏达州严格的州法规规定,2025年禁止在化妆品中故意添加PFAS,促使加工商探索新的阻隔化学技术併升级回收基础设施。美国西部家庭每年在个人保养用品上的支出为1,038美元,远高于908美元的全国平均。这一趋势在安姆科(Amcor)与贝瑞全球(Berry Global)于2025年4月进行的全股票合併中得到了体现,预计此次合併将产生6.5亿美元的协同效应,并在2028年之前带来超过30亿美元的现金流。这些因素正在推动美国个人护理包装市场价值的稳定成长,提高产品种类(SKU)的普及率,并促进对可重复填充包装设计的需求。

美国个人护理包装市场趋势与洞察

可支配收入的增加推动了对包装产品的需求。

到2024年,个人照护支出将达到每户908美元,欧洲和美国的成长速度将更快,平均年支出为1,038美元。强劲的工资成长将推动产品种类多样化、高端包装和特色配方的发展,从而刺激美国个人护理包装市场的需求成长。玻璃和金属材质的包装将受益最大,因为消费者普遍认为玻璃和金属与品质和永续性有关。

适合在Instagram上分享的美感加速了优质化。

如今,设计本身也成为了一种行销管道,促使品牌投资于引人注目的造型、压花工艺和上镜的客製化色彩。玻璃瓶和拉丝铝製气雾剂比传统的HDPE瓶表现更佳,因为它们更符合环保讯息,也更适合在社群平台上进行视觉叙事。欧莱雅与IBM合作,利用人工智慧训练永续配方,这清楚地展现了科技的融合如何兼顾外观和功能。

高昂的研发和模具成本限制了创新。

开发新型吹塑成型模具和精密帮浦的成本可能超过每条生产线100万美元。规模较小的加工商难以承担多次试验的费用,尤其是在生物基树脂需要专用设备和漫长的资质认证流程时。折迭式施用器的专利申请表明,差异化点胶技术背后蕴含着复杂性和高资本投入。

细分市场分析

由于成本低、设计灵活且供应链成熟,塑胶包装预计在2024年仍将占据美国个人护理用品包装市场50.6%的份额。然而,受PFAS(全氟烷基和多氟烷基物质)污染治理以及消费者对可再生基材支援的影响,预计到2030年,纸和纸板包装市场将以9.5%的复合年增长率成长。各大品牌正在尝试使用阻隔涂布纸盒和纤维模塑罐,这些产品能够通过水分测试,且不会影响保存期限。再生PET的整合以及试验化学回收工厂的建设,有助于缓解人们对循环利用的担忧,并保护塑胶的铅含量。

循环经济政策正推动加工商提高消费后再生树脂(PCR)的含量并建立回收计划。同时,玻璃和金属因其奢侈品定位而受益。高端护肤品牌纷纷采用厚壁瓶身和带刷头的铝製包装,并宣称其可无限循环利用,以此来证明其溢价的合理性。垂直整合也推动了材料创新,例如安姆科(Amcor)对树脂采购的投资,确保了不断增长的美国个人护理包装市场所需的消费后再生树脂供应。

由于瓶装产品具有知名度、货架吸引力以及适用于乳液、洗髮精、沐浴乳露等多种产品的多功能性,预计到2024年,瓶装产品将占美国个人护理包装市场38.2%的份额。然而,受电商空间利用率高和材料用量低的推动,软包装袋预计将以11.2%的复合年增长率成长。可重复使用的吸嘴和自立袋提升了消费者的便利性,而超薄膜则减轻了运输重量。

软管、棒状包装和精密泵头分别适用于不同的应用场景,例如防晒棒用于防晒护理,无气泵头用于视网醇精华液,在这些应用中,剂量精准度比单价更为重要。随着品牌转向单一材料纸质解决方案以简化路边回收,可折迭纸盒正日益普及。在所有包装形式中,NFC晶片和QR码将包装转变为互动中心,这在竞争激烈的美国个人护理包装市场中成为一项关键的差异化优势。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 由于可支配所得增加,个人护理用品SKU消费量也随之增加。

- 对高端、适合在Instagram上晒照的包装美学的需求

- 电子商务的蓬勃发展需要一种便于运输且安全的格式。

- 订阅和补充装模式推动耐用/可重复使用包装的发展

- 符合美国运输安全管理局 (TSA) 标准的旅行包装,适合经常出游的消费者。

- 智慧/物联网赋能的包装,用于互动和可追溯性

- 市场限制

- 新型材料和製程的研发和模具成本高昂

- 美国收紧塑胶和 PFAS 法规

- 再生树脂价格和供应品质不稳定

- 补货和退货计划中的逆向物流摩擦

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争的激烈程度

第五章 市场规模与成长预测

- 依材料类型

- 塑胶

- 玻璃

- 金属

- 纸和纸板

- 依产品类型

- 瓶子

- 管子和棍子

- 泵浦和分配器

- 小袋

- 折迭式纸盒

- 其他的

- 透过使用

- 护肤

- 护髮

- 口腔护理

- 化妆品和彩妆品

- 除臭剂和香水

- 除毛膏

- 其他的

- 按永续性属性

- 可回收(单一材料)

- 消费后回收 (PCR) 成分

- 可填充/可重复使用

- 可堆肥/生物基

第六章 竞争情势

- 市场集中度

- 策略倡议与发展

- 市占率分析

- 公司简介

- Albea Services SA

- HCP Packaging Co. Ltd

- Berry Global Group Inc.

- Silgan Holdings Inc.

- DS Smith PLC

- Graham Packaging Company

- Kaufman Container

- AptarGroup Inc.

- Amcor PLC

- Cosmopak USA LLC

- APC Packaging

- Rieke Corp(Trimas)

- Berlin Packaging LLC

- Glenroy Inc.

- TricorBraun

- Quadpack

- ProAmpac

- WestRock Company

- Gerresheimer AG

- Sonoco Products Co.

- International Paper Co.

第七章 市场机会与未来展望

The US Personal Care Packaging Market size is estimated at USD 4.61 billion in 2025, and is expected to reach USD 6.03 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Persistent PFAS phase-outs, mounting sustainability mandates and the social-media driven quest for eye-catching packs are reshaping material selection and design philosophies. Tight state rules Minnesota's 2025 ban on intentionally added PFAS in cosmetics among them push converters to explore new barrier chemistries and upgrade recycling infrastructure. Regional spending patterns amplify these shifts: households in the West devote USD 1,038 each year to personal-care items, well above the USD 908 national average, which explains the region's early uptake of premium, sustainable formats. Brand owners also intensify vertical integration to lock in packaging innovation capacity, a trend underscored by Amcor's all-stock combination with Berry Global in April 2025, expected to generate USD 650 million in synergies and more than USD 3 billion in cash flow by 2028. Together, these forces support steady value growth, SKU proliferation and rising demand for refill-ready designs across the US personal care packaging market.

US Personal Care Packaging Market Trends and Insights

Rising Disposable Income Fuels Pack Demand

Personal-care outlays reached USD 908 per household in 2024 and climb even higher in the West, where annual spending averaged USD 1,038. Steady wage gains translate into greater SKU variety, premium pack finishes and niche formulations, which in turn boost unit-volume requirements across the US personal care packaging market. Glass and metal formats benefit the most because consumers associate them with quality and sustainability.

Instagram-Ready Aesthetics Accelerate Premiumization

Design now doubles as a marketing channel, prompting brands to invest in striking shapes, embossing and custom colorways that photograph well. Glass jars and brushed-aluminum aerosols outperform conventional HDPE bottles because they align with eco-messaging and visual storytelling on social platforms. L'Oreal's partnership with IBM to train AI on sustainable formulations underscores how tech convergence supports both look and function.

High R&D and Tooling Costs Limit Innovation

Developing a new blow-mold or precision pump can exceed USD 1 million per line. Small converters struggle to fund multiple trials, particularly when bio-based resins demand specialized machinery and extended qualification. Patent filings for collapsible applicators illustrate the complexity as well as the capital intensity behind differentiated dispensing technology.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Drives Ship-Ready Protective Formats

- Subscription and Refill Models Favor Durable Solutions

- State-Level PFAS Rules Add Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic retained 50.6% US personal care packaging market share in 2024 thanks to low cost, design flexibility and well-established supply chains. Yet the paper and paperboard segment is projected to log a 9.5% CAGR through 2030, buoyed by PFAS crackdowns and consumer favor for renewable substrates. Brands experiment with barrier-coated cartons and molded-fiber jars that pass moisture tests without compromising shelf appeal. Recycled PET integration and pilot chemical recycling plants help plastics defend their lead by easing circularity concerns.

Circular-economy policies push converters to raise post-consumer-resin (PCR) content and build take-back schemes. Simultaneously, glass and metal profit from luxury positioning: prestige skin-care labels deploy heavy-walled flacons and brushed-aluminum sticks to justify price premiums while touting infinite recyclability. Material innovation is also spurred by vertical integration, exemplified by Amcor's resin-sourcing investments that safeguard PCR supply for the expanding US personal care packaging market.

Bottles commanded 38.2% of the US personal care packaging market size in 2024 due to familiarity, shelf impact and versatility across lotions, shampoos and body washes. However, flexible pouches are projected to log an 11.2% CAGR, propelled by e-commerce cube-efficiency and lower material usage. Reclosable spouts and stand-up formats bolster consumer convenience, while ultra-thin films curb shipping weight.

Tubes, sticks and precision pumps cater to targeted applications think SPF sticks for sun-care or airless pumps for retinol serums where dosing accuracy matters more than unit cost. Folding cartons gain ground as brands migrate to mono-material paper solutions that simplify curbside recycling. Across all formats, NFC chips and QR codes elevate packs into engagement hubs, a key differentiator in the crowded US personal care packaging market.

US Personal Care Packaging Market Report is Segmented by Material Type (Plastic, Glass, Metal, Paper and Paperboard), Product Type (Bottles, Tubes and Sticks, Pumps and Dispensers, Pouches and More), Application (Skin Care, Hair Care, Oral Care, and More), Sustainability Attribute (Recyclable, Post-Consumer-Recycled Content, Refillable/Reusable, Compostable/Bio-based). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Albea Services SA

- HCP Packaging Co. Ltd

- Berry Global Group Inc.

- Silgan Holdings Inc.

- DS Smith PLC

- Graham Packaging Company

- Kaufman Container

- AptarGroup Inc.

- Amcor PLC

- Cosmopak USA LLC

- APC Packaging

- Rieke Corp (Trimas)

- Berlin Packaging LLC

- Glenroy Inc.

- TricorBraun

- Quadpack

- ProAmpac

- WestRock Company

- Gerresheimer AG

- Sonoco Products Co.

- International Paper Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumption of personal-care SKUs on higher disposable income

- 4.2.2 Demand for premium, "Instagram-ready" pack aesthetics

- 4.2.3 E-commerce boom needing ship-ready protective formats

- 4.2.4 Subscription and refill models driving durable / reusable packs

- 4.2.5 TSA-size travel packs for on-the-go consumers

- 4.2.6 Smart / IoT-enabled packs for engagement and traceability

- 4.3 Market Restraints

- 4.3.1 High RandD and tooling costs for novel formats and materials

- 4.3.2 Tightening U.S. plastics and PFAS regulations

- 4.3.3 Volatile recycled-resin price and supply quality

- 4.3.4 Reverse-logistics friction for refill / return programs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Paper and Paperboard

- 5.2 By Product Type

- 5.2.1 Bottles

- 5.2.2 Tubes and Sticks

- 5.2.3 Pumps and Dispensers

- 5.2.4 Pouches

- 5.2.5 Folding Cartons

- 5.2.6 Others

- 5.3 By Application

- 5.3.1 Skin Care

- 5.3.2 Hair Care

- 5.3.3 Oral Care

- 5.3.4 Makeup and Color Cosmetics

- 5.3.5 Deodorants and Fragrances

- 5.3.6 Depilatories

- 5.3.7 Others

- 5.4 By Sustainability Attribute

- 5.4.1 Recyclable (mono-material)

- 5.4.2 Post-consumer-recycled (PCR) Content

- 5.4.3 Refillable / Reusable

- 5.4.4 Compostable / Bio-based

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Albea Services SA

- 6.4.2 HCP Packaging Co. Ltd

- 6.4.3 Berry Global Group Inc.

- 6.4.4 Silgan Holdings Inc.

- 6.4.5 DS Smith PLC

- 6.4.6 Graham Packaging Company

- 6.4.7 Kaufman Container

- 6.4.8 AptarGroup Inc.

- 6.4.9 Amcor PLC

- 6.4.10 Cosmopak USA LLC

- 6.4.11 APC Packaging

- 6.4.12 Rieke Corp (Trimas)

- 6.4.13 Berlin Packaging LLC

- 6.4.14 Glenroy Inc.

- 6.4.15 TricorBraun

- 6.4.16 Quadpack

- 6.4.17 ProAmpac

- 6.4.18 WestRock Company

- 6.4.19 Gerresheimer AG

- 6.4.20 Sonoco Products Co.

- 6.4.21 International Paper Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

个人护理包装市场分析及预测(至2035年):按类型、产品类型、材料类型、应用、技术、最终用户、製程、组件和功能划分

个人护理包装市场分析及预测(至2035年):按类型、产品类型、材料类型、应用、技术、最终用户、製程、组件和功能划分 个人护理包装市场规模、份额和成长分析(按材料、产品类型、应用、包装类型和地区划分)-2026-2033年产业预测

个人护理包装市场规模、份额和成长分析(按材料、产品类型、应用、包装类型和地区划分)-2026-2033年产业预测 个人护理包装市场-2026-2031年预测

个人护理包装市场-2026-2031年预测 个人护理包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

个人护理包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 个人护理包装市场按产品类型、应用和地区划分中国个人护理包装:市场占有率分析、产业趋势、统计数据及成长预测(2025-2030)

个人护理包装市场按产品类型、应用和地区划分中国个人护理包装:市场占有率分析、产业趋势、统计数据及成长预测(2025-2030) 个人护理包装市场报告,按材料类型(塑胶、玻璃、金属、纸张)、包装类型(瓶、罐、袋、管、罐等)、应用(皮肤护理、头髮护理、沐浴和淋浴、化妆品等)和地区划分,2025 年至 2033 年中东和非洲的个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)亚太地区个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)北美个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)

个人护理包装市场报告,按材料类型(塑胶、玻璃、金属、纸张)、包装类型(瓶、罐、袋、管、罐等)、应用(皮肤护理、头髮护理、沐浴和淋浴、化妆品等)和地区划分,2025 年至 2033 年中东和非洲的个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)亚太地区个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)北美个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)