|

市场调查报告书

商品编码

1907333

个人护理包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Personal Care Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

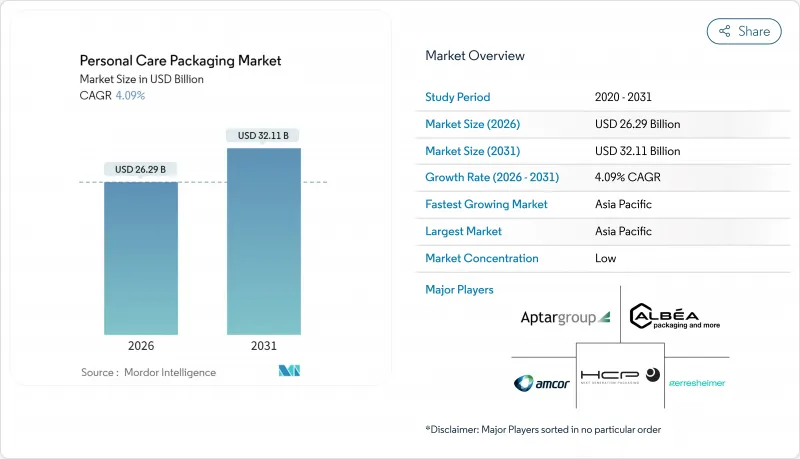

个人护理包装市场预计将从 2025 年的 252.6 亿美元成长到 2026 年的 262.9 亿美元,到 2031 年将达到 321.1 亿美元,2026 年至 2031 年的复合年增长率为 4.09%。

持续成长与新兴市场的优质化、至少30%的消费后回收(PCR)成分要求以及需要高防护性、即用型包装的全通路模式密切相关。以PCR PET、生物基聚合物和海洋塑胶原料为核心的材料创新,降低了监管风险并促进了产品差异化。边缘人工智慧填充线降低了单品生产成本,而家用可重复填充分配器则提升了消费者的便利性并减少了材料消耗。这些因素共同增强了北美和欧洲个人护理包装市场对树脂价格波动和一次性使用法规的抵御能力。

全球个人护理包装市场趋势与洞察

新兴市场美妆产品SKU的高端化

优质化透过金属光泽、压纹和多组件配置等技术,向注重性价比的消费者传递独特性,从而提升本土和国际品牌的品牌形象,使其成为消费者嚮往的品牌。数位装饰技术实现了经济高效的小批量生产,使得频繁推出限量版产品成为可能,这些产品的价格通常比普通产品高出20%至40%。护肤品的成功经验正推动护髮和除臭剂领域采用类似的策略,强化了消费者对包装精緻度与产品功效和安全性之间关係的认知。

全通路支援有助于提供保护和便于交付的包装。

电子商务的快速发展要求包装既要能承受单小包裹运输的衝击,又要保持商店市级的品牌形象。整合缓衝层、防篡改瓶盖和经过跌落测试的结构设计,无需二次包装,在某些情况下可减少高达 30% 的材料消费量。自动化技术能够实现零售和线上 SKU 之间的快速切换,随着各类别电子商务渗透率每年增长超过 25%,生产週期也得以缩短。

聚烯和PET原料价格波动

树脂成本一年内波动幅度可能超过40%,挤压加工业者的获利空间,促使他们采取动态定价和避险策略。供应限制进一步加剧了再生树脂价格的波动,推动垂直采购和长期合约的签订,以保障盈利。

细分市场分析

塑胶因其成本效益和可适应的阻隔性能,预计到2025年将占据个人护理包装市场58.22%的份额。聚乙烯和聚丙烯将成为该领域的主要生产驱动力,而聚对苯二甲酸乙二醇酯(PET)则因一次性使用法规的影响而落后。生物基树脂和聚合再生树脂(PCR)在2031年之前将维持4.22%的复合年增长率,从而缓解法规对个人护理包装市场规模的影响。玻璃将继续作为高端香水的优质包装材料,而金属气雾剂将继续在髮胶喷雾和除臭剂领域占据一席之地。纸板在对防潮性能要求不高的二级包装领域需求不断增长。

对先进回收技术和相容剂化学的持续投入,使加工商能够在不影响透明度和保质期的前提下,满足消费后回收物(PCR)标准。各大品牌正尝试使用无母粒和无添加剂配方,以最大限度地提高产品报废后的可回收性。这些进展表明,在政策压力日益增大的情况下,塑胶仍然处于行业前沿,而创新正在稳定个人护理包装市场。

到2025年,硬质容器将占据个人护理包装市场80.96%的份额,预计年复合成长率将达到5.51%,这主要得益于消费者对产品耐用性和品牌价值的重视。真空罐、玻璃滴管和带致动器的宝特瓶符合高端护肤和护髮产品的定位。虽然软包装袋凭藉旅行装和填充用填充包装正在逐渐占据市场,但品牌商仍依赖硬质主包装来提升产品在商店的吸引力和感知价值。

轻量化和模组化组装在保持刚性的同时减少了材料用量。混合解决方案将坚固的外壳与柔性补充容器相结合,在提供熟悉的用户体验的同时,永续性。随着业界对具备NFC认证功能的智慧封盖的广泛应用,硬质包装在数位化消费者互动策略中也继续发挥关键作用。

区域分析

亚太地区预计到2025年将占据个人护理包装市场41.62%的份额,并预计在2031年之前以5.18%的复合年增长率增长,这主要得益于可支配收入的增长、都市区化进程的推进以及男士护理市场的活性化。中国凭藉其一体化的供应链和快速成长的电子商务,将持续维持销售主导地位;而印度则因现代分销方式的兴起,销售量也呈现快速成长。日本和韩国引领全球智慧包装的潮流,将NFC标籤和热敏油墨应用于产品互动和真伪检验。

在北美,个人护理包装市场依然庞大,这主要得益于护肤和护髮品类的高端需求和品牌忠诚度。日益严格的再生塑胶(PCR)含量法规迫使加工商扩大机械和化学回收利用,巩固了该地区作为创新试验场的地位。在美国,对防篡改和儿童安全包装的需求推动了市场成长,而加拿大也呈现类似的趋势,并更加重视双语标籤。墨西哥的贸易协定以及其接近性原料产地的地理优势,为出口生产提供了成本效益高的基础。

欧洲的趋势正受到严格的减废弃物政策的影响。德国和法国正在量贩店中试行设立补充装站点,加速可重复使用包装的普及。英国在应对脱欧后复杂的清关程序的同时,也维持其高端香水玻璃容器的生产。南欧正利用其在高端硬包装领域的设计传统,而北欧市场则在推动使用纸盒作为二次包装,以满足循环经济指标的要求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴市场美妆产品优质化

- 全通路支援推动了保护性包装和运输包装的发展

- 永续性规则:要求至少含有 30% 的再生塑胶 (PCR) 成分

- 家用可重复填充分配器迅速普及

- 配备边缘人工智慧的填充线可降低 SKU 成本

- 东南亚男士护理市场快速成长

- 市场限制

- 聚烯和PET原料价格波动

- 欧盟及美国部分州已禁止使用一次性塑胶製品。

- 铝和玻璃供应链瓶颈

- 由于固态洗漱用品的兴起,初级包装被取代

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

第五章 市场规模与成长预测

- 依材料类型

- 塑胶

- 聚乙烯

- 聚丙烯

- PET和PVC

- 聚苯乙烯

- 生物基塑料

- 其他塑胶材料类型

- 玻璃

- 金属

- 纸和纸板

- 塑胶

- 按包装类型

- 柔软的

- 难的

- 依产品类型

- 瓶子和罐子

- 管子和棍子

- 泵浦和分配器

- 小袋和包装袋

- 瓶盖和封口

- 其他产品类型

- 透过使用

- 护肤

- 护髮

- 口腔护理

- 化妆品

- 除臭剂和香水

- 婴儿护理

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Albea SA

- HCP Packaging Group

- Gerresheimer AG

- Amcor plc

- AptarGroup, Inc.

- Cosmopak USA LLC

- Quadpack Industries, SA

- Libo Cosmetics Co., Ltd.

- Mpack Poland sp. z oo

- POLITECH SP. Z OO

- Rieke Corporation(TriMas Corporation)

- Berlin Packaging LLC

- MKTG INDUSTRY SRL

- Silgan Holdings, Inc.

- Stoelzle Oberglas GmbH

- EPL Limited

- Verescence Inc.

- Apackaging Group LLC

- Heinz-Glass GmbH & Ko. KGaA

- Roetell Group

- Vitro SAB De CV

- Vidraria Anchieta Ltda.

- Lumson SpA

第七章 市场机会与未来展望

The personal care packaging market is expected to grow from USD 25.26 billion in 2025 to USD 26.29 billion in 2026 and is forecast to reach USD 32.11 billion by 2031 at 4.09% CAGR over 2026-2031.

Sustained growth is linked to premiumization in emerging economies, the enforcement of a minimum 30% post-consumer recycled (PCR) content, and omni-channel fulfilment models that require ship-ready packs with high protective performance. Material innovation centered on PCR PET, bio-based polymers, and ocean-plastic feedstock mitigates regulatory risk and fuels product differentiation. Edge-AI filling lines are cutting SKU production costs, while refill-at-home dispensing formats broaden consumer convenience and lower material intensity. Together, these factors strengthen the personal care packaging market's resilience against volatile resin prices and single-use restrictions in North America and Europe.

Global Personal Care Packaging Market Trends and Insights

Premiumization of Beauty SKUs in Emerging Markets

Premiumization elevates local and global brands to aspirational status through metallic finishes, embossed textures, and multi-component assemblies that convey exclusivity to value-oriented consumers. Digital embellishment enables economically viable short runs, encouraging frequent limited-edition launches that command 20-40% price premiums. Success in skin care drives similar strategies in hair care and deodorants, reinforcing consumer perception that package sophistication signals efficacy and safety.

Omni-Channel Fulfillment Driving Protective and Ship-Ready Packs

E-commerce acceleration compels packages to survive single-parcel distribution while projecting shelf-quality branding. Integrated cushioning, tamper-evident closures, and drop-test-rated structures remove secondary boxes and trim material consumption by 30% for some adopters. Automation supports rapid line changeovers between retail and online SKUs, tightening production cycles as category e-commerce penetration exceeds 25% annually.

Volatile Polyolefin and PET Feed-Stock Prices

Resin costs swing more than 40% within a year, compressing converter margins and prompting dynamic pricing and hedging programs. Recycled resin prices fluctuate even more due to limited supply, driving vertically integrated sourcing and long-term contracts to shield profitability.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Rules Mandating More than 30% PCR Content

- Rapid Adoption of Refill-At-Home Dispensing Formats

- Supply-Chain Chokepoints in Aluminium and Glass

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic held 58.22% of the personal care packaging market share in 2025, supported by cost efficiency and adaptable barrier performance. Within the segment, polyethylene and polypropylene led volumes, while PET trailed under scrutiny from single-use restrictions. Bio-based and PCR resins underpin a 4.22% CAGR to 2031, cushioning regulatory impacts on the personal care packaging market size. Glass retained its luxury positioning for prestige fragrances, whereas metal aerosols sustained their niche in hair sprays and deodorants. Paperboard gains traction in secondary packs where moisture barriers are non-critical.

Continued investment in advanced recycling and compatibilizer chemistry allows converters to meet PCR thresholds without sacrificing clarity or shelf life. Brands experiment with colorless masterbatches and additive-free formulations to maximize end-of-life recyclability. These developments keep plastic at the forefront even as policy pressure intensifies, demonstrating how innovation stabilizes the personal care packaging market.

Rigid formats represented 80.96% of the personal care packaging market size in 2025 and are forecast to expand at a 5.51% CAGR, driven by consumer perception of durability and brand prestige. Airless jars, glass droppers, and PET bottles with spray actuators satisfy premium skin and hair care positioning. Flexible pouches penetrate travel sizes and refill pods, but brand owners still rely on rigid primary containers for shelf presence and perceived value.

Light-weighting and modular assemblies help offset material intensity while preserving rigidity. Hybrid solutions pair rigid outer shells with flexible refills, merging user familiarity with sustainability gains. Industry adoption of smart closures capable of NFC authentication keeps rigid packaging relevant in digital consumer engagement strategies.

The Personal Care Packaging Market Report is Segmented by Material Type (Plastic, Glass, Metal, and Paper and Paperboard), Packaging Format (Flexible and Rigid), Product Type (Bottles and Jars, Tubes and Sticks, Pumps and Dispensers, Pouches and Sachets, and More), Application (Skin Care, Hair Care, Oral Care, Make-Up Products, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 41.62% of the personal care packaging market share in 2025 and will expand at a 5.18% CAGR to 2031, lifted by rising disposable incomes, urban migration, and vibrant male grooming uptake. China sustains volume leadership on the back of integrated supply chains and surging e-commerce, while India registers rapid unit growth as modern trade formats multiply. Japan and South Korea steer global smart-packaging trends, embedding NFC tags and heat-sensitive inks for product interaction and authenticity verification.

North America maintains a sizeable personal care packaging market due to premiumization and brand loyalty in skin and hair care. Regulatory emphasis on PCR content pushes converters to scale mechanical and chemical recycling, cementing the region's role as an innovation testbed. The United States drives demand for tamper-resistant, child-safe packs, whereas Canada mirrors these tendencies with an additional focus on bilingual labeling. Mexico offers cost-effective production hubs for export-oriented runs, benefiting from trade agreements and proximity to raw material suppliers.

Europe's profile is shaped by stringent waste-reduction mandates. Germany and France pilot refill stations in mass retail, accelerating uptake of reusable packs. The United Kingdom navigates post-Brexit customs complexities yet retains high-value niche production in luxury fragrance glass. Southern Europe leverages design heritage in premium rigid formats, while Northern European markets advance carton-based secondary packs to satisfy circularity metrics.

- Albea S.A.

- HCP Packaging Group

- Gerresheimer AG

- Amcor plc

- AptarGroup, Inc.

- Cosmopak USA LLC

- Quadpack Industries, S.A.

- Libo Cosmetics Co., Ltd.

- Mpack Poland sp. z o.o.

- POLITECH SP. Z O.O.

- Rieke Corporation (TriMas Corporation)

- Berlin Packaging LLC

- MKTG INDUSTRY SRL

- Silgan Holdings, Inc.

- Stoelzle Oberglas GmbH

- EPL Limited

- Verescence Inc.

- Apackaging Group LLC

- Heinz-Glass GmbH & Ko. KGaA

- Roetell Group

- Vitro SAB De CV

- Vidraria Anchieta Ltda.

- Lumson S.p.A

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of Beauty SKUs in Emerging Markets

- 4.2.2 Omni-Channel Fulfilment Driving Protective and Ship-Ready Packs

- 4.2.3 Sustainability Rules Mandating more than 30 % PCR Content

- 4.2.4 Rapid Adoption of Refill-At-Home Dispensing Formats

- 4.2.5 Edge-Ai Enabled Filling Lines Cutting SKU Cost

- 4.2.6 Explosive Growth of Male Grooming in Southeast Asia

- 4.3 Market Restraints

- 4.3.1 Volatile Polyolefin and PET Feed-Stock Prices

- 4.3.2 Single-Use-Plastics Bans Across the EU and Select US States

- 4.3.3 Supply-Chain Chokepoints in Aluminium and Glass

- 4.3.4 Rise of Solid-Format Toiletries Replacing Primary Packs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.1.1 Polyethylene

- 5.1.1.2 Polypropylene

- 5.1.1.3 PET and PVC

- 5.1.1.4 Polystyrene

- 5.1.1.5 Bio-Based Plastics

- 5.1.1.6 Other Plastic Material Types

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Paper and Paperboard

- 5.1.1 Plastic

- 5.2 By Packaging Format

- 5.2.1 Flexible

- 5.2.2 Rigid

- 5.3 By Product Type

- 5.3.1 Bottles and Jars

- 5.3.2 Tubes and Sticks

- 5.3.3 Pumps and Dispensers

- 5.3.4 Pouches and Sachets

- 5.3.5 Caps and Closures

- 5.3.6 Other Product Types

- 5.4 By Application

- 5.4.1 Skin Care

- 5.4.2 Hair Care

- 5.4.3 Oral Care

- 5.4.4 Make-Up Products

- 5.4.5 Deodorants and Fragrances

- 5.4.6 Baby Care

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN Countries

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Albea S.A.

- 6.4.2 HCP Packaging Group

- 6.4.3 Gerresheimer AG

- 6.4.4 Amcor plc

- 6.4.5 AptarGroup, Inc.

- 6.4.6 Cosmopak USA LLC

- 6.4.7 Quadpack Industries, S.A.

- 6.4.8 Libo Cosmetics Co., Ltd.

- 6.4.9 Mpack Poland sp. z o.o.

- 6.4.10 POLITECH SP. Z O.O.

- 6.4.11 Rieke Corporation (TriMas Corporation)

- 6.4.12 Berlin Packaging LLC

- 6.4.13 MKTG INDUSTRY SRL

- 6.4.14 Silgan Holdings, Inc.

- 6.4.15 Stoelzle Oberglas GmbH

- 6.4.16 EPL Limited

- 6.4.17 Verescence Inc.

- 6.4.18 Apackaging Group LLC

- 6.4.19 Heinz-Glass GmbH & Ko. KGaA

- 6.4.20 Roetell Group

- 6.4.21 Vitro SAB De CV

- 6.4.22 Vidraria Anchieta Ltda.

- 6.4.23 Lumson S.p.A

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

个人护理包装市场分析及预测(至2035年):按类型、产品类型、材料类型、应用、技术、最终用户、製程、组件和功能划分

个人护理包装市场分析及预测(至2035年):按类型、产品类型、材料类型、应用、技术、最终用户、製程、组件和功能划分 个人护理包装市场规模、份额和成长分析(按材料、产品类型、应用、包装类型和地区划分)-2026-2033年产业预测

个人护理包装市场规模、份额和成长分析(按材料、产品类型、应用、包装类型和地区划分)-2026-2033年产业预测 个人护理包装市场-2026-2031年预测

个人护理包装市场-2026-2031年预测 个人护理包装市场按产品类型、应用和地区划分

个人护理包装市场按产品类型、应用和地区划分 美国个人护理包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)中国个人护理包装:市场占有率分析、产业趋势、统计数据及成长预测(2025-2030)

美国个人护理包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)中国个人护理包装:市场占有率分析、产业趋势、统计数据及成长预测(2025-2030) 个人护理包装市场报告,按材料类型(塑胶、玻璃、金属、纸张)、包装类型(瓶、罐、袋、管、罐等)、应用(皮肤护理、头髮护理、沐浴和淋浴、化妆品等)和地区划分,2025 年至 2033 年中东和非洲的个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)亚太地区个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)北美个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)

个人护理包装市场报告,按材料类型(塑胶、玻璃、金属、纸张)、包装类型(瓶、罐、袋、管、罐等)、应用(皮肤护理、头髮护理、沐浴和淋浴、化妆品等)和地区划分,2025 年至 2033 年中东和非洲的个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)亚太地区个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)北美个人护理包装:市场占有率分析、行业趋势和成长预测(2025-2030)