|

市场调查报告书

商品编码

1906035

中东和非洲货运物流市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)Middle East And Africa Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

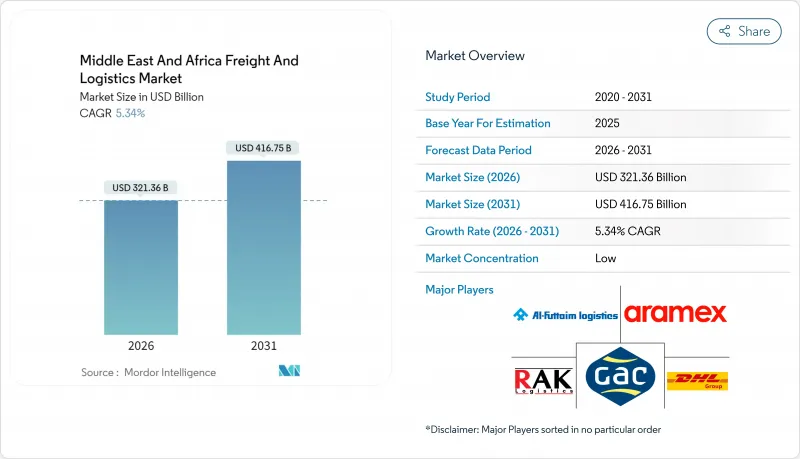

预计到 2026 年,中东和非洲的货运和物流市场规模将达到 3,213.6 亿美元。

这意味着从 2025 年的 3,050.7 亿美元成长到 2031 年的 4,167.5 亿美元,2026 年至 2031 年的年复合成长率(CAGR)为 5.34%。

这一成长前景得益于该地区连接亚洲、欧洲和非洲的战略位置,以及因红海航道中断而推动的大规模基础设施投资和永久性运力扩张。电子商务的扩张、新型多模态走廊的开发以及低温运输需求的激增,正在提升基准和单次货运收入。主权财富基金、自由贸易协定和数位化货运平台在缓解地缘政治波动的同时,也加剧了竞争。那些能够最大限度地提高网路密度、采用先进技术并实践永续的营运商,将有望获得丰厚的回报。

中东及非洲货运物流市场趋势及洞察

电子商务和跨境零售的快速成长

跨境电商正在提升最后一公里配送的频率,其中国内宅配(CEP)占货运量的67.88%,而国际包裹递送预计到2030年将以5.77%的复合年增长率增长。物流业者正在扩展自动化分类中心和多承运商API,这些设施连接杰贝阿里港和阿勒马克图姆国际机场。沿岸地区的营运商正在实施人工智慧路线规划,并与当地大学合作,以应对数位人才短缺的问题。全通路零售商要求整合履约,并将物流量转移到快递网路。

对多模态物流基础设施的巨额投资

沙乌地阿拉伯计划在2030年投资1,333亿美元用于港口、机场和铁路建设,其中包括在NEOM港建设首批全自动起重机的计划,该项目预计将于2026年投入运作。杜拜环球港务集团(DP World)2024年25亿美元的营运规模和创纪录的200亿美元收入,显示了私人资本的大力投入。自动化和可再生能源的整合正在缩短船舶停留时间,改善成本曲线,并重塑转运竞争力。

公路、铁路和港口基础设施不平衡

由于内陆非洲国家依赖沿海门户,基础设施不平衡推高了物流成本。非洲开发银行指出,道路密度不均和通用海上资产资金不足是长期存在的瓶颈问题。公私合营走廊和收费公路融资框架在矿业走廊以外地区吸引的私人资本有限。运输能力集中在少数几个枢纽,增加了其受天气和劳工动盪影响的风险,阻碍了其向内陆市场的渗透。

细分市场分析

2025年,批发和零售贸易占总收入的33.92%,而製造业由于本地化和工业园区的扩张,在2031年之前将以5.58%的复合年增长率实现最快增长。石油、天然气和矿业物流依然规模庞大,这得益于大宗商品分销和能源安全支出。建筑物流受益于大型基础设施计划,而农业和食品运输则在粮食安全战略的推动下不断扩张。

尼日利亚耗资200亿美元的奥吉迪格本工业园区凸显了对专业重型起重和计划货物运输服务的需求。准时制生产需要同步的物料流入,这推动了对即时追踪和预测性库存分析的需求。

截至2025年,货运代理将占中东和非洲货运物流市场59.21%的份额,而宅配、速递和小包裹运输将推动市场成长,到2031年复合年增长率将达到5.57%。公路散装运输将保持其市场地位,而受电子商务的推动,限时小包裹运输将有所增长。货运代理和仓储业将持续稳定成长,其中温控仓储利润率较高。归类于「其他活动」的技术主导附加价值服务将快速扩张,从而推动对端到端数位化整合的需求。

国际货运代理商正投入数十亿美元资金建设其枢纽,而 Aramex 将藉助 ADQ 的支持巩固其区域市场份额。机器人技术和人工智慧库存管理工具将进一步拉动沿岸地区仓库的生产力差距,打造一个集包裹递送、交叉转运和货运代理于一体的平台。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务和跨境零售的快速成长

- 对多模态物流基础设施的大规模投资

- 自由贸易协定(FTA)的扩展和新兴贸易走廊的成长

- 药品和生鲜食品的低温运输需求

- 利用仓库自动化弥补劳力短缺

- 快速采用数位货运平台和即时视觉化工具

- 市场限制

- 道路、铁路和港口基础设施不完善

- 复杂的海关规定和边境延误

- 红海/苏伊士运河瓶颈造成的交通中断

- 司机短缺和本地化政策

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治与疫情的影响

第五章 市场规模与成长预测

- 透过物流功能

- 宅配、特快和小包裹 (CEP)

- 按目的地类型

- 国内的

- 国际的

- 按目的地类型

- 货运代理

- 透过交通工具

- 航空

- 海路和内河航道

- 其他的

- 透过交通工具

- 货物运输

- 透过交通工具

- 航空

- 铁路

- 路

- 海路和内河航道

- 管道

- 透过交通工具

- 仓储和存储

- 透过温度控制

- 非温控型

- 温度控制

- 透过温度控制

- 其他服务

- 宅配、特快和小包裹 (CEP)

- 按最终用户行业划分

- 农业、渔业、林业

- 建造

- 製造业

- 石油天然气、采矿和采石

- 批发和零售

- 其他的

- 按地区

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 卡达

- 阿曼

- 科威特

- 奈及利亚

- 南非

- 其他中东和非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- DHL

- Aramex

- Gulf Agency Company(GAC)

- RAK Logistics

- Al-Futtaim Logistics

- Almajdouie Group

- Gulf Warehousing Company

- RSA Global

- Saudi Transport & Investment Co.(Mubarrad)

- City Logistics

- BLG Logistics

- Kuehne+Nagel

- CEVA Logistics

- DSV

- Rhenus Logistics

- ATC Allied Transport

- Barloworld Logistics

- Unitrans Supply Chain Solutions(Pty)Ltd

- Cargo Carriers(Pty)Limited

- Compass Logistics International

第七章 市场机会与未来展望

Middle East And Africa Freight And Logistics Market size in 2026 is estimated at USD 321.36 billion, growing from 2025 value of USD 305.07 billion with 2031 projections showing USD 416.75 billion, growing at 5.34% CAGR over 2026-2031.

The growth outlook flows from the region's pivotal position linking Asia, Europe, and Africa, combined with heavy infrastructure spending and permanent capacity upgrades triggered by Red Sea shipping disruptions. E-commerce expansion, the rollout of new multimodal corridors, and a surge in cold-chain demand strengthen baseline tonnage and yield per shipment. Sovereign wealth funds, free trade agreements, and digital freight platforms reinforce competitive intensity while mitigating geopolitical volatility. Operators that maximize network density, technology adoption, and sustainable practices are positioned to capture outsized returns.

Middle East And Africa Freight And Logistics Market Trends and Insights

E-commerce boom and cross-border retail

Cross-border e-commerce lifts last-mile shipment frequency, with domestic CEP covering 67.88% of traffic while international CEP advances at a 5.77% CAGR through 2030. Logistics providers are scaling automated sortation hubs and multi-carrier APIs that link Jebel Ali Port to Al Maktoum International Airport. Gulf operators deploy AI routing and collaborate with local universities to fill digital talent gaps. Omnichannel retailers demand integrated fulfillment that merges warehousing, click-and-collect, and door delivery, shifting volume toward express networks.

Mega-investments in multimodal logistics infrastructure

Saudi Arabia earmarked USD 133.3 billion for ports, airports, and railways through 2030, including Port of NEOM's first fully automated cranes slated for 2026 launch. DP World's USD 2.5 billion program and record USD 20 billion 2024 revenue signal deep private capital engagement. Automation and renewable energy integration compress dwell times and improve cost curves, reshaping transshipment competitiveness.

Uneven road, rail, and port infrastructure

Infrastructure gaps raise logistics costs for landlocked African economies relying on coastal gateways. The African Development Bank cites road density disparities and underfunded common-user marine assets as persistent bottlenecks. PPP corridors and toll finance frameworks attract limited private capital outside mining routes. Concentrated capacity in a handful of hubs heightens vulnerability to weather or labor stoppages, stalling hinterland market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Cold-chain demand for pharma and perishables

- Rapid adoption of digital freight platforms and real-time visibility tools

- Red Sea/Suez chokepoint disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wholesale and retail trade contributed 33.92% of 2025 revenue, while manufacturing posts the fastest 5.58% CAGR through 2031 as localization and industrial parks proliferate. Oil, gas, and mining logistics remain sizable, supported by commodity flows and energy security spending. Construction logistics taps infrastructure mega-projects, and agri-food shipments expand under food-security strategies.

Nigeria's USD 20 billion Ogidigben industrial park underscores demand for specialized heavy-lift and project cargo services. Just-in-time production requires synchronized inbound material flows, elevating demand for real-time tracking and predictive inventory analytics

Freight transport retained 59.21% of the Middle East and Africa freight and logistics market in 2025, while courier, express, and parcel leads growth at 5.57% CAGR to 2031. Road-based bulk remains foundational, yet time-definite parcels capture e-commerce tailwinds. Freight forwarding and warehousing post steady gains, and temperature-controlled storage earns premium margins. Technology-driven value-added services under "other" activities scale quickly, feeding demand for end-to-end digital orchestration.

International integrators pledge nine-figure capex for hubs, whereas Aramex leverages ADQ backing to consolidate regional share. Robotics and AI inventory tools widen productivity differentials in Gulf warehouses, creating platforms that fuse parcel delivery, cross-dock, and forwarding under a single interface.

The Middle East and Africa Freight and Logistics Market Report is Segmented by Logistics Function (Freight Forwarding, Freight Transport, and More), End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others), Geography (United Arab Emirates, Saudi Arabia, Nigeria, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL

- Aramex

- Gulf Agency Company (GAC)

- RAK Logistics

- Al-Futtaim Logistics

- Almajdouie Group

- Gulf Warehousing Company

- RSA Global

- Saudi Transport & Investment Co. (Mubarrad)

- City Logistics

- BLG Logistics

- Kuehne + Nagel

- CEVA Logistics

- DSV

- Rhenus Logistics

- ATC Allied Transport

- Barloworld Logistics

- Unitrans Supply Chain Solutions (Pty) Ltd

- Cargo Carriers (Pty) Limited

- Compass Logistics International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Boom and Cross-Border Retail

- 4.2.2 Mega-Investments in Multimodal Logistics Infrastructure

- 4.2.3 Growth of FTAs and Emerging Trade Corridors

- 4.2.4 Cold-Chain Demand for Pharma and Perishables

- 4.2.5 Warehouse Automation to Offset Labour Shortages

- 4.2.6 Rapid Adoption of Digital Freight Platforms and Real-Time Visibility Tools

- 4.3 Market Restraints

- 4.3.1 Uneven Road, Rail and Port Infrastructure

- 4.3.2 Complex Customs Rules and Border Delays

- 4.3.3 Red-Sea/Suez Chokepoint Disruptions

- 4.3.4 Driver Shortages and Localisation Policies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics & Pandemics

5 Market Size & Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Courier, Express, and Parcel (CEP)

- 5.1.1.1 By Destination Type

- 5.1.1.1.1 Domestic

- 5.1.1.1.2 International

- 5.1.1.1 By Destination Type

- 5.1.2 Freight Forwarding

- 5.1.2.1 By Mode of Transport

- 5.1.2.1.1 Air

- 5.1.2.1.2 Sea and Inland Waterways

- 5.1.2.1.3 Others

- 5.1.2.1 By Mode of Transport

- 5.1.3 Freight Transport

- 5.1.3.1 By Mode of Transport

- 5.1.3.1.1 Air

- 5.1.3.1.2 Rail

- 5.1.3.1.3 Road

- 5.1.3.1.4 Sea and Inland Waterways

- 5.1.3.1.5 Pipelines

- 5.1.3.1 By Mode of Transport

- 5.1.4 Warehousing and Storage

- 5.1.4.1 By Temperature Control

- 5.1.4.1.1 Non-Temperatured Control

- 5.1.4.1.2 Temperatured Control

- 5.1.4.1 By Temperature Control

- 5.1.5 Other Services

- 5.1.1 Courier, Express, and Parcel (CEP)

- 5.2 By End User Industry

- 5.2.1 Agriculture, Fishing, and Forestry

- 5.2.2 Construction

- 5.2.3 Manufacturing

- 5.2.4 Oil and Gas, Mining and Quarrying

- 5.2.5 Wholesale and Retail Trade

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 United Arab Emirates

- 5.3.2 Saudi Arabia

- 5.3.3 Qatar

- 5.3.4 Oman

- 5.3.5 Kuwait

- 5.3.6 Nigeria

- 5.3.7 South Africa

- 5.3.8 Rest of Middle East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL

- 6.4.2 Aramex

- 6.4.3 Gulf Agency Company (GAC)

- 6.4.4 RAK Logistics

- 6.4.5 Al-Futtaim Logistics

- 6.4.6 Almajdouie Group

- 6.4.7 Gulf Warehousing Company

- 6.4.8 RSA Global

- 6.4.9 Saudi Transport & Investment Co. (Mubarrad)

- 6.4.10 City Logistics

- 6.4.11 BLG Logistics

- 6.4.12 Kuehne + Nagel

- 6.4.13 CEVA Logistics

- 6.4.14 DSV

- 6.4.15 Rhenus Logistics

- 6.4.16 ATC Allied Transport

- 6.4.17 Barloworld Logistics

- 6.4.18 Unitrans Supply Chain Solutions (Pty) Ltd

- 6.4.19 Cargo Carriers (Pty) Limited

- 6.4.20 Compass Logistics International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告 货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分

货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分 2026-2030年全球货物审核与支付市场

2026-2030年全球货物审核与支付市场 东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)南美货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)南美货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)