|

市场调查报告书

商品编码

1907332

纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

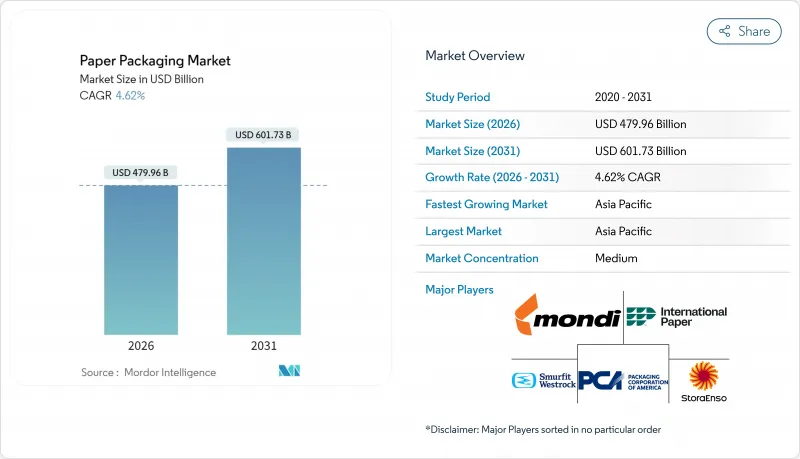

2025年纸包装市场价值为4,588亿美元,预计到2031年将达到6017.3亿美元,而2026年为4799.6亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.62%。

这项扩张的驱动力来自鼓励使用可再生基材的环境法规、线上零售的持续成长以及生物基阻隔涂层的快速发展,这些技术使纸张在防潮和防油性能方面能够与塑胶相媲美。与多层塑胶相比,生产者延伸责任制 (EPR) 的收费系统降低了纤维基材料的合规成本,使生产者从中受益。同时,对奈米纤维素技术的投资有望实现不含 PFAS 的性能,这与美国和欧盟即将逐步淘汰化学物质的目标相符。数位印刷和小批量生产的经济效益推动了供应侧的柔软性,扩大了纸包装市场的潜在规模,使加工商能够以可观的利润承接小批量、高度客製化的宣传活动。

全球纸包装市场趋势与洞察

阻隔涂布纸板解决方案的开发推动了高端应用的发展

基于生物聚合物和奈米纤维素的先进防水、防潮、防油阻隔涂层,在提升纸张性能的同时,也保持了纸张的可回收性。实验室测试表明,纤维素奈米纤维涂层可将氧气透过率降低90%以上,并使纸张的折迭耐久性比未涂层纸板提高一倍。美国食品药物管理局(FDA)已确认,含全氟烷基和多氟烷基物质(PFAS)的防油添加剂已从食品接触市场移除,市场需求转向更安全的化学物质。在欧洲,多家加工商正在迅速提高硼酸盐交联聚乙烯醇涂层的工业化生产能力,这种涂层具有优异的水蒸气阻隔性能,并符合可堆肥标准。随着品牌商寻求在不影响保质期的前提下替代塑胶包装,优质阻隔涂层纸板正成为即食食品、冷冻食品和个人护理礼品包装的标准配置,从而推动纸质包装市场的价值增长。

电子商务对瓦楞纸包装的强劲需求重塑了生产重点。

全球线上零售持续超越实体店面销售,因此每个小包裹都需要能够承受自动化处理的保护性承重外包装。瓦楞纸箱目前估计约占电商出货量的80%,稳固确立了其作为末端物流支柱的地位。预计到2024年,以中国和印度为首的亚洲大型市场将新增数十亿件小包裹,这将推动纸箱工厂的扩张以及为网店安装高速数位印刷生产线。生产结构正转向更轻的瓦楞型材,以在保持抗压强度的同时降低运输成本。为了满足电商需求,综合生产商优先提高箱板纸的产量,而非印刷用纸。这种需求支撑着成熟经济体和新兴经济体纸包装市场的稳定成长。

森林砍伐监测对传统供应链结构构成挑战。

欧盟《森林砍伐条例》要求进口商在2025年底前为所有木质原料提供包裹等级的可追溯性认证。占欧盟特种纸浆进口量60%的美国牛皮纸浆,现在必须包含第三方检验的地理座标。引入卫星监测和监管链审核会增加采购成本,并可能导致运输延误。缺乏先进数据系统的小型造纸厂可能会被拥有认证森林的大型垂直整合企业抢占市场份额,从而改变纸包装市场的竞争格局。随着时间的推移,更严格的原产地规则可能会对供应造成压力,并限制该产业在依赖进口纤维的市场中的成长潜力。

细分市场分析

截至2025年,箱板纸将占纸包装市场54.12%的份额,这主要得益于瓦楞纸包装产业的成熟以及其在电子商务配送中的核心地位。同时,纸板将在各种纤维等级中实现最高的复合年增长率(CAGR),达到7.05%。纸板基纸包装的市场规模预计将会扩大,这反映出高端套筒包装在食品和个人保健产品领域日益增长的需求。加工商正在透过改造閒置的印刷纸生产线,配备适用于固态漂白硫酸盐浆(SBS)和折迭纸盒生产的涂布头,来提高产能运转率。折迭纸盒非常适合高解析度数位印刷,能够提升产品在商店的吸引力。其优异的阻隔阻隔性也使其能够进入冷藏食品领域。同时,箱板纸生产商正在投资研发轻质牛皮纸衬里,以减轻运输重量并提高永续性。混合使用原生材料和再生材料可以优化强度重量比,使箱板纸保持竞争力,从而巩固其在纸包装市场中的领先地位。

纸板的成长潜力正推动欧洲和北美地区资本快速流入,产能迅速扩张,预计2026年运作将超过100万吨。食品接触认证和製药无尘室相容性提升了纸板的吨值,尤其是固态实心纸板。欧盟多个国家对黑色塑胶的限制促使高端糖果甜点和化妆品包装转向白色纸板,进一步刺激了市场需求。奈米黏土等性能增强添加剂可在不影响可回收性的前提下提供防潮性能,从而减少对塑胶薄膜的依赖。随着零售品牌寻求能够体现品质和永续性的单一材料包装,纸板正成为纸包装市场最大的受益者。

到2025年,瓦楞纸箱将占据纸包装市场61.48%的份额,这得益于其无与伦比的防护强度以及在运输、工业和食品分销领域的广泛应用。然而,折迭纸盒预计将以5.12%的复合年增长率成长,超过整体成长速度,这主要得益于个人化图案、快速回应季节性宣传活动以及小批量生产的需求。整合到模切机中的数位列印头缩短了换模时间,并实现了无需高成本库存的大规模客製化。高端化妆品、营养补充剂和植物性食品都青睐折迭纸盒,因为它们具有美观的柔软性和便于上架的特性。

瓦楞纸箱製造商正透过内印刷和高饱和度印刷技术来抢占品牌展示空间,而折迭纸盒则凭藉触感饰面和压纹工艺保持着优势。家电配件正逐渐从塑胶泡壳包装转向带有模塑纤维衬垫的加固纸盒,以吸引永续性的消费者。此外,受柔软性袋启发而开发的创新撕拉条开口设计进一步提升了便利性。这些设计和技术的进步正推动着纸质包装市场份额的稳定成长。

区域分析

预计到2025年,亚太地区将以47.62%的市占率引领纸包装市场,并在2031年之前以5.51%的复合年增长率持续成长。快速的都市化、不断增强的中产阶级购买力以及大规模的食品配送生态系统,都支撑着南亚和东南亚的纤维需求。区域企业正利用成本效益高的综合工厂,将人工林与内部加工设施结合,以缩短面向出口客户的前置作业时间。地方政府透过对节能机械设备提供关税减免,鼓励对永续包装的投资,进一步加速了产能扩张。

北美是创新中心,推动了数位印刷技术的应用,并主导奈米纤维素试点计画的商业化进程。多个州收紧掩埋法规,刺激了对可回收包装的需求,从而支撑了国内箱板纸的需求。美国丰富的软木资源确保了原生纸浆的稳定供应,可与进口的再生纸(OCC)混合使用。同时,欧洲严格的回收目标和生产者延伸责任制(EPR)计画的实施,创造了可预测的政策环境,鼓励设备持续更新换代。德国和斯堪的斯堪地那维亚的造纸厂正越来越多地从石化燃料锅炉转向生物质锅炉,在高能源价格的背景下,减少了范围1排放,并提高了成本竞争力。

拉丁美洲和中东及非洲目前仅占市场份额的一小部分,但这两个地区的成长速度都高于全球平均水平。巴西纸浆生产商正积极融入下游纸板生产环节,以减轻商品週期波动的影响;波湾合作理事会(GCC)成员国则在扩大瓦楞纸板产能,以满足不断增长的电子商务中心的需求。在非洲,不完善的回收网络阻碍了再生纤维的供应,但国际发展计画正在资助试点材料回收设施,为未来的循环经济奠定基础。这些区域趋势巩固了纸包装市场多元化的需求基础,从而增强了其长期韧性。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 开发阻隔涂层纸板解决方案

- 电子商务对瓦楞纸包装的需求不断增长

- 品牌所有者向单一材料包装的转型

- 强制性生产者延伸责任制(EPR)

- 奈米纤维素阻隔技术取得突破

- 加工厂现场数位印刷的经济效益。

- 市场限制

- 对森林砍伐和纤维供应的审查

- 再生纤维价格波动剧烈

- 逐步淘汰 PFAS「永久性化学物质」的代价

- 新兴市场退货流量有限

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 全球再生纸生产统计数据

- 再生纸 - 生产数量

- 再生纸-进口价值和数量

- 再生纸-出口价值和数量

- 再生纸产量 - 主要生产国

- 纸板进出口状况

- 出口(价值和数量)

- 进口(价值和数量)

第五章 市场规模与成长预测

- 按年级

- 纸板

- 固态漂白硫酸盐纸浆(SBS)

- 未漂白硫酸盐纸浆(SUS)

- 折迭板(FBB)

- 涂布再生纸板(CRB)

- 未涂布再生纸板(URB)

- 其他等级的纸板

- 货柜纸板

- 白色牛皮纸衬垫

- 其他牛皮纸衬垫

- 白色顶部测试衬垫

- 其他测试衬垫

- 半化学开槽

- 回收长笛

- 纸板

- 副产品

- 折迭纸箱

- 瓦楞纸箱

- 其他产品

- 按最终用户行业划分

- 食物

- 饮料

- 卫生保健

- 个人护理

- 家居用品

- 电气和电子设备

- 其他终端用户产业

- 按包装类型

- 硬纸板(纸板、厚纸)

- 半硬质(可折迭瓦楞纸箱)

- 柔性纸(小袋、包装纸)

- 模塑纤维和纸浆

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- Packaging Corporation of America

- Stora Enso Oyj

- Graphic Packaging International, LLC

- Nippon Paper Industries Co. Ltd.

- Sonoco Products Company

- Oji Holdings Corporation

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings

- Lee & Man Paper Manufacturing

- Sappi Limited

- Ilim Group

- Klabin SA

- Asia Pulp & Paper(APP)

第七章 市场机会与未来展望

The paper packaging market was valued at USD 458.8 billion in 2025 and estimated to grow from USD 479.96 billion in 2026 to reach USD 601.73 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

This expansion is propelled by environmental regulations that reward recyclable substrates, the continued rise of online retail, and rapid progress in bio-based barrier coatings that let paper compete with plastics on moisture and grease resistance. Producers benefit from Extended Producer Responsibility fee schedules that lower compliance costs for fiber-based materials relative to multilayer plastics. At the same time, investments in nano-cellulose technology promise PFAS-free performance that aligns with looming U.S. and EU chemical phase-outs. Supply-side flexibility, powered by digital printing and smaller batch economics, is enabling converters to serve short-run, highly customized campaigns at attractive margins, expanding addressable volume for the paper packaging market.

Global Paper Packaging Market Trends and Insights

Development of Barrier-Coated Paperboard Solutions Drive Premium Applications

Advanced water-, oxygen-, and grease-barrier coatings based on bio-polymers and nano-cellulose are elevating paper's performance while preserving its recyclability. Laboratory trials show that cellulose nanofibril coatings can reduce oxygen transmission by more than 90% and double folding endurance compared with uncoated board. The U.S. Food & Drug Administration confirmed that grease-proofing agents containing PFAS have exited the food-contact market, shifting demand toward safer chemistries. In Europe, several converters are fast-tracking industrial runs of boric-acid-cross-linked poly(vinyl alcohol) coatings that deliver robust water vapor protection and meet compostability standards. As brand owners pursue plastic replacement without compromising shelf life, premium barrier-coated board is becoming the default for ready-to-eat foods, frozen meals, and personal-care gift packs, boosting value growth in the paper packaging market.

E-Commerce Corrugated Demand Surge Reshapes Production Priorities

Global online retail continues to outperform brick-and-mortar channels, and each parcel requires protective, stackable outer packaging that can withstand automated handling. Corrugated cases now account for an estimated 80% of e-commerce shipments, cementing their role as the workhorse for last-mile logistics. Asian mega-markets led by China and India added double-digit billions of parcels in 2024, prompting box-plant expansions and high-speed digital print lines dedicated to web-shop volumes. The production mix is shifting toward lightweight fluting profiles that cut freight costs yet retain compression strength, and integrated producers are prioritizing incremental containerboard tonnage over graphic paper grades to keep pace with e-commerce pull-through. This demand foundation underpins steady volume growth for the paper packaging market in both mature and emerging economies.

Deforestation Scrutiny Challenges Traditional Supply-Chain Structures

The EU Deforestation Regulation obliges importers to demonstrate plot-level traceability for all wood-based inputs by the end of 2025. U.S. Kraft pulp, representing 60% of EU specialty-grade imports, must now carry geo-coordinates verified by third parties. Implementing satellite monitoring and chain-of-custody audits raises procurement costs and risks of shipment delays. Smaller mills lacking sophisticated data systems may cede share to vertically integrated majors with certified forests, altering competitive balances within the paper packaging market. Over time, tighter provenance rules could squeeze supply and curb the sector's growth potential in markets that rely on imported fiber.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Migration Toward Mono-Material Packaging Architectures

- Extended Producer Responsibility Mandates Accelerate Market Transformation

- Volatile Recycled-Fiber Pricing Creates Margin Compression Pressures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Containerboard held a 54.12% paper packaging market share in 2025, supported by deep corrugated infrastructure and its central role in e-commerce shipping. Meanwhile, cartonboard is registering a 7.05% CAGR, the fastest among fiber grades. The paper packaging market size for cartonboard applications is projected to rise, reflecting premium penetration in food and personal-care sleeves. Converters are refitting idle graphic-paper machines with coating heads suited to Solid Bleached Sulfate and Folding Boxboard production, improving asset utilization. Folding Boxboard's compatibility with high-definition digital print elevates shelf appeal, while dispersion-barrier upgrades enable chilled-food entry. At the same time, containerboard producers are investing in lightweight kraftliner to cut shipping mass, enhancing sustainability credentials. Virgin-recycled blends optimize strength-to-weight ratios and keep containerboard competitive, ensuring it remains the volume backbone of the paper packaging market.

Cartonboard's growth profile attracts capital for rapid European and North American capacity expansions, with start-ups exceeding 1 million tons by 2026. Food-contact certification and pharmaceutical clean-room compliance boost value per ton, particularly for solid-bleached grades. Regulatory bans on black plastics in several EU countries redirect premium confectionery and cosmetic packs to white cartonboard formats, lifting demand further. Performance-enhancing additives such as nano-clays deliver moisture barriers without compromising recyclability, reducing reliance on plastic films. As retail brands demand mono-material packs that convey quality and sustainability, cartonboard emerges as the prime beneficiary within the paper packaging market.

Corrugated boxes occupied 61.48% of the paper packaging market in 2025 owing to their unmatched protective strength and versatility across shipping, industrial, and grocery channels. Folding cartons, however, are forecast to outpace overall growth, expanding at a 5.12% CAGR on the back of personalized graphics, quick-response seasonal campaigns, and smaller lot sizes. Digital printheads integrated into die-cutters reduce changeover times, paving the way for mass-customization without costly inventories. Premium beauty, nutraceuticals, and plant-based foods all favor folding cartons for their aesthetic flexibility and shelf-ready formats.

Corrugated producers respond with inside-print and high-color capabilities to keep hold of branding real estate, but folding cartons maintain an edge in tactile finishes and embossing. Consumer-electronics accessories increasingly shift from plastic clamshells to reinforced cartons married with molded-fiber inserts, capturing sustainability-minded shoppers. Novel tear-strip opening features borrowed from flexible pouches further boost convenience. These design and technology advances underpin steady share migration within the broader paper packaging market.

The Paper Packaging Market Report is Segmented by Grade (Cartonboard [Solid Bleached Sulphate, and More], and Containerboard [White-Top Kraftliner, and More]), Product (Folding Cartons, Corrugated Boxes, and More), End-User Industry (Food, Beverage, Healthcare, Personal Care, Household Care, and More), Packaging Format (Rigid, Semi-Rigid, Flexible, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the paper packaging market with a 47.62% revenue share in 2025 and is projected to record a 5.51% CAGR to 2031. Rapid urbanization, expanding middle-class purchasing power, and large-scale food-delivery ecosystems underpin fiber demand in South and Southeast Asia. Regional players leverage cost-efficient integrated mills that pair plantation forests with in-house converting, shortening lead times for export-oriented customers. Local governments incentivize sustainable-pack investments through duty rebates on energy-efficient machinery, further accelerating capacity additions.

North America remains an innovation nucleus, driving digital-print adoption and spearheading nano-cellulose pilot commercialization. Tightening landfill legislation in several states spurs demand for curbside-recyclable packs, bolstering domestic containerboard offtake. The United States also benefits from abundant softwood resources, ensuring steady virgin-fiber availability to blend with imported OCC. Meanwhile, Europe's stringent recyclability targets and EPR rollouts create a predictable policy environment that favors continuous equipment upgrades. German and Scandinavian mills transition from fossil to biomass boilers, reducing Scope 1 emissions and sharpening cost competitiveness despite high energy prices.

Latin America and the Middle East and Africa collectively hold modest shares today, yet both regions register above-global average growth. Brazilian pulp producers integrate downstream into cartonboard to mitigate commodity cycles, while Gulf Cooperation Council economies add corrugated capacity to serve expanding e-commerce hubs. Africa's underdeveloped collection network hinders recycled-fiber supply, but international development programs are funding pilot materials-recovery facilities, laying groundwork for future circularity. Collectively, these regional trajectories reinforce the diversified demand base that supports the long-term resilience of the paper packaging market.

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- Packaging Corporation of America

- Stora Enso Oyj

- Graphic Packaging International, LLC

- Nippon Paper Industries Co. Ltd.

- Sonoco Products Company

- Oji Holdings Corporation

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings

- Lee & Man Paper Manufacturing

- Sappi Limited

- Ilim Group

- Klabin S.A.

- Asia Pulp & Paper (APP)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Development of barrier-coated paperboard solutions

- 4.2.2 Rise in e-commerce corrugated demand

- 4.2.3 Brand-owner shift toward mono-material packs

- 4.2.4 Extended Producer Responsibility (EPR) mandates

- 4.2.5 Nano-cellulose barrier breakthroughs

- 4.2.6 Converting-plant on-site digital printing economics

- 4.3 Market Restraints

- 4.3.1 Deforestation and fibre-supply scrutiny

- 4.3.2 Volatile recycled-fibre pricing

- 4.3.3 PFAS "forever-chemicals" phase-out costs

- 4.3.4 Limited recovery logistics in emerging markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Global Recovered Paper Production Statistics

- 4.8.1 Recovered Paper - Production Quantity

- 4.8.2 Recovered Paper - Import Value and Quantity

- 4.8.3 Recovered Paper - Export Value and Quantity

- 4.8.4 Recovered Paper Production - Leading Countries

- 4.9 Cartonboard EXIM Scenario

- 4.9.1 Exports (Value and Volume)

- 4.9.2 Imports (Value and Volume)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade

- 5.1.1 Cartonboard

- 5.1.1.1 Solid Bleached Sulphate (SBS)

- 5.1.1.2 Solid Unbleached Sulphate (SUS)

- 5.1.1.3 Folding Boxboard (FBB)

- 5.1.1.4 Coated Recycled Board (CRB)

- 5.1.1.5 Uncoated Recycled Board (URB)

- 5.1.1.6 Other Cartonboard Grades

- 5.1.2 Containerboard

- 5.1.2.1 White-top Kraftliner

- 5.1.2.2 Other Kraftliners

- 5.1.2.3 White-top Testliner

- 5.1.2.4 Other Testliners

- 5.1.2.5 Semi-chemical Fluting

- 5.1.2.6 Recycled Fluting

- 5.1.1 Cartonboard

- 5.2 By Product

- 5.2.1 Folding Cartons

- 5.2.2 Corrugated Boxes

- 5.2.3 Other Products

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare

- 5.3.4 Personal Care

- 5.3.5 Household Care

- 5.3.6 Electrical and Electronics

- 5.3.7 Other End-User Industries

- 5.4 By Packaging Format

- 5.4.1 Rigid (Corrugated, Solid Board)

- 5.4.2 Semi-rigid (Folding Cartons)

- 5.4.3 Flexible Paper (Sachets, Wraps)

- 5.4.4 Molded Fibre and Pulp

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Mondi plc

- 6.4.4 Packaging Corporation of America

- 6.4.5 Stora Enso Oyj

- 6.4.6 Graphic Packaging International, LLC

- 6.4.7 Nippon Paper Industries Co. Ltd.

- 6.4.8 Sonoco Products Company

- 6.4.9 Oji Holdings Corporation

- 6.4.10 Georgia-Pacific LLC

- 6.4.11 Nine Dragons Paper Holdings

- 6.4.12 Lee & Man Paper Manufacturing

- 6.4.13 Sappi Limited

- 6.4.14 Ilim Group

- 6.4.15 Klabin S.A.

- 6.4.16 Asia Pulp & Paper (APP)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

中国纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)亚太地区纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)越南纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

中国纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)亚太地区纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)越南纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球纸瓶市场规模、份额、趋势和成长分析报告(2026-2034年)

全球纸瓶市场规模、份额、趋势和成长分析报告(2026-2034年) 平顶均质机市场:按产品类型、应用、最终用户和分销管道划分 - 全球预测 2026-2032黄油包装材料市场:全球预测(2026-2032 年),按包装材料、包装类型、分销管道和最终用户划分印度纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

平顶均质机市场:按产品类型、应用、最终用户和分销管道划分 - 全球预测 2026-2032黄油包装材料市场:全球预测(2026-2032 年),按包装材料、包装类型、分销管道和最终用户划分印度纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本纸包装市场报告(按类型(折迭纸盒、瓦楞纸箱及其他)、最终用途行业(食品饮料、医疗保健、个人护理和家庭护理、工业及其他)和地区划分,2026-2034年)

日本纸包装市场报告(按类型(折迭纸盒、瓦楞纸箱及其他)、最终用途行业(食品饮料、医疗保健、个人护理和家庭护理、工业及其他)和地区划分,2026-2034年) 纸包装市场规模、份额和成长分析(按材料、类型、等级、最终用途和地区划分):产业预测(2026-2033 年)

纸包装市场规模、份额和成长分析(按材料、类型、等级、最终用途和地区划分):产业预测(2026-2033 年)