|

市场调查报告书

商品编码

1910550

新加坡第三方物流(3PL) 市场:份额分析、产业趋势、统计数据和成长预测 (2026-2031)Singapore 3PL - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

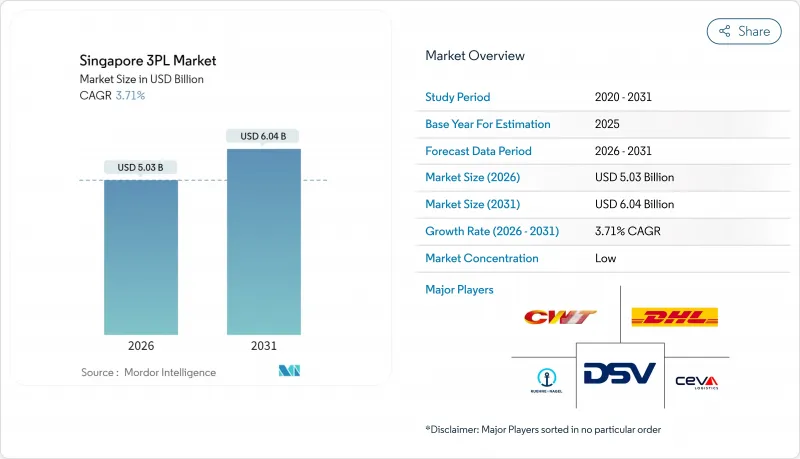

新加坡第三方物流(3PL) 市场在 2025 年的价值为 48.5 亿美元,预计到 2031 年将达到 60.4 亿美元,高于 2026 年的 50.3 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.71%。

新加坡物流业的稳定扩张得益于其无与伦比的多模态能力、65项自由贸易协定网络以及一系列大型基础设施大型企划,这些因素共同巩固了新加坡作为东南亚主要交通和配送中心的地位。电子商务的快速发展推动了生命科学生产对低温运输的需求,而仓储自动化技术的日益普及也扩大了外包物流的目标客户群。同时,混合资产模式降低了服务创新的进入门槛。然而,结构性成本压力——例如土地和人事费用上涨、港口拥堵加剧以及新的碳排放报告要求——正在加剧,这使得规模化、自动化程度高且监管能力强的营运商更具优势。全球物流巨头的策略性收购表明,在新加坡拥有高端业务布局对于建立亚太地区的端到端供应链至关重要。

新加坡第三方物流(3PL) 市场趋势与洞察

国内和跨境电子商务的爆炸性成长

东南亚线上零售的快速成长正在改变人们对履约速度、逆向物流服务和最后一公里配送效率的需求。新加坡占据了相当大的流量,零售商将库存集中在该国,从而能够为该地区6.8亿消费者提供两到三天的配送服务。物流供应商正在扩建小包裹分类线并整合海关API,以更好地处理日益复杂的SKU和退货流程。新加坡邮政投资2,220万美元对其区域电商物流中心进行设施升级,使其处理能力翻了两番,达到每天40万件包裹,凸显了应对措施的资本密集特征。社群经销商和大件商品类别进一步扩大了第三方物流服务商的收入基础。同时,东协内部监管协调的加强正在减少跨境摩擦,从而提升经由新加坡口岸处理的货物量。

政府主导的大型企划(大士大型港口、樟宜货运枢纽)

耗资200亿美元的图阿斯超级港计画于2040年全面完工,年吞吐能力将达到6,500万个标准箱。该港口将配备全自动岸边起重机、无人驾驶车辆和基于人工智慧的泊位调度系统。这些设施将缩短船舶週转时间,并降低物流用户的营运成本。配合樟宜机场的货运基础设施扩建(包括第二个航空货运物流园区),年吞吐能力将从300万吨提升至540万吨。自由贸易区模式,以加快转运週期。这些长期计划,加上地缘政治动盪导致供应链改道需求日益增长,将使新加坡在吸引改道货物方面占据先机,因为邻近港口正面临土地和水深限制。

房地产和人事费用上涨

土地稀缺导致工业用地租金上涨,预计到2025年将达到每平方公尺每月11.8至31.1美元。同时,儘管GDP成长放缓,名目工资仍上涨了5.2%。根据渐进式工资模式,保全人员目前的最低月薪为1,961美元,而零工经济宅配员的强制性退休金缴款则使其总收入增加17%至20%。这些结构性成本因素正在挤压依赖劳力密集仓储营运和末端配送业务的企业的利润空间,加速了自动化技术的普及和部分非核心职能的境外外包。

细分市场分析

截至2025年,国内运输管理将占新加坡第三方物流(3PL)市场的32.65%,反映出在人口稠密、多式联运网路支撑的新加坡岛屿上协调最后一公里配送路线的复杂性。随着零售商对交货期限和即时可视性的需求日益增长,这一细分市场持续稳步发展。加值仓储和配送服务虽然收入基数较小,但预计到2031年将以7.02%的复合年增长率成长,因为营运商希望透过外包套件组装、贴标和退货管理来降低营运资本。高盈利和合约稳定性吸引新进入者,但中级自动化所需的资本投资使现有企业保持了优势。

边缘运算感测器和人工智慧驱动的货架陈列软体将拣货到出货週期缩短了20%,提高了客户的期望值。这推动了对整合运输、仓储和清关的编配平台的需求,这些平台将整合到一个统一的服务等级协定(SLA)中。新加坡、马来西亚和泰国之间跨境卡车运输路线的增加提高了路线密度,这对国际运输管理服务提供者来说是一个好消息。随着混合动力卡车的日益普及,在其仓库网路中整合电池更换设施的公司有望获得更多客户份额,从而巩固新加坡第三方物流(3PL)市场从纯粹运输向综合物流解决方案的结构性转变。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 国内和跨境电子商务的爆炸性成长

- 大型政府主导计划(大士港、樟宜货运枢纽)

- 生命科学和精准医疗领域的低温运输需求

- 东协贸易一体化与新加坡自由贸易网络

- 仓储自动化与机器人竞赛

- 电池换流基础设施能够支援大规模电动车队。

- 市场限制

- 房地产和劳动成本飙升

- 由于需求突然增加,港口和机场出现拥挤

- 第三方物流(3PL) IT 基础架构的网路安全回应成本

- 强制性碳排放报告给中小企业带来的负担

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 新加坡作为东协转运枢纽的角色

- 电子商务产业概况(国内和跨境)

- 新冠疫情及地缘政治事件的影响检验

第五章 市场规模与成长预测

- 透过服务

- 国内运输管理(DTM)

- 路

- 铁路

- 海路

- 水道

- 国际运输管理(ITM)

- 路

- 铁路

- 海路

- 水道

- 加值仓储及配送服务 (VAWD)

- 国内运输管理(DTM)

- 最终用户

- 车

- 能源与公共产业

- 製造业

- 生命科学与医疗保健

- 科技与电子

- 电子商务

- 消费品和日用必需品(快速消费品)

- 食品/饮料

- 其他的

- 透过物流模型

- 轻资产(管理型)

- 资产密集型(拥有车辆和仓库)

- 杂交种

第六章 竞争情势

- 市场集中度分析

- 战略倡议和投资

- 市占率分析

- 公司简介

- DHL Group

- DSV

- CEVA Logistics

- CWT Ltd

- Kuehne+Nagel

- Toll Group

- Nippon Express

- UPS Inc.

- FedEx

- Singapore Post Ltd(SingPost)

- CJ Logistics Asia

- Rhenus Logistics Pte Ltd

- Yang Kee Logistics Pte Ltd

- Ninja Van

- Uparcel

- Kintetsu World Express

- Yusen Logistics

- Nippon Express

- Geodis

- Kerry Logistics

第七章 市场机会与未来展望

The Singapore 3PL Market was valued at USD 4.85 billion in 2025 and estimated to grow from USD 5.03 billion in 2026 to reach USD 6.04 billion by 2031, at a CAGR of 3.71% during the forecast period (2026-2031).

The steady expansion stems from Singapore's unrivaled multimodal connectivity, its network of 65 free-trade agreements, and a pipeline of infrastructure megaprojects that collectively deepen the city-state's role as Southeast Asia's principal transshipment and distribution hub. Rapid e-commerce penetration accelerated cold-chain demand from life-sciences production, and rising adoption of warehouse automation increases the addressable base for outsourced logistics, while hybrid asset models lower entry barriers for service innovation. At the same time, escalating land and labor costs, acute port congestion, and new carbon-reporting mandates add structural cost pressure that rewards operators with scale, automation, and strong regulatory compliance capabilities. Strategic acquisitions by global logistics majors highlight how ownership of premium Singapore footprints is becoming essential for end-to-end Asia-Pacific supply-chain orchestration.

Singapore 3PL Market Trends and Insights

Explosive Growth of Domestic & Cross-Border E-commerce

Southeast Asia's online retail boom is transforming demand profiles for fulfillment speed, reverse-logistics services, and last-mile routing efficiency. Singapore captures outsized volumes because merchants consolidate inventory in the republic to reach 680 million regional consumers in two-to-three-day delivery windows. Logistics providers are scaling parcel-sortation lines and integrating customs-clearance APIs to handle higher SKU complexity and return flows. Singapore Post quadrupled processing capacity to 400,000 parcels daily at its Regional eCommerce Logistics Hub after a USD 22.2 million upgrade, illustrating the capital intensity of this response. Social-commerce sellers and bulky-item categories further broaden the revenue pool for third-party specialists, while regulatory harmonization across ASEAN lowers cross-border friction and boosts volumes handled through Singapore gateways.

Government Megaprojects (Tuas Mega-Port, Changi Cargo Hub)

The USD 20 billion Tuas Mega-Port, slated for full completion by 2040 with 65 million TEU annual capacity, introduces fully automated quay cranes, driverless vehicles, and AI-driven berth scheduling that together compress vessel turnaround times and trim operating costs for logistics users. Parallel expansion of Changi Airport's cargo infrastructure, including a second air-freight logistics park, will lift capacity from 3 million to 5.4 million tons yearly and embed a free-trade zone model that accelerates transshipment cycle times. These long-horizon projects dovetail with supply-chain rerouting caused by geopolitical disruptions, giving Singapore a first-mover advantage in capturing diverted traffic as neighboring gateways confront land and depth constraints.

Escalating Real Estate & Labor Costs

Industrial rents climbed to USD 11.8-31.1 per m2 monthly in 2025 amid land scarcity, while nominal wages advanced 5.2% even as GDP growth lagged. Security officers now earn at least USD 1,961 per month under the Progressive Wage Model, and compulsory pension contributions for gig couriers add a 17-20% payroll burden. These structural cost inflators compress margins for providers relying on labor-intensive warehousing and last-mile fleets, prompting accelerated automation rollouts and selective offshoring of non-core activities.

Other drivers and restraints analyzed in the detailed report include:

- Cold-chain Demand from Life-sciences & Precision Medicine

- ASEAN Trade Integration & Singapore's Free-trade Network

- Port & Airport Congestion from Demand Surges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Domestic Transportation Management accounted for 32.65% of the Singapore third-party logistics market in 2025, reflecting the complexity of orchestrating final-mile routes across a densely populated island supported by multimodal links. The segment continues to grow steadily as retailers push tighter cut-off times and real-time visibility expectations. Value-Added Warehousing & Distribution, while representing a smaller revenue base, is forecast to deliver a 7.02% CAGR through 2031 as merchants outsource kitting, labeling, and returns management to trim working capital. Higher margin profiles and sticky contracts attract new entrants, but the capital spend required for mezzanine-floor automation preserves an edge for incumbents.

Edge-computing sensors and AI-powered slot-assignment software have cut pick-to-ship cycles by 20%, heightening customer expectations and boosting demand for orchestration platforms that bundle transport, warehousing, and customs clearance into a single SLA. Cross-border trucking lanes linking Singapore to Malaysia and Thailand add route density that benefits international transportation management providers. As hybrid electric trucks gain mileage, firms integrating battery-swap nodes within their depot networks stand to capture incremental wallet share, reinforcing the structural shift from pure haulage toward integrated logistics solutions within the Singapore third-party logistics market.

The Singapore Third-Party Logistics (3PL) Market Report is Segmented by Service (Domestic Transportation Management, International Transportation Management, and More), by End User (Automotive, Energy & Utilities, Manufacturing, Life Sciences & Healthcare, Technology & Electronics, E-Commerce, and More), and by Logistics Model (Asset-Light, Asset-Heavy, Hybrid). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Group

- DSV

- CEVA Logistics

- CWT Ltd

- Kuehne + Nagel

- Toll Group

- Nippon Express

- UPS Inc.

- FedEx

- Singapore Post Ltd (SingPost)

- CJ Logistics Asia

- Rhenus Logistics Pte Ltd

- Yang Kee Logistics Pte Ltd

- Ninja Van

- Uparcel

- Kintetsu World Express

- Yusen Logistics

- Nippon Express

- Geodis

- Kerry Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of domestic & cross-border e-commerce

- 4.2.2 Government megaprojects (Tuas Mega-Port, Changi Cargo Hub)

- 4.2.3 Cold-chain demand from life-sciences & precision medicine

- 4.2.4 ASEAN trade integration & Singapore's free-trade network

- 4.2.5 Warehouse-automation & robotics adoption race

- 4.2.6 Battery-swap infrastructure enabling heavy-EV fleets

- 4.3 Market Restraints

- 4.3.1 Escalating real-estate & labour costs

- 4.3.2 Port & airport congestion from demand surges

- 4.3.3 Cyber-security compliance costs for 3PL IT stacks

- 4.3.4 Mandatory carbon-reporting burdens on SMEs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Singapore as ASEAN Trans-shipment Hub

- 4.9 E-commerce Sector Snapshot (Domestic & Cross-border)

- 4.10 Covid-19 Impact Review and Geo-Political Events

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Domestic Transportation Management (DTM)

- 5.1.1.1 Roadways

- 5.1.1.2 Railways

- 5.1.1.3 Airways

- 5.1.1.4 Waterways

- 5.1.2 International Transportation Management (ITM)

- 5.1.2.1 Roadways

- 5.1.2.2 Railways

- 5.1.2.3 Airways

- 5.1.2.4 Waterways

- 5.1.3 Value-Added Warehousing & Distribution (VAWD)

- 5.1.1 Domestic Transportation Management (DTM)

- 5.2 By End User

- 5.2.1 Automotive

- 5.2.2 Energy & Utilities

- 5.2.3 Manufacturing

- 5.2.4 Life Sciences & Healthcare

- 5.2.5 Technology & Electronics

- 5.2.6 E-commerce

- 5.2.7 Consumer Goods & FMCG

- 5.2.8 Food & Beverages

- 5.2.9 Others

- 5.3 By Logistics Model

- 5.3.1 Asset-Light (Management-Based)

- 5.3.2 Asset-Heavy (Own Fleet & Warehouses)

- 5.3.3 Hybrid

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves & Investments

- 6.3 Market-Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 DSV

- 6.4.3 CEVA Logistics

- 6.4.4 CWT Ltd

- 6.4.5 Kuehne + Nagel

- 6.4.6 Toll Group

- 6.4.7 Nippon Express

- 6.4.8 UPS Inc.

- 6.4.9 FedEx

- 6.4.10 Singapore Post Ltd (SingPost)

- 6.4.11 CJ Logistics Asia

- 6.4.12 Rhenus Logistics Pte Ltd

- 6.4.13 Yang Kee Logistics Pte Ltd

- 6.4.14 Ninja Van

- 6.4.15 Uparcel

- 6.4.16 Kintetsu World Express

- 6.4.17 Yusen Logistics

- 6.4.18 Nippon Express

- 6.4.19 Geodis

- 6.4.20 Kerry Logistics

7 Market Opportunities & Future Outlook

2026年全球第三方物流(3PL)市场报告

2026年全球第三方物流(3PL)市场报告 2026-2030年全球汽车第三者物流市场

2026-2030年全球汽车第三者物流市场 第三方物流软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分

第三方物流软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分 美国第三方物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)英国第三方物流(3PL):市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙第三方物流(3PL) 市场:份额分析、产业趋势与统计、成长预测 (2026-2031)

美国第三方物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)英国第三方物流(3PL):市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙第三方物流(3PL) 市场:份额分析、产业趋势与统计、成长预测 (2026-2031) 第三方物流全球市场规模、份额、趋势和成长分析报告(2026-2034)

第三方物流全球市场规模、份额、趋势和成长分析报告(2026-2034) 生物製药低温运输物流服务市场按服务类型、温度类型、运输方式、产品类型、包装类型和最终用途划分,全球预测(2026-2032年)日本第三方物流(3PL)市场:份额分析、产业趋势、统计数据和成长预测(2026-2031)

生物製药低温运输物流服务市场按服务类型、温度类型、运输方式、产品类型、包装类型和最终用途划分,全球预测(2026-2032年)日本第三方物流(3PL)市场:份额分析、产业趋势、统计数据和成长预测(2026-2031) 第三方物流市场-全球产业规模、份额、趋势、机会及预测(依运输方式、服务类型、产业、地区及竞争格局划分,2021-2031年预测)

第三方物流市场-全球产业规模、份额、趋势、机会及预测(依运输方式、服务类型、产业、地区及竞争格局划分,2021-2031年预测)