|

市场调查报告书

商品编码

1940673

英国第三方物流(3PL):市场占有率分析、产业趋势与统计、成长预测(2026-2031)United Kingdom Third Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

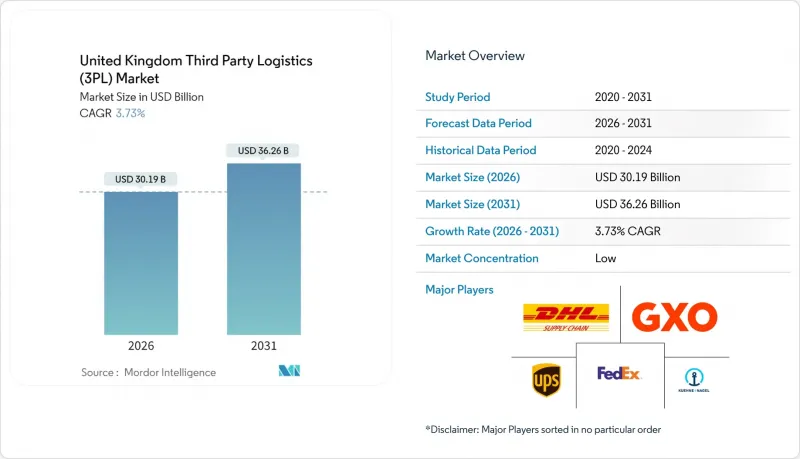

英国第三方物流市场预计将从 2025 年的 291 亿美元成长到 2026 年的 301.9 亿美元,到 2031 年达到 362.6 亿美元,2026 年至 2031 年的复合年增长率为 3.73%。

市场规模的变化反映了该行业从快速扩张向稳步成熟过渡的过程,其驱动因素包括英国脱欧相关的海关摩擦、日益深化的电子商务文化、政府的脱碳政策以及持续的劳动力短缺。企业纷纷转向外包物流合作伙伴,因为第三方物流(3PL) 可以吸收监管衝击、整合技术投资,并大规模提供低碳运输方案。随着国际公司收购本地专业公司以确保港口准入和都市区仓储网络,竞争日益激烈,而国内公司则透过自动化和电动车队来应对。公路、铁路和卡车停靠站基础设施的发展带来了新的运输能力,但也给营运商带来了更大的压力,他们需要满足消费者对直销服务日益增长的期望。这些因素共同构成了一个市场基础,在这个市场中,韧性和柔软性决定企业的长期成功。

英国第三方物流(3PL) 市场趋势与洞察

电子商务小包裹量爆炸性成长

如今,线上零售已占英国购物总量的30%。订单频率的激增迫使第三方物流公司在都市区扩展微型仓配中心,亚马逊的「计划 Juniper」网路便是例证,该网路已将配送时间缩短至数小时。 DPD集团英国公司已在米尔顿凯恩斯完成了超过2500次自主「最后一公里」配送,这表明机器人技术能够满足商业级服务合约的要求。伦敦的Portal Way位置260个“黑暗厨房”,这表明快速商业模式正在重塑仓储需求。随着零售商优先考虑全通路能力,那些将B2B分销与小包裹消费者配送相结合的供应商正在获得更高的合约价值和更长期的合作协议。

政府为货运提供脱碳奖励

政府已拨款2.54亿美元用于零排放重型货车(HGV)试点项目,目标是在2040年前逐步淘汰新型柴油卡车。领先已获得竞标优势,例如,HIVED公司订购了11辆配备600千瓦时电池、续航里程达310英里的梅赛德斯-奔驰eActros电动卡车,以扩充其全电动中程运输车队。此外,政府还将投入2,096万美元维修38个卡车停靠站,包括配备大容量充电桩和扩建驾驶设施,以缓解电动卡车的里程焦虑。由于低温运输运输每年排放1,410万吨二氧化碳当量,温控电气化已成为监管重点。 ISO 14001认证正逐渐成为公共部门竞标的必要条件,这将形成一种机制,奖励那些早期投资永续资产的第三方物流(3PL)供应商。

司机和仓库工人短缺

英国国内重型货车驾驶人缺口高达5万人,限制了英国第三方物流市场的扩张速度,目前供应量为32万人,而需求量为37万人。驾驶人平均年龄为51岁,其中55%的司机年龄在50至65岁之间,这意味着离职率正在上升。人事费用占第三方物流营运成本的40%以上,自2024年初以来大幅上涨,当时19%的公司表示有职缺。一项2096万美元的基金旨在对38个卡车停靠站进行现代化改造,以提高该工作的吸引力,但伦敦和曼彻斯特不断上涨的住宅成本阻碍了新员工的招聘。英国脱欧后,欧盟工人大量外流,加剧了仓库劳动力短缺的问题,迫使第三方物流公司转向机器人和人工智慧驱动的货位管理。

细分市场分析

到2025年,英国国内运输管理将占英国第三方物流市场规模的41.45%,反映了该岛国以公路运输为主的货运模式。国际运输管理对于跨境贸易仍然至关重要,但由于关税波动带来的挑战,利润率面临压力。随着电子商务客户将高价值的拣货包装、退货处理和套件组装等业务外包,增值仓储和配送服务正以7.01%的复合年增长率快速成长。自动化仓库系统、温控仓库和一体化清关区域的引入,正将仓库从成本中心转变为盈利枢纽。儘管政府斥资1168亿美元发展公路和铁路,为多式联运创造了机会,但由于都市区消费丛集集中在主要公路沿线,第三方物流(3PL)在2031年之前仍将在英国道路运输保持主导地位。铁路和短途海运营运商将专注于需要大宗货物运输的可再生能源计划,与公路运输形成互补而非替代关係。

企业对仓储的日益依赖重塑了合约结构。客户要求采用与订单行数挂钩的可变成本定价模式,这与机器人拣选的扩充性。随着对气候敏感的食品和药品分销范围的扩大,低温运输设施将获得更高的利益。自动化降低了劳动力需求,营运商正将人员重新部署到更高价值的配置管理和品质检验任务中。将预测分析融入库存管理的第三方物流业者将获得优先供应商地位,进而强化产业整合趋势。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务小包裹处理量呈爆炸性成长

- 政府为货运提供脱碳奖励

- 仓库自动化与机器人

- 英国脱欧后,对近岸外包和海关整合第三方物流的需求增加。

- 订阅式D2C模式需要微型仓配

- 产品安全法规促进安全物流

- 市场限制

- 司机和仓库工人短缺

- 与英国脱欧相关的海关摩擦和文书工作

- 重型货车 (HGV) 充电基础设施和电网容量限制对车队电气化的影响

- 物流地产税增加(自2026年起重新评估后)

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 仓储市场趋势

- 来自 CEP、最后一公里和低温运输的需求

- 电子商务洞察

- 新冠疫情的影响及疫情后的重组

第五章 市场规模与成长预测

- 透过服务

- 国内运输管理(DTM)

- 路

- 铁路

- 空运

- 水道

- 国际运输管理(ITM)

- 路

- 铁路

- 空运

- 水道

- 加值仓储及配送服务 (VAWD)

- 国内运输管理(DTM)

- 最终用户

- 车

- 能源与公共产业

- 製造业

- 生命科学与医疗保健

- 科技与电子

- 电子商务

- 消费品和日用必需品(快速消费品)

- 食品/饮料

- 其他的

- 透过物流模型

- 轻资产(管理基础)

- 资产密集型(拥有车辆和仓库)

- 杂交种

- 英国地区

- 英格兰

- 苏格兰

- 威尔斯

- 北爱尔兰

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- DHL Group

- Kuehne+Nagel

- GXO Logistics

- FedEx

- United Parcel Service, Inc.

- DSV

- CEVA Logistics

- Yusen Logistics

- Rhenus Logistics

- Eddie Stobart Logistics

- Xpediator

- Bibby Distribution

- Torque Logistics

- Pointbid Logistics

- XPO Logistics

- Culina Group

- Geodis

- Parcel Hub

- Evri(Formerly Hermes)

- Walker Logistics

第七章 市场机会与未来展望

The United Kingdom Third Party Logistics Market is expected to grow from USD 29.10 billion in 2025 to USD 30.19 billion in 2026 and is forecast to reach USD 36.26 billion by 2031 at 3.73% CAGR over 2026-2031.

The market size trajectory reflects the sector's gradual move from rapid expansion to steady maturation, shaped by Brexit-related customs friction, a deepening e-commerce culture, government decarbonization mandates, and persistent labor shortages. Businesses are migrating toward outsourced logistics partners because 3PLs can absorb regulatory shocks, aggregate technology investments, and deliver lower-carbon transport options at scale. Competitive intensity is rising as international players buy local specialists to secure port access and urban warehousing footprints, while domestic firms counter with automation and electric-fleet rollouts. Infrastructure upgrades across roads, rail, and truck stops provide new capacity yet also pressure operators to meet rising service expectations in direct-to-consumer fulfillment. Together, these forces underpin a market where resilience and flexibility determine long-term success.

United Kingdom Third Party Logistics (3PL) Market Trends and Insights

Explosive E-commerce Parcel Volumes

Online retail now represents 30% of all U.K. shopping. Rapid ordering frequencies compel 3PLs to enlarge urban micro-fulfillment footprints, evidenced by Amazon's Project Juniper network that cuts delivery windows to hours. DPD Group UK has already completed more than 2,500 autonomous last-mile deliveries in Milton Keynes, proving robotics can meet commercial service-level agreements. London's Portal Way hosts 260 dark kitchens that illustrate how quick-commerce models reshape warehousing demand. As retailers favor omnichannel fulfillment, operators that marry B2B distribution with direct-to-consumer parcel flows secure higher contract values and longer tenures.

Government Decarbonization Incentives for Freight

The government has earmarked USD 254 million for zero-emission HGV trials and set a 2040 deadline for phasing out new diesel trucks. Early movers gain bidding advantages; HIVED expanded its fully electric middle-mile fleet by ordering 11 Mercedes-Benz eActros units with 600 kWh batteries capable of 310-mile ranges. A further USD 20.96 million upgrade of 38 truck stops introduces high-capacity chargers and improved driver amenities, lowering range-anxiety barriers for electric haulage. Cold-chain transport emits 14.1 MtCO2e annually, making temperature-controlled electrification a regulatory priority. ISO 14001 certification is becoming table stakes in public-sector tenders, thereby rewarding 3PLs that invest early in sustainable assets.

Driver & Warehouse-Labor Shortage

The country is short 50,000 HGV drivers, with supply at 320,000 against demand for 370,000, limiting the expansion pace of the United Kingdom's third-party logistics market. The average driver age is 51, and 55% are within 50-65, signaling worsening attrition. Labor costs absorb more than 40% of 3PL operating spend and rose sharply after 19% of firms reported vacancies in early 2024. A USD 20.96 million fund to modernize 38 truck stops aims to improve job attractiveness, yet high housing costs in London and Manchester deter recruits. Warehouse labor gaps compound the issue as EU workers depart post-Brexit, pushing 3PLs toward robots and AI-driven slotting.

Other drivers and restraints analyzed in the detailed report include:

- Warehouse Automation & Robotics Adoption

- Post-Brexit Near-Shoring & Customs-Integrated 3PL Demand

- Brexit-Related Customs Friction & Paperwork

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The United Kingdom's third-party logistics market size attributable to Domestic Transportation Management stood at 41.45% share in 2025, mirroring the island nation's road-centric freight patterns. International Transportation Management remains critical for cross-border trade but wrestles with customs-driven volatility that depresses margins. Value-Added Warehousing & Distribution is accelerating at 7.01% CAGR as e-commerce clients outsource high-touch pick-pack, returns, and kitting tasks. Automated storage systems, climate-controlled chambers, and integrated customs areas turn warehouses into revenue-rich nodes rather than cost centers. Government road and rail upgrades worth USD 116.8 billion unlock intermodal plays, but the United Kingdom's third-party logistics market share for roads stays dominant through 2031 because urban consumption clusters hug motorway spines. Rail and short-sea players niche into renewable-energy projects requiring oversized-cargo moves, complementing rather than displacing trucking.

Growing enterprise reliance on warehousing has re-shaped contract structures. Clients demand variable-cost pricing tied to order lines, which suits the scalable nature of robotic picking. Cold-chain facilities earn premiums as climate-sensitive food and pharmaceutical flows expand. As automation compresses labor needs, operators redeploy headcount into value-added configuration and quality-check tasks. 3PLs that layer predictive analytics on inventory get preferred-supplier status, reinforcing consolidation trends.

The United Kingdom Third-Party Logistics Market Report is Segmented by Service (Domestic Transportation Management, International Transportation Management, and More), by End User (Automotive, Energy & Utilities, Manufacturing, Life Sciences & Healthcare, and More), by Logistics Model (Asset-Light, Asset-Heavy, Hybrid), and by Region (England, Scotland, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Group

- Kuehne + Nagel

- GXO Logistics

- FedEx

- United Parcel Service, Inc.

- DSV

- CEVA Logistics

- Yusen Logistics

- Rhenus Logistics

- Eddie Stobart Logistics

- Xpediator

- Bibby Distribution

- Torque Logistics

- Pointbid Logistics

- XPO Logistics

- Culina Group

- Geodis

- Parcel Hub

- Evri (Formerly Hermes)

- Walker Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive e-commerce parcel volumes

- 4.2.2 Government decarbonisation incentives for freight

- 4.2.3 Warehouse automation & robotics adoption

- 4.2.4 Post-Brexit near-shoring & customs-integrated 3PL demand

- 4.2.5 Subscription D2C models requiring micro-fulfilment

- 4.2.6 Product-security legislation boosting secure logistics

- 4.3 Market Restraints

- 4.3.1 Driver & warehouse-labour shortage

- 4.3.2 Brexit-related customs friction & paperwork

- 4.3.3 HGV-charging & grid-capacity limits for fleet electrification

- 4.3.4 Logistics-property tax rise (post-2026 revaluation)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Warehousing Market Trends

- 4.9 Demand from CEP, Last-mile, Cold-chain

- 4.10 Ecommerce Insights

- 4.11 Impact of COVID-19 & Post-pandemic Reset

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Domestic Transportation Management (DTM)

- 5.1.1.1 Roadways

- 5.1.1.2 Railways

- 5.1.1.3 Airways

- 5.1.1.4 Waterways

- 5.1.2 International Transportation Management (ITM)

- 5.1.2.1 Roadways

- 5.1.2.2 Railways

- 5.1.2.3 Airways

- 5.1.2.4 Waterways

- 5.1.3 Value-Added Warehousing & Distribution (VAWD)

- 5.1.1 Domestic Transportation Management (DTM)

- 5.2 By End User

- 5.2.1 Automotive

- 5.2.2 Energy & Utilities

- 5.2.3 Manufacturing

- 5.2.4 Life Sciences & Healthcare

- 5.2.5 Technology & Electronics

- 5.2.6 E-commerce

- 5.2.7 Consumer Goods & FMCG

- 5.2.8 Food & Beverages

- 5.2.9 Others

- 5.3 By Logistics Model

- 5.3.1 Asset-Light (Management-Based)

- 5.3.2 Asset-Heavy (Own Fleet & Warehouses)

- 5.3.3 Hybrid

- 5.4 By UK Region

- 5.4.1 England

- 5.4.2 Scotland

- 5.4.3 Wales

- 5.4.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne + Nagel

- 6.4.3 GXO Logistics

- 6.4.4 FedEx

- 6.4.5 United Parcel Service, Inc.

- 6.4.6 DSV

- 6.4.7 CEVA Logistics

- 6.4.8 Yusen Logistics

- 6.4.9 Rhenus Logistics

- 6.4.10 Eddie Stobart Logistics

- 6.4.11 Xpediator

- 6.4.12 Bibby Distribution

- 6.4.13 Torque Logistics

- 6.4.14 Pointbid Logistics

- 6.4.15 XPO Logistics

- 6.4.16 Culina Group

- 6.4.17 Geodis

- 6.4.18 Parcel Hub

- 6.4.19 Evri (Formerly Hermes)

- 6.4.20 Walker Logistics

7 Market Opportunities & Future Outlook

第三方化学品分销市场:依产品类型、实体形态、服务及最终用途产业划分-2026-2032年全球市场预测第三方物流(3PL) 软体市场:2026-2032 年全球市场预测(按应用、部署类型、服务类型、组织规模和最终用户产业划分)

第三方化学品分销市场:依产品类型、实体形态、服务及最终用途产业划分-2026-2032年全球市场预测第三方物流(3PL) 软体市场:2026-2032 年全球市场预测(按应用、部署类型、服务类型、组织规模和最终用户产业划分) 第三方化学品分销市场:按类型、应用和地区划分(2026-2034 年)第三方物流市场:依产品/服务、服务模式、定价模式、运输方式、应用领域及最终用户产业划分-2026-2032年全球市场预测

第三方化学品分销市场:按类型、应用和地区划分(2026-2034 年)第三方物流市场:依产品/服务、服务模式、定价模式、运输方式、应用领域及最终用户产业划分-2026-2032年全球市场预测 2026年全球第三方物流(3PL)市场报告

2026年全球第三方物流(3PL)市场报告 2026-2030年全球汽车第三者物流市场

2026-2030年全球汽车第三者物流市场 第三方物流软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分

第三方物流软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分 美国第三方物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙第三方物流(3PL) 市场:份额分析、产业趋势与统计、成长预测 (2026-2031)

美国第三方物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙第三方物流(3PL) 市场:份额分析、产业趋势与统计、成长预测 (2026-2031) 第三方物流全球市场规模、份额、趋势和成长分析报告(2026-2034)

第三方物流全球市场规模、份额、趋势和成长分析报告(2026-2034)