|

市场调查报告书

商品编码

1910801

菲律宾瓷砖市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Philippines Ceramic Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

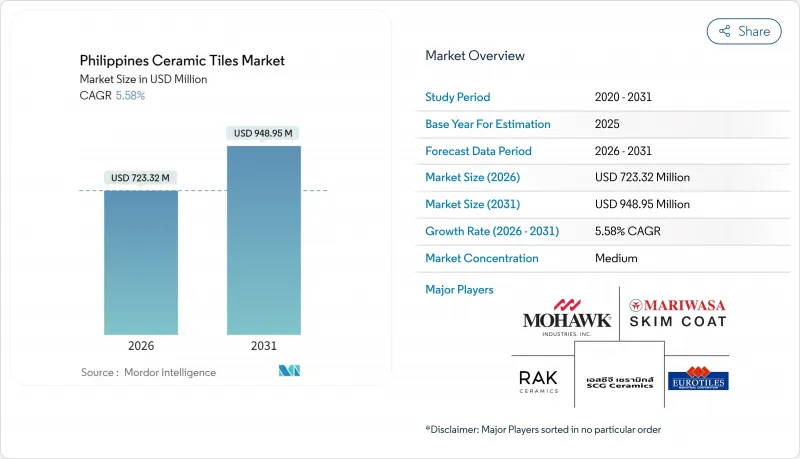

预计菲律宾瓷砖市场将从 2025 年的 6.851 亿美元增长到 2026 年的 7.2332 亿美元,并预计到 2031 年将达到 9.4895 亿美元,2026 年至 2031 年的复合年增长率为 5.58%。

公共基础设施的扩建、持续的住宅维修以及消费者对耐用型地面铺装材料偏好,共同支撑了这一增长趋势。然而,生产商也面临能源成本波动和进口压力等挑战。本地企业正透过节能窑炉、喷墨列印技术和拓展分销网络等措施应对这些不利因素,并透过「建设更美好、更多」计画来保障利润并维持市场需求。中维萨亚斯和棉兰老岛地区的消费溢出效应正在扩大马尼拉大都会区以外的潜在需求,显示计划储备正朝着健康多元化的方向发展。同时,疫情期间的卫生问题也加速了大尺寸瓷砖的普及,这种瓷砖更易于清洁且缝隙更少,进一步强化了菲律宾瓷砖市场的优质化趋势。

菲律宾瓷砖市场趋势与洞察

疫情后住宅建设復苏

政府的住宅政策(55个计划,17万套住房)刺激了菲律宾瓷砖市场的劳动力需求和材料采购。宿雾的住宅市场正经历销售成长,这主要得益于海外劳工汇款,这些汇款推动了中檔公寓的销售,并增加了浴室和起居空间中瓷砖的使用。像宿雾地产(Cebu Landmasters)这样的开发商约占中维萨亚斯地区新建公寓供应量的三分之一,计划开发21个新计画,总价值达披索,这些项目将需要大量的瓷砖。在东维萨亚斯地区,建筑许可证的价值年增5.4%,推动住宅的平均成本达到每平方公尺披索,维持了陶瓷装饰材料的基本消耗。预计全国将出现1000万套住宅的供不应求,这为菲律宾瓷砖市场未来多年的住宅需求前景提供了支撑。

扩大商业和非住宅建筑

商业和非住宅建设活动的成长是瓷砖市场的主要驱动力。越来越多的专业设计师和建筑师指定瓷砖作为非住宅地板材料,也印证了这一点。菲律宾各类公共、工业及商业设施的开发与建设,显着提升了对磁砖的需求。瓷砖因其耐用性而备受青睐,尤其是在人流量大的区域,即使在高强度使用下也能保持美观。农业设施、教育机构和工业园区的扩建,进一步扩大了瓷砖的应用范围。

商业领域的成长与现代商业环境中日益增长的设计需求相辅相成。不断扩张的瓷砖市场和特色瓷砖品牌细分市场创造了巨大的商机,这主要得益于瓷砖品牌专卖店的兴起,这些专卖店在一个展示室内提供丰富的产品系列。线上比价工具和扩增实境(AR)应用等技术的进步进一步推动了这一趋势,客户可以使用智慧型手机直接在施工现场预览设计方案,从而做出明智的决策,简化商业计划的选材和安装流程。

电力价格上涨给国内生产商带来压力

能源成本约占生产成本的三分之一,而窑炉製造的成本会随着马尼拉电力公司 (MERALCO) 调整发电价格而每月重新计算。与泰国和越南的同行相比,菲律宾工厂每千瓦时电费更高,这阻碍了规模经济,也抑制了出口。随着菲律宾的液化天然气 (LNG) 产能扩大 200%,对 LNG 的依赖程度将加深,将长期成本波动纳入陶瓷烧製预算。小规模工厂在安装现代化窑炉和汽电共生设备方面面临资金筹措挑战,其较低的利润率也增加了电价上涨和货币贬值时破产的风险。持续的成本压力可能导致产能整合,从而降低菲律宾瓷砖市场的供应多样性。

细分市场分析

到2025年,陶瓷瓷砖将占菲律宾瓷砖市场收入份额的54.85%,这反映了全球瓷砖耐用性标准以及菲律宾消费者对高端饰面的长期信赖。喷墨技术持续推动这一细分市场的发展,该技术无需维护即可复製大理石和木材的视觉效果,从而巩固了中高收入住宅对品牌的忠诚度。马赛克瓷砖虽然仍属于小众市场,但预计将以5.74%的复合年增长率增长,这主要得益于特色墙的安装以及将当地工艺融入现代室内设计的传统工艺復兴计划。由于防滑性能,无釉和釉药陶瓷在实用区域将继续保持其受欢迎程度,而其他装饰系列,例如手绘和图案表面,将满足旅游业主导的纪念品需求。生产商正在将窑炉运作重新分配给瓷器生产,随着注重设计的买家愿意支付溢价,预计在进口压力不断增加的情况下,大众市场SKU的利润率将有所提高。

瓷砖的强势地位也得益于其经济实惠的拥有成本。其超过25年的使用寿命和低吸水率意味着更少的更换频率,满足了在区域城市建造出租物业的投资者的需求。虽然进口产品曾经主导高端市场,但如今国产产品已能提供媲美欧洲美学的品质,缩短了交货时间,并降低了计划业主面临的外汇风险。马赛克瓷砖的流行反映了酒店整修中对定制浴室日益增长的需求,这些浴室注重打造适合拍照的背景。市场细分錶明,即使马赛克瓷砖正在探索新的收入来源,瓷砖在菲律宾瓷砖市场也不太可能失去市场份额。生产重点表明,资本正集中于大尺寸瓷砖生产线,这些生产线可以轻鬆切换亮面、哑光和纹理饰面。

到2025年,地板材料铺设将占总需求的51.62%,这主要得益于马尼拉大都会老旧公寓的翻新以及地方政府预算资助的新学校建设。由于耐用性要求,陶瓷表面成为购物中心、交通枢纽和医疗机构走廊的主要饰面材料,这些场所每天可承受超过5000人次的客流量。屋顶应用虽然正在兴起,但预计将以5.63%的复合年增长率成为成长最快的领域,这主要得益于气候智慧型建筑标准下对防水和太阳能反射瓷砖的需求不断增长。墙壁材料应用将保持个位数的温和增长,因为开发商在备餐厨房和卫生间等场所寻求卫生、易于消毒的表面,以取代容易滋生霉菌的油漆。应用领域的多元化将使收入来源多样化,并保护生产商免受菲律宾整体瓷砖市场特定行业週期性低迷的影响。

住宅装修商在厨房维修倾向于选择防滑瓷砖,而商业地产业主则优先考虑防污瓷砖,以降低多年合约期间的清洁成本。防水屋顶瓦吸水率低,并配有机械锚固件,因此适用于比科尔和东维萨亚斯等颱风多发地区。教育机构正在推广使用防接触表面以应对新冠疫情,并将乙烯基地板材料更换为能够耐受强效消毒剂的瓷砖。交通枢纽(如克拉克机场、MRT-7、宿雾BRT)在其候车大厅铺设了耐磨等级为PEI IV和V的瓷质砖,订单量庞大。这些趋势表明,地板材料将继续占据菲律宾瓷质砖市场的大部分份额,而新兴的屋顶规范将创造一个前景广阔的相邻市场。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 疫情后住宅建设復苏

- 政府的「建设更好、建设更多」基础建设计划

- 对大尺寸瓷砖的需求不断增长

- 零售连锁店在区域城市的扩张

- 节能型窑炉可降低单位成本

- 马尼拉大都会区地面装饰材料绿建筑强制规定

- 市场限制

- 电力价格上涨给国内生产商带来压力

- 液化天然气价格波动推高燃料成本

- 来自中国和越南的进口渗透率不断提高

- 农村地区技术纯熟劳工短缺

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解近期产业发展动态(新产品发布、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模及成长预测(金额:美元)

- 依产品类型

- 陶瓷瓷砖

- 釉药磁砖

- 无釉陶瓷砖

- 马赛克瓷砖

- 其他(装饰瓷砖、图案瓷砖、手工瓷砖)

- 透过使用

- 地板材料

- 墙

- 屋顶材料

- 最终用户

- 住宅

- 商业的

- 饭店业(饭店、度假村)

- 零售店

- 办公室和机构

- 卫生保健

- 教育设施

- 交通枢纽(机场、捷运、客运站)

- 其他商业用户

- 依建筑类型

- 新建工程

- 维修和更换

- 透过分销管道

- 磁砖和石材专卖店

- 居家装潢和DIY专卖店

- 线上零售

- 直接向承包商销售

- 按地区

- 吕宋岛

- 维萨扬群岛

- 棉兰老岛

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mariwasa Siam Ceramics Inc.

- Eurotiles Industrial Corporation

- SCG Ceramics(COTTO)

- RAK Ceramics PJSC

- PORCELANOSA Grupo

- Mohawk Industries Inc.(Daltile)

- Kajaria Ceramics Ltd.

- China Ceramics Co. Ltd.

- Guangdong Dongpeng Ceramic Co., Ltd.

- Pamesa Ceramica

- Grupo Lamosa

- HRD Singapore Pte Ltd(Niro Granite)

- Italgraniti Group

- Atlas Concorde SpA

- FC Tile Depot

- ABC Tile Center

- Wilcon Depot Inc.

- Cebu Home and Builders Centre

- Tile Express Shop

- Royal Tern Ceramics

第七章 市场机会与未来展望

The Philippines ceramic tiles market is expected to grow from USD 685.1 million in 2025 to USD 723.32 million in 2026 and is forecast to reach USD 948.95 million by 2031 at 5.58% CAGR over 2026-2031.

Expansion of public infrastructure, steady residential upgrades, and rising preference for durable floor finishes underpin this trajectory, even as producers grapple with volatile energy costs and import pressure. Domestic players are countering headwinds through energy-efficient kilns, ink-jet printing, and wider distribution footprints that help protect margins and sustain demand pull from the Build Better More program. Regional spending spillovers in Central Visayas and Mindanao are broadening addressable demand beyond Metro Manila, signaling healthy diversification in project pipelines. Simultaneously, pandemic-era hygiene concerns have accelerated the adoption of large-format porcelain slabs that promise easier cleaning and fewer grout lines, reinforcing premiumization trends in the Philippines' ceramic tiles market.

Philippines Ceramic Tiles Market Trends and Insights

Post-pandemic Residential Construction Rebound

Government-backed housing initiatives targeting 170,000 units across 55 projects are reviving labor demand and material procurement in the Philippines ceramic tiles market. Cebu's residential sector shows rising turnover as overseas Filipino workers channel remittances into mid-priced condominiums that typically specify ceramic tiles for wet areas and living spaces. Developers such as Cebu Landmasters hold roughly one-third share of condominium launches in Central Visayas and have scheduled 21 new projects collectively worth PHP 31.5 billion that will require extensive tile packages. Across Eastern Visayas, the value of building permits rose 5.4% year-on-year, and average residential construction costs hit PHP 9,151 per square meter, sustaining baseline consumption of ceramic finishes. A projected 10 million-unit national housing backlog underpins multi-year visibility for residential demand in the Philippines ceramic tiles market.

Expanding Commercial and Non-residential Construction

The growth in commercial and non-residential construction activities has become a significant driver for the ceramic tiles market, supported by the increasing presence of professional designers and architects who specify porcelain ceramic tiles for non-residential flooring applications. The development of various institutional, industrial, and commercial facilities has created substantial demand for ceramic floor tiles Philippines, with these materials being particularly valued for their ability to withstand heavy foot traffic and maintain their appearance in high-use areas. The expansion of agricultural facilities, educational institutions, and industrial complexes has further diversified the application base for ceramic tiles.

The commercial sector's growth is complemented by the rising sophistication of design requirements in modern business environments. The expanding ceramic tile market and dedicated tiles brand sector have created significant opportunities, with an increasing number of tiles brand name stores offering diverse product portfolios in single showrooms. This trend has been further enhanced by technological advancements such as online price comparison tools and augmented reality applications, allowing customers to make informed decisions and visualize designs directly at construction sites using smartphones, thereby streamlining the selection and installation process for commercial projects.

High Electricity Tariffs Squeezing Domestic Producers

Energy costs account for roughly one-third of production spending, exposing kiln-based manufacturing to price recalculations each month that MERALCO revises generation charges. Compared with peers in Thailand or Vietnam, Philippine factories pay premium kilowatt-hour rates, which curtail economies of scale and hamper export ambitions. LNG dependence will deepen as the county expands regasification capacity by 200%, baking long-term cost volatility into ceramic firing budgets. Smaller plants struggle to finance modern kilns or cogeneration units, and their thinner margins heighten liquidation risk when tariff spikes coincide with currency depreciation. Persistent cost stress may consolidate capacity, lowering supply diversity within the Philippines ceramic tiles market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Interior Design Trends and Aesthetic Preferences

- Government "Build Better More" Infrastructure Pipeline

- Rising Import Penetration from China and Vietnam

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Porcelain commanded 54.85% revenue share in 2025, mirroring global durability standards and longstanding consumer trust in the Philippines ceramic tiles market size for premium finishes. The segment continues to reap benefits from ink-jet technology that replicates marble or timber visuals without the maintenance burden, entrenching brand loyalty among mid- to high-income homeowners. Mosaic tiles, though niche, are projected to record a 5.74% CAGR-fueled by accent-wall installations and artisanal revival programs that foothold local crafts into contemporary interiors. Unglazed and glazed ceramic formats retain loyalty in utility areas to slip resistance, while "other" decorative lines showcase hand-painted or patterned surfaces that support tourism-driven souvenir demand. Producers reallocating kiln cycles toward porcelain anticipate wider margin spreads, given the willingness among design-centric buyers to pay premiums while import pressure remains heavier in mass-market SKUs.

Porcelain's entrenched position also reflects cost-of-ownership economics: life cycles exceed 25 years, and low water absorption means fewer replacements, which resonates with investors building rental inventories in provincial cities. Imports once cornered top-end styles, but domestic imitations now match European aesthetics, tightening delivery timelines and lessening foreign exchange exposure for project owners. Mosaic uptake mirrors push toward bespoke bathrooms in hospitality refurbishments that prioritize Instagram-ready backdrops. Segment dynamics indicate that Philippines ceramic tiles market share held by porcelain is unlikely to cede ground, even as mosaics open incremental revenue pockets. Manufacturing priorities are thus skewing capital toward large-format porcelain lines that can toggle between glossy, matte, and textured finishes on demand.

Floor installations accounted for 51.62% of total demand in 2025, anchored by renovation cycles in Metro Manila's aging condominium stock and new-build schools funded by LGU budgets. Durability mandates make ceramic surfaces the baseline finish for malls, transport terminals, and healthcare corridors that face pedestrian loads exceeding 5,000 footfalls daily. Roofing applications, albeit just emerging, are set to clock the highest 5.63% CAGR as flood-resistant and solar-reflective tiles gain traction under climate-resilience building codes. Wall cladding sustains mid-single-digit growth as developers pivot toward hygienic, easy-to-sanitize surfaces in prep kitchens and restrooms, supplanting paints susceptible to mold. Application dispersion ensures diversified revenue streams, cushioning producers from cyclical dips in any single vertical within the broader Philippines ceramic tiles market.

Residential remodelers gravitate to anti-slip textures for kitchen refurbishments, while commercial landlords prefer stain-resistant variants that reduce janitorial expense over multi-year lease cycles. Flood-resistant rooftop tiles feature low water absorption and mechanical anchors suited for typhoon-exposed geographies such as Bicol and Eastern Visayas. Educational campuses adopting contact-safe surfaces after COVID-19 have swapped vinyl flooring for ceramic alternatives that withstand aggressive disinfectant regimens. Transport nodes-Clark Airport, MRT-7, Cebu BRT-embed porcelain in concourses due to abrasion grades PEI IV and V, reinforcing high-volume orders. Collectively, these patterns confirm floors will sustain the lion's share of Philippines ceramic tiles market size while emerging roofing specifications create promising adjacencies.

The Philippines Ceramic Tiles Market Report is Segmented by Product Type (Porcelain Tiles, Glazed Ceramic Tiles, and More), Application (Floor, Wall, Roofing), End-User (Residential, Commercial), Construction Type (New Construction, Renovation and Replacement), Distribution Channel (Specialty Stores, Home Improvement Stores, Online Retail, Direct Sales), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mariwasa Siam Ceramics Inc.

- Eurotiles Industrial Corporation

- SCG Ceramics (COTTO)

- RAK Ceramics PJSC

- PORCELANOSA Grupo

- Mohawk Industries Inc. (Daltile)

- Kajaria Ceramics Ltd.

- China Ceramics Co. Ltd.

- Guangdong Dongpeng Ceramic Co., Ltd.

- Pamesa Ceramica

- Grupo Lamosa

- HRD Singapore Pte Ltd (Niro Granite)

- Italgraniti Group

- Atlas Concorde S.p.A.

- FC Tile Depot

- ABC Tile Center

- Wilcon Depot Inc.

- Cebu Home and Builders Centre

- Tile Express Shop

- Royal Tern Ceramics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Pandemic Residential Construction Rebound

- 4.2.2 Government "Build Better More" Infrastructure Pipeline

- 4.2.3 Growing Preference For Large-Format Porcelain Slabs

- 4.2.4 Retail-Chain Expansion In Tier-2 Cities

- 4.2.5 Energy-Efficient Kilns Lowering Unit Costs

- 4.2.6 Metro Manila Green-Building Mandate For Floor Finishes

- 4.3 Market Restraints

- 4.3.1 High Electricity Tariffs Squeezing Domestic Producers

- 4.3.2 Volatile LNG Prices Inflating Firing Costs

- 4.3.3 Rising Import Penetration From China And Vietnam

- 4.3.4 Skilled-Labor Shortages In Provincial Regions

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Porcelain Tiles

- 5.1.2 Glazed Ceramic Tiles

- 5.1.3 Unglazed Ceramic Tiles

- 5.1.4 Mosaic Tiles

- 5.1.5 Others (Decorative, Patterned, Handmade)

- 5.2 By Application

- 5.2.1 Floor

- 5.2.2 Wall

- 5.2.3 Roofing

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality (Hotels, Resorts)

- 5.3.2.2 Retail Spaces

- 5.3.2.3 Offices & Institutions

- 5.3.2.4 Healthcare

- 5.3.2.5 Educational Facilities

- 5.3.2.6 Transport Hubs (Airports, Metro, Bus Terminals)

- 5.3.2.7 Other Commercial Users

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Renovation and Replacement

- 5.5 By Distribution Channel

- 5.5.1 Specialty Tile & Stone Stores

- 5.5.2 Home Improvement & DIY Stores

- 5.5.3 Online Retail

- 5.5.4 Direct Sales to Contractors

- 5.6 By Geography

- 5.6.1 Luzon

- 5.6.2 Visayas

- 5.6.3 Mindanao

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Mariwasa Siam Ceramics Inc.

- 6.4.2 Eurotiles Industrial Corporation

- 6.4.3 SCG Ceramics (COTTO)

- 6.4.4 RAK Ceramics PJSC

- 6.4.5 PORCELANOSA Grupo

- 6.4.6 Mohawk Industries Inc. (Daltile)

- 6.4.7 Kajaria Ceramics Ltd.

- 6.4.8 China Ceramics Co. Ltd.

- 6.4.9 Guangdong Dongpeng Ceramic Co., Ltd.

- 6.4.10 Pamesa Ceramica

- 6.4.11 Grupo Lamosa

- 6.4.12 HRD Singapore Pte Ltd (Niro Granite)

- 6.4.13 Italgraniti Group

- 6.4.14 Atlas Concorde S.p.A.

- 6.4.15 FC Tile Depot

- 6.4.16 ABC Tile Center

- 6.4.17 Wilcon Depot Inc.

- 6.4.18 Cebu Home and Builders Centre

- 6.4.19 Tile Express Shop

- 6.4.20 Royal Tern Ceramics

7 Market Opportunities & Future Outlook

- 7.1 Adoption of flood-resistant outdoor ceramic paving tiles

- 7.2 Local producers adopting inkjet printing for custom designs

陶瓷砖市场报告:按类型、应用和地区划分 2026-2034 年

陶瓷砖市场报告:按类型、应用和地区划分 2026-2034 年 防滑瓷砖市场规模、份额和成长分析:按类型、商业模式、应用、最终用途、地区和行业预测,2026-2033年

防滑瓷砖市场规模、份额和成长分析:按类型、商业模式、应用、最终用途、地区和行业预测,2026-2033年 全球陶瓷砖市场:机会与策略展望(至2034年)

全球陶瓷砖市场:机会与策略展望(至2034年) 陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分

陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分 美国陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031)日本水泥瓦市场:规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年印尼陶瓷砖市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲瓷砖市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031)日本水泥瓦市场:规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年印尼陶瓷砖市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲瓷砖市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)