|

市场调查报告书

商品编码

1910841

欧洲瓷砖市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)Europe Ceramic Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

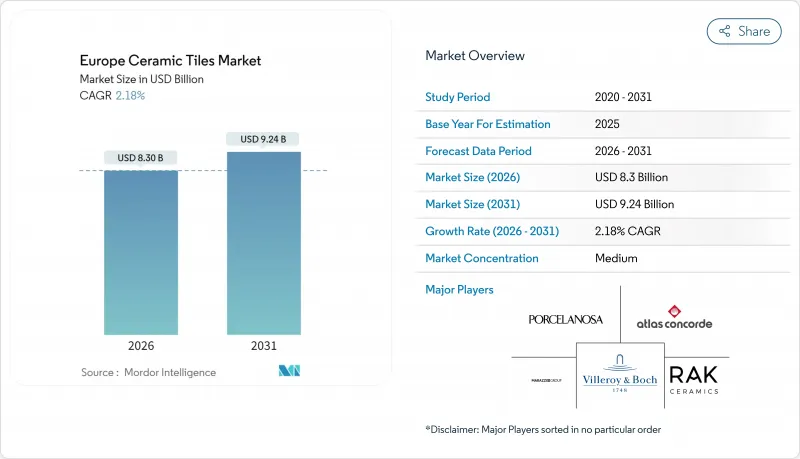

预计到 2026 年,欧洲瓷砖市场规模将达到 83 亿美元,从 2025 年的 81.2 亿美元成长到 2031 年的 92.4 亿美元,2026 年至 2031 年的复合年增长率为 2.18%。

当前市场需求环境保持稳定,疫情后的维修支出、欧盟资助的维修补贴以及中东欧地区持续的都市化抵消了不断上涨的能源和碳排放合规成本。大型製造商正在对其窑炉进行现代化改造,以降低天然气价格波动的风险;同时,原始设备製造商(OEM)正优先考虑抗菌和低挥发性有机化合物(VOC)的表面处理,以符合绿色建筑认证标准。数位化销售管道正在加速发展,而专业零售商则透过提供商店设计服务和专家安装支援来维持其市场地位。能够迅速调整生产线以提高能源效率并符合环境、社会和治理(ESG)揭露要求的製造商,将更有可能保持利润率并赢得公共部门的翻新合约。

欧洲瓷砖市场趋势与洞察

新冠疫情后奖励策略引发了一波快速的住宅翻维修。

欧洲家庭已将原本用于旅行和娱乐的预算转向住宅维修,这一趋势使得房屋维修需求在2025年之前保持高位。復苏与韧性基金每年向房屋维修注入约900亿欧元,确保瓷砖供应商订单稳定。高品质陶瓷瓷砖受益最大,因为住宅在厨房和浴室装修中优先考虑瓷砖的耐用性和自然美观。德国、法国和荷兰的房屋维修活动尤其显着,儘管货币政策紧缩,但这些国家的居民可支配所得水准依然较高。然而,从2026年起,不断上涨的抵押房屋抵押贷款利率和消费价格可能会减缓非必需性房屋维修的步伐。

节能窑炉可降低生产成本

新一代窑炉配备高速燃烧器和余热回收系统,可将燃气消费量降低高达 50%,从而提高企业在能源市场波动期间的 EBITDA 抗风险能力。义大利和西班牙的丛集正主导这一趋势,预计到 2024 年,将有 28 家製造商投入运作热电联产装置。欧洲投资银行向 Panaria 集团提供的 5,000 万欧元贷款表明,脱碳目标与成本竞争力之间的政策契合度很高。实现两位数排放的生产商将有资格获得欧盟排放权交易体系配额,并在公共竞标的资格预审中获得声誉优势。从长远来看,窑炉维修可望缩小欧洲与土耳其/亚洲竞争对手之间的可变成本差距。

天然气价格波动

天然气约占生产成本的30%,2024年现货价格波动迫使多家生产商运作数週。投入成本的波动使长期供应合约变得复杂,并促使下游批发商从亚洲进口多元化。拥有避险计画和自备可再生能源的公司表现相对较好,但价格转嫁机制在对价格敏感的维修细分市场仅部分奏效。这次能源衝击暴露了欧洲瓷砖市场易受地缘政治风险影响的脆弱性,并凸显了烧製线可再生能源电气化的迫切性。儘管随着天然气蕴藏量恢復正常,短期内情况有所缓解,但预计在氢气窑得到更广泛应用之前,波动风险仍将持续存在。

细分市场分析

瓷质砖因其耐冻性和低于1%的吸水率,适用于室内外环境,截至2025年,其在欧洲瓷砖市场占46.75%的份额。马赛克瓷砖虽然供应仍然有限,但由于高端卫浴和厨房维修中对复杂图案和大胆配色的偏爱,预计到2031年将以2.58%的复合年增长率增长。釉药瓷砖用于中檔翻新项目,而无釉瓷砖则因其防滑性能,在工业地面和交通枢纽等场所仍然备受欢迎。受木纹和石纹瓷砖作为木材和大理石替代品的美学吸引力推动,预计到2031年,欧洲瓷砖市场规模将超过42.8亿美元。高端供应商正透过「透明着色」、「边缘修整」和薄砖技术来降低运输重量,同时又不牺牲耐用性,从而实现差异化竞争。

马赛克製造仍然是资本密集型产业,玻璃网背衬和手工铺设工序增加了工时,但单位利润率弥补了产量小规模。设计师通常会为饭店大厅和水疗中心指定使用马赛克,客製化的几何图案能够提升物业价值。自动化技术的进步,例如机器人镶嵌,正在逐步降低每平方公尺的成本,为中端市场开闢了新的机会。永续性意识的建筑师也优先考虑使用由回收玻璃和陶瓷碎片製成的马赛克,并将循环经济原则融入计划提案中。总体而言,产品差异化可能会使欧洲瓷砖市场保持分散化,但对于那些拥有强大品牌知名度和专业技术的公司来说,它仍然盈利。

预计到2025年,地板材料铺设将占欧洲瓷砖市场规模的59.45%,主要得益于瓷砖的使用寿命长,且在高人流量区域经久耐用。商业地产业主选择瓷砖,是因为其终身维修成本低于复合地板和地毯,从而增强了瓷砖市场的基准销售稳定性。儘管该细分市场的复合年增长率不高,但其庞大的销售量确保了它将继续为瓷砖製造商带来可观的收入。耐冰挤压瓷砖在北欧庭院和阿尔卑斯山滑雪胜地拥有一定的市场份额,并形成了季节性的需求高峰。连续喷墨数位印刷技术带来的更高逼真度,使地板磁砖成为比采石场石材更经济实惠的选择。

墙面应用虽然目前规模仍较小,但预计到2031年将以2.59%的复合年增长率增长,这主要得益于抗菌釉药和可打造无缝视觉效果的大尺寸瓷砖。医院和住宿设施对抗菌表面的需求日益增长,例如Panaria集团的PROTECT系列,该系列可抑制99.9%的细菌滋生。 120 x 278公分的大尺寸磁砖可缩短安装时间,并减少可能滋生病原体的接缝-这些特性符合后疫情时代的设计要求。轻薄的磁砖可以直接铺设在现有表面上,避免拆除产生的废弃物,并减少维修停工时间。因此,墙面应用是整个欧洲瓷砖市场的策略成长领域。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 感染疾病应对措施后,住宅维修热潮迅速扩大

- 节能窑炉可降低生产成本

- 欧盟「翻新浪潮」政策津贴

- 绿建筑认证实施情形

- 中欧和东欧的都市化推动了对多用户住宅的需求。

- 过渡到抗菌抗病毒表面瓷砖

- 市场限制

- 天然气价格波动

- 欧盟排放交易体系(EU ETS)导致熔炉碳成本增加

- LVT和SPC地板更换

- 西欧建设产业人手不足

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解近期产业发展动态(新产品发布、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模及成长预测(金额:美元)

- 依产品类型

- 陶瓷瓷砖

- 釉药磁砖

- 无釉陶瓷砖

- 马赛克瓷砖

- 其他(装饰瓷砖、图案瓷砖、手工瓷砖)

- 透过使用

- 地面

- 墙

- 屋顶材料

- 最终用户

- 住宅

- 商业的

- 饭店业(饭店、度假村)

- 零售空间

- 办公室和公共机构

- 卫生保健

- 教育设施

- 交通枢纽(机场、捷运、客运站)

- 其他商业用户

- 依建筑类型

- 新建工程

- 维修和更换

- 透过分销管道

- 磁砖和石材专卖店

- 居家装潢和DIY专卖店

- 线上零售

- 直接向承包商销售

- 按地区

- 德国

- 义大利

- 西班牙

- 法国

- 英国

- 波兰

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Marazzi Group Srl

- Porcelanosa Grupo

- RAK Ceramics

- Ceramiche Atlas Concorde

- Villeroy & Boch

- Grupo STN

- Novoceram(Panaria)

- Tau Ceramica

- Iris Ceramica Group

- Gruppo Concorde

- ABK Group

- Emilgroup

- Florim

- Pamesa Ceramica

- Keraben Grupo

- Lasselsberger(Rako)

- Kajaria Ceramics(EU subsidiaries)

- Mohawk Industries(Dal-Tile Europe)

- Levantina

- Gigacer

第七章 市场机会与未来展望

Europe ceramic tiles market size in 2026 is estimated at USD 8.3 billion, growing from 2025 value of USD 8.12 billion with 2031 projections showing USD 9.24 billion, growing at 2.18% CAGR over 2026-2031.

The current demand environment remains stable because post-pandemic renovation spending, EU-funded retrofit grants and steady urbanization in Central and Eastern Europe counterbalance higher energy and carbon-compliance costs. Large producers mitigate volatile natural-gas prices through kiln modernizations, while OEMs emphasize antibacterial and low-VOC surfaces that align with green-building certification criteria. Digital sales channels accelerate, yet specialty retailers keep traction by offering in-store design services and professional installation support. Manufacturers that quickly adapt production lines for energy efficiency and ESG disclosure have clearer paths to preserve margins and secure public-sector renovation contracts.

Europe Ceramic Tiles Market Trends and Insights

Rapid Residential Renovation Wave Post-COVID Stimulus

European households redirected unspent travel and entertainment budgets toward home upgrades, and that behavior kept renovation volumes elevated through 2025. The Recovery and Resilience Facility channels close to EUR 90 billion per year into building upgrades, ensuring steady order inflows for tile suppliers. Premium porcelain formats benefit most as homeowners prioritize longevity and natural-look aesthetics in kitchens and bathrooms. Renovation activity is especially pronounced in Germany, France and the Netherlands, where disposable income levels remain supportive despite tighter monetary policy. Nevertheless, higher mortgage rates and consumer inflation could temper the pace of discretionary remodeling from 2026.

Energy-Efficient Kilns Lowering Production Cost

Next-generation kilns equipped with high-speed burners and waste-heat recovery reduce gas consumption by as much as 50% and improve EBITDA resilience when energy markets spike. Italian and Spanish clusters lead adoption, with 28 manufacturers operating combined-heat-and-power units by 2024. The European Investment Bank's EUR 50 million loan to Panariagroup underscores policy alignment between decarbonization goals and cost competitiveness. Producers achieving double-digit emission reductions earn EU ETS allowances and build reputational advantages that aid in public tender pre-qualification. Over the long term, kiln retrofits are expected to narrow variable-cost gaps between European and Turkish or Asian competitors.

Volatile Natural-Gas Prices

Natural-gas represents roughly 30% of production cost, and 2024 spot-price swings forced several producers to idle kilns for weeks. Input-cost volatility complicates long-term supply contracts, encouraging downstream wholesalers to diversify toward Asian imports. Firms with hedging programs or captive renewable power have fared better, yet pass-through pricing remains only partially effective in price-sensitive renovation sub-segments. The energy shock showcased Europe ceramic tiles market exposure to geopolitical risk and underlined the urgency of renewable electrification in firing lines. Short-term relief is visible as gas storage levels normalize, although volatility risks persist until hydrogen-ready kilns scale.

Other drivers and restraints analyzed in the detailed report include:

- EU "Renovation Wave" Policy Grants

- Green Building Certification Uptake

- Tightening EU ETS Carbon Costs on Kilns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Porcelain tiles retained 46.75% share of the Europe ceramic tiles market in 2025 owing to frost resistance and sub-1% water absorption that suit indoor and outdoor environments. Mosaic formats, although volume-light, are projected to clock a 2.58% CAGR through 2031 because luxury bathroom and kitchen remodels favor intricate patterns and bold colorways. Glazed ceramic serves mid-price refurbishment jobs, while unglazed tiles keep traction in factory floors and transit hubs that demand slip resistance. The Europe ceramic tiles market size for porcelain is expected to exceed USD 4.28 billion by 2031, supported by wood-look and stone-look aesthetics that displace timber and marble. Premium suppliers differentiate via through-body pigmentation, rectified edges and thin-tile technologies that reduce shipping weight without sacrificing durability.

Mosaic manufacturing remains capital-intensive because glass-mesh backing and hand-placement steps add labor hours, yet unit margins compensate for modest volumes. Designers specify mosaics for hotel lobbies and spa facilities where bespoke geometry raises perceived property value. Automation advances such as robotic tesserae placement are gradually lowering cost per square meter, opening mid-market opportunities. Sustainability-minded architects also privilege mosaics that upcycle waste glass or porcelain shards, integrating circular-economy narratives into project bids. Overall, product differentiation will keep the Europe ceramic tiles market fragmented but profitable for firms with brand equity and specialized capability.

Floor installations captured 59.45% of the Europe ceramic tiles market size in 2025, underpinned by long replacement cycles and durability in high-traffic zones. Commercial landlords choose porcelain slabs to cut lifetime maintenance costs versus laminate or carpet, reinforcing baseline volume stability. The segment's CAGR is muted, yet shear volume ensures it remains a revenue bedrock for kiln operators. Ice-resistant extruded tiles also hold niche appeal in Nordic patios and alpine ski resorts, adding seasonal peaks to demand. Continuous-inkjet digital printing enhances realism, making floor tiles an affordable alternative to quarried stone.

Wall applications, while smaller, are forecast to expand at a 2.59% CAGR through 2031 due to germ-resistant glazes and large-format panels that create seamless visuals. Hospitals and hospitality venues increasingly request antimicrobial surfaces such as Panariagroup's PROTECT line, which inhibits 99.9% of bacterial colonization. Large 120 X 278 cm tiles shorten installation times and reduce grout lines that can harbor pathogens, attractive traits in post-pandemic design briefs. Lightweight slim panels also enable direct-to-existing-surface installation, avoiding demolition waste and lowering renovation downtime. Consequently, wall applications represent a strategic growth vector within the wider Europe ceramic tiles market.

The Europe Ceramic Tiles Market Report is Segmented by Product Type (Porcelain Tiles, Glazed Ceramic Tiles, and More), Application (Floor, Wall, Roofing), End-User (Residential, Commercial), Construction Type (New Construction, Renovation and Replacement), Distribution Channel (Specialty Tile & Stone Stores, and More), and Geography (Germany, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Marazzi Group S.r.l

- Porcelanosa Grupo

- RAK Ceramics

- Ceramiche Atlas Concorde

- Villeroy & Boch

- Grupo STN

- Novoceram (Panaria)

- Tau Ceramica

- Iris Ceramica Group

- Gruppo Concorde

- ABK Group

- Emilgroup

- Florim

- Pamesa Ceramica

- Keraben Grupo

- Lasselsberger (Rako)

- Kajaria Ceramics (EU subsidiaries)

- Mohawk Industries (Dal-Tile Europe)

- Levantina

- Gigacer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid residential renovation wave post-COVID stimulus

- 4.2.2 Energy-efficient kilns lowering production cost

- 4.2.3 EU "Renovation Wave" policy grants

- 4.2.4 Green Building certification uptake

- 4.2.5 Urbanisation in CEE boosting multi-family housing

- 4.2.6 Shift to antibacterial & antiviral surface tiles

- 4.3 Market Restraints

- 4.3.1 Volatile natural-gas prices

- 4.3.2 Tightening EU ETS carbon costs on kilns

- 4.3.3 Substitution by LVT & SPC flooring

- 4.3.4 Labour shortages in Western Europe construction

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Porcelain Tiles

- 5.1.2 Glazed Ceramic Tiles

- 5.1.3 Unglazed Ceramic Tiles

- 5.1.4 Mosaic Tiles

- 5.1.5 Others (Decorative, Patterned, Handmade)

- 5.2 By Application

- 5.2.1 Floor

- 5.2.2 Wall

- 5.2.3 Roofing

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality (Hotels, Resorts)

- 5.3.2.2 Retail Spaces

- 5.3.2.3 Offices & Institutions

- 5.3.2.4 Healthcare

- 5.3.2.5 Educational Facilities

- 5.3.2.6 Transport Hubs (Airports, Metro, Bus Terminals)

- 5.3.2.7 Other Commercial Users

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Renovation and Replacement

- 5.5 By Distribution Channel

- 5.5.1 Specialty Tile & Stone Stores

- 5.5.2 Home Improvement & DIY Stores

- 5.5.3 Online Retail

- 5.5.4 Direct Sales to Contractors

- 5.6 By Geography

- 5.6.1 Germany

- 5.6.2 Italy

- 5.6.3 Spain

- 5.6.4 France

- 5.6.5 United Kingdom

- 5.6.6 Poland

- 5.6.7 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Marazzi Group S.r.l

- 6.4.2 Porcelanosa Grupo

- 6.4.3 RAK Ceramics

- 6.4.4 Ceramiche Atlas Concorde

- 6.4.5 Villeroy & Boch

- 6.4.6 Grupo STN

- 6.4.7 Novoceram (Panaria)

- 6.4.8 Tau Ceramica

- 6.4.9 Iris Ceramica Group

- 6.4.10 Gruppo Concorde

- 6.4.11 ABK Group

- 6.4.12 Emilgroup

- 6.4.13 Florim

- 6.4.14 Pamesa Ceramica

- 6.4.15 Keraben Grupo

- 6.4.16 Lasselsberger (Rako)

- 6.4.17 Kajaria Ceramics (EU subsidiaries)

- 6.4.18 Mohawk Industries (Dal-Tile Europe)

- 6.4.19 Levantina

- 6.4.20 Gigacer

7 Market Opportunities & Future Outlook

- 7.1 Advances in Self-Cleaning Photocatalytic Coatings for Tiles

- 7.2 Circular Economy Initiatives: Tile Take-Back and Recycling Schemes

2026年全球水泥瓦市场报告2026年全球瓷器和陶瓷马赛克市场报告2026年全球磁砖填缝剂市场报告2026年全球陶瓷地砖和墙砖市场报告

2026年全球水泥瓦市场报告2026年全球瓷器和陶瓷马赛克市场报告2026年全球磁砖填缝剂市场报告2026年全球陶瓷地砖和墙砖市场报告 陶瓷砖市场报告:按类型、应用和地区划分 2026-2034 年

陶瓷砖市场报告:按类型、应用和地区划分 2026-2034 年 防滑瓷砖市场规模、份额和成长分析:按类型、商业模式、应用、最终用途、地区和行业预测,2026-2033年全球陶瓷砖市场:机会与策略展望(至2034年)

防滑瓷砖市场规模、份额和成长分析:按类型、商业模式、应用、最终用途、地区和行业预测,2026-2033年全球陶瓷砖市场:机会与策略展望(至2034年) 陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分

陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分 美国陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031)

美国陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031)