|

市场调查报告书

商品编码

1910870

日本低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Japan Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

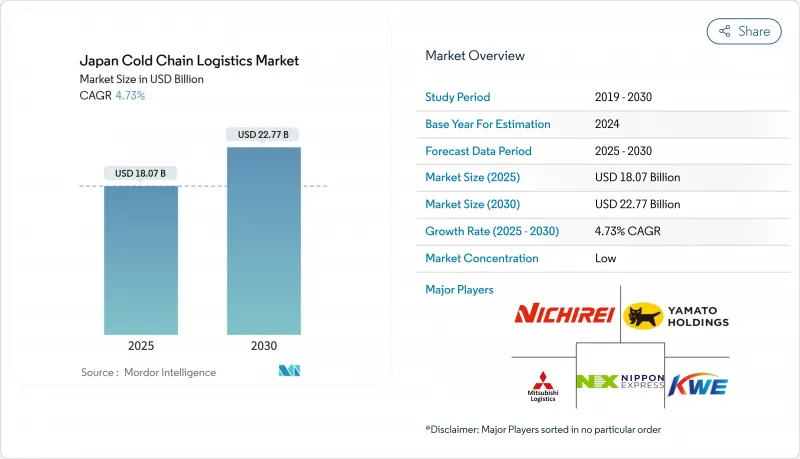

据估计,日本低温运输物流市场规模在 2026 年将达到 189.2 亿美元,高于 2025 年的 180.7 亿美元,预计到 2031 年将达到 237.8 亿美元。

预计2026年至2031年年复合成长率(CAGR)为4.68%。

短期内,对温度敏感的电商食品配送、超精准的药品分销以及创纪录的水产品出口正在汇聚,形成一波需求浪潮,加速设施升级、车辆电气化以及数位化可视化平台的普及。零售商正将微型仓配中心改造为多区域枢纽,以应对当日达订单的激增;生物製药企业则在2-8°C的低温环境下储备冗余储存容量,以保护高价值库存。政府资助的疫苗储备将确保超低温设施的持续运作,而区域全面经济伙伴关係协定(RCEP)带来的贸易扩张也将促进长期成长,重振海运冷藏运输路线。为此,大型物流业者正在加速併购、自动化以及替代燃料车辆的测试,以提高获利能力并降低碳排放风险。

日本低温运输物流市场趋势与洞察

需要温度控制的电子商务食品配送

线上生鲜购物的快速普及正在重新定义仓储设施的规模和位置。乐天玛特目前在东京和关西地区每天处理7万份冷藏和冷冻订单,其微型仓配中心配备了产品运输机器人和三区储存模组。便利商店连锁企业也在采用类似的模式:7-Eleven的7NOW服务计划在全国2万家门市扩展,建造一个高密度的「最后一公里」配送网络,该网络依赖于零下低温储物柜和保温托特包。零售商还推出了移动餐车,为郊区的老年人提供服务,并将配送车辆用作移动冷藏室。这些变化有利于能够小规模灵活扩展的第三方业者。同时,现有仓库业主正在投资高层仓库的自动化改造,以在订单量下降的情况下维持利润率。最终形成了一个生态系统,在这个系统中,与消费者接近性与托盘搬运的准确性同等重要。

生物製药、细胞和基因治疗产品线(2-8°C)

日本生物製药产业正在扩展精准物流,以减少GLP-1供应链审核中发现的480亿美元温度偏差损失。可在4°C下维持稳定的新型mRNA製剂显着降低了对-80°C低温储存的依赖,新建设施也开始采用双温区策略。筑波医疗物流中心二期工程设有15-25°C、2-8°C和-20°C三个温度隔离区以及三重冗余电源,充分体现了满足PMDA检验标准所需的巨额资本投入。小规模物流公司难以资金筹措如此复杂的设施建设成本,因此加速将业务外包给拥有检验的资料记录器、全天候监控系统以及符合GDP标准的标准作业程式(SOP)的公司。茨城县和埼玉县週边地区的集中布局造成了供需失衡,促使九州和北海道地区计划区域配送中心(DC)。

持证冷藏车司机短缺

司机数量持续下降,平均年龄超过50岁,年工作时长受加班限制。由于操作冷冻系统需要高级认证,低温运输营运商受到的影响比常温运输业者更大。日本通运正透过投资Gatik AI来应对这项挑战,以侦测和营运资料中心之间的自动驾驶中间运输路线。一项由政府支持的东京至大阪试点计画旨在2027年获得编队行驶认证。在自动驾驶普及之前,业者正将长途运输业务转移到铁路和滚装船运输,将宝贵的司机资源集中在复杂的「最后一公里」配送上。如果工资奖励措施未能吸引新的持牌业者,区域路线将面临服务缺口和全国覆盖范围缩小的风险。

细分市场分析

截至2025年,冷藏仓库将占日本低温运输物流市场收入的41.30%,反映出食品和製药业库存缓衝策略的建立。多温控设施正在采用穿梭起重机和移动货架,以在不扩大用地面积的情况下容纳不断增加的SKU。 LOGI FLAG TECH越谷i大楼展示了私人业者如何透过安装太阳能板和天然冷媒,在降低公用事业成本的同时,实现-25°C的设定温度。虽然公共仓库对寻求灵活条款的中小型企业仍然具有吸引力,但高附加价值药品份额的不断增长正促使大型托运人转向使用能够确保符合GDP标准的专用自有设施。

预计到2031年,附加价值服务将以每年4.72%的速度成长,主要受销售点附近套件组装、重新贴标和后处理服务需求成长的推动。营运商正透过整合品质保证实验室和快速组装区,并将托盘储存转化为收入来源,来弥补吞吐量放缓的局面。冷藏运输需求保持稳定,Konoike Transport公司为永旺集团的都市区配送引入了续航里程达120公里的电动卡车。模式转换也不断扩大:栗林海云公司在其仙台至大阪的冷冻麵条航线上,从100%的卡车运输转向滚装船运输,二氧化碳排放减少了74%,并将港到港的运输时间缩短至3小时。空运在临床试验和紧急召回方面仍然占据着一定的市场份额,但随着JR Freight公司引入更多冷藏货柜,其市场份额正被温控铁路运输蚕食。

其他福利

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务生鲜配送的成长,需要温度控制

- 不断扩展的生物製药、细胞和基因治疗产品线需要2-8°C的物流。

- 政府补贴的疫苗储备措施

- 受RCEP关税减让影响,水产品出口快速成长。

- 透过自动化和物联网降低托盘级搬运成本

- 透过引入氢燃料冷藏卡车来减少对柴油的依赖

- 市场限制

- 由于劳动力老化,持有执照的冷藏车驾驶人短缺。

- 都市区不断上涨的房地产价格限制了新建冷库的建设。

- 夏季高峰尖峰时段超低温冷冻库可能导致电网不稳定

- 严格的氟碳化合物淘汰法规正在推动对维修设施的投资增加。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 排放标准和ESG目标的影响

- 地缘政治与疫情的影响

第五章 市场规模与成长预测

- 按服务类型

- 冷藏保管

- 公共仓库

- 私人仓库

- 冷藏运输

- 路

- 铁路

- 海路

- 航空邮件

- 附加价值服务

- 冷藏保管

- 按温度类型

- 冷藏(0-5°C)

- 冷冻(-18 至 0°C)

- 室温

- 超低温冷冻(约20℃或更低)

- 透过使用

- 水果和蔬菜

- 肉类/家禽

- 鱼贝类

- 乳製品和冷冻甜点

- 麵包糖果甜点

- 即食餐

- 药品和生技药品

- 疫苗和临床试验材料

- 化学品/特殊材料

- 其他的

- 按地区(国内)

- 关东

- 关西

- 中部

- 九州、冲绳

- 北海道和东北地区

- 其他中东和非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Nippon Express

- Yamato Holdings

- Nichirei Logistics Group

- Mitsubishi Logistics

- Kintetsu World Express

- Itochu Logistics

- Sagawa Express

- Konoike Transport Co., Ltd

- K-Line Logistics

- DHL Supply Chain

- Kuehne+Nagel

- CEVA Logistics

- Mitsui-Soko Group

- SENKO Co., Ltd.

- Suzuyo & Co.

- SF Express

- 邮船物流(日本邮船株式会社旗下部门)

- MOL Logistics

- Matsuoka Co., Ltd.

- YOKOREI Co., Ltd

第七章 市场机会与未来展望

Japan Cold Chain Logistics Market size in 2026 is estimated at USD 18.92 billion, growing from 2025 value of USD 18.07 billion with 2031 projections showing USD 23.78 billion, growing at 4.68% CAGR over 2026-2031.

In the near term, temperature-sensitive e-commerce grocery delivery, ultra-precision pharmaceutical distribution, and record seafood exports form a synchronized demand wave that accelerates facility upgrades, fleet electrification, and digital visibility platforms. Retailers convert micro-fulfillment centers into multi-zone hubs to handle surging same-day orders, while biologics producers secure redundant 2-8 °C capacity to protect high-value inventory. Long-term growth also benefits from government-funded vaccine stockpiles that ensure continuous utilization of ultra-low-temperature assets and from expanded Regional Comprehensive Economic Partnership (RCEP) trade flows that stimulate maritime reefer lanes. In response, major logistics providers pursue mergers, automation rollouts, and alternative-fuel vehicle pilots to improve margins and reduce carbon exposure.

Japan Cold Chain Logistics Market Trends and Insights

Temperature-sensitive e-commerce grocery delivery

Rapid online grocery adoption is redefining facility scale and location. Rakuten Mart now processes 70,000 chilled and frozen orders daily across Tokyo and Kansai, supported by micro-fulfillment centers equipped with goods-to-person robots and three-zone storage modules. Convenience chains replicate this model: 7-Eleven's 7NOW service plans nationwide coverage through 20,000 stores, creating dense last-mile networks that rely on sub-zero lockers and insulated totes. Retailers also deploy mobile shops to reach suburban seniors, turning delivery vans into rolling cold rooms. These shifts favor agile third-party operators able to add capacity in smaller increments, while legacy warehouse owners invest in high-bay automation to protect margins as order sizes decline. The result is an ecosystem where proximity to the consumer is valued as highly as pallet throughput accuracy.

Biologics & cell-gene therapy pipeline (2-8 °C)

Japan's biopharma sector is scaling precision logistics to curb USD 48 billion in global temperature excursion losses revealed by GLP-1 supply chain audits. New mRNA formulations that remain stable at 4 °C slash dependence on -80 °C storage, prompting a dual-temperature strategy in new builds. Tsukuba Medical Logistics Center Phase 2 offers segregated 15-25 °C, 2-8 °C, and -20 °C zones with triple-redundant power, underscoring the capital intensity required to meet PMDA validation rules. Smaller carriers struggle to finance such complexity, accelerating contract outsourcing to firms with validated data-loggers, 24/7 monitoring, and GDP-compliant SOPs. Geographic concentration around Ibaraki and Saitama generates supply-demand imbalances that spur regional DC projects in Kyushu and Hokkaido.

Shortage of licensed reefer-truck drivers

Driver numbers continue to decline as the median age tops 50 and overtime caps limit annual hours. Cold chain fleets feel the pinch more than ambient carriers because advanced endorsements are required to handle refrigerant systems. Nippon Express addressed the gap by investing in Gatik AI to test autonomous middle-mile routes between DCs. Government-backed pilots linking Tokyo and Osaka aim to certify platooning by 2027. Until autonomy scales, operators shift long-haul volumes onto rail and RORO vessels, preserving scarce drivers for intricate last-mile drops. Rural routes risk service gaps that could weaken national coverage if wage premiums fail to attract new licensees.

Other drivers and restraints analyzed in the detailed report include:

- Government-subsidized vaccine stockpiling

- Surge in seafood exports via RCEP corridors

- High urban real-estate prices for cold warehouses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage controlled 41.30% of 2025 revenue within the Japan cold chain logistics market, reflecting entrenched inventory-buffer strategies across food and pharma sectors. Multi-temperature facilities deploy shuttle cranes and mobile racks to handle SKU proliferation without expanding footprints. The LOGI FLAG TECH Koshigaya I build demonstrates how private operators embed solar panels and natural refrigerants to curb utility bills while achieving -25 °C setpoints. Public warehouses remain attractive to SMEs seeking flexible terms, yet the growing share of high-value pharmaceuticals steers larger shippers toward dedicated in-house sites that guarantee GDP compliance.

Value-added services are set to grow 4.72% annually through 2031 as customers demand kitting, re-labeling, and post-processing near point-of-sale. Providers integrate QA labs and light assembly zones, converting pallet storage into fee-earning activities that offset slower throughput. Refrigerated transportation keeps stable demand as Konoike Transport deploys electric trucks with 120-kilometer range for Aeon Group urban deliveries. Modal shifts expand: Kuribayashi Shipping's switch from 100% trucking to RORO ships on Sendai-Osaka frozen noodle lanes cut CO2 74% while trimming transit to 3 hours dock-to-dock. Airfreight retains a niche for clinical trials and urgent recalls but yields share to temperature-controlled rail as JR Freight adds reefer containers.

The Japan Cold Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, Value-Added Services), Temperature Type (Chilled, Frozen, Ambient, Deep-Frozen/Ultra-Low), Application (Fruits & Vegetables, Meat & Poultry, Fish & Seafood, Dairy & Frozen Desserts, Bakery & Confectionery, and More), and Geography (Kanto, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nippon Express

- Yamato Holdings

- Nichirei Logistics Group

- Mitsubishi Logistics

- Kintetsu World Express

- Itochu Logistics

- Sagawa Express

- Konoike Transport Co., Ltd

- K-Line Logistics

- DHL Supply Chain

- Kuehne + Nagel

- CEVA Logistics

- Mitsui-Soko Group

- SENKO Co., Ltd.

- Suzuyo & Co.

- SF Express

- Yusen Logistics (Part of NYK Line)

- MOL Logistics

- Matsuoka Co., Ltd.

- YOKOREI Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of temperature-sensitive e-commerce grocery delivery

- 4.2.2 Growing biologics and cell-gene therapy pipeline requiring 2-8 °C logistics

- 4.2.3 Government-subsidised vaccine stockpiling initiatives

- 4.2.4 Surge in seafood exports driven by RCEP tariff reductions

- 4.2.5 Automation and IoT lowering per-pallet handling costs

- 4.2.6 Hydrogen-powered reefer truck pilots lowering diesel dependency

- 4.3 Market Restraints

- 4.3.1 Shortage of licensed reefer-truck drivers amid ageing workforce

- 4.3.2 High urban real-estate prices limiting new cold-warehouse builds

- 4.3.3 Grid-instability risk for ultra-low-temp freezers during summer peaks

- 4.3.4 Stringent fluorocarbon phase-out rules increasing retrofit CAPEX

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Emission Standards and ESG Targets

- 4.9 Impact of Geopolitics and Pandemic

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.3 By Application

- 5.3.1 Fruits and Vegetables

- 5.3.2 Meat and Poultry

- 5.3.3 Fish and Seafood

- 5.3.4 Dairy and Frozen Desserts

- 5.3.5 Bakery and Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals and Biologics

- 5.3.8 Vaccines and Clinical Trial Materials

- 5.3.9 Chemicals and Specialty Materials

- 5.3.10 Other Applications

- 5.4 By Region (Domestic)

- 5.4.1 Kanto

- 5.4.2 Kansai

- 5.4.3 Chubu

- 5.4.4 Kyushu and Okinawa

- 5.4.5 Hokkaido and Tohoku

- 5.4.6 Rest of Japan

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Nippon Express

- 6.4.2 Yamato Holdings

- 6.4.3 Nichirei Logistics Group

- 6.4.4 Mitsubishi Logistics

- 6.4.5 Kintetsu World Express

- 6.4.6 Itochu Logistics

- 6.4.7 Sagawa Express

- 6.4.8 Konoike Transport Co., Ltd

- 6.4.9 K-Line Logistics

- 6.4.10 DHL Supply Chain

- 6.4.11 Kuehne + Nagel

- 6.4.12 CEVA Logistics

- 6.4.13 Mitsui-Soko Group

- 6.4.14 SENKO Co., Ltd.

- 6.4.15 Suzuyo & Co.

- 6.4.16 SF Express

- 6.4.17 Yusen Logistics (Part of NYK Line)

- 6.4.18 MOL Logistics

- 6.4.19 Matsuoka Co., Ltd.

- 6.4.20 YOKOREI Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

低温运输物流车辆市场依运输方式、温度范围、冷冻技术及终端用户产业划分-2026-2032年全球预测

低温运输物流车辆市场依运输方式、温度范围、冷冻技术及终端用户产业划分-2026-2032年全球预测 义大利低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印度低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)德国低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

义大利低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印度低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)德国低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本冷链物流市场规模、份额、趋势及预测(按服务、温度类型、应用和地区划分,2026-2034年)

日本冷链物流市场规模、份额、趋势及预测(按服务、温度类型、应用和地区划分,2026-2034年) 低温运输市场规模、份额和成长分析(按类型、温度、技术、温度控制和地区划分)—产业预测(2026-2033 年)

低温运输市场规模、份额和成长分析(按类型、温度、技术、温度控制和地区划分)—产业预测(2026-2033 年) 农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析

农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析 低温运输市场规模、份额和趋势分析报告:按类型、温度范围、应用、地区和细分市场预测(2026-2033 年)

低温运输市场规模、份额和趋势分析报告:按类型、温度范围、应用、地区和细分市场预测(2026-2033 年) 全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年)

全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年)