|

市场调查报告书

商品编码

1934830

新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Singapore Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

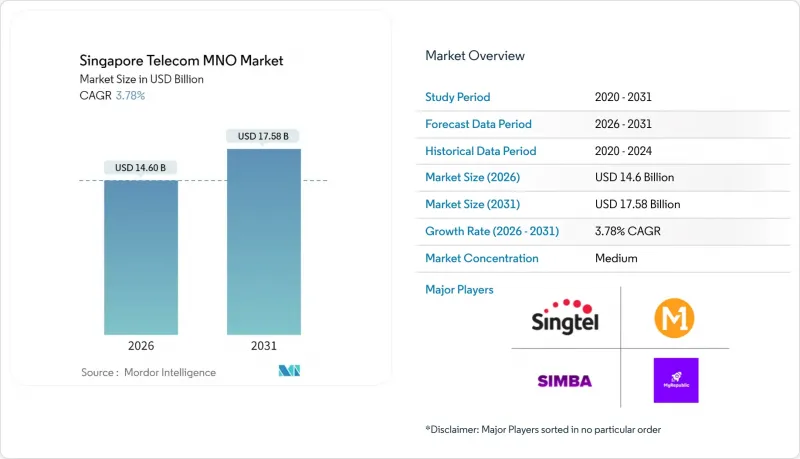

预计新加坡电信行动网路营运商 (MNO) 市场将从 2025 年的 140.7 亿美元成长到 2026 年的 146 亿美元,到 2031 年将达到 175.8 亿美元,2026 年至 2031 年的复合年增长率为 3.78%。

就用户数量而言,预计市场将从2025年的1009万增长到2030年的1169万,在预测期(2025-2030年)内复合年增长率低于2.98%。这一稳步增长的趋势得益于强有力的基础设施投资、覆盖全国的5G独立组网以及积极的云端优先公共倡议,这些因素共同推动了企业需求,同时保持了高端消费者的升级需求。住宅光纤普及率已达100%,使业者能够将Gigabit级宽频与5G行动套餐捆绑销售,支援平均每月超过50GB的行动数据流量。政府和工业领域的数位化加速,推动了对安全、高容量连接的需求,通讯业者正透过网路切片产品来满足关键任务工作负载的需求,并提供人工智慧驱动的网路安全套餐来应对这一需求。来自Simba和其他十多家行动虚拟网路营运商(MVNO)日益激烈的竞争,已将新加坡的资料通讯速率推至东南亚最低水平之列,但谨慎的资本支出週期和新的企业收入来源帮助维持了利润率。透过针对海事和港口用途的专用网路试验以及对云端边缘部署的积极投资,新加坡电信行动网路营运商(MNO)市场正将自身打造成为工业5G应用案例的区域典范。

新加坡电信行动网路营运商市场趋势与洞察

全国范围内的5G独立组网部署和网路切片

2025年,新加坡成为全球首个在所有人口密集区域实现5G独立组网覆盖的国家,赋予通讯业者架构上的自由度,可为对延迟敏感的流量分配专用网路切片。新加坡电信的700MHz频宽将室内覆盖率提升40%,同时以远低于一般行动套餐的成本实现超低频宽的物联网网路切片,从而拓展了目标企业应用场景。网路切片技术也为高阶消费者「5G+」套餐提供了支撑,确保尖峰时段的频宽,预计到2025年,早期采用者的平均每用户收入(ARPU)将提升23%。

数位化优先的公共部门措施和云端迁移

2024年底,超过80%的政府系统将运作在商业云端平台。这一里程碑事件立即提升了政府机构及其供应商对安全连接的需求。 2024年12月推出的「共享责任架构」鼓励金融机构与通讯业者在网路钓鱼防范方面开展进一步的合作创新,并在合规主导的通讯和API安全领域创造新的收入来源。

来自虚拟营运商和Simba的激烈竞争

Simba 的「50GB 10 新元套餐」重塑了消费者对价格的预期,帮助这家第四大通讯业者在 2024 年实现超过 10% 的用户份额。由于有超过 10 家 MVNO 瞄准微型用户群体,解约率每月超过 1.7%,这限制了任何营运商在无线存取能源成本不断上涨的情况下提高标价的空间。

细分市场分析

到2025年,数据产品将占新加坡电信行动网路营运商(MNO)市场份额的52.64%,这反映了行动宽频的广泛普及和100%的住宅光纤接入。物联网(IoT)和机器对机器(M2M)通讯将以3.94%的复合年增长率(CAGR)领跑,这主要得益于智慧工厂试点专案和城市级感测器网路对超可靠、低延迟连接的需求。语音服务将占19.74%,但随着OTT服务持续萎缩,其成长速度将会放缓。 OTT和付费电视将占10.08%,其中串流媒体套餐将带来温和成长。其他附加价值服务,包括託管安全和GPU即服务,将成长3.88%,因为营运商正在实现收入来源多元化。这种多元化表明,新加坡电信行动网路营运商市场的规模越来越与企业数位转型预算挂钩,而非传统的消费者语音服务趋势。

竞争格局正在推动服务融合。通讯业者将无限流量的纯SIM卡套餐与2Gbps家庭宽频和云端储存捆绑销售,价格与2019年单独购买这些产品的价格相同,推动了多产品组合的普及率超过65%。从大士港的自动导引运输车到樟宜机场的AR引导飞机检查,预计到2031年,工业5G应用案例将带来3.4亿美元的新增业务收益,进一步巩固了向高收益平台服务的结构性转变。

新加坡电信行动网路营运商 (MNO) 市场按服务类型(语音服务、数据及网际网路服务、通讯服务、物联网及机器对机器 (IoT & M2M) 服务、OTT 及付费电视服务、其他服务)及最终用户(企业、消费者)进行细分。市场预测以价值(美元)和用户数量(用户数)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 监理与政策框架

- 当前竞争格局中的频宽状况和拥有情形

- 通讯业生态系统

- 宏观经济与外在因素

- 波特五力模型

- 竞争对手之间的竞争

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 领先行动网路营运商的关键绩效指标(2020-2025)

- 独立行动用户和渗透率

- 行动网路使用者数量和普及率

- 按接入技术分類的SIM卡连线数和渗透率

- 蜂巢式物联网/M2M连接

- 宽频连线(移动和固定)

- ARPU(每位用户平均收入)

- 每用户平均数据使用量(GB/月)

- 市场驱动因素

- 全国独立的组网 5G 部署将支援高端消费者和企业应用场景

- 加强公共部门的数位化优先措施将推动安全、高容量连接的需求。

- 光纤到府 (FTTH) 部署的快速普及使得提供Gigabit级配套服务成为可能。

- 行动数据人均消耗量的快速成长(每月超过50GB)推动了ARPU值的成长。

- 私营海事和港口网络试点计画推动工业界采用 5G 技术(低调进行)

- 针对游戏玩家和金融科技用户的 5G 网路切片(优先通道)将创造新的 B2C 获利机会(但关注度较低)。

- 市场限制

- 来自虚拟营运商和第四家行动网路营运商(Simba)的过度竞争导致消费者价格弹性居高不下。

- OTT服务的兴起正在蚕食传统语音/简讯和付费电视的收入。

- 高昂的频谱续费和能源成本对EBITDA获利率带来压力。

- 国内市场规模有限,限制了5G独立组网的规模经济效益,而5G独立组网则需要大量的资本投资(低利率)。

- 技术展望

- 电信业主要经营模式分析

- 定价模型和定价分析

第五章 市场规模与成长预测

- 通信总收入和每位用户平均收入

- 服务类型

- 语音服务

- 数据和网际网路服务

- 通讯服务

- 物联网和机器对机器服务

- OTT和付费电视服务

- 其他服务(附加价值服务、漫游/国际服务、企业/批发服务等)

- 最终用户

- 公司

- 一般消费者

第六章 竞争情势

- 市场集中度

- 主要供应商的策略与投资动向(2023-2025)

- 2024年行动网路营运商市场占有率分析

- MNO snapshot(subscribers, churn rate, ARPU, etc.)

- 行动网路营运商公司简介*

- Singtel

- M1(Keppel)

- Simba Telecom

- MyRepublic

第七章 市场机会与未来展望

The Singapore Telecom MNO Market is expected to grow from USD 14.07 billion in 2025 to USD 14.6 billion in 2026 and is forecast to reach USD 17.58 billion by 2031 at 3.78% CAGR over 2026-2031.

In terms of subscriber volume, the market is expected to grow from 10.09 million units in 2025 to 11.69 million units by 2030, at a CAGR of less than 2.98% during the forecast period (2025-2030). This steady trajectory reflects resilient infrastructure investment, nationwide 5G standalone coverage, and aggressive cloud-first public initiatives that jointly lift enterprise demand while sustaining premium consumer upgrades. Household fiber penetration sits at 100%, enabling operators to bundle gigabit-class broadband with 5G mobile tiers, which in turn supports average monthly mobile data consumption above 50 GB. Intensifying digitalization across government and industry pushes demand for secure, high-capacity connectivity, and operators are responding with network-slicing products for mission-critical workloads and AI-enabled cybersecurity bundles. Competitive tension, sparked by the entry of Simba and more than ten MVNOs, has driven data prices to the lowest level in Southeast Asia, yet prudent capex cycles and new enterprise revenue streams help sustain margins. Maritime and port private-network pilots, plus aggressively funded cloud-edge rollouts, position the Singapore MNO telecom market as a regional showcase for industrial 5G use cases.

Singapore Telecom MNO Market Trends and Insights

Nationwide 5G standalone roll-out with network slicing

Singapore became the first country to blanket all populated areas with 5G standalone in 2025, giving operators the architectural freedom to allocate dedicated slices for latency-sensitive traffic. Singtel's 700 MHz layer lifted indoor coverage by 40% while permitting ultra-low-bandwidth IoT slices that cost only a fraction of regular mobile plans, expanding addressable enterprise use cases. Network slicing also underpins premium consumer "5G +" bundles that guarantee bandwidth during peak hours, generating a 23% ARPU uplift among early adopters in 2025

Digital-first public-sector initiatives and cloud migration

More than 80% of eligible government systems ran on the commercial cloud by late-2024, a milestone that immediately multiplied secure connectivity demand from agencies and their vendors. The Shared Responsibility Framework launched in December 2024 further compels financial institutions to co-innovate with telecom operators on anti-phishing defenses, spawning new compliance-driven messaging and API-security revenues.

Hyper-competition from MVNOs and Simba

Simba's SGD 10-for-50 GB plan re-anchored consumer price expectations and helped the fourth operator exceed 10% subscriber share by 2024. With more than ten MVNOs targeting micro-segments, churn has risen above 1.7% monthly, curbing the ability of any provider to push list prices upward despite rising radio-access energy costs.

Other drivers and restraints analyzed in the detailed report include:

- Full fiber-to-the-home saturation enabling 10 Gbps upgrades

- Surging per-capita mobile data use (>50 GB monthly)

- OTT substitution of voice/SMS and Pay-TV

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data products commanded 52.64% of Singapore telecom MNO market share in 2025, reflecting ubiquitous mobile broadband adoption and 100% household fiber access. IoT and M2M posted the highest 3.94% CAGR, fueled by smart-factory pilots and city-wide sensor grids that demand ultrareliable low-latency connectivity. Voice held 19.74% yet lagged in growth as OTT erosion persisted. OTT and PayTV represented 10.08%, bolstered modestly by streaming bundles. Other value-added services including managed security and GPU-as-a-Service grew at 3.88% as operators diversified revenue. This breadth underscores how the Singapore MNO telecom market size increasingly tracks enterprise digital-transformation budgets rather than legacy consumer voice trends.

The competitive configuration encourages convergence. Operators package unlimited-data SIM-only plans with 2 Gbps home broadband and cloud storage at price points equal to 2019 single surfaces, driving multi-product take-rates above 65%. Industrial 5G use cases from automated guided vehicles at Tuas Port to AR-guided aircraft checks at Changi are projected to inject USD 340 million incremental service revenue by 2031, reinforcing the structural pivot toward high-margin platform services.

The Singapore Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), and End User (Enterprises, Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Singtel

- M1 (Keppel)

- Simba Telecom

- MyRepublic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 Market Landscape

- 4.1 Market Overview

- 4.2 Regulatory And Policy Framework

- 4.3 Spectrum Landscape And Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic And External Drivers

- 4.6 Porter's Five Forces

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers And Penetration Rate

- 4.7.2 Mobile Internet Users And Penetration Rate

- 4.7.3 SIM Connections by Access Technology And Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile And Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 Nationwide Stand-alone 5G roll-out unlocks premium consumer and enterprise use-cases

- 4.8.2 Intensifying digital-first public-sector initiatives driving secure high-capacity connectivity demand

- 4.8.3 Rapid fibre-to-the-home (FTTH) saturation enabling gigabit-class bundled offers

- 4.8.4 Surging mobile data consumption per-capita (>50 GB/mo) supports ARPU uplift

- 4.8.5 Maritime And port private-network pilots catalyse Industrial 5G adoption (UNDER-RADAR)

- 4.8.6 5G network-slicing -priority lanes- for gamers And fintech users creates new B2C monetisation (UNDER-RADAR)

- 4.9 Market Restraints

- 4.9.1 Hyper-competition from MVNOs And fourth MNO (Simba) keeps consumer price elasticity high

- 4.9.2 OTT substitution erodes legacy voice/SMS and Pay-TV revenues

- 4.9.3 High spectrum-renewal And energy costs compress EBITDA margins

- 4.9.4 Limited domestic market size caps scale economics for heavy-capex 5G standalone (UNDER-RADAR)

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming & International Services, Enterprise And Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.5 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.5.1 Singtel

- 6.5.2 M1 (Keppel)

- 6.5.3 Simba Telecom

- 6.5.4 MyRepublic

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space And Unmet-Need Assessment

虚拟行动服务业者(MVNO) 市场:市场规模、份额和趋势分析(按类型、商业模式、服务类型、合约类型、最终用途和地区划分),细分市场预测(2026-2033 年)

虚拟行动服务业者(MVNO) 市场:市场规模、份额和趋势分析(按类型、商业模式、服务类型、合约类型、最终用途和地区划分),细分市场预测(2026-2033 年) 行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)