|

市场调查报告书

商品编码

1937399

美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)US Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

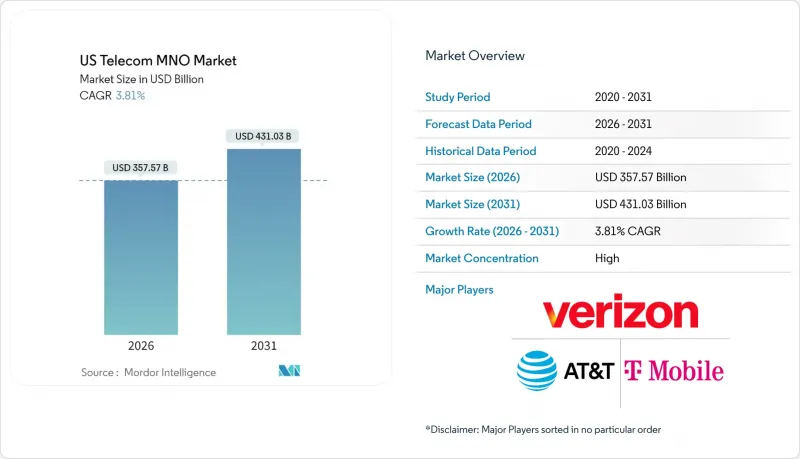

据估计,到 2026 年,美国电信行动网路营运商 (MNO) 市值将达到 3,575.7 亿美元,高于 2025 年的 3,444.5 亿美元。

预计到 2031 年将达到 4,310.3 亿美元,2026 年至 2031 年的复合年增长率为 3.81%。

这种稳定成长的趋势反映了市场环境的日趋成熟,传统语音和通讯服务逐渐萎缩,而数据密集型应用、专用蜂窝网路部署和整合企业平台则不断扩大利润空间。通讯业者部署加值服务层级、网路即服务 (NaaS)提案和低延迟边缘节点,从而加强高成本5G 资产的货币化是成长的关键。公共和私人补贴用于改善遍远地区的网路覆盖,积极实现频谱资源货币化,以及人工智慧驱动的网路自动化,这些因素持续扩大潜在的总收入池。由于三家全国性业者主导频谱深度和零售分销网络,竞争依然较为温和,即使在预付解约率上升的情况下,也能保持合理的定价策略。资本纪律、能源优化和频谱復用相结合,使得营运商能够在不显着侵蚀自由现金流的情况下,继续投资于网路密集化建设。

美国电信行动网路营运商市场趋势与洞察

5G独立组网(SA)核心网部署加速资料货币化

全面过渡到独立组网 (SA) 架构使通讯业者能够创建具有保证延迟和吞吐量的虚拟网路切片,从而实现传统非独立组网部署无法实现的服务差异化。 T-Mobile 已将公共网路切片商业化,每年已产生 2 亿美元的经常性收入,而 Verizon 则利用 SA 技术在 10 毫秒内支援製造机器人的边缘工作负载。企业合约通常会捆绑 API 接口,使开发人员能够将运营商级的身份验证和收费功能直接整合到他们的应用程式中。预计到 2028 年,这将创造约 200 亿美元的平台收入。高价值网路切片的每用户平均收入 (ARPU) 是大众行动宽频的三到五倍,这将直接推动美国电信行动网路营运商 (MNO) 市场的发展。

固定无线存取 (FWA) 取代了传统的铜线

2024年底,全美固定无线接取(FWA)用户数将超过1000万,这主要得益于中频宽和C频段频谱的开发,使得农村丛集的平均下行速度可达300Mbps。该产品可直接取代传统的DSL和同轴电缆服务区域,填补光纤覆盖的空白,并加速通讯业者5G无线投资的回报。 FWA还能增强住宅商品搭售,在用户拥有住宅网路订阅的情况下,可将无线营运商的行动线路接取率提高18%。人口密集郊区的容量限制推动了主动天线的扩展和频谱共用演算法的应用,但与铺设沟槽相比,其经济效益仍然显着。到2027年,用户的快速成长将使美国电信行动网路营运商(MNO)市场的复合年增长率(CAGR)提高0.8个百分点。

通货膨胀对预付用户平均收入(ARPU)带来压力。

能源和人事费用上涨迫使通讯业者提高套餐价格,但预付用户如果月帐单增加超过5美元,往往会即时取消订阅。 AT&T 2025年的资费调整暂时导致预付解约率上升了190个基点,进而导致挽留奖励和行销费用大规模增加。为了用户,通讯业者现在客户维繫全面的内容套餐、大流量套餐和先买后付的设备分期付款服务,这在短期内将使EBITDA获利率下降40-60个基点。

细分市场分析

2025年,数据和网路业务占总营收的53.12%,成为美国电信行动网路营运商(MNO)市场最大的收入来源。无限流量智慧型手机方案、固定无线存取(FWA)订阅和专用企业存取共同推动了每用户行动数据流量较去年同期成长7.8%。利用载波聚合技术的优质套餐在2025年的现场测试中实现了5.5 Gbps的实测吞吐量,进一步巩固了其速度优势,也证明了其价格差异的合理性。由于被OTT(Over-The-Top)服务所替代,语音和简讯的使用率出现了两位数的下降,导致总合收入份额低于10%。同时,物联网(IoT)和机器对机器(M2M)服务展现出最快的成长势头,这得益于新增的3000万台授权蜂巢式终端设备以及工厂、港口和医院等场所专用网路部署的增加。预计到 2031 年,该细分市场的复合年增长率将达到 3.92%,这将带来长期的成长动力,抵消传统服务的下滑,并维持美国电信行动网路营运商市场的扩张。

企业资料合约日益重视基于服务等级协定 (SLA) 的吞吐量和网路切片隔离,因此其利润率高于消费级线路,合约期限也更长。批发漫游和虚拟通讯业者带来了额外收入,主要用于在非尖峰时段摊提频谱资产。嵌入自优化网路中的进阶分析功能可将电力消耗降低约 15%,从而节省营运成本,用于投资建设更多小型基地台,进一步巩固公司在美国电信行动网路营运商 (MNO) 市场以数据为中心的地位。

美国电信行动网路营运商 (MNO) 市场按服务类型(语音服务、数据和互联网服务、通讯服务、物联网和机器对机器 (M2M) 服务、OTT 和付费电视服务、其他服务)和最终用户(企业、消费者)进行细分。市场预测以价值(美元)和用户数量(用户数)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 监理与政策框架

- 频谱环境和竞争性拥有情形

- 通讯业生态系统

- 宏观经济与外在因素

- 波特五力分析

- 竞争对手之间的竞争

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 领先行动网路营运商的关键绩效指标(2020-2025)

- 独立行动用户和渗透率

- 行动网路使用者数量和普及率

- 按接入技术分類的SIM卡连线数和渗透率

- 蜂巢式物联网/M2M连接

- 宽频连线(移动和固定)

- ARPU(每位用户平均收入)

- 每用户平均数据使用量(GB/月)

- 市场驱动因素

- 加速 5G 独立核心网路部署以促进资料货币化

- 固定无线存取(FWA)取代了传统的铜线。

- 透过引入仅支援 eSIM 的设备来降低客户流失率

- 联邦政府商业、就业和发展(BEAD)以及中途交通补助金,旨在促进遍远地区网路发展

- 来自工业物联网和园区网路的专用蜂窝网路需求

- 人工智慧驱动的无线存取网优化可降低营运成本

- 市场限制

- 通货膨胀对预付合约的平均每用户收入(ARPU)带来压力

- 光纤铺设过多会削弱无线宽频(FWA)的经济可行性。

- C波段航空干扰对策成本

- 美国联邦通讯委员会加强对併购的监管

- 技术展望

- 电信业主要经营模式分析

- 定价模型和定价分析

第五章 市场规模与成长预测

- 通信总收入和每位用户平均收入

- 服务类型

- 语音服务

- 数据和网际网路服务

- 通讯服务

- 物联网和机器对机器服务

- OTT和付费电视服务

- 其他服务(附加价值服务、漫游和国际服务、企业和批发服务等)

- 最终用户

- 公司

- 一般消费者

第六章 竞争情势

- 市场集中度

- 主要供应商的策略与投资动向(2023-2025)

- 2024年行动网路营运商市场占有率分析

- Product Benchmarking Analysis for mobile network services

- MNO snapshot(subscribers, churn rate, ARPU, etc.)

- 行动网路营运商公司简介*

- Verizon Communications Inc.

- AT&T Inc.

- T-Mobile US, Inc.

第七章 市场机会与未来展望

US Telecom MNO market size in 2026 is estimated at USD 357.57 billion, growing from 2025 value of USD 344.45 billion with 2031 projections showing USD 431.03 billion, growing at 3.81% CAGR over 2026-2031.

This steady trajectory reflects a mature arena in which legacy voice and messaging streams shrink while data-heavy applications, private cellular deployments, and integrated enterprise platforms expand margins. Heightened monetization of costly 5G assets is central to growth, with operators rolling out premium service tiers, network-as-a-service propositions, and low-latency edge nodes. Private and public sector subsidies for rural coverage, aggressive monetization of spectrum holdings, and AI-driven network automation continue to widen total addressable revenue pools. Competitive intensity remains contained because three national carriers dominate spectrum depth and retail distribution, allowing disciplined pricing even as prepaid churn rises. Capital discipline, energy optimization, and spectrum refarming collectively underpin operators' ability to fund continued densification without materially eroding free cash flow .

US Telecom MNO Market Trends and Insights

5G Stand-Alone Core Roll-outs Accelerating Data Monetization

Full migration to stand-alone (SA) architecture allows carriers to create virtual slices that guarantee latency and throughput, adding service differentiation unavailable on legacy non-stand-alone deployments. T-Mobile commercialized public-safety slices that already contribute USD 200 million in recurring annual revenue, while Verizon leverages SA to support sub-10 millisecond edge workloads for manufacturing robotics . Enterprise deals often bundle API exposure so developers can embed carrier-grade authentication and billing directly into applications, a pathway to an estimated USD 20 billion platform revenue pool by 2028 . Higher-value network slices translate into 3-5 times the ARPU of mass-market mobile broadband, directly lifting the US Telecom MNO market.

Fixed-Wireless Access (FWA) Displacing Legacy Copper

National FWA subscriptions crossed the 10 million mark by end-2024 as mid-band and C-band spectrum enabled 300 Mbps average downlink in rural clusters. The product directly cannibalizes outdated DSL and coax footprints, fills fiber coverage gaps, and accelerates operators' payback on 5G radios. FWA also strengthens household bundling, with wireless carriers attaching mobile lines at an 18% higher rate when a home internet account is present. Capacity constraints in dense suburbs trigger active-antenna expansions and spectrum-sharing algorithms, yet economics remain favorable relative to trenching. Rapid customer growth adds 0.8 percentage points to the US Telecom MNO market CAGR through 2027.

Inflation-Induced ARPU Pressure in Prepaid

Elevated energy and labor expenses compel carriers to raise plan prices, yet prepaid customers exhibit immediate churn when monthly bills climb by more than USD 5. AT&T's 2025 upward revisions triggered a temporary 190-basis-point increase in prepaid churn, forcing larger retention credits and marketing spend. Operators now extend inclusive content bundles, high-data allotments, and buy-now-pay-later device financing to defend subscriber counts, trimming EBITDA margin by 40-60 basis points over the near term.

Other drivers and restraints analyzed in the detailed report include:

- eSIM-Only Device Launches Simplifying Churn

- Federal BEAD and Middle-Mile Grants Stimulating Rural Build-outs

- Fiber Over-builds Eroding FWA Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The data and internet category represented 53.12% of 2025 revenue, delivering the single-largest contribution to the US Telecom MNO market size. Unlimited smartphone plans, FWA subscriptions, and enterprise dedicated access collectively underpinned a 7.8% uplift in mobile data traffic per user year-on-year. Premium tiers exploiting carrier aggregation hit verified 5.5 Gbps throughput during 2025 field tests, reinforcing perceived speed leadership and justifying price differentials. Voice and SMS collectively fell below 10% revenue share as over-the-top substitutes drove double-digit usage declines. Meanwhile, IoT and M2M services posted the fastest trajectory, supported by 30 million incremental licensed cellular endpoints and a swelling pipeline of private network installs inside factories, ports, and hospitals. The sub-segment's 3.92% CAGR through 2031 adds a long-run lift that offsets eroding legacy lines, thereby sustaining expansion in the US Telecom MNO market.

Enterprise data contracts increasingly request SLA-backed throughput and network-slice isolation, commands that draw higher margins and longer-term commitments than consumer lines. Wholesale roaming and virtual operator partnerships add incremental revenue but primarily serve to amortize spectrum assets during off-peak hours. Advanced analytics embedded in self-optimizing networks slash power draw by around 15% and thereby release opex for reinvestment in additional small cells, further reinforcing data-centric positioning across the US Telecom MNO market.

The US Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), and End User (Enterprises, Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Verizon Communications Inc.

- AT&T Inc.

- T-Mobile US, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Regulatory and Policy Framework

- 4.3 Spectrum Landscape and Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic and External Drivers

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers and Penetration Rate

- 4.7.2 Mobile Internet Users and Penetration Rate

- 4.7.3 SIM Connections by Access Technology and Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile and Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 5G Stand-Alone Core Roll-outs Accelerating Data-Monetization

- 4.8.2 Fixed-Wireless Access (FWA) Displacing Legacy Copper

- 4.8.3 eSIM-Only Device Launches Simplifying Churn

- 4.8.4 Federal BEAD and Middle-Mile Grants Stimulating Rural Build-outs

- 4.8.5 Private-Cellular Demand from IIoT and Campus Networks

- 4.8.6 AI-Driven RAN Optimization Lowering OPEX

- 4.9 Market Restraints

- 4.9.1 Inflation-Induced ARPU Pressure in Pre-paid

- 4.9.2 Fiber Over-builds Eroding FWA Economics

- 4.9.3 C-Band Aviation Mitigation Costs

- 4.9.4 Heightened FCC Scrutiny on MandA

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom Sector

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 Product Benchmarking Analysis for mobile network services

- 6.5 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.6 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.6.1 Verizon Communications Inc.

- 6.6.2 AT&T Inc.

- 6.6.3 T-Mobile US, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)