|

市场调查报告书

商品编码

1940705

美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)US MVNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

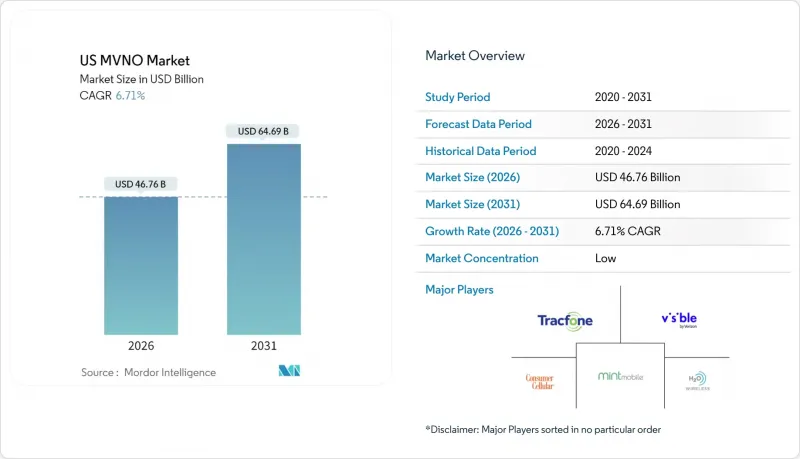

2025年美国行动虚拟网路营运商(MVNO)市值为438.2亿美元,预计2031年将达到646.9亿美元,高于2026年的467.6亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.71%。

强劲成长主要得益于消费者对低价套餐的持续需求、企业物联网连接外包以及云端技术的快速普及加速了产品上市。有线电视业者正利用其宽频优势拓展无线交叉销售,零售商也推出专属eSIM品牌以深化数位互动。大型通讯业者担忧收入稀释,正透过网路切片和策略收购等手段,将批发流量和利润来源锁定在自身生态系统内。持续涌现的API优先型批发平台进一步降低了进入门槛,并刺激了服务创新。这势必会持续加剧美国行动虚拟网路营运商(MVNO)市场各区隔领域的竞争压力。

美国虚拟营运商市场趋势与洞察

对低成本无线套餐的需求不断增长

随着通货膨胀给家庭预算带来压力,越来越多的消费者转向美国行动虚拟网路营运商 (MVNO) 市场的低成本服务。业者也积极响应,推出透明且免佣金的定价方案,价格比主流业者的套餐低 30% 至 40%。 Visible 的五年 15 美元价格保证与 Mint Mobile 引人注目的促销活动相媲美,充分展现了竞争如何影响品牌认知。批量批发协议、高效的后端营运和数位化用户註册流程,使得 MVNO 即使在价格下降的情况下也能维持利润率。口碑推荐和灵活的预付条款降低了用户解约率,强化了成本优势带来的良性循环,进而促进用户成长。

扩大5G覆盖范围以支援MVNO功能对等

全国独立的组网5G网路部署消除了曾经区分低价品牌和网路营运商的效能差距。网路切片技术的普及使虚拟营运商(MVNO)能够提供以往仅限于直接与营运商签订合约的差异化安全、延迟和吞吐量等级。功能上的趋同正在重塑竞争格局:品牌不再为数据速度慢而道歉,而是着重宣传游戏通行证、AR特权和捆绑云端储存等服务创新。随着设备升级週期的加快,新款5G设备预设支援eSIM配置,进一步促进了用户更顺畅地过渡到美国MVNO市场。

网路优先顺序降低对服务品质感知的影响

大多数批发合约在网路拥塞尖峰时段期分配的是QCI 9频宽,导致用户网速比后付费业者用户慢。城市高峰时段资料通讯不可用的申诉正在损害品牌信誉,迫使美国行动虚拟网路营运商(MVNO)市场参与者要么加大价格竞争,要么协商更昂贵的QCI 8频宽存取。 2025年初发生的重大服务中断事件以及Mint Mobile间歇性限速问题凸显了社群媒体如何迅速传播负面使用者体验。除非MVNO营运商能够获得优先通道或依赖卫星备用方案,否则承诺与现实之间的差距可能会导致客户流失激增。

细分市场分析

2025年,云端部署将占美国行动虚拟网路营运商(MVNO)市场57.25%的份额,复合年增长率(CAGR)为12.89%。这种架构无需资本密集型硬件,并可灵活扩展用户规模以满足激增的需求。 AT&T的MVNX等平台即服务(PaaS)解决方案将收费、策略和分析功能整合到模组化API中,从而将服务推出时间从数月缩短至数週。这种转型可将营运成本降低高达40%,进而释放资源用于行销和功能开发。虽然本地部署解决方案在高度监管的行业仍然很受欢迎,但随着云端认证的普及,其市场份额正在下降。容器化微服务的柔软性确保了与卫星网关和物联网设备云端的未来集成,为云端MVNO抓住美国MVNO市场下一波成长浪潮奠定了基础。

云端运算思维催生了一种快速试错的文化。品牌可以即时进行A/B测试,透过无线方式向配套应用程式推送更新,并将客户流失风险的征兆可视化,从而推动有针对性的客户留存计画。资料居住问题曾经是发展的障碍,如今正透过符合州隐私法的独立云端区域来解决。早期采用者报告称,在迁移到由云端人工智慧驱动的全自动支援聊天机器人后,用户净推荐值(NPS)有所提高。这些因素共同作用,使云端营运成为实验的核心,保持美国行动虚拟网路营运商(MVNO)市场的活力和竞争力。

2025年,全功能虚拟业者(MVNO)将占据美国MVNO市场的45.30%,复合年增长率(CAGR)为10.73%。拥有核心网路元件使这些业者能够客製化费率方案、整合金融科技附加服务,并收集详细的用户资料以优化提升销售演算法。 CompaxDigital与T-Mobile的BSS/OSS集成,展示了品牌在无需从零开始建立基础设施的情况下,如何利用策略工具实现深度整合。虽然在优先考虑快速上线而非差异化的情况下,轻量级MVNO仍然具有吸引力,但价格压缩正迫使许多运营商在用户数量达到盈亏平衡点后转向完全掌控网路。

营运自主权能够保护完全虚拟网路营运商 (MVNO) 免受批发政策突变的影响,例如新的限速规则和 SIM 卡交换费。它还能简化与多家营运商的谈判,这对于将地面电波和卫星网路整合到单一产品单元 (SKU) 中至关重要。随着获客成本的上升,拥有交叉销售接点(从设备保险到串流媒体套餐)的价值正在飙升,这推动了美国 MVNO 市场向完全 MVNO 模式的策略转型。

美国行动虚拟网路营运商 (MVNO) 市场报告按部署模式(云端/本地部署)、营运类型(经销商/其他)、用户类型(消费者/企业/其他)、用途(折扣/商业/其他)、网路技术(2G/3G/其他)和分销通路(线上/纯数位/实体零售/其他)进行细分。市场预测以价值(美元)和用户数量(用户数)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对低成本无线套餐的需求不断增长

- 扩大5G覆盖范围将使行动虚拟网路营运商(MVNO)之间的功能对等。

- 将物联网连接外包给行动虚拟网路营运商 (MVNO) 以服务企业

- FCC的亲竞争政策与批发授权

- 零售商推出的仅支援 eSIM 的数位品牌正在崛起

- 利用API驱动的批发市场降低进入门槛

- 市场限制

- 网路优先顺序降低对服务品质感知的影响

- 价格竞争进一步挤压了虚拟业者本已微薄的利润空间。

- 小众虚拟网路营运商 (MVNO) 数位广告客户获取成本 (CAC) 不断上升

- 行动网路营运商对5G-SA切片接取的限制阻碍了服务创新。

- 价值链分析

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 对影响市场的宏观经济因素进行评估

第五章 市场规模及成长预测(价值及数量)

- 按部署模式

- 云

- 本地部署

- 按操作模式

- 经销商

- 服务提供者

- 完整的虚拟营运商

- 轻量级/品牌虚拟营运商

- 用户类型

- 个人

- 公司

- 仅限物联网

- 透过使用

- 折扣

- 营业内容

- 细胞M2M

- 其他的

- 透过网路技术

- 2G/3G

- 4G/LTE

- 5G

- 卫星通讯/NTN

- 透过分销管道

- 线上/数位独家

- 传统零售店

- 职业子品牌店

- 第三方/批发

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Tracfone Wireless

- H2O Wireless

- Visible

- Mint Mobile

- Consumer Cellular

- Cricket Wireless

- Straight Talk Wireless

- Boost Mobile

- Metro by T-Mobile

- Google Fi Wireless

- TruConnect

- Ting Mobile

- Red Pocket Mobile

- US Mobile

- Simple Mobile

- Total by Verizon

- Xfinity Mobile

- Spectrum Mobile

- TextNow

- Optimum Mobile

- Lycamobile USA

第七章 市场机会与未来展望

The US MVNO Market was valued at USD 43.82 billion in 2025 and estimated to grow from USD 46.76 billion in 2026 to reach USD 64.69 billion by 2031, at a CAGR of 6.71% during the forecast period (2026-2031).

Robust growth comes from sustained consumer appetite for lower-cost plans, enterprise outsourcing of IoT connectivity, and rapid cloud adoption that cuts time-to-market. Cable operators translate broadband strength into wireless cross-sell gains, while retailers launch eSIM-only brands that deepen digital engagement. Large carriers, worried about revenue dilution, counter with network slicing and strategic acquisitions that keep wholesale traffic-and profit streams-inside their own ecosystems. The steady influx of API-first wholesale platforms further flattens entry barriers and stimulates service innovation, ensuring that competitive pressure remains intense across every segment of the US MVNO market.

US MVNO Market Trends and Insights

Growing demand for budget-friendly wireless plans

Inflation keeps household budgets tight, pushing more consumers toward low-cost offerings in the US MVNO market. Operators answer with transparent, fee-free pricing that undercuts major carrier plans by 30-40%. Visible's five-year USD 15 rate guarantee directly counters Mint Mobile's headline promotions and illustrates how price competition now shapes brand perception. Bulk wholesale agreements, lean back-end operations, and digital onboarding let MVNOs preserve margins even while rates fall. Word-of-mouth referrals and flexible prepaid terms push churn down, reinforcing the cost advantage loop that sustains subscriber expansion.

5G coverage expansion supporting MVNO feature parity

Nationwide standalone 5G deployments erase the performance gap that once separated discount brands from network owners. Access to network slicing allows MVNOs to offer differentiated security, latency, and throughput tiers once reserved for direct carrier contracts. Feature parity reshapes competitive positioning: brands now lead with service innovation-gaming passes, AR perks, or bundled cloud storage-rather than apologizing for slower data. As device upgrade cycles accelerate, new 5G-only handsets default to eSIM provisioning, further smoothing customer migration to the US MVNO market.

Network deprioritization impacting perceived QoS

Most wholesale contracts allocate QCI 9 during peak congestion, leaving subscribers with slower speeds than postpaid carrier users. Complaints of unusable data during city-center rush hours dent brand credibility, forcing US MVNO market players to double down on price or negotiate costly premium QCI 8 access. Visible downtime in early 2025 and Mint Mobile's intermittent throttling issues highlight how quickly social media amplifies negative user experiences. Unless MVNOs secure higher priority lanes or lean on satellite fallback, the gap between promise and reality could flare into churn spikes.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise and IoT connectivity outsourcing to MVNOs

- FCC pro-competition policies and wholesale mandates

- Price wars compressing already thin MVNO margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments held a 57.25% share of the US MVNO market in 2025 and are growing at a 12.89% CAGR. These architectures strip away capex-heavy hardware and let operators scale subscribers in line with demand surges. Platform-as-a-Service offerings-such as ATandT's MVNX stack-bundle billing, policy, and analytics into modular APIs that speed launch cycles from months to weeks. The shift lowers operating costs by up to 40%, freeing resources for marketing and feature development. On-premise solutions remain the pick for heavily regulated verticals, but their share erodes as cloud certifications expand. The flexibility of containerized microservices also future-proofs integrations with satellite gateways and IoT device clouds, positioning cloud MVNOs to capture the next wave of US MVNO market growth.

The cloud mindset fosters a fail-fast culture: brands A/B test plan mixes in real time, push over-the-air updates to companion apps, and surface churn-risk signals that prompt targeted retention offers. Data residency concerns, once a stumbling block, now find remedies in sovereign cloud zones that meet state privacy statutes. Early adopters report subscriber NPS gains after migrating to fully automated support chatbots anchored on cloud AI. Together, these factors make cloud operation the engine room of experimentation that keeps the US MVNO market vibrant and fiercely competitive.

Full MVNOs represented 45.30% of US MVNO market share in 2025 and are expanding at a 10.73% CAGR. Ownership of core network elements lets these players customize rate plans, embed fintech add-ons, and harvest granular usage data that refines upsell algorithms. CompaxDigital's BSS/OSS link-up with T-Mobile demonstrates the strategic tooling now available to brands that want deeper integration without building infrastructure from scratch. Light MVNOs still appeal when speed to launch outweighs differentiation needs, but price compression forces many to graduate toward full control as soon as subscriber bases hit breakeven scale.

Operational autonomy shields full MVNOs from abrupt wholesale policy changes, such as new throttling rules or SIM swap fees. It also simplifies multi-carrier negotiations, a critical advantage when bundling terrestrial and satellite links into single SKUs. As consumer acquisition costs rise, the value of owning cross-sell touchpoints-from device insurance to streaming bundles-climbs sharply, reinforcing the strategic migration toward full MVNO status in the US MVNO market.

The US MVNO Market Report is Segmented by Deployment Model (Cloud, On-Premises), Operational Mode (Reseller, and More), Subscriber Type (Consumer, Enterprise, and More), Application (Discount, Business and More), Network Technology (2G/3G, and More), Distribution Channel (Online/Digital-only, Traditional Retail Stores, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Tracfone Wireless

- H2O Wireless

- Visible

- Mint Mobile

- Consumer Cellular

- Cricket Wireless

- Straight Talk Wireless

- Boost Mobile

- Metro by T-Mobile

- Google Fi Wireless

- TruConnect

- Ting Mobile

- Red Pocket Mobile

- US Mobile

- Simple Mobile

- Total by Verizon

- Xfinity Mobile

- Spectrum Mobile

- TextNow

- Optimum Mobile

- Lycamobile USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for budget-friendly wireless plans

- 4.2.2 5G coverage expansion supporting MVNO feature parity

- 4.2.3 Enterprise & IoT connectivity outsourcing to MVNOs

- 4.2.4 FCC pro-competition policies and wholesale mandates

- 4.2.5 Rise of eSIM-only digital brands launched by retailers

- 4.2.6 API-driven wholesale marketplaces lowering entry barriers

- 4.3 Market Restraints

- 4.3.1 Network deprioritization impacting perceived QoS

- 4.3.2 Price wars compressing already thin MVNO margins

- 4.3.3 Rising digital-ad CAC for niche MVNO customer acquisition

- 4.3.4 MNO 5G-SA slice-access lockouts limiting service innovation

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Operational Mode

- 5.2.1 Reseller

- 5.2.2 Service Operator

- 5.2.3 Full MVNO

- 5.2.4 Light / Brand MVNO

- 5.3 By Subscriber Type

- 5.3.1 Consumer

- 5.3.2 Enterprise

- 5.3.3 IoT-specific

- 5.4 By Application

- 5.4.1 Discount

- 5.4.2 Business

- 5.4.3 Cellular M2M

- 5.4.4 Others

- 5.5 By Network Technology

- 5.5.1 2G/3G

- 5.5.2 4G/LTE

- 5.5.3 5G

- 5.5.4 Satellite/NTN

- 5.6 By Distribution Channel

- 5.6.1 Online/Digital-only

- 5.6.2 Traditional Retail Stores

- 5.6.3 Carrier Sub-brand Stores

- 5.6.4 Third-Party/Wholesale

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tracfone Wireless

- 6.4.2 H2O Wireless

- 6.4.3 Visible

- 6.4.4 Mint Mobile

- 6.4.5 Consumer Cellular

- 6.4.6 Cricket Wireless

- 6.4.7 Straight Talk Wireless

- 6.4.8 Boost Mobile

- 6.4.9 Metro by T-Mobile

- 6.4.10 Google Fi Wireless

- 6.4.11 TruConnect

- 6.4.12 Ting Mobile

- 6.4.13 Red Pocket Mobile

- 6.4.14 US Mobile

- 6.4.15 Simple Mobile

- 6.4.16 Total by Verizon

- 6.4.17 Xfinity Mobile

- 6.4.18 Spectrum Mobile

- 6.4.19 TextNow

- 6.4.20 Optimum Mobile

- 6.4.21 Lycamobile USA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)