|

市场调查报告书

商品编码

1937405

泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)Thailand Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

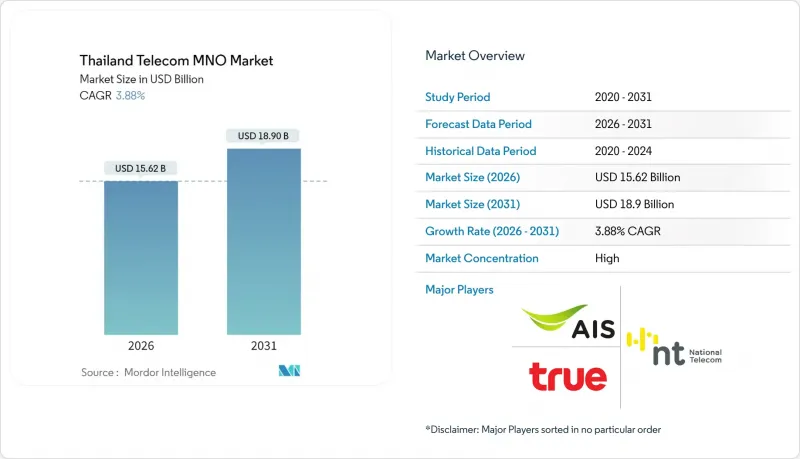

2025年泰国电信行动网路营运商市场价值150.4亿美元,预计到2031年将达到189亿美元,高于2026年的156.2亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.88%。

这一成长轨迹表明,在包括AIS-True-dtac双寡头垄断格局、5G加速部署以及向企业主导的专用网路转型等结构性变化中,营收仍保持稳定成长。数据和互联网服务已占收入的约三分之二,物联网连接正在全国范围内的NB-IoT基础设施中快速扩展。同时,东部经济走廊的智慧产业计划正在推动对超低延迟连接的大规模投资,而农村地区智慧型手机普及率的提高也扩大了潜在用户群体。在监管方面,频谱价格上涨给营运商的财务状况带来了压力,而数位经济支持目标和普遍服务义务基金则为网路扩展开闢了新的途径。因此,竞争格局正在从单纯的价格竞争转向技术领先、服务品质和企业解决方案的深度。

泰国电信行动网路营运商市场趋势与洞察

全国范围内的 5G 部署加速了行动数据货币化

到2024年,5G网路将覆盖泰国95%的人口,为通讯业者实现比4G快24倍的速度奠定基础,并支持推出高端定价模式。 AIS总合获得超过1460MHz的频谱资源,涵盖低频、中频和高频频宽,并取得了泰国最高的118.84Mbps速度评分。除了面向消费者的eMBB服务外,该基础设施还将支援边缘运算架构,并为企业开闢新的收入来源。 True Corporation正在透过2.6GHz频段的动态频谱共用来提高频谱效率,使其能够同时支援4G和5G流量。在泰国美的工厂等地的私人5G部署,已实现了15-20%的效率提升和30%的营运成本节约,这表明企业愿意为有保障的吞吐量付费。根据政府预测,到 2035 年,5G 预计将为国内生产总值) 增加 93 亿美元,进一步巩固泰国通讯业者市场的数据驱动型成长地位。

OTT影片和游戏流量的快速成长推动了ARPU值的成长

OTT影片和云端游戏平台的普及导致行动数据消耗激增,推动了用户向高端套餐的转变,尤其是在都市区千禧世代。提供包含加值内容、服务品质保证和无限资料通讯的业者发现,5G用户的平均每用户收入(ARPU)比4G用户高出10-15%。云端游戏对延迟的敏感度使得5G独立组网(SA)模式更具优势,从而能够提供差异化的服务,降低曼谷竞争激烈的后付费市场中的客户流失率。在全国范围内,55%的亚太地区通讯业者预计2024年ARPU将实现成长,泰国通讯业者也正顺应这一趋势,采用基于使用量的分级收费系统。全高清和4K影片串流媒体是最大的流量类别,因此需要在人口密集地区持续增加无线接取网路的密度。

全球最高的频谱授权费对营运商的财务状况造成压力

泰国2023年的频谱竞标筹集了32亿美元,使其成为全球人均频谱使用费最高的国家。经济模拟显示,若牌照费超过2,000亿泰铢,五年内5G普及率将降至50%,低于低成本情境的70%。 True Corporation公布季度亏损,部分原因是频谱相关债务的高利率。泰国国家电信公司对700MHz频谱的343亿泰铢投资也同样拖累了现金流,凸显了未来网路投资预算面临的结构性压力。高昂的维修成本可能延缓遍远地区的5G部署,并限制先进独立组网(SA)能力的研发。

细分市场分析

预计到2025年,数据和网路收入将占泰国电信行动网路营运商(MNO)市场份额的63.78%,并在2031年之前保持领先地位,这主要得益于影片串流、云端游戏和远端办公应用的兴起。语音流量持续长期下降,随着即时通讯应用取代传统短信,其在泰国电信MNO市场规模中的占比已降至10.00%以下。物联网(IoT)和机器对机器(M2M)目前收入占比不高,但其复合年增长率(CAGR)高达4.00%,是增长最快的领域,这主要得益于全国范围内的窄带物联网(NB-IoT)覆盖和工业级5G独立组网(SA)切片技术的应用,后者支持性部署、物流和维护。通讯业者正将连接服务与设备管理平台和分析仪錶板结合,以实现远高于基本数据费率的平均每连接收入(ARPC)。 OTT和付费电视服务提供了交叉销售机会:True利用其内容库,而AIS则与全球串流媒体品牌合作,透过零费率优惠来鼓励用户升级资料方案。

泰国差异化的频谱拥有情形正在重塑服务经济格局。 AIS 新增的 700 MHz频宽提升了资讯服务的室内覆盖范围,而 True 的 2.6 GHz DSS 则提高了峰值容量。两家业者都在试点网路切片概念验证,为工厂、医院和 AGV 车队提供有保障的延迟服务。全球预测显示,到 2029 年,蜂巢式物联网连接数将达到 64 亿,泰国通讯业者正致力于透过产业客製化解决方案抢占这一市场的重要份额。附加价值服务(VAS) 和漫游服务目前仍处于小众市场,但随着泰国旅游业需求的復苏,其重要性日益凸显。与区域合作伙伴达成的无缝 5G漫游协定,使通讯业者能够吸引高消费游客。

泰国电信行动网路业者 (MNO) 市场按服务类型(语音服务、数据及网际网路服务、通讯服务、物联网及机器对机器 (IoT & M2M) 服务、OTT 及付费电视服务、其他服务)及最终用户(企业、消费者)进行细分。市场预测以价值(美元)和用户数量(用户数)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 监理与政策框架

- 频谱环境与竞争格局

- 通讯业生态系统

- 宏观经济与外在因素

- 波特五力分析

- 竞争对手之间的竞争

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 领先行动网路营运商的关键绩效指标(2020-2025)

- 独立行动用户和渗透率

- 行动网路使用者数量和普及率

- 按接入技术分類的SIM卡连线数和渗透率

- 蜂巢式物联网/M2M连接

- 宽频连线(移动和固定)

- ARPU(每位用户平均收入)

- 每用户平均数据使用量(GB/月)

- 市场驱动因素

- 全国范围内的 5G 部署加速了行动数据货币化

- OTT影片和游戏流量的快速成长推动了ARPU值的成长

- 企业数位转型推动专用LTE和5G SA的需求

- 智慧型手机在农村地区的普及率飙升

- 东部经济走廊(EEC)智慧产业计划需要超低延迟连接

- 普遍服务义务(USO)基金对远距基地台的补贴

- 市场限制

- 全球最高的频谱牌照费对营运商的财务状况带来了压力。

- True-dtac合併后采取的纾困措施加剧了价格竞争。

- 国家数位身分实施的延迟限制了先进的金融科技和电信捆绑业务的发展

- 高密度5G基地台网路将推高电费

- 技术展望

- 电信业主要经营模式分析

- 定价模式和定价分析

第五章 市场规模与成长预测

- 通信总收入和每位用户平均收入

- 按服务类型

- 语音服务

- 数据和网际网路服务

- 通讯服务

- 物联网和机器对机器服务

- OTT和付费电视服务

- 其他服务(附加价值服务、漫游和国际服务、企业和批发服务等)

- 最终用户

- 公司

- 一般消费者

第六章 竞争情势

- 市场集中度

- 主要供应商的策略与投资动向(2023-2025)

- 2024年行动网路营运商市场占有率分析

- Product Benchmarking Analysis for mobile network services

- MNO snapshot(subscribers, churn rate, ARPU, etc.)

- 行动网路营运商公司简介*

- Advanced Info Service(AIS)

- True Corporation Public Company Limited

- National Telecom(NT)

第七章 市场机会与未来展望

The Thailand Telecom MNO Market was valued at USD 15.04 billion in 2025 and estimated to grow from USD 15.62 billion in 2026 to reach USD 18.9 billion by 2031, at a CAGR of 3.88% during the forecast period (2026-2031).

That trajectory reflects measured topline expansion even as the sector undergoes deep structural change driven by the AIS-True-dtac duopoly, accelerated 5G rollouts, and an enterprise-led push toward private networks. Data and Internet services already account for almost two-thirds of revenue, while IoT connections scale quickly on nationwide NB-IoT infrastructure. At the same time, the Eastern Economic Corridor's smart-industry projects anchor large investments in ultra-low-latency connectivity, and rising rural smartphone adoption broadens the addressable subscriber base. On the regulatory front, high spectrum prices weigh on operator finances, yet supportive digital-economy targets and the Universal Service Obligation Fund open further network-expansion avenues. Competitive differentiation, therefore, shifts from pure price plays to technology leadership, quality of service, and enterprise solution depth.

Thailand Telecom MNO Market Trends and Insights

Nationwide 5G rollout accelerating mobile data monetization

5G networks covered 95% of Thailand's population in 2024, giving operators a platform for speed improvements 24 times faster than 4G and enabling premium pricing tiers . AIS holds more than 1,460 MHz across low-, mid-, and high-bands, translating into the country's highest Speed Score of 118.84 . Beyond consumer eMBB services, the same infrastructure supports edge-computing architectures that unlock new enterprise revenue streams. True Corporation improves spectral efficiency through Dynamic Spectrum Sharing on the 2.6 GHz band, a method that concurrently sustains 4G and 5G traffic. Private 5G deployments at factories like Midea Thailand delivered 15-20% efficiency gains and 30% opex savings, validating enterprise willingness to pay for guaranteed throughput. Government projections show 5G could inject USD 9.3 billion into national GDP by 2035, further anchoring the Thailand Telecom MNO market to data-driven growth .

Explosion in OTT video and gaming traffic driving ARPU uplift

Mobile data consumption surged as over-the-top video and cloud-gaming platforms gained traction, prompting a migration to higher-tier plans across urban millennials. Operators that bundle premium content, quality-of-service guarantees, and unlimited data observe ARPU premiums of 10-15% among 5G users versus 4G cohorts. Cloud gaming's sensitivity to latency favors 5G standalone slices, enabling differentiated offers that reduce churn in the highly contested Bangkok post-paid segment. Nationally, 55% of Asia-Pacific operators posted ARPU growth in 2024, and Thai carriers mirror this trend by leveraging data-usage-based pricing ladders. Video streaming in full-HD and 4K constitutes the single largest traffic category, compelling continued radio-access-network densification across populous corridors.

World-leading spectrum license fees straining operator balance sheets

Thailand's 2023 auctions raised USD 3.2 billion, positioning its spectrum fees among the costliest worldwide on a per-capita basis. Economic simulations show that license costs above THB 200 billion reduce five-year 5G adoption to 50%, versus 70% under lower-cost scenarios . True Corporation reported quarterly losses attributable in part to elevated interest expenses on spectrum-related debt. National Telecom's THB 34.3 billion outlay for 700 MHz blocks similarly eroded cash flow, highlighting systemic pressure on future network-investment budgets. High carrying costs risk delaying rural 5G rollouts and curtailing R&D for advanced standalone capabilities.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise digital-transformation boosting private-LTE and 5G SA demand

- Soaring smartphone penetration in rural provinces

- Intensifying price wars following True-dtac merger remedies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data and Internet revenue represented 63.78% of Thailand Telecom MNO market share in 2025 and is projected to retain primacy through 2031 as video streaming, cloud gaming, and remote work applications multiply. Voice traffic continues its secular decline, falling below 10.00% of Thailand Telecom's MNO market size as messaging apps displace traditional SMS. IoT and M2M contribute a modest top-line share today but register the fastest 4.00% CAGR, driven by nationwide NB-IoT availability and industrial-grade 5G SA slices that enable predictive maintenance, logistics tracking, and smart-meter rollouts. Operators bundle connectivity with device-management platforms and analytics dashboards, broadening average revenue per connection well beyond basic data charges. OTT and Pay-TV services present cross-sell upside: True leverages its content library while AIS partners with global streaming brands, using zero-rating to spur data-plan upgrades.

Thailand's differentiated spectrum holdings shape service-type economics. AIS's additional 700 MHz blocks improve in-building coverage for data services, while True's 2.6 GHz DSS boosts peak capacity. Both carriers pilot network-slicing proofs-of-concept that sell guaranteed latency to factories, hospitals, and AGV fleets. Global forecasts place 6.4 billion cellular-IoT connections by 2029, and Thai operators seek an outsized slice of that volume through vertical-specific solutions. VAS and roaming lines remain niche but gain relevance as Thailand reopens tourism flows; seamless 5G roaming agreements with regional partners position carriers to capture high-spending visitors.

The Thailand Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), and End User (Enterprises, Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Advanced Info Service (AIS)

- True Corporation Public Company Limited

- National Telecom (NT)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Regulatory and Policy Framework

- 4.3 Spectrum Landscape and Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic and External Drivers

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers and Penetration Rate

- 4.7.2 Mobile Internet Users and Penetration Rate

- 4.7.3 SIM Connections by Access Technology and Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile and Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 Nationwide 5G rollout accelerating mobile data monetisation

- 4.8.2 Explosion in OTT video and gaming traffic driving ARPU uplift

- 4.8.3 Enterprise digital-transformation boosting private-LTE and 5G SA demand

- 4.8.4 Soaring smartphone penetration in rural provinces

- 4.8.5 Eastern Economic Corridor (EEC) smart-industry projects requiring ultra-low-latency connectivity

- 4.8.6 Universal Service Obligation (USO) Fund subsidies for remote-area base-stations

- 4.9 Market Restraints

- 4.9.1 World-leading spectrum licence fees straining operator balance sheets

- 4.9.2 Intensifying price wars following True-dtac merger remedies

- 4.9.3 Delay in National Digital-ID rollout limiting advanced fintech-telco bundles

- 4.9.4 Rising electricity costs for dense 5G site grids

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom Sector

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 Product Benchmarking Analysis for mobile network services

- 6.5 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.6 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.6.1 Advanced Info Service (AIS)

- 6.6.2 True Corporation Public Company Limited

- 6.6.3 National Telecom (NT)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)