|

市场调查报告书

商品编码

1940848

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)ASEAN Mobile Virtual Network Operator (MVNO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

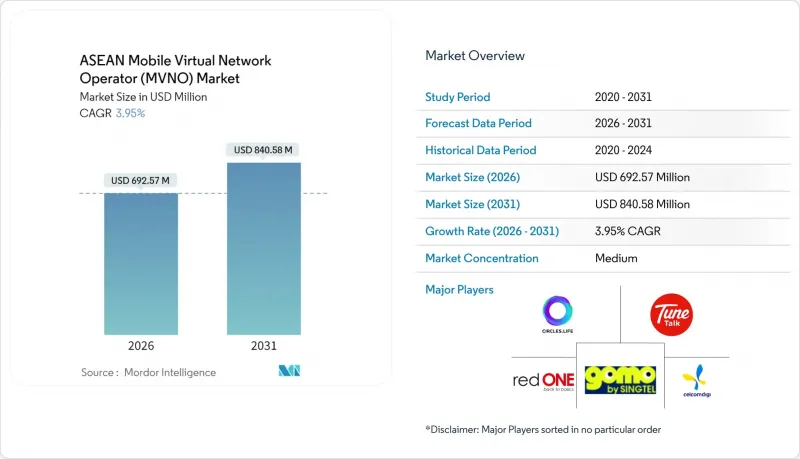

预计东协行动虚拟网路营运商 (MVNO) 市场将从 2025 年的 6.6625 亿美元成长到 2026 年的 6.9257 亿美元,到 2031 年将达到 8.4058 亿美元,2026 年至 2031 年的复合年增长率为 3.95%。

就用户数而言,市场规模预计将从2025年的814万成长到2030年的945万,预测期间(2025-2030年)复合年增长率(CAGR)为3.03%。这一显着成长主要得益于卫星和其他非地面电波网路(NTN)的扩张,虚拟通讯业者采用混合架构,规避了传统行动通讯业者(MNO)的基础设施限制。云端原生核心网、跨境eSIM套餐和放鬆管制正在共同重塑竞争格局,使灵活的新进入者无需大量资本支出即可实现规模化发展。对年轻人资料方案和企业物联网连接的需求正在推动流量成长,而行动网路营运商的数位子品牌则加剧了价格竞争,并透过附加价值服务迫使市场差异化。主权资料法规和区域漫游要求之间的相互作用,使得合规专业知识成为东协虚拟行动网路营运商(MVNO)市场所有参与者的策略资产。

东协行动虚拟网路营运商(MVNO)市场趋势与洞察

行动互联网和智慧型手机普及率不断提高

到2025年,东协地区的智慧型手机普及率将超过67%,超过4.4亿行动网路用户将期待高容量资料通讯和流畅的应用体验。越南新颁布的《电信法》将机器对机器(M2M)通讯归类为基础服务,允许行动虚拟网路营运商(MVNO)无需附加价值服务许可证即可销售物联网连接服务。这项明确规定正在加速工业领域的应用,尤其是在中国当地以外地区多元化发展的电子和服饰产业丛集中。虚拟通讯业者( VOC)受惠于提供纯数据套餐,因此免去了传统的语音通话费用。然而,数据使用量的快速成长正在压缩单位成本,因此需要先进的流量管理工具来维持东协MVNO市场的利润率。

关于批发准入的监理改革

越南第163/2024号法令规定了非歧视性的批发条款,为海外云端服务提供了明确的程序,并缩短了境外託管MVNO核心网的核准週期。马来西亚的单一批发网络模式为覆盖率高达80%的人口提供折扣5G资费,但其集中式结构限制了MNO产品的差异化,并为面向企业垂直领域的全功能MVNO拓展了机会。泰国继续以区域区块进行频谱竞标,迫使MVNO在多个省份之间协商漫游协议。这些政策转变将为东协MVNO市场引入新进者,并使其能够在不同的法规环境下维持统一的服务品质。

批发定价柔软性有限

儘管存在鼓励竞争的政策,但真正基于成本的批发价格谈判仍然充满挑战,尤其是在现有业者拥有频谱优势的地区。泰国区域频谱碎片化迫使虚拟营运商(MVNO)签订多份漫游协定,削弱了它们的议价能力。不断上涨的5G基础设施成本促使行动网路营运商(MNO)收取高额接取附加费,限制了虚拟业者建立维持利润率的入门级套餐的能力。这种限制迫使东协虚拟营运商市场的许多品牌要么透过附加价值服务来抵消高昂的网路费用,要么探索卫星卸载策略。

细分市场分析

预计到2025年,基于云端的核心网路将占东协虚拟营运商(MVNO)市场规模的65.32%,并在2031年之前以8.83%的复合年增长率成长。这主要得益于虚拟业者优先考虑营运支出(OpEx)而非资本支出(CapEx),并积极寻求快速的跨境扩张。越南2024年第163号法令(将海外云端视为基于註册而非许可证的系统)的监管澄清,进一步加速了云端技术的普及。云端的扩充性降低了小众品牌进入市场的门槛,并支援即时分析,从而优化东协MVNO市场的定价、行销和反诈骗策略。

在延迟、冗余和资料居住规则比成本更重要的情况下,本地部署仍将继续。金融机构和公共机构通常会在国家资料中心内申请私人核心网路。混合部署结合了云端控制和边缘处理,并利用 5G 非地面电波网路网关来扩展覆盖范围。采用这种混合模式的营运商报告称,在光纤中断期间,服务连续性得到了改善,并且对重视确定性性能的工业客户更具吸引力。

转售/精简模式仍占据东协虚拟行动网路营运商 (MVNO) 市场 60.85% 的份额,因为它能够以最少的基础设施实现快速商业化。然而,其对主机运营商的高度依赖限制了服务的客製化。全功能 MVNO 虽然资本密集,但在对直接互联的需求推动下,正以 18.12% 的复合年增长率成长。这种直接互联能够实现企业路由自主性、网路切片能力以及差异化的物联网和企业服务。这些业者直接控制 IMS 核心网路、发卡银行配置伺服器和批发采购,从而带来更高的每用户平均收入 (ARPU)。

服务供应商型虚拟营运商 (MVNO) 占据中间位置,拥有 HLR/HSS 等技术,但将无线存取控制权交给行动网路营运商 (MNO)。这吸引了那些重视忠诚度整合但又希望避免大规模电信投资的大型电商公司。因此,东协 MVNO 市场呈现多元化格局,涵盖了从纯粹的品牌建设企业到垂直整合的新兴企业,每家公司都根据其目标细分市场的经济状况量身定制架构。

这份《东协行动虚拟网路营运商(MVNO)市场报告》依部署模式(例如,云端/本地部署)、营运模式(例如,服务供应商)、用户类型(例如,消费者)、使用情况(例如,折扣服务)、网路技术(例如,2G/3G)、分销通路(例如,线上/纯数位通路)和国家/地区进行细分。市场预测以价值(美元)和数量(用户数)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 行动互联网和智慧型手机普及率不断提高

- 关于批发准入的监理改革

- 年轻人对价格实惠的资料方案的需求

- 行动网路营运商数位子品牌整合策略

- 跨境eSIM旅游套装快速成长

- 面向物联网的企业MVNO采用情况

- 市场限制

- 批发定价柔软性有限

- 跨国授权的复杂性

- 云端核心中的资料主权问题

- 5G-SA资源对MVNO QoS的限制

- 价值链分析

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 对影响市场的宏观经济因素进行评估

第五章 市场规模与成长预测

- 按部署模式

- 云

- 本地部署

- 按操作模式

- 经销商/精简版/品牌虚拟营运商

- 服务提供者

- 完整的虚拟营运商

- 用户类型

- 消费者

- 对于企业

- 物联网专用类型

- 透过使用

- 折扣

- 商业

- 细胞M2M

- 其他的

- 透过网路技术

- 2G/3G

- 4G/LTE

- 5G

- 卫星通讯/NTN

- 透过分销管道

- 线上/数位独家

- 传统零售店

- 通讯业者子品牌商店

- 第三方/批发

- 按国家/地区

- 汶莱

- 柬埔寨

- 印尼

- 寮国

- 马来西亚

- 缅甸

- 菲律宾

- 新加坡

- 泰国

- 越南

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Circles.Life(Liberty Wireless Pte Ltd.)

- GOMO(Singtel Mobile Singapore Pte Ltd.)

- redONE Network Sdn Bhd

- Tune Talk Sdn Bhd

- Celcom Berhad

- XOX Mobile Sdn Bhd

- MyRepublic Limited

- Cherry Prepaid(Cosmic Technologies Inc.)

- Itel Mobile(Transsion Holdings)

- Wintel(Masan Group Corporation)

- Penguin Telecom(Advanced Wireless Network Co., Ltd.)

第七章 市场机会与未来展望

The ASEAN Mobile Virtual Network Operator Market is expected to grow from USD 666.25 million in 2025 to USD 692.57 million in 2026 and is forecast to reach USD 840.58 million by 2031 at 3.95% CAGR over 2026-2031.

In terms of subscriber volume, the market is expected to grow from 8.14 million subscribers in 2025 to 9.45 million subscribers by 2030, at a CAGR of 3.03% during the forecast period (2025-2030). Behind this headline growth, satellite and other non-terrestrial networks (NTN) expand as virtual operators adopt hybrid architectures that bypass traditional mobile-network-operator (MNO) infrastructure constraints. Cloud-native cores, cross-border eSIM packages, and regulatory liberalization collectively reshape competitive dynamics, allowing nimble entrants to scale without heavy capex. Demand for youth-centric data plans and enterprise IoT connectivity amplifies traffic volumes, while MNO digital sub-brands intensify price competition and force differentiation through value-added services. The interplay of sovereign data rules and regional roaming requirements makes compliance expertise a strategic asset for every participant in the ASEAN MVNO market.

ASEAN Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Rising Mobile-Internet and Smartphone Penetration

Smartphone ownership surpassed 67% of the ASEAN population in 2025, translating into more than 440 million mobile internet users who expect high-data allowances and seamless app experiences. Vietnam's new telecom framework classifies machine-to-machine (M2M) traffic as a basic service, enabling MVNOs to sell IoT connectivity without value-added service permits . The clarification accelerates industrial adoption, especially in electronics and garment clusters that diversify beyond mainland China. Virtual operators capitalize by offering data-only plans free from legacy voice costs, yet the surge in data usage compresses unit prices and demands sophisticated traffic-management tools to sustain margins within the ASEAN MVNO market.

Regulatory Reforms on Wholesale Access

Vietnam's Decree 163/2024 mandates nondiscriminatory wholesale terms and codifies clear procedures for offshore cloud services, reducing approval cycles for MVNO cores hosted outside the country . Malaysia's single-wholesale-network model offers discounted 5G rates until 80% population coverage, but its centralized structure limits MNO product differentiation and widens opportunities for full MVNOs targeting enterprise verticals. Thailand continues to auction spectrum in regional blocks, compelling MVNOs to negotiate roaming in multiple provinces. Collectively, these policy shifts open the ASEAN MVNO market to new entrants that can juggle divergent regimes while maintaining uniform quality of service.

Limited Wholesale Pricing Flexibility

Despite pro-competition mandates, negotiating genuinely cost-based wholesale rates remains difficult, particularly where incumbent operators wield spectrum advantages. Thailand's provincial spectrum fragmentation forces MVNOs into multiple roaming contracts that dilute bargaining power. Elevated 5G infrastructure costs prompt MNOs to impose premium access surcharges, limiting the ability of virtual players to craft entry-level plans that preserve margin. This restraint compels many brands in the ASEAN MVNO market to offset higher network charges with value-added services or to explore satellite offload strategies.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Affordable Youth-Centric Data Plans

- MNO Digital-Sub-Brand Convergence Strategies

- Multi-Country Licensing Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based cores generated 65.32% of the ASEAN MVNO market size in 2025 and will rise at an 8.83% CAGR to 2031 as virtual operators favor opex over capex and pursue rapid cross-border launches. Regulatory clarity under Vietnam's Decree 163/2024, which treats offshore clouds as registrable rather than licensable, further accelerates adoption. Cloud elasticity lowers onboarding costs for niche brands and empowers real-time analytics that optimize pricing, marketing, and fraud controls across the ASEAN MVNO market.

On-premise deployments persist in sectors where latency, redundancy, or data-residency rules override cost considerations. Financial institutions and public-safety agencies often demand private cores within domestic data centers. Hybrid variants blend cloud control with edge processing, leveraging 5G non-terrestrial-network gateways to extend coverage. Operators adopting this mix report smoother service continuity during fiber outages and a stronger appeal among industrial clients that value deterministic performance.

Reseller/light models still represent 60.85% of ASEAN MVNO market share because they require minimal infrastructure and yield fast commercialization. Yet their dependence on host operators curbs service customization. Full MVNOs, while capital-intensive, grow at 18.12% CAGR as firms seek routing autonomy, network-slicing capabilities, and direct interconnects that enable differentiated IoT and enterprise offerings. These players directly manage IMS cores, issuer provisioning servers, and wholesale procurement, culminating in higher average revenue per user.

Service-operator MVNOs occupy a midpoint, owning elements such as HLR/HSS but leaving radio-access control to MNOs. They appeal to e-commerce majors that value loyalty integration but shun deep telecom investment. The operational spectrum within the ASEAN MVNO market thus ranges from pure-branding ventures to vertically integrated challengers, each aligning architecture with target segment economics.

The ASEAN Mobile Virtual Network Operator (MVNO) Market Report is Segmented by Deployment Model (Cloud, On-Premise), Operational Mode (Service Operator, and More), Subscriber Type (Consumer, and More), Application (Discount, and More), Network Technology (2G/3G, and More), Distribution Channel (Online/Digital-only, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Circles.Life (Liberty Wireless Pte Ltd.)

- GOMO (Singtel Mobile Singapore Pte Ltd.)

- redONE Network Sdn Bhd

- Tune Talk Sdn Bhd

- Celcom Berhad

- XOX Mobile Sdn Bhd

- MyRepublic Limited

- Cherry Prepaid (Cosmic Technologies Inc.)

- Itel Mobile (Transsion Holdings)

- Wintel (Masan Group Corporation)

- Penguin Telecom (Advanced Wireless Network Co., Ltd.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising mobile-internet and smartphone penetration

- 4.2.2 Regulatory reforms on wholesale access

- 4.2.3 Demand for affordable youth-centric data plans

- 4.2.4 MNO digital-sub-brand convergence strategies

- 4.2.5 Cross-border eSIM tourism packs boom

- 4.2.6 IoT-focused enterprise MVNO uptake

- 4.3 Market Restraints

- 4.3.1 Limited wholesale pricing flexibility

- 4.3.2 Multi-country licensing complexity

- 4.3.3 Data-sovereignty concerns with cloud cores

- 4.3.4 5G-SA resource constraints on MVNO QoS

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Operational Mode

- 5.2.1 Reseller / Light / Brand MVNO

- 5.2.2 Service Operator

- 5.2.3 Full MVNO

- 5.3 By Subscriber Type

- 5.3.1 Consumer

- 5.3.2 Enterprise

- 5.3.3 IoT-specific

- 5.4 By Application

- 5.4.1 Discount

- 5.4.2 Business

- 5.4.3 Cellular M2M

- 5.4.4 Others

- 5.5 By Network Technology

- 5.5.1 2G/3G

- 5.5.2 4G/LTE

- 5.5.3 5G

- 5.5.4 Satellite/NTN

- 5.6 By Distribution Channel

- 5.6.1 Online/Digital-only

- 5.6.2 Traditional Retail Stores

- 5.6.3 Carrier Sub-brand Stores

- 5.6.4 Third-Party/Wholesale

- 5.7 By Country

- 5.7.1 Brunei

- 5.7.2 Cambodia

- 5.7.3 Indonesia

- 5.7.4 Laos

- 5.7.5 Malaysia

- 5.7.6 Myanmar

- 5.7.7 Philippines

- 5.7.8 Singapore

- 5.7.9 Thailand

- 5.7.10 Vietnam

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Circles.Life (Liberty Wireless Pte Ltd.)

- 6.4.2 GOMO (Singtel Mobile Singapore Pte Ltd.)

- 6.4.3 redONE Network Sdn Bhd

- 6.4.4 Tune Talk Sdn Bhd

- 6.4.5 Celcom Berhad

- 6.4.6 XOX Mobile Sdn Bhd

- 6.4.7 MyRepublic Limited

- 6.4.8 Cherry Prepaid (Cosmic Technologies Inc.)

- 6.4.9 Itel Mobile (Transsion Holdings)

- 6.4.10 Wintel (Masan Group Corporation)

- 6.4.11 Penguin Telecom (Advanced Wireless Network Co., Ltd.)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)