|

市场调查报告书

商品编码

1940744

亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Asia Pacific Mobile Virtual Network Operator (MVNO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

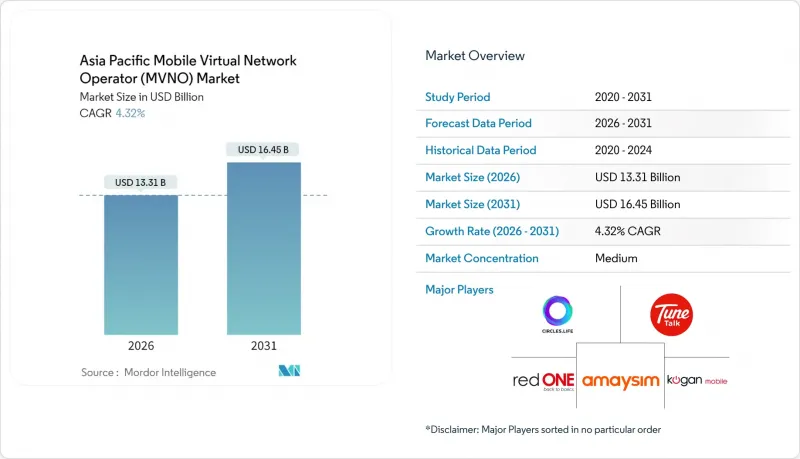

预计到 2026 年,亚太地区的行动虚拟网路营运商 (MVNO) 市场规模将达到 133.1 亿美元。

预计该产业规模将从 2025 年的 127.6 亿美元成长到 2031 年的 164.5 亿美元,2026 年至 2031 年的复合年增长率为 4.32%。

就用户数量而言,预计市场规模将从2025年的8367万增长到2030年的9954万,在预测期内(2025-2030年)的复合年增长率(CAGR)为3.54%。市场扩张的驱动力包括5G的积极部署、物联网(IoT)的日益普及以及监管机构主导的批发定价改革,这些改革降低了市场准入门槛,同时也加剧了竞争。云端原生营运模式、卫星整合和金融科技合作正成为提高成本效益和实现差异化的关键手段,使虚拟通讯业者)能够抓住传统行动网路营运商(MNO)难以获利的未开发消费市场和企业应用情境。网路切片服务的需求不断增长,尤其是在製造业、物流业和智慧城市计画中,进一步扩大了亚太地区MVNO市场的潜在客户群。同时,卫星/NTN技术的应用正在为以前无利可图的农村地区带来网路覆盖。儘管市场仍然分散,但将云端的可扩展性与超级应用的分发管道相结合的领先采用者已经降低了客户获取成本,并迫使现有企业在批发价格上做出妥协。

亚太地区行动虚拟网路营运商(MVNO)市场趋势与洞察

透过网路切片实现5G的快速部署和差异化

韩国、日本和中国都市区积极推动全国范围内的5G网路覆盖扩张,加上批发价格最高可达52%的降幅,为行动虚拟网路营运商(MVNO)提供了经济实惠的容量和尖端的网路切片功能。基于切片的服务等级协定(SLA)使虚拟业者能够为云端游戏、扩增实境(AR)购物和工业机器人等应用程式建立延迟保障层级。初步试点项目表明,与共用的尽力而为套餐相比,延迟降低了35-40毫秒,从而在不增加频谱成本的情况下实现了更高的每用户平均收入(ARPU)增长。透过将这些切片与企业级VPN捆绑销售,MVNO将自身定位为託管服务整合商,而非价格主导的经销商。区域互通性试验,例如中国移动国际与马来西亚合作伙伴进行的跨境切片测试,已经验证了切片「漫游」的可行性,并在依赖出口的製造业走廊中创造了差异化价值。

物联网连接的快速成长和以设备为中心的虚拟营运商 (MVNO) 模式

从日本的智慧工厂蓝图到中国重启的“中国製造2025”,亚洲的产业政策倡议正在催生海量的蜂窝M2M通信合同,而传统通讯业者由于收费结构分散和漫游费用僵化,难以充分满足这些合同的需求。像Soracom和1NCE这样的专业物联网行动虚拟网路营运商(MVNO)聚合了160多个国家/地区的多个IMSI设定文件,使原始设备製造商(OEM)能够交付预先连接设备。 API驱动的入口网站将配置前置作业时间缩短至几分钟,而全球统一费率套餐则消除了出口商的帐单衝击风险。随着NB-IoT RedCap和卫星NB-IoT技术的日益成熟,这些MVNO能够实现单张SIM卡上地面电波和非地面电波通讯的切换。儘管资料通讯量较低,但商业性成果已使每台设备的平均每用户收入(ARPU)达到消费级水平的两到三倍。

批发价持续高企

印度的定价环境竞争激烈,零售价格徘徊在每GB 0.01美元左右,但行动虚拟网路营运商(MVNO)的批发价格仍比此水平高出22-30%,几乎没有套利空间。此外,现有业者BSNL在虚拟品牌推广方面的能力有限,也限制了其市占率成长的潜力。类似的结构性失衡现像在马来西亚也普遍存在,尤其是在4G网路层面,因为Digital Nasional Berhad的5G服务并未包含在内。在菲律宾,MVNO面临不同频宽接入费用的差异。由此导致的利润空间压缩正在挤压行销预算,并将损益平衡点推迟五年以上。

细分市场分析

至2025年,云端部署将占据亚太地区行动虚拟网路营运商(MVNO)市场69.58%的份额,并在2031年之前以8.54%的复合年增长率成长。来自AWS或Azure的公共云端核心可将资本支出降低高达45%,并将上线时间从18个月缩短至不到6个月。这解释了为什么2024年后成立的七家MVNO中有五家采用了完整的SaaS架构。随着超大规模云端超大规模资料中心业者在印尼和泰国开设新的区域,支持满足资料主权要求的本地工作负载,亚太地区云端赋能MVNO市场的规模预计将进一步扩大。收入分成商业模式使营运商无需支付许可费,并允许他们将营运成本与用户成长相匹配。

在国家公共网路和工厂自动化等对低延迟要求极高的监管产业,本地部署解决方案仍然可行。日本的边缘微型资料中心託管着私有的 5G 核心网,并将传输路由到企业广域网,无需经过公共互联网,从而将延迟降低 10-15 毫秒。然而,本地部署和云端之间的界线正变得日益模糊,Kubernetes 打包技术在这些部署中得到了越来越广泛的应用。云端子版本、多重云端灾害復原、无伺服器收费和 API 市场将在预测期内推动大部分创新,进一步巩固云端的主导地位。

到2025年,转售商/轻型营运商将继续主导亚太地区的虚拟行动网路营运商(MVNO)市场,市占率将达到56.62%,而全功能MVNO预计将以18.88%的复合年增长率成长。全功能MVNO能够掌控核心网络,从而製定差异化的漫游策略并整合卫星通信,这对于以供应链为中心的企业至关重要。法国Lyca Mobile迁移到自有核心网路后,跨国语音利润率提高了22%,显示拥有讯号链路能够转化为可获利的业务能力。

服务提供者模式是一种折衷方案:客户支援和营运支援系统 (OSS) 由内部团队负责,而核心网路则依赖託管行动网路营运商 (MNO)。这种模式非常适合新兴市场,因为在这些市场,完整核心网路的监管费用仍然很高。然而,对 5G 切片、API 开放和多重云端编配日益增长的需求正促使雄心勃勃的品牌转向完全掌控网路。 MVNE 即服务平台降低了投资门槛,可将前期成本降低 55%。因此,随着企业在东协贸易走廊寻求客製化的服务等级协定 (SLA),预计到 2031 年,MVNO 的全面渗透率将达到 27.4% 的市场份额。

亚太地区行动虚拟网路营运商 (MVNO) 市场报告按部署模式(云端/本地部署)、营运模式(服务供应商/其他)、用户类型(消费者/其他)、应用领域(折扣/其他)、网路技术(2G/3G/其他)、分销管道(线上/纯数位/其他)和国家/地区进行细分。市场预测以价值(美元)和数量(用户数)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 透过网路切片实现5G的快速部署和服务差异化

- 物联网连接的激增将催生以设备为中心和以企业为中心的物联网虚拟网路营运商 (MVNO)。

- 智慧型手机普及率不断提高,以及纯数位消费者群体的增加。

- 非地面电波网路(NTN/HAPS)的出现将使在偏远地区的部署成为可能。

- 金融科技/超级应用程式透过捆绑行动方案来提高用户留存率

- 监管机构透过降低批发价格来降低进入门槛(例如韩国、澳洲)

- 市场限制

- 持续高涨的批发价格正在挤压虚拟业者的利润空间。

- 价格主导的竞争导致平均每用户收入(ARPU)极低,解约率极高。

- eSIM标准碎片化和API不相容增加了部署成本。

- 由于严格的SIM卡註册和资料本地化法律,合规负担加重。

- 价值链分析

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 对影响市场的宏观经济因素进行评估

第五章 市场规模与成长预测

- 按部署模式

- 云

- 本地部署

- 按操作模式

- 经销商/精简版/品牌虚拟营运商

- 服务提供者

- 完整的虚拟营运商

- 用户类型

- 对于消费者而言

- 企业

- 仅限物联网

- 透过使用

- 折扣

- 商业

- 细胞M2M

- 其他用途

- 透过网路技术

- 2G/3G

- 4G/LTE

- 5G

- 卫星通讯/NTN

- 透过分销管道

- 线上/数位独家

- 传统零售店

- 通讯业者子品牌商店

- 第三方/批发

- 按国家/地区

- 中国

- 印度

- 日本

- 越南

- 马来西亚

- 菲律宾

- 新加坡

- 韩国

- 亚太其他地区

第六章 竞争情势

- 2024年市场集中度

- 2023-2025年策略趋势

- 2024年市占率分析

- 公司简介

- Circles.Life(Liberty Wireless Pte Ltd)

- Rakuten Mobile, Inc.

- Amaysim Mobile Pty Ltd

- Kogan Mobile Operations Pty Ltd

- Tune Talk Sdn. Bhd.

- Red One Network Sdn. Bhd.

- GOMO(Singtel Mobile Singapore Pte Ltd)

- Lebara Group

- Lycamobile Limited

- 1NCE GmbH

- Soracom, Inc.

- Transatel(NTT Group)

- Ais Penguin SIM(Advanced Wireless Network Co., Ltd.(AWN))

- MyRepublic Group Limited

- iiJmio(Internet Initiative Japan Inc.(IIJ))

- U+Mobile(LG Uplus Corp.)

- KT M Mobile Corporation

- Skinny(Spark New Zealand Trading Limited)

- Smiles Connect(Digital Wallet Solutions Corporation)

- Eight Telecom Pte. Ltd.

第七章 市场机会与未来展望

Asia Pacific Mobile Virtual Network Operator (MVNO) Market size in 2026 is estimated at USD 13.31 billion, growing from 2025 value of USD 12.76 billion with 2031 projections showing USD 16.45 billion, growing at 4.32% CAGR over 2026-2031.

In terms of subscriber volume, the market is expected to grow from 83.67 million subscribers in 2025 to 99.54 million subscribers by 2030, at a CAGR of 3.54% during the forecast period (2025-2030). The market's expansion is propelled by aggressive 5G roll-outs, proliferating IoT deployments, and regulator-led wholesale tariff reforms that lower entry barriers while intensifying competition. Cloud-native operating models, satellite integration, and fintech tie-ups are now primary levers for cost efficiency and differentiation, enabling virtual operators to capture underserved consumer niches and enterprise use cases that traditional MNOs find hard to monetize. Intensifying demand for network-sliced services, especially in manufacturing, logistics, and smart-city programs, further widens the addressable pool for the Asia-Pacific MVNO market, while satellite/NTN technology adoption unlocks previously uneconomic rural coverage zones. Fragmentation persists, yet early movers that combine cloud scalability with super-app distribution channels are already compressing customer acquisition costs and pushing incumbents toward wholesale rate concessions.

Asia Pacific Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Rapid 5G Roll-Out and Network-Slicing Differentiation

Aggressive nationwide 5G coverage in South Korea, Japan, and urban China is arriving alongside wholesale rate reductions of up to 52%, arming MVNOs with both affordable capacity and cutting-edge network-slicing features. With slice-based SLAs, virtual operators are crafting latency-guaranteed tiers for cloud gaming, AR shopping, and industrial robotics. Early pilots indicate latency cuts of 35-40 ms versus shared best-effort plans, translating into premium ARPU uplift without incurring spectrum costs. Bundling these slices into enterprise VPNs is letting MVNOs position themselves as managed-service integrators rather than price-led resellers. Regional interoperability trials, such as China Mobile International's cross-border slice with Malaysian partners, show that slice "roaming" is achievable, creating differentiated value in export-heavy manufacturing corridors.

IoT Connection Boom and Device-Centric MVNO Models

Asia's industrial policy drives, from Japan's Smart Factory Roadmap to China's "Made in 2025" reboot, are spawning high-volume cellular M2M deals that conventional operators underserve because of fragmented billing and rigid roaming tariffs. Specialized IoT MVNOs such as Soracom and 1NCE aggregate multi-IMSI profiles across 160+ countries, enabling OEMs to ship pre-connected devices. Their API-driven portals cut provisioning lead times to minutes, and flat-rate global plans remove bill-shock risk for exporters. As NB-IoT RedCap and satellite NB-IoT mature, these MVNOs can toggle between terrestrial and non-terrestrial bearers from a single SIM. The commercial result is per-device ARPU that is 2-3 times consumer levels despite low data payloads.

Persistently High Wholesale Rates

India typifies a price war environment where retail tariffs hover near USD 0.01 per GB, yet MVNO wholesale offers remain 22-30% above that level, leaving no room for arbitrage . Additionally, incumbent BSNL's limited capacity to host virtual brands caps addressable share. Similar structural imbalances persist in Malaysia's 4G layers outside Digital Nasional Berhad's 5G scope, while Philippines MVNOs face differentiated access fees across spectrum bands. The resulting margin compression stifles marketing budgets and delays breakeven beyond the five-year mark.

Other drivers and restraints analyzed in the detailed report include:

- Rising Smartphone Penetration and Digital Onboarding

- Emergence of Non-Terrestrial Networks (NTN)

- Ultra-Low ARPU and High Churn

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud configurations retained 69.58% of the Asia-Pacific MVNO market share in 2025 and are tracking an 8.54% CAGR through 2031. Public-cloud cores from AWS and Azure lower capex by up to 45% while time-to-launch shrinks from 18 months to under six, explaining why 5 of 7 MVNOs launched since 2024 used a full SaaS stack. The Asia-Pacific MVNO market size for cloud deployments will widen further as hyperscalers open new zones in Indonesia and Thailand, enabling localized workloads that meet data-sovereignty mandates. Revenue-share commercial models free operators from license fees, aligning opex with subscriber ramp-up.

On-premise solutions remain relevant for regulated segments such as national public-safety networks and latency-critical factory automation. Edge-microdata centers in Japan host private 5G cores that export traffic to corporate WANs without traversing public Internet, shaving 10-15 ms latency. Yet even these deployments increasingly leverage Kubernetes packaging, blurring the line between on-premise and cloud. Over the forecast horizon, cloud sub-variants, multi-cloud disaster recovery, serverless billing, and API marketplaces will drive most innovation, reinforcing cloud's leadership.

Reseller/light constructs still dominate the Asia-Pacific MVNO market with a 56.62% share in 2025, but full MVNOs are projected to post a 18.88% CAGR. Control over core elements lets full MVNOs craft differentiated roaming policies and integrate satellite switching, critical for supply-chain-centric enterprises. Lycamobile's migration onto its own core in France yielded 22% cross-border voice margin expansion, evidence that ownership of signaling planes translates into monetizable features .

Service-operator formats provide a compromise: they assume customer care and OSS but rely on host-MNO cores. This suits emerging markets where regulatory fees on full cores remain onerous. However, the mounting need for 5G slices, API exposure, and multi-cloud orchestration is nudging ambitious brands toward full control. Investment hurdles are mitigated by MVNE-as-a-service platforms, cutting upfront spend by 55%. Consequently, full MVNO penetration is set to reach 27.4% volume share by 2031 as enterprises seek bespoke SLAs across ASEAN trade corridors.

The Asia Pacific Mobile Virtual Network Operator (MVNO) Market Report is Segmented by Deployment Model (Cloud, and On-Premise), Operational Mode (Service Operator, and More), Subscriber Type (Consumer, and More), Application (Discount, and More), Network Technology (2G/3G, and More), Distribution Channel (Online/Digital-only, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Circles.Life (Liberty Wireless Pte Ltd)

- Rakuten Mobile, Inc.

- Amaysim Mobile Pty Ltd

- Kogan Mobile Operations Pty Ltd

- Tune Talk Sdn. Bhd.

- Red One Network Sdn. Bhd.

- GOMO (Singtel Mobile Singapore Pte Ltd)

- Lebara Group

- Lycamobile Limited

- 1NCE GmbH

- Soracom, Inc.

- Transatel (NTT Group)

- Ais Penguin SIM (Advanced Wireless Network Co., Ltd. (AWN))

- MyRepublic Group Limited

- iiJmio (Internet Initiative Japan Inc. (IIJ))

- U+ Mobile (LG Uplus Corp.)

- KT M Mobile Corporation

- Skinny (Spark New Zealand Trading Limited)

- Smiles Connect (Digital Wallet Solutions Corporation)

- Eight Telecom Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G roll-out and network-slicing-enabled service differentiation

- 4.2.2 IoT connection boom spawning device-centric and enterprise IoT MVNOs

- 4.2.3 Rising smartphone penetration and digital-only consumer acquisition

- 4.2.4 Emergence of non-terrestrial networks (NTN/HAPS) opening remote-area play

- 4.2.5 Fintech / super-app bundling of mobile plans to deepen user stickiness

- 4.2.6 Regulator-mandated wholesale price cuts (e.g., KR, AU) lowering entry barriers

- 4.3 Market Restraints

- 4.3.1 Persistently high wholesale rates squeezing MVNO margins

- 4.3.2 Price-led rivalry driving ultra-low ARPU and high churn

- 4.3.3 Fragmented eSIM standards and API incompatibility inflating onboarding costs

- 4.3.4 Stringent SIM-registration and data-localization laws raising compliance burden

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Operational Mode

- 5.2.1 Reseller / Light / Brand MVNO

- 5.2.2 Service Operator

- 5.2.3 Full MVNO

- 5.3 By Subscriber Type

- 5.3.1 Consumer

- 5.3.2 Enterprise

- 5.3.3 IoT-specific

- 5.4 By Application

- 5.4.1 Discount

- 5.4.2 Business

- 5.4.3 Cellular M2M

- 5.4.4 Other Applications

- 5.5 By Network Technology

- 5.5.1 2G/3G

- 5.5.2 4G/LTE

- 5.5.3 5G

- 5.5.4 Satellite/NTN

- 5.6 By Distribution Channel

- 5.6.1 Online / Digital-only

- 5.6.2 Traditional Retail Stores

- 5.6.3 Carrier Sub-brand Stores

- 5.6.4 Third-Party/Wholesale

- 5.7 By Country

- 5.7.1 China

- 5.7.2 India

- 5.7.3 Japan

- 5.7.4 Vietnam

- 5.7.5 Malaysia

- 5.7.6 Philippines

- 5.7.7 Singapore

- 5.7.8 South Korea

- 5.7.9 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration, 2024

- 6.2 Strategic Moves, 2023-2025

- 6.3 Market Share Analysis, 2024

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Circles.Life (Liberty Wireless Pte Ltd)

- 6.4.2 Rakuten Mobile, Inc.

- 6.4.3 Amaysim Mobile Pty Ltd

- 6.4.4 Kogan Mobile Operations Pty Ltd

- 6.4.5 Tune Talk Sdn. Bhd.

- 6.4.6 Red One Network Sdn. Bhd.

- 6.4.7 GOMO (Singtel Mobile Singapore Pte Ltd)

- 6.4.8 Lebara Group

- 6.4.9 Lycamobile Limited

- 6.4.10 1NCE GmbH

- 6.4.11 Soracom, Inc.

- 6.4.12 Transatel (NTT Group)

- 6.4.13 Ais Penguin SIM (Advanced Wireless Network Co., Ltd. (AWN))

- 6.4.14 MyRepublic Group Limited

- 6.4.15 iiJmio (Internet Initiative Japan Inc. (IIJ))

- 6.4.16 U+ Mobile (LG Uplus Corp.)

- 6.4.17 KT M Mobile Corporation

- 6.4.18 Skinny (Spark New Zealand Trading Limited)

- 6.4.19 Smiles Connect (Digital Wallet Solutions Corporation)

- 6.4.20 Eight Telecom Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)