|

市场调查报告书

商品编码

1939164

英国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United Kingdom Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

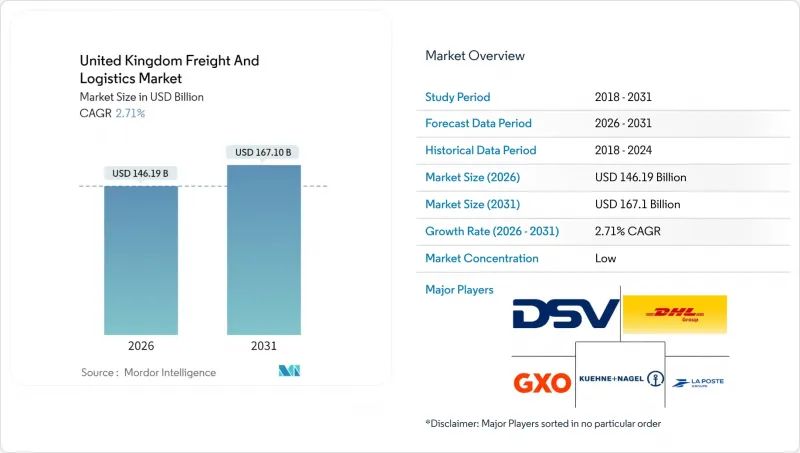

英国货运和物流市场预计将从 2025 年的 1,423.3 亿美元成长到 2026 年的 1,461.9 亿美元,到 2031 年达到 1,671 亿美元,2026 年至 2031 年的复合年增长率为 2.71%。

这一稳定成长的趋势反映出,该产业已发展成熟且适应性强,正围绕电子商务履约、製造业近岸外包和数位化清关进行转型。都市区小包裹密度的增加、仲介经纪流程的推进以及深水港基础设施建设的改善,都增强了货运量的增长势头;而驾驶员人口老龄化和地缘政治航运衝击则抑制了增长。公路、铁路、海运和空运等多种运输方式的平衡,使英国货运和物流市场保持稳健。然而,由于红海环岛运输成本上升以及锂电池的保险要求,高端航空货运的运输变得复杂。市场竞争依然温和,近期的大型收购案表明,市场正向规模优势、技术深度以及应对力等因素倾斜。

英国货运及物流市场趋势及洞察

电子商务復苏提升小包裹密度

2025年英国强劲的线上零售支出将推动每条配送路线的小包裹递送数量增加,从而降低配送成本,并改善当日达服务的经济效益。亚马逊退出实体杂货店业务,转而专注于宅配服务,凸显了其数位化优先的概念。 Co-op等快速零售业者目前服务于83%的家庭,而Gopuff与Morrisons的合作则将白天的门市容量重新用于「暗店」营运。大都会圈伦敦和曼彻斯特的高密度始发地-目的地丛集使微型仓配配送中心的产能每平方英尺提高了40-50%,从而推动了对都市区分拣机器人的进一步投资。这些高密度区域透过抵消劳动力和燃料通膨,并为替代燃料车辆建立规模基础,从而支持了英国的货运和物流市场。

製造业近岸外包促进了中程货运量的成长

供应商从欧洲大陆逐步回流英国的趋势正在国防采购、製药和精密工程领域加速发展。预计到2033年,西北和西米德兰兹地区丛集的产量将增加12%,从而带动工业园区和出口枢纽之间的中程货运需求。 BAE系统公司位于谢菲尔德的新建9.6万平方公尺的工厂正是这一转变的典型代表,69%的製造商计划提高其国内化率。稳定的订单流正在缓解干线运输的运转率,并支持英国货运和物流市场中各运输公司和铁路货运业者的运力投资。

驾驶员队伍老化和学徒招募率低

重型货车驾驶人的平均年龄超过55岁,而报名学徒的人数比实际需要的人数少约40%。 15%至20%的薪资成长以及严格的资格认证期限正促使运输公司试用自动驾驶车辆和灵活的轮班。温控货物和危险品运输的司机短缺尤为突出,加剧了英国货运和物流市场的营运风险。

细分市场分析

到2025年,製造业将占销售额的36.85%,主要得益于英格兰西北部和西南部製药和航太产业丛集。国内采购趋势(69%的生产商计划增加英国供应商)将支撑中程运输量的稳定性。 2026年至2031年间,批发和零售业的复合年增长率将达到2.97%,反映了电子商务生鲜食品和全通路能力的兴起。

随着快速商业网路向大伦敦以外地区扩展,预计到2031年,英国货运和物流在批发和零售市场的份额将增加2个百分点。公共部门基础设施建设为建筑物流提供了支持,而石油、天然气、采矿和采石业则正将重心转向离岸风力发电和氢气管道。 「其他」类别涵盖了可再生能源设备物流等新兴领域,有助于英国货运和物流市场需求的多元化。

到2025年,货运代理将占英国货运和物流市场收入的63.02%,这得益于港口、机场和米德兰兹物流枢纽之间的无缝连接。宅配、速递和小包裹服务预计将在2026年至2031年间以3.12%的复合年增长率成长,这主要受小包裹密度增加和自动分拣系统应用的推动。积极的行业整合正在模糊传统的行业界限,多家服务供应商将运输、仓储和仲介业务相结合,以赢得端到端的合约。

受24小时送达服务需求的推动,预计到2031年,英国宅配、快捷邮件和小包裹领域的货运和物流市场规模将达到241.8亿美元。仓储服务受惠于库存缓衝策略,而货运代理则围绕着海关自动化带来的经济效益。诸如计划货运代理和逆向物流等专业「其他服务」正在将可再生能源循环和循环供应链货币化,展现出抵御宏观经济波动的能力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 人口统计数据

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 通货膨胀

- 经济表现及概况

- 电子商务产业的趋势

- 製造业趋势

- 运输和仓储业的GDP

- 出口趋势

- 进口趋势

- 燃油价格

- 卡车运输营运成本

- 卡车运输车队规模(按类型)

- 主要卡车供应商

- 物流绩效

- 按交通方式分享

- 海运船队运力

- 班轮运输连接

- 停靠港口和演出

- 货运费率趋势

- 货物吨位趋势

- 基础设施

- 法规结构(公路和铁路)

- 法规结构(海事和航空)

- 价值炼和通路分析

- 市场驱动因素

- 电子商务復苏提升小包裹密度

- 製造业近岸外包促进了中程航运量的成长

- 海关流程自动化加快了数位货运速度

- 线上杂货和当日送达服务的成长扩大了都市区微型仓配

- 来自可再生能源计划的货物运输量迅速成长

- 利用人工智慧优化扩大低温运输产能

- 市场限制

- 驾驶员队伍老化和学徒招募率低

- 西海岸港口疏浚工程延误导致陆路运输路线紧张

- 绕道红海会推高运往英国的进口运费。

- 锂电池保险价格上涨抑制了航空货运需求。

- 市场创新

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 终端用户产业

- 农业、渔业、林业

- 建设业

- 製造业

- 石油天然气、采矿和采石

- 批发和零售

- 其他的

- 物流职能

- 快递、快捷邮件和小包裹(CEP)

- 目的地

- 国内的

- 国际的

- 目的地

- 货运代理

- 透过交通工具

- 航空

- 海路和内河航道

- 其他的

- 透过交通工具

- 货物运输

- 透过交通工具

- 航空

- 管道

- 铁路

- 路

- 海路和内河航道

- 透过交通工具

- 仓储

- 透过温度控制

- 非温控型

- 温度控制

- 透过温度控制

- 其他服务

- 快递、快捷邮件和小包裹(CEP)

第六章 竞争情势

- 市场集中度

- 关键策略倡议

- 市占率分析

- 公司简介

- Advanced Supply Chain Group

- Americold(Including Americold Whitchurch)

- Ballyvesey Holdings, Ltd.(Including Montgomery Transport)

- CMA CGM Group(Including CEVA Logistics)

- Culina Group

- DACHSER

- Delamode Group(Formerly Xpediator PLC)

- DHL Group

- DP World(Including P&O Ferrymasters)

- DSV A/S(Including DB Schenker)

- Europa Worldwide Group

- Expeditors International of Washington, Inc.

- FedEx

- GBA Logistics

- Gregory Group

- GXO Logistics, Inc.(Including Wincanton PLC)

- Hellmann Worldwide Logistics

- Hoyer Group(Including Hoyer UK Ltd)

- Huboo

- Kinaxia Logistics Limited(Including Mark Thompson Transport)

- Kuehne+Nagel

- La Poste Group(Including DPD Group, and CitySprint(UK)Ltd.)

- Lineage, Inc.

- Maritime Group Ltd.

- Meachers Global Logistics

- Otto Group(Including Evri Limited)

- Owens Group

- Pall-Ex Group

- PD Ports(Owned by Brookfield Asset Management)

- Peel Ports Group

- Rhenus Group

- Samskip

- SITRA Group(Including Abbey Logistics Group)

- Solstor UK, Ltd.

- Swain Group

- Turners(Soham)Ltd.

- United Parcel Service of America, Inc.(UPS)(Including Coyote Logistics)

- WH Malcolm, Ltd.

- Walden Group(Including Moviantio)

- Whistl UK Ltd.

- XPO, Inc.

第七章 市场机会与未来展望

The United Kingdom freight and logistics market is expected to grow from USD 142.33 billion in 2025 to USD 146.19 billion in 2026 and is forecast to reach USD 167.1 billion by 2031 at 2.71% CAGR over 2026-2031.

This steady trajectory reflects a mature yet adaptive sector that is reshaping itself around e-commerce fulfillment, manufacturing near-shoring, and digital customs processing. Parcel density gains in urban areas, automation of broker workflows, and infrastructure commitments at deep-sea ports are reinforcing throughput momentum, while an aging driver pool and geopolitical shipping shocks temper the growth curve. Balance across road, rail, sea, and air modes keeps the United Kingdom freight and logistics market resilient, even as Red Sea re-routing inflates inbound costs and lithium-battery insurance requirements complicate premium air cargo flows. Competitive intensity remains moderate, with recent blockbuster acquisitions indicating a shift toward scale, technology depth, and environmental compliance advantages.

United Kingdom Freight And Logistics Market Trends and Insights

E-Commerce Rebound Boosts Parcel Density

Robust U.K. online retail spending in 2025 is lifting parcel stops per route, which lowers per-delivery cost and improves same-day service economics. Amazon's exit from brick-and-mortar grocery and renewed focus on home delivery underline a digital-first mindset. Quick-commerce operators such as Co-op now reach 83% of households, while Gopuff's partnership with Morrisons repurposes daytime store capacity to dark-store operations. Dense origin-destination clusters in Greater London and Manchester have seen micro-fulfillment throughput rise 40-50% per square foot, encouraging further investment in urban sortation robotics. These density gains sustain the United Kingdom freight and logistics market by offsetting labor and fuel inflation and by anchoring scale for alternative-fuel fleets.

Manufacturing Near-Shoring Lifts Mid-Haul Volumes

Defense procurement, pharmaceuticals, and precision engineering are fueling a gradual relocation of supplier footprints from continental Europe back to the United Kingdom. Output from regional clusters in the North West and West Midlands is projected to rise 12% by 2033, adding mid-haul freight demand between industrial parks and export gateways. BAE Systems' new 96,000-square-foot facility in Sheffield exemplifies the shift, while 69% of manufacturers plan to deepen domestic sourcing. Consistent order flows smooth utilization on trunk routes, underpinning capacity investments by hauliers and rail-freight operators across the United Kingdom freight and logistics market.

Driver Workforce Ageing and Low Apprentice Intake

The median age of heavy-goods-vehicle operators has climbed past 55, while apprenticeship enrollments lag replacements by roughly 40%. Rising wage bills of 15-20% and tight certification windows push carriers toward autonomous-vehicle pilots and flexible shift scheduling. Scarcity is most pronounced in temperature-controlled and hazardous-materials niches, elevating operating risk across the United Kingdom freight and logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Customs-Broker Automation Accelerates Digital Forwarding

- Growth in Online Grocery and Same-Day Delivery Scales Urban Micro-Fulfillment

- West-Coast Port Dredge Delays Strain Road Corridors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 36.85% of turnover in 2025, benefitting from pharmaceutical and aerospace clusters in the North West and South West. Domestic sourcing trends, with 69% of producers planning to add U.K. suppliers, anchor steady mid-haul volumes. Wholesale and Retail Trade, expanding at a 2.97% CAGR (2026-2031), reflects grocery e-commerce diffusion and omnichannel fulfillment.

The United Kingdom freight and logistics market share for Wholesale and Retail Trade is set to climb by 2 percentage points by 2031 as quick-commerce networks extend beyond London. Construction logistics ride public-sector infrastructure programs, while Oil, Gas, Mining, and Quarrying pivot to offshore wind and hydrogen pipelines. The "Others" bucket covers nascent verticals such as renewable-equipment logistics, reinforcing demand diversification across the United Kingdom freight and logistics market.

Freight Transport owned 63.02% of 2025 revenue in the United Kingdom freight and logistics market, leveraging seamless connectivity between ports, airports, and Midlands distribution hubs. Courier, Express, and Parcel services enjoy a 3.12% CAGR (2026-2031) on the back of higher parcel density and autonomous sortation rollouts. Active consolidation blurs traditional silos, with multi-service providers bundling transport, warehousing, and brokerage to win end-to-end contracts.

The United Kingdom freight and logistics market size for the Courier, Express, and Parcel segment is projected to reach USD 24.18 billion by 2031, supported by 24-hour delivery expectations. Warehousing and Storage gains from inventory-buffer strategies, while Freight Forwarding pivots on customs-automation economies. Specialized "Other Services", such as project cargo and reverse logistics, monetise the renewable-energy cycle and circular supply chains, showing resilience against macro-volatility.

The United Kingdom Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel, Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Advanced Supply Chain Group

- Americold (Including Americold Whitchurch)

- Ballyvesey Holdings, Ltd. (Including Montgomery Transport)

- CMA CGM Group (Including CEVA Logistics)

- Culina Group

- DACHSER

- Delamode Group (Formerly Xpediator PLC)

- DHL Group

- DP World (Including P&O Ferrymasters)

- DSV A/S (Including DB Schenker)

- Europa Worldwide Group

- Expeditors International of Washington, Inc.

- FedEx

- GBA Logistics

- Gregory Group

- GXO Logistics, Inc. (Including Wincanton PLC)

- Hellmann Worldwide Logistics

- Hoyer Group (Including Hoyer UK Ltd)

- Huboo

- Kinaxia Logistics Limited (Including Mark Thompson Transport)

- Kuehne+Nagel

- La Poste Group (Including DPD Group, and CitySprint (UK) Ltd.)

- Lineage, Inc.

- Maritime Group Ltd.

- Meachers Global Logistics

- Otto Group (Including Evri Limited)

- Owens Group

- Pall-Ex Group

- PD Ports (Owned by Brookfield Asset Management)

- Peel Ports Group

- Rhenus Group

- Samskip

- SITRA Group (Including Abbey Logistics Group)

- Solstor UK, Ltd.

- Swain Group

- Turners (Soham) Ltd.

- United Parcel Service of America, Inc. (UPS) (Including Coyote Logistics)

- W H Malcolm, Ltd.

- Walden Group (Including Moviantio)

- Whistl UK Ltd.

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.23 Regulatory Framework (Sea and Air)

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Rebound Boosts Parcel Density

- 4.25.2 Manufacturing Near-Shoring Lifts Mid-Haul Volumes

- 4.25.3 Customs-Broker Automation Accelerates Digital Forwarding

- 4.25.4 Growth in Online Grocery and Same-Day Delivery Scales Urban Micro-Fulfilment

- 4.25.5 Renewable-Energy Project-Cargo Surge

- 4.25.6 AI-Optimized Cold-Chain Capacity Gains

- 4.26 Market Restraints

- 4.26.1 Driver Workforce Ageing and Low Apprentice Intake

- 4.26.2 West-Coast Port Dredge Delays Strain Road Corridors

- 4.26.3 Red Sea Re-Routing Inflates UK Import Freight Rates

- 4.26.4 Lithium-Battery Insurance Hikes Curb Air-Freight Demand

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Buyers

- 4.28.3 Bargaining Power of Suppliers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Advanced Supply Chain Group

- 6.4.2 Americold (Including Americold Whitchurch)

- 6.4.3 Ballyvesey Holdings, Ltd. (Including Montgomery Transport)

- 6.4.4 CMA CGM Group (Including CEVA Logistics)

- 6.4.5 Culina Group

- 6.4.6 DACHSER

- 6.4.7 Delamode Group (Formerly Xpediator PLC)

- 6.4.8 DHL Group

- 6.4.9 DP World (Including P&O Ferrymasters)

- 6.4.10 DSV A/S (Including DB Schenker)

- 6.4.11 Europa Worldwide Group

- 6.4.12 Expeditors International of Washington, Inc.

- 6.4.13 FedEx

- 6.4.14 GBA Logistics

- 6.4.15 Gregory Group

- 6.4.16 GXO Logistics, Inc. (Including Wincanton PLC)

- 6.4.17 Hellmann Worldwide Logistics

- 6.4.18 Hoyer Group (Including Hoyer UK Ltd)

- 6.4.19 Huboo

- 6.4.20 Kinaxia Logistics Limited (Including Mark Thompson Transport)

- 6.4.21 Kuehne+Nagel

- 6.4.22 La Poste Group (Including DPD Group, and CitySprint (UK) Ltd.)

- 6.4.23 Lineage, Inc.

- 6.4.24 Maritime Group Ltd.

- 6.4.25 Meachers Global Logistics

- 6.4.26 Otto Group (Including Evri Limited)

- 6.4.27 Owens Group

- 6.4.28 Pall-Ex Group

- 6.4.29 PD Ports (Owned by Brookfield Asset Management)

- 6.4.30 Peel Ports Group

- 6.4.31 Rhenus Group

- 6.4.32 Samskip

- 6.4.33 SITRA Group (Including Abbey Logistics Group)

- 6.4.34 Solstor UK, Ltd.

- 6.4.35 Swain Group

- 6.4.36 Turners (Soham) Ltd.

- 6.4.37 United Parcel Service of America, Inc. (UPS) (Including Coyote Logistics)

- 6.4.38 W H Malcolm, Ltd.

- 6.4.39 Walden Group (Including Moviantio)

- 6.4.40 Whistl UK Ltd.

- 6.4.41 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告 货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分

货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分 2026-2030年全球货物审核与支付市场

2026-2030年全球货物审核与支付市场 东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)南美货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)南美货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)