|

市场调查报告书

商品编码

1939568

南美货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)South America Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

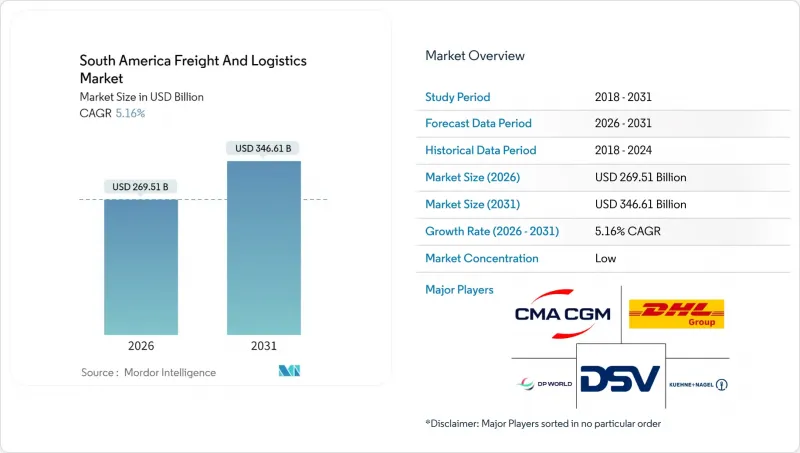

2025年南美货运和物流市场价值为2,562.9亿美元,预计到2031年将达到3,466.1亿美元,高于2026年的2,695.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.16%。

这一扩张反映了该地区作为近岸外包目的地的吸引力、持续的基础设施现代化以及数位化供应链解决方案的快速普及。巴西凭藉其多元化的工业基础和港口网络保持着规模经济优势,而由中国支持的秘鲁昌凯超级港预计将分流太平洋贸易流,并刺激内陆货运量。电子商务的成长正在重塑对小包裹密集型网路的需求,而技术赋能的供应商可以提供灵活高效的「最后一公里」配送服务。然而,与气候相关的河流水位波动、长期存在的道路拥堵以及复杂的跨境法规正在限制该行业的成长潜力。

南美洲货运与物流市场趋势及洞察

电子商务和最后一公里需求的快速成长

巴西、阿根廷和智利等大都会圈数位化零售的快速普及,正推动网路设计朝着以小包裹为中心的物流模式转变,这需要密集的微型仓配中心网路。 Mercado Libre计划在2025年底将其在巴西的配送中心数量从10个增加到21个,以支持其当日达和次日达的承诺。不断增长的消费者期望正在推动对都市区分拣中心和低温运输微型仓库的投资,这些设施能够实现生鲜食品和药品两小时送达。小型包裹的出现降低了传统零担货运的装载率,同时也为限时送达服务提供了更高的定价空间。三大经济体之间的跨境电子商务正在推动国际小包裹货运量的成长,给传统的海关程序带来压力,并刺激了对技术赋能的清关服务的需求。

近岸外包主导製造地迁移

为降低供应链风险,汽车和电子产品製造商正将生产从亚太地区转移到南美,从而形成零件和成品的双向流动。巴西的工业园区吸引着寻求南方共同市场(Mercosur)内优惠关税待遇的供应商,而墨西哥日益增强的竞争力也给南美国家带来了更大的压力,迫使它们精简物流成本。能够整合多式联运和合规安排的营运商将有机会占据市场主导地位。由于设施位置取决于基础设施质量,因此投资于靠近製造区的保税仓库的物流公司能够创造强大的价值提案。

长期存在的公路和铁路瓶颈

巴西-桑托斯走廊、阿根廷-罗萨里奥粮食走廊和智利铜矿石走廊的运力限制导致货物滞留时间过长,旺季期间每个货柜的滞期费超过200美元。老旧的单线铁路和过时的号誌系统阻碍了模式转换,而这种转变本来可以缓解公路拥塞。资金短缺导致双线铁路和改良型多式联运码头的建设进程延缓。拥有专属运力的现有企业维持定价权,而依赖现有网路的新兴企业则难以扩大规模。

细分市场分析

到2025年,製造业将占南美洲货运和物流市场规模的34.68%,其中巴西的汽车和电子产品丛集是核心。生产商优先选择靠近港口的位置,以最大限度地减少内陆运输的复杂性。受都市区购买力提升推动消费主导物流扩张的限制,预计2026年至2031年批发和零售业将以5.42%的复合年增长率成长。零售商正在将交叉转运能力融入区域配送中心,以整合到货并对小包裹进行分拣,从而实现最后一公里配送。

农业部门在收穫季节仍将保持其结构性重要地位,但低温运输出口的监管复杂性使其利润率高于散装粮食运输。石油和天然气货物运输增速放缓但货运量保持稳定,为专业槽式货柜营运商提供了支撑。建筑材料运输需求与基础设施投资激增密切相关,这有利于拥有灵活运输合约的承运商。零售补货和製造业供应链的整合为在供应链各个环节重复利用资产的综合供应商创造了机会。

到2025年,货运代理将成为最大的收入驱动力,占南美货运和物流市场规模的61.37%。商品出口、进口补给和工业供应链支撑着散货和货柜货物的持续流动。受电子商务和都市区当日达需求成长的推动,宅配业务(CEP)预计将在2026年至2031年间以5.73%的复合年增长率成长。随着轻资产、小包裹递送平台不断扩大其覆盖范围,传统卡车运输业者在南美货运和物流市场的份额将会下降。整合货运代理和温控仓储服务的营运商透过为高成长的农产品出口商提供合规包装服务,正在获得价格优势。

技术应用也在重塑价值结构。货运匹配应用程式提高了卡车运转率,并使小规模车队能够参与传统的个人货运网路。货运代理业务仍然很重要,因为它们需要应对欧盟碳排放调节机制和森林砍伐预防认证,而这些措施增加了文件负担。 Expeditors 2024 年第三季在拉丁美洲的营收成长了 31%,这凸显了市场对合规驱动型货运代理服务的高端需求。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第3章执行摘要

第四章 市场情势

- 市场概览

- 人口统计数据

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 通货膨胀

- 経済パフォーマンスと概要

- 电子商务产业的趋势

- 製造业の动向

- 运输和仓储业的GDP

- 出口趋势

- 进口趋势

- 燃油价格

- トラック输送の运営コスト

- 卡车运输车队规模(按类型)

- 主要トラック供给业者

- 物流绩效

- 输送モード别シェア

- 海上输送船队の积载能力

- 班轮运输连接

- 寄港地とパフォーマンス

- 货物运赁の动向

- 货物输送量の动向

- 基础设施

- 法规结构(公路和铁路)

- 阿根廷

- 巴西

- 智利

- 秘鲁

- 法规结构(海事和航空)

- 阿根廷

- 巴西

- 智利

- 秘鲁

- 价值炼和通路分析

- 市场驱动因素

- 电子商务和最后一公里需求的快速成长

- 近岸外包主导製造地迁移

- 港口和走廊基础设施开发

- 利用数位货运平台提高整车运输价格

- 为高附加价值农产品出口提供低温运输支持

- 透过区域自由贸易协定深化关税同盟

- 市场限制

- 长期存在的公路和铁路瓶颈

- 高昂的物流税费和通行费

- 南方共同市场区域内跨境监管的片段化

- 气候变迁造成的破坏(洪水、干旱)

- 市场创新

- ポーターの五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- エンドユーザー产业

- 农业、渔业、林业

- 建造

- 製造业

- 石油天然气、采矿和采石

- 批发和零售

- 其他的

- 物流职能

- 宅配、速递和小包裹(CEP)

- 目的地タイプ别

- 国内的

- 国际的

- 目的地タイプ别

- 货运代理

- 透过交通工具

- 航空

- 海上・内陆水路

- 其他的

- 透过交通工具

- 货物运输

- 透过交通工具

- 航空

- 管道

- 铁路

- 路

- 海上・内陆水路

- 透过交通工具

- 仓储和存储

- 温度管理别

- 非温度管理

- 温度控制

- 温度管理别

- 其他服务

- 宅配、速递和小包裹(CEP)

- 国家

- 阿根廷

- 巴西

- 智利

- 秘鲁

- 南美洲其他地区

第6章 竞合情势

- 市场集中度

- 主要な戦略的动きs

- 市占率分析

- 公司简介

- Agencias Universales SA(AGUNSA)

- Alonso Group

- Americold

- CMA CGM Group(Including CEVA Logistics)

- Correios

- DHL Group

- DP World

- DSV A/S(Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx Corp.

- Kuehne+Nagel

- Log-In Logistica Integrada

- MercadoLibre, Inc.

- Rappi Logistics

- Romeu

- Rumo Logistica

- SAAM

- Scan Global Logistics(Including Blu Logistics)

- TASA Logistica

- United Parcel Service of America, Inc.(UPS)

第七章 市场机会与未来展望

The South America freight and logistics market was valued at USD 256.29 billion in 2025 and estimated to grow from USD 269.51 billion in 2026 to reach USD 346.61 billion by 2031, at a CAGR of 5.16% during the forecast period (2026-2031).

The expansion reflects the region's appeal as a nearshoring destination, continued infrastructure modernization, and rapid adoption of digital supply-chain solutions. Brazil retains scale benefits through its diversified industrial base and port network, while Peru's China-backed Chancay megaport is set to redirect Pacific trade flows and stimulate hinterland freight volumes. E-commerce growth is reshaping demand toward parcel-intensive networks that reward technology-enabled providers with agile last-mile capabilities. At the same time, climate-driven river level volatility, chronic road bottlenecks, and complex cross-border regulation temper the sector's growth potential.

South America Freight And Logistics Market Trends and Insights

E-Commerce Boom and Last-Mile Demand

Rapid digital retail adoption across metropolitan Brazil, Argentina, and Chile is transforming network design toward parcel-heavy flows that require dense micro-fulfillment footprints. Mercado Libre plans to raise its Brazilian distribution center count from 10 to 21 by end-2025 to support same-day and next-day delivery commitments. Heightened consumer expectations are pulling investment into urban sortation hubs and cold-chain micro-depots capable of meeting two-hour delivery windows for fresh groceries and pharmaceuticals. Parcel fragmentation pushes load factors down for traditional LTL yet enables premium pricing for time-definite services. Cross-border e-commerce among the three largest economies is adding international parcel volumes that test legacy customs procedures and stimulate demand for tech-enabled brokerage.

Nearshoring-Led Manufacturing Relocation

Supply-chain de-risking motivates automotive and electronics producers to relocate capacity from Asia-Pacific toward South America, generating bidirectional freight flows of components and finished goods. Brazil's industrial clusters attract suppliers seeking tariff advantages within MERCOSUR, while Mexico's competitiveness raises pressure on southern neighbors to streamline logistics costs. Integrated providers that can orchestrate multimodal moves and regulatory compliance stand to capture disproportionate share. Facility siting decisions hinge on infrastructure quality; therefore, logistics firms that invest in bonded warehousing close to manufacturing zones create compelling value propositions.

Chronic Road and Rail Bottlenecks

Capacity limitations in Brazil's Santos corridor, Argentina's Rosario grain routes, and Chile's copper corridors translate into prolonged dwell times and demurrage costs exceeding USD 200 per container during peak seasons. Legacy single-track rail and outdated signaling hamper modal shifts that could relieve road congestion. Funding gaps slow double-tracking and intermodal terminal upgrades. Incumbent providers with dedicated capacity maintain pricing power, while start-ups reliant on fluid networks struggle to scale.

Other drivers and restraints analyzed in the detailed report include:

- Port and Corridor Infrastructure Upgrades

- Digital Freight Platforms Improving Truck Load Factors

- High Logistics Taxes and Tolls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 34.68% of the South America freight and logistics market size in 2025, anchored by Brazil's autos and electronics clusters. Producers favor near-port locations to minimize inland drayage complexity. Wholesale and retail trade is projected for a 5.42% CAGR (2026-2031)as rising urban purchasing power fuels consumption-driven logistics. Retailers deploy regional distribution centers with embedded cross-dock functions that consolidate inbound freight and stage parcels for last-mile delivery.

Agriculture remains structurally significant during harvest cycles, yet compliance-heavy cold-chain exports provide higher margins than bulk grain shipments. Oil and gas cargoes display lower growth but stable volumes that support specialized tank container operators. Construction freight demand tracks infrastructure spending surges, rewarding carriers with flexible capacity contracts. Convergence of retail replenishment and manufacturing inputs creates opportunities for integrated providers that reuse assets across supply-chain stages.

Freight transport contributed the largest revenue slice, equal to 61.37% of the South America freight and logistics market size in 2025. Commodity exports, import replenishment, and industrial resupply underpin sustained bulk and container flows. CEP activities are forecast for a 5.73% CAGR (2026-2031), catalyzed by urban e-commerce and same-day delivery commitments. The South America freight and logistics market share held by legacy truckload carriers will trend lower as asset-light parcel platforms widen service reach. Providers integrating freight forwarding with temp-controlled warehousing gain pricing leverage by bundling compliance services for high-growth agrifood exporters.

Technology adoption also reshapes value pools. Load-matching applications increase truck utilization, allowing small fleets to penetrate formerly relationship-based freight networks. Freight forwarding retains relevance by navigating EU carbon adjustment mechanisms and deforestation certifications that increase documentary burden. Expeditors' 31% Latin American revenue jump in Q3 2024 illustrates the premium demand for compliance-centric forwarding.

The South America Freight and Logistics Market Report is Segmented by Logistics Function (Courier, Express, and Parcel, Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Wholesale and Retail Trade, Others), and Geography (Chile, Argentina, and Brazil). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Agencias Universales SA (AGUNSA)

- Alonso Group

- Americold

- CMA CGM Group (Including CEVA Logistics)

- Correios

- DHL Group

- DP World

- DSV A/S (Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx Corp.

- Kuehne+Nagel

- Log-In Logistica Integrada

- MercadoLibre, Inc.

- Rappi Logistics

- Romeu

- Rumo Logistica

- SAAM

- Scan Global Logistics (Including Blu Logistics)

- TASA Logistica

- United Parcel Service of America, Inc. (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.22.1 Argentina

- 4.22.2 Brazil

- 4.22.3 Chile

- 4.22.4 Peru

- 4.23 Regulatory Framework (Sea and Air)

- 4.23.1 Argentina

- 4.23.2 Brazil

- 4.23.3 Chile

- 4.23.4 Peru

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Boom and Last-Mile Demand

- 4.25.2 Nearshoring-Led Manufacturing Relocation

- 4.25.3 Port and Corridor Infrastructure Upgrades

- 4.25.4 Digital Freight Platforms Improving Truck Load Factors

- 4.25.5 Cold-Chain Compliance for High-Value Agrifood Exports

- 4.25.6 Regional Free-Trade Agreements Deepening Customs Union

- 4.26 Market Restraints

- 4.26.1 Chronic Road and Rail Bottlenecks

- 4.26.2 High Logistics Taxes and Tolls

- 4.26.3 Mercosur Cross-Border Regulatory Fragmentation

- 4.26.4 Climate-Driven Disruption (Floods, Droughts)

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Suppliers

- 4.28.3 Bargaining Power of Buyers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Peru

- 5.3.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Agencias Universales SA (AGUNSA)

- 6.4.2 Alonso Group

- 6.4.3 Americold

- 6.4.4 CMA CGM Group (Including CEVA Logistics)

- 6.4.5 Correios

- 6.4.6 DHL Group

- 6.4.7 DP World

- 6.4.8 DSV A/S (Including DB Schenker)

- 6.4.9 Expeditors International of Washington, Inc.

- 6.4.10 FedEx Corp.

- 6.4.11 Kuehne+Nagel

- 6.4.12 Log-In Logistica Integrada

- 6.4.13 MercadoLibre, Inc.

- 6.4.14 Rappi Logistics

- 6.4.15 Romeu

- 6.4.16 Rumo Logistica

- 6.4.17 SAAM

- 6.4.18 Scan Global Logistics (Including Blu Logistics)

- 6.4.19 TASA Logistica

- 6.4.20 United Parcel Service of America, Inc. (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告 货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分

货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分 2026-2030年全球货物审核与支付市场

2026-2030年全球货物审核与支付市场 东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国货运和物流:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国货运和物流:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)