|

市场调查报告书

商品编码

1939594

越南货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vietnam Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

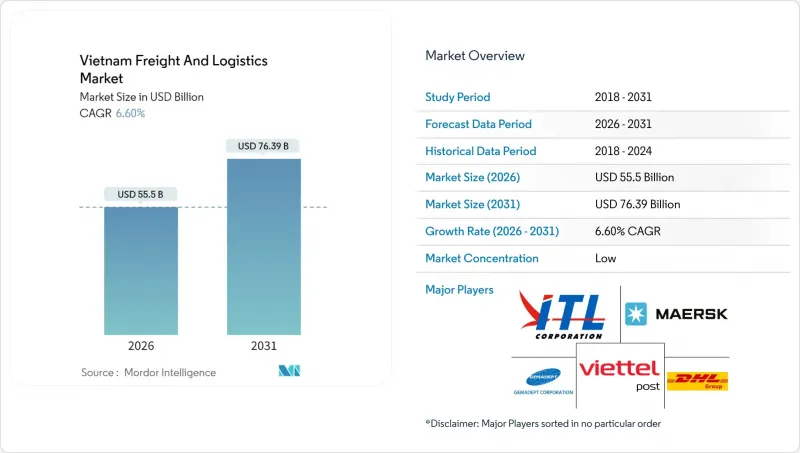

预计越南货运和物流市场规模将从 2025 年的 520.6 亿美元成长到 2026 年的 555 亿美元,到 2031 年将达到 763.9 亿美元,2026 年至 2031 年的复合年增长率为 6.6%。

这一成长轨迹反映了製造业的持续涌入、电子商务小包裹的成长以及150亿美元的公共投资,这些投资用于道路、港口和机场建设。结构性利多因素包括来自中国的近岸外包、东协单一窗口海关清关的数位化以及对温控运输需求的成长,这些因素推动了陆运、海运和空运走廊货运量的成长。随着国际一体化企业加强在越南的业务布局,以及国内业者透过低温运输和最后一公里投资扩大规模,竞争日益激烈。因此,越南的货运和物流市场正受惠于基础建设、贸易自由化和数位转型带来的良性循环,这缩短了货物停留时间并开拓了新的服务领域。

越南货运及物流市场趋势及展望

电子商务小包裹热潮推动最后一公里配送创新

预计到2024年,随着线上市场的扩张和社交电商带来的地理限制的放宽,越南国内小包裹量将成长45%。在越南的货运和物流市场,宅配网路正在采用自动化分类机和人工智慧路线规划引擎,将平均递送时间从48小时缩短至24小时。然而,由于最后一公里网路的碎片化,越南的小包裹递送成本比泰国高出28%,这促使营运商透过微型枢纽共用和众包司机的方式将服务扩展到农村地区。监理支持也在推动经济发展。价值低于200美元的小包裹清关程序已简化,海关滞留时间从5天缩短至1天。资本正顺应需求,ViettelPost开设了15个机器人分类中心,Giao Hang Nhanh承诺在2025年实现乡级覆盖。这些措施将加强数位化基础,加速未来包裹量的成长,并巩固CEP(宅配)作为越南货运和物流市场成长最快细分市场的地位。

近岸外包正在改变製造业物流

随着电子和服装产业从中国转移,预计到2024年,越南製造业物流需求将增加28%,全球品牌纷纷寻求对冲地缘政治和成本风险。在北部丛集,高附加价值电子产品的分销优先依赖空运,内排机场的零件吞吐量年增35%。这导致运力增加和航班时刻重新分配。光是三星的扩张就需要每月2,400个标准箱的货运量,富士康和立讯精密也分别运作通往出口门户的闭合迴路通道。服装製造商正在利用海陆联运,将前置作业时间缩短至比传统中国路线缩短40%。提供套件组装、退货处理和品管仓储服务的营运商如今获得了更高的利润,这标誌着越南货运和物流市场正从纯粹的运输模式转向综合合约物流模式。

货柜短缺造成成本压力

由于越南的进出口比例为3:1,大量空货柜滞留在内陆,导致平均搬迁成本上升,20英尺货柜为85美元,40英尺货柜为170美元。 2024年,在咖啡和纺织品旺季,货柜运转率降至70%以下,导致货柜不平衡附加费上涨25%。货运代理商正利用物联网追踪标籤和共用池来提高运转率,并将单次运输成本降低15-20%,但结构性的贸易失衡使得短途运输附加费短期内不太可能降低。这导致越南货运和物流市场波动,挤压了中小托运人的利润空间。

细分市场分析

到2025年,製造业将占越南货运和物流市场份额的35.12%,这主要得益于电子产品和服饰中心对与海外买家精准库存同步的需求。严格的週期要求推动了RFID技术在零件配套和延迟仓储方面的应用,从而提高了第三方物流(3PL)的渗透率。批发和零售业正在迎头赶上,预计2026年至2031年将以6.98%的复合年增长率成长,这主要得益于现代超市、D2C品牌和跨境电商平台不断扩大SKU和分销点。在海鲜、水果和疫苗产业,运输失败造成的损失远超过物流溢价,因此需要采用GDP认证的合作伙伴并完善低温运输通讯协定。日益严格的药品可追溯性监管提高了进入门槛,促使市场更加关注拥有检验流程的营运商,并加剧了越南货运和物流市场的整合。

农业和建筑等传统行业的核心运输量保持不变,但运输方式正在转变。湄公河三角洲的驳船和铁路试验正在将大米和沙子等大宗货物从拥挤的公路运输中转移出去。石油、天然气和矿业物流仍然高度专业化,高安全标准和复杂的包机安排更有利于那些专注于特定领域的货运代理。

截至2025年,出口製造业在大宗货物运输中主导,占越南货运和物流市场的64.12%。然而,随着社群电商和跨境购物的蓬勃发展,宅配、速递和小包裹业务的收入持续成长,预计2026年至2031年的复合年增长率将达到7.52%。集中式出口包裹递送(宅配)的快速成长正推动营运商实现枢纽自动化并整合海关API,将交货週期缩短一半。仓储业也顺应数位化趋势,预计在水产养殖和疫苗供应链的推动下,温控仓储资产在2026年至2031年间的复合年增长率将达到7.89%。随着区块链载货证券和物联网感测器网路的普及,服务边界正在变得模糊。在越南货运和物流市场,货运代理商正将即时视觉性与增值包装相结合,以确保在商品同质化趋势下获得利润。

儘管货运仍占据主导地位,但运输方式正在转变。道路运输的规模将在2031年之前保持稳定,但空运和快递将在速度比成本更重要的特定运输领域占据更大份额。数位化货运平台将整合现货货运,使卡车运转率提高12%,并解决空驶返程和人工文书工作等挑战。综合规划将实现公路、海运和铁路相结合的多模态路线,从而减少二氧化碳排放,并吸引具有环境、社会和治理(ESG)意识的出口商。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 人口统计数据

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 通货膨胀

- 经济表现和公司概况

- 电子商务产业的趋势

- 製造业趋势

- 运输和仓储业的GDP

- 出口趋势

- 进口趋势

- 燃油价格

- 卡车运输营运成本

- 卡车运输车队规模(按类型)

- 主要卡车供应商

- 物流绩效

- 按交通方式分享

- 海运船队运力

- 班轮运输连接

- 停靠港口和演出

- 货运费率趋势

- 货物吨位趋势

- 基础设施

- 法规结构(公路和铁路)

- 法规结构(海事和航空)

- 价值炼和通路分析

- 市场驱动因素

- 电子商务小包(B2C 和 C2C)的蓬勃发展

- 电子产品和服装生产向越南近岸外包

- 东协「单一窗口」海关数位化

- 跨境公路货运量迅速成长,目的地为中国、寮国和柬埔寨

- 进口可再生能源零件(风力发电机叶片、太阳能发电相关零件)

- 水产养殖出口和疫苗物流的低温运输需求

- 市场限制

- 国内货柜供需失衡及空货柜搬迁成本

- 卡车驾驶人短缺和劳动力老化

- 由于最后一公里网路分散,高成本(每站里程成本)

- 由于排放交易体系(ETS)导致碳排放监管成本增加

- 市场创新

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 终端用户产业

- 农业、渔业、林业

- 建设业

- 製造业

- 石油天然气、采矿和采石

- 批发和零售

- 其他的

- 物流职能

- 宅配、快捷邮件和小包裹(CEP)

- 按目的地

- 国内的

- 国际的

- 按目的地

- 货运代理

- 透过交通工具

- 航空

- 海路和内河航道

- 其他的

- 透过交通工具

- 货物运输

- 透过交通工具

- 航空

- 管道

- 铁路

- 路

- 海路和内河航道

- 透过交通工具

- 仓储

- 透过温度控制

- 非温控型

- 温度控制

- 透过温度控制

- 其他服务

- 宅配、快捷邮件和小包裹(CEP)

第六章 竞争情势

- 市场集中度

- 重大策略倡议

- 市占率分析

- 公司简介

- AP Moller-Maersk

- Aviation Logistics Corporation

- Bee Logistics Corporation

- DHL Group

- DSV A/S(Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx

- Gemadept

- Giao Hang Nhanh

- Hai Minh Group

- Hop Nhat International Joint Stock Company

- Indo Trans Logistics Corporation

- Kuehne+Nagel

- MACS Maritime Joint Stock Company

- Noi Bai Express and Trading Joint Stock Company

- NYK(Nippon Yusen Kaisha)Line

- PetroVietnam Transportation Corporation(PVTrans)

- Phuong Trang Bus Joint Stock Company-FUTA Bus Lines

- Saigon Cargo Service Corporation(SCSC)

- Samsung SDS

- Sojitz Corporation

- Transimex

- U&I Logistics Corporation

- United Parcel Service of America, Inc.(UPS)

- Vietfracht HoChiMinh

- Vietnam Foreign Trade Logistics Joint Stock Company(VINATRANS)

- Vietnam Maritime Corporation(Vinalines)

- ViettelPost(Including Viettel Logistics)

- Voltrans Logistics

- ZIM Integrated Shipping Services, Ltd.

第七章 市场机会与未来展望

The Vietnam freight and logistics market is expected to grow from USD 52.06 billion in 2025 to USD 55.5 billion in 2026 and is forecast to reach USD 76.39 billion by 2031 at 6.6% CAGR over 2026-2031.

This trajectory reflects sustained manufacturing inflows, e-commerce parcel growth, and public spending of USD 15 billion on roads, ports, and airports. Structural tailwinds include near-shoring from China, ASEAN single-window customs digitalization, and rising demand for temperature-controlled distribution that together lift volumes across road, sea, and air corridors. Competitive intensity is sharpening as international integrators deepen local footprints while domestic operators scale through cold-chain and last-mile investments. The Vietnam freight and logistics market, therefore, benefits from a virtuous cycle of infrastructure, trade liberalization, and digital transformation that reduces dwell times and unlocks new service niches.

Vietnam Freight And Logistics Market Trends and Insights

E-commerce Parcel Boom Drives Last-Mile Innovation

Domestic parcel volumes jumped 45% in 2024 as online marketplaces proliferated and social-commerce blunted geographic constraints. The Vietnam freight and logistics market has seen courier networks deploy automated sorters and AI route engines that shrink average delivery windows from 48 to 24 hours. Yet fragmented last-mile networks mean per-parcel delivery costs remain 28% above Thailand, spurring providers to pool micro-hubs and leverage crowdsourced drivers to widen rural reach. Regulatory momentum adds tailwind: simplified clearance for parcels under USD 200 now cuts customs dwell from five days to one. Capital follows demand, with ViettelPost opening 15 robotic sort centers and Giao Hang Nhanh pledging commune-level coverage by 2025. These moves embed digital density that accelerates future volume scaling and entrenches CEP as the fastest-growing slice of the Vietnam freight and logistics market.

Near-Shoring Transforms Manufacturing Logistics

Electronics and apparel relocations from China lifted manufacturing logistics demand 28% in 2024 as global brands hedged geopolitical and cost risk. Northern clusters host high-value electronics flows that prefer airfreight; component uplift at Noi Bai Airport climbed 35% year-over-year, forcing capacity additions and slot reprioritization. Samsung's expansion alone requires 2,400 TEU moves monthly, while Foxconn and Luxshare each operate closed-loop corridors to export gateways. Apparel producers leverage road-sea combinations, redirecting lead times 40% shorter than legacy China lanes. Providers offering kitting, return-handling, and quality-control warehousing now command premium margins, signaling a shift from pure transport to integrated contract logistics within the Vietnam freight and logistics market.

Container Imbalance Creates Cost Pressures

An export-to-import ratio of 3:1 strands empties inland, raising average repositioning outlay to USD 85 per 20-foot box and USD 170 for 40-foot units. Container imbalance charges rose 25% in 2024 as availability dipped below 70% during peak coffee and textile seasons. Forwarders deploy tracking IoT tags and shared pools to lift utilization and shave 15-20% from separate carrier costs, yet structural trade asymmetry means headhaul surcharges are unlikely to abate quickly. The Vietnam freight and logistics market thus endures volatility that squeezes margins for SME shippers.

Other drivers and restraints analyzed in the detailed report include:

- ASEAN Single Window Accelerates Cross-Border Efficiency

- Cross-Border Road Freight Corridor Expansion

- Workforce Shortages Constrain Capacity Growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing drove 35.12% of Vietnam freight and logistics market share in 2025, anchored by electronics and garment hubs that mandate precise inventory sync with overseas buyers. Tight cycle times spur RFID-enabled component kitting and postponement warehousing, raising third-party logistics penetration. Wholesale and retail trade is catching up, projected to rise 6.98% CAGR (2026-2031) as modern grocery, direct-to-consumer brands, and cross-border marketplaces widen SKUs and delivery nodes. Cold-chain protocols expand with seafood, fruit, and vaccines, where shipment failure costs far exceed logistics premiums and justify GDP-certified partners. Regulatory pushes for pharmaceutical traceability raise barriers, funneling demand toward players with validated processes, reinforcing consolidation trends inside the Vietnam freight and logistics market.

Traditional sectors such as agriculture and construction keep baseline tonnage but face modal substitution; barge and rail pilots in the Mekong Delta shift bulky rice and sand away from congested highways. Oil, gas, and mining logistics remain specialist, with higher safety compliance and charter-party complexity that reward niche forwarders.

Freight transport generated 64.12% of the Vietnam freight and logistics market size in 2025 as export manufacturing dictated bulk cargo flows. Yet courier, express, and parcel revenue is on course for a 7.52% CAGR (2026-2031), commandeering incremental share as social-commerce and cross-border shopping proliferate. The CEP surge pushes operators to automate hubs and integrate customs APIs, compressing cut-off-to-delivery cycles by half. Warehousing follows digital cues; temperature-controlled assets are set to grow at 7.89% CAGR (2026-2031), supported by aquaculture and vaccine supply chains. As blockchain bills of lading and IoT sensor networks become standard, service boundaries blur; freight transporters bundle real-time visibility and value-added packaging to secure margin against commoditization in the Vietnam freight and logistics market.

Continued freight-transport primacy masks intra-modal shifts. Road retains scale through 2031, but airfreight and express haulage capture discretionary shipments where velocity trumps cost. Digital freight platforms aggregate spot loads that raise truck utilization by 12%, attacking pain points of empty backhauls and manual paperwork. Integrated planning unlocks multimodal itineraries that blend road, sea, and rail, trimming CO2 and appealing to ESG-minded exporters.

The Vietnam Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- A.P. Moller - Maersk

- Aviation Logistics Corporation

- Bee Logistics Corporation

- DHL Group

- DSV A/S (Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx

- Gemadept

- Giao Hang Nhanh

- Hai Minh Group

- Hop Nhat International Joint Stock Company

- Indo Trans Logistics Corporation

- Kuehne+Nagel

- MACS Maritime Joint Stock Company

- Noi Bai Express and Trading Joint Stock Company

- NYK (Nippon Yusen Kaisha) Line

- PetroVietnam Transportation Corporation (PVTrans)

- Phuong Trang Bus Joint Stock Company - FUTA Bus Lines

- Saigon Cargo Service Corporation (SCSC)

- Samsung SDS

- Sojitz Corporation

- Transimex

- U&I Logistics Corporation

- United Parcel Service of America, Inc. (UPS)

- Vietfracht HoChiMinh

- Vietnam Foreign Trade Logistics Joint Stock Company (VINATRANS)

- Vietnam Maritime Corporation (Vinalines)

- ViettelPost (Including Viettel Logistics)

- Voltrans Logistics

- ZIM Integrated Shipping Services, Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.23 Regulatory Framework (Sea and Air)

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Parcel Boom (B2C and C2C)

- 4.25.2 Near-Shoring of Electronics and Apparel Production into Vietnam

- 4.25.3 ASEAN "Single Window" Customs Digitalisation

- 4.25.4 Surge in Cross-Border Road Freight to China-Laos-Cambodia

- 4.25.5 Renewable-Energy Component Imports (Wind-Turbine Blades, Solar)

- 4.25.6 Cold-Chain Demand for Aquaculture Exports and Vaccine Logistics

- 4.26 Market Restraints

- 4.26.1 Domestic Container Imbalance and Empty-Repositioning Costs

- 4.26.2 Truck Driver Shortages and Ageing Workforce

- 4.26.3 Fragmented Last-Mile Network Driving High Mile-Per-Stop Cost

- 4.26.4 Increasing Carbon-Emission Compliance Costs (ETS-Style)

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Suppliers

- 4.28.3 Bargaining Power of Buyers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Move

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 Aviation Logistics Corporation

- 6.4.3 Bee Logistics Corporation

- 6.4.4 DHL Group

- 6.4.5 DSV A/S (Including DB Schenker)

- 6.4.6 Expeditors International of Washington, Inc.

- 6.4.7 FedEx

- 6.4.8 Gemadept

- 6.4.9 Giao Hang Nhanh

- 6.4.10 Hai Minh Group

- 6.4.11 Hop Nhat International Joint Stock Company

- 6.4.12 Indo Trans Logistics Corporation

- 6.4.13 Kuehne+Nagel

- 6.4.14 MACS Maritime Joint Stock Company

- 6.4.15 Noi Bai Express and Trading Joint Stock Company

- 6.4.16 NYK (Nippon Yusen Kaisha) Line

- 6.4.17 PetroVietnam Transportation Corporation (PVTrans)

- 6.4.18 Phuong Trang Bus Joint Stock Company - FUTA Bus Lines

- 6.4.19 Saigon Cargo Service Corporation (SCSC)

- 6.4.20 Samsung SDS

- 6.4.21 Sojitz Corporation

- 6.4.22 Transimex

- 6.4.23 U&I Logistics Corporation

- 6.4.24 United Parcel Service of America, Inc. (UPS)

- 6.4.25 Vietfracht HoChiMinh

- 6.4.26 Vietnam Foreign Trade Logistics Joint Stock Company (VINATRANS)

- 6.4.27 Vietnam Maritime Corporation (Vinalines)

- 6.4.28 ViettelPost (Including Viettel Logistics)

- 6.4.29 Voltrans Logistics

- 6.4.30 ZIM Integrated Shipping Services, Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告

2026年全球货车市场报告2026年全球货运和物流市场报告2026年全球零碳运输市场报告 货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分

货运及物流市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者及运输方式划分 2026-2030年全球货物审核与支付市场

2026-2030年全球货物审核与支付市场 东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)南美货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东协货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中东欧货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)亚太地区货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)南美货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国货运与物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)