|

市场调查报告书

商品编码

1939722

美国地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United States Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

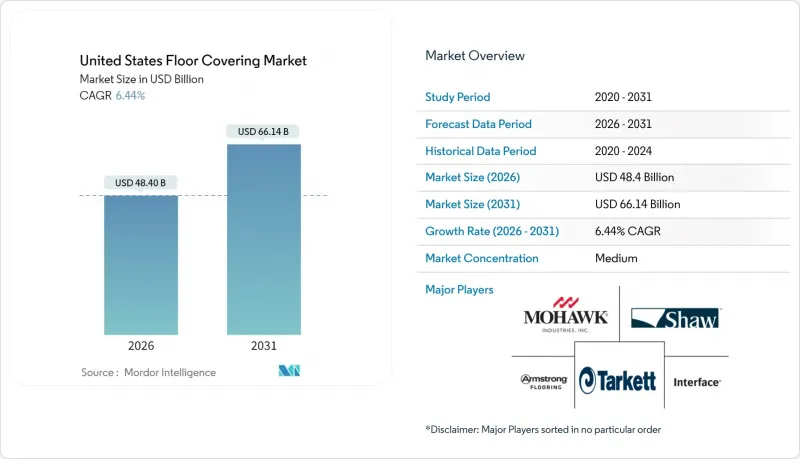

2025年美国地板市场价值454.7亿美元,预计到2031年将达到661.4亿美元,高于2026年的484亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.44%。

目前,美国地板市场正受到住宅维修活动活性化、弹性地板材料产品创新以及阳光地带人口成长的推动。商业维修需求旺盛,加上税收优惠抵消了高额借贷成本的影响,进一步支撑了市场。领先的製造商正专注于防水和耐刮擦技术,而直接面向消费者的电子商务模式正在迅速改变市场准入模式。然而,原物料价格持续上涨和安装人员严重短缺仍然是主要的成本压力,给美国地板市场的乐观前景蒙上了一层阴影。

美国地板材料市场趋势与分析

受IRA支持的商业维修税收优惠政策加速了地板材料更换。

免税实体资格的扩大刺激了政府机构和非营利机构的需求,这些机构先前因种种原因推迟了地板材料更换。维修与疫情后的室内布局调整相契合,而兼具隔音和隔热性能的地板材料升级方案也成为首要考虑因素。随着设计公司调整竞标以适应税务申报时间表,订单在人口密集的商业区也看到了稳定的订单积压。这种转变推动了对采用再生材料并符合节能目标的优质弹性地板材料和地毯砖的需求。

灵活办公空间的快速成长正在推动办公室和共享办公空间对模组化地板材料的需求。

混合办公模式的兴起推动了对模组化地板材料的需求,这种地板可以根据座位安排的变化进行拆卸和重新安装。受企业需要快速应对租赁续约的推动,地毯砖的销售量超过了疫情前的商业预期。在融合住宅和商业空间的「耐用型」设计中,设计师们选择的产品既要提供舒适的脚感,又要保证滚轮的耐用性,从而将柔软的质感与硬朗的元素相结合。吸音背衬系统有助于降低开放式空间的噪音,并支援健康认证。卡扣式系统因其能最大限度地减少停机时间而成为小规模安装区域的首选——这一特性对于透过空间轮换来盈利的共同工作空间来说至关重要。因此,供应商正在投资染料喷印技术,该技术能够实现快速定制,而无需延长前置作业时间。

高利率抑制了新的办公大楼和零售建筑项目。

预计2023年商业房地产交易量将下降37%,2024年将进一步下降14%。开发商推迟了投机性新建设,抑制了大规模核心筒计划对地板材料的需求。现有办公大楼的空置率延长了维修週期,迫使业主进行渐进式升级,而不是彻底更换地板。随着电子商务占据自由裁量权支配支出的大部分,零售业的资本支出也同样谨慎。因此,美国地板材料市场正将重心转向预算范围内可行的维修项目。提案提供成本节约型工程产品系列以及资金筹措支持,但主要都会区的需求不足仍限制整体成长。

细分市场分析

到2025年,地毯和地垫将占美国地板材料市场35.62%的份额,这主要得益于它们在多用户住宅和办公室的隔音效果。然而,弹性地板材料预计将以7.80%的复合年增长率成长,比美国整体地板材料市场成长高出约1.4个百分点。兼具防水和易维护特性的豪华乙烯基瓷砖(LVT)和硬芯地板产品正在推动其普及。这种转变导致入门级价位的非弹性硬质地板(例如现场涂饰木地板和瓷砖)的市场份额下降。尤其值得一提的是,不含PVC的弹性地板材料系列,例如Mohawk的PureTec系列,正受到永续性的消费者的青睐。

碳酸钙填料成本的稳定性也提振了2024年弹性地板材料市场,为翻新高峰期的促销价格提供了支撑。因此,SPC卡扣式地板在社交平臺销售的消费套装中占据了重要地位。製造商透过采用享有延长保固期的专有耐磨层来提高利润率,这项特性吸引了重视长期价值的住宅。

美国地板材料市场按产品类型(地毯、弹性地板材料、豪华乙烯基瓷砖(LVT)等)、最终用户(住宅、商业办公室)、分销管道(专业地板材料零售商、大型五金建材超市等)和地区(东北部、东南部等)进行细分。市场预测以美元(USD)为以金额为准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

第五章 市场概览

- 市场驱动因素

- 根据《美国再投资与就业法案》(IRA)提供的商业设施维修税收优惠政策,地板材料更换速度加快。

- 灵活办公空间的快速成长正在推动办公室和共享办公空间对模组化地板的需求。

- 医疗设施建设的快速成长对低挥发性有机化合物(VOC)和耐磨地板材料提出了更高的要求。

- 由于电子商务仓库的扩张,耐用硬地面材料的安装量增加。

- 住宅和维修活动的成长

- 消费者越来越偏好永续性和低维护成本。

- 市场限制

- 高利率抑制了新的办公大楼和零售建筑项目。

- 石油化学原料价格的波动给乙烯基和橡胶製品的利润率带来了压力。

- 熟练承包商短缺导致人事费用上升和计划延期。

- 由于强制要求避免将地毯丢弃掩埋,导致地毯处理成本增加。

- 价值/供应链分析

- 监理展望

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 产业间竞争

- 定价分析

第六章 市场规模与成长预测

- 依产品类型

- 地毯和毛毯

- 宽幅地毯

- 地毯砖

- 块毯

- 弹性地板材料

- 豪华乙烯基瓷砖(LVT)

- 乙烯基板材和VCT

- 橡胶地板

- 油布

- 非弹性硬质地板

- 陶瓷和陶瓷瓷砖

- 天然石瓷砖

- 实木地板

- 工程木地板

- 复合地板

- 竹子和软木地板

- 地毯和毛毯

- 最终用户

- 住宅

- 商业的

- 零售

- 饭店及休閒

- 卫生保健

- 教育

- 公共和公共机构

- 其他的

- 透过分销管道

- 专业地板零售商

- 大型家居建材商店

- 独立承包商/零售商

- 直接面向消费者(电子商务)

- 批发商/经销商

- 按地区(美国)

- 东北

- 东南

- 中西部

- 西南

- 西

第七章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介:莫霍克工业公司

- Shaw Industries Group Inc.

- Tarkett SA

- Armstrong Flooring Inc.

- Interface Inc.

- Mannington Mills Inc.

- Gerflor Group

- Forbo Flooring Systems

- LG Hausys(Hanwha)

- Beaulieu International Group

- The Dixie Group Inc.

- Milliken & Company

- Engineered Floors LLC

- Karndean Designflooring

- Roppe Corporation

- Congoleum Corporation

- AHF Products(Bruce)

- Somerset Hardwood Flooring

- Quick-Step USA

- LL Flooring Holdings Inc.

- COREtec Floors

- Tandus Centiva(Tarkett)

- Market Opportunities & Future Outlook

- White-Space & Unmet-Need Assessment

The US flooring market was valued at USD 45.47 billion in 2025 and estimated to grow from USD 48.4 billion in 2026 to reach USD 66.14 billion by 2031, at a CAGR of 6.44% during the forecast period (2026-2031).

Residential renovation activity, resilient product innovation, and strong population growth in Sunbelt states underpin the current momentum of the US flooring market. Demand is reinforced by tax-advantaged commercial retrofits that offset the drag from high borrowing costs. Scale manufacturers concentrate on waterproof and scratch-resistant technologies, while direct-to-consumer e-commerce rapidly reshapes go-to-market models. Sustained raw-material inflation and an acute installer shortage remain the key cost pressures that temper the otherwise upbeat outlook of the US flooring market.

United States Floor Covering Market Trends and Insights

IRA-Backed Commercial Retrofit Tax Incentives Accelerating Flooring Upgrades

Expanded eligibility for tax-exempt entities unlocks demand from government and nonprofit facilities that have historically delayed floor replacements. Retrofits dovetail with post-pandemic reconfiguration of interiors, so flooring upgrades that deliver both acoustic and thermal performance rise to the top of specification lists. Design firms are aligning bids with tax schedules, creating a steady backlog for installers in dense commercial districts. The change supports premium resilient and carpet-tile platforms that incorporate recycled content while meeting energy targets.

Flexible Workspace Boom Driving Modular Flooring Demand in Offices and Co-working Hubs

Hybrid work models catalyze demand for modular flooring that can be lifted and re-laid when seating plans change. Carpet tile volumes surpassed pre-pandemic commercial forecasts as operators seek quick-turn solutions during lease renegotiations. Resimercial aesthetics blend soft textures with hard-surface accents so designers specify collections that balance underfoot comfort with chair-castor durability. Acoustic backing systems mitigate noise in open plans and support wellness certifications. Smaller installation zones favour click-lock systems that minimize downtime, a feature prized by co-working providers that monetize space churn. Suppliers are therefore investing in dye-infusion print technologies that enable rapid customization without extending lead times.

High Interest Rates Suppressing New Office and Retail Build-outs

Transaction volumes in commercial real estate fell 37% in 2023 and a further 14% in 2024 . Developers defer speculative ground-ups, curbing floor covering demand in large core-shell projects. Vacancies in legacy office towers extend retrofit cycles, pushing landlords to phase upgrades rather than execute full-floor replacements. Retail capital expenditure is similarly cautious as e-commerce captures discretionary spending. The US flooring market thus shifts focus toward refurbishment programs that can proceed under constrained budgets. Suppliers bundle value-engineered lines with financing support, yet volume shortfalls in gateway cities continue to temper overall growth.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare Construction Surge Requiring Low-VOC Resilient Surfaces

- E-commerce Warehouse Expansion Increasing Durable Hard-Surface Installations

- Skilled Installer Shortage Elevating Labor Costs and Project Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carpets and rugs retained 35.62% of the US flooring market in 2025 due to acoustic benefits in multifamily housing and offices. However, resilient flooring is forecast to grow at a 7.80% CAGR, almost 1.4 percentage points above the overall US flooring market. Luxury vinyl tile and rigid core collections spearhead adoption because they deliver waterproof performance and easy maintenance. The shift pulls share from non-resilient hard surfaces such as site-finished wood and ceramic in entry-level price tiers. Notably, PVC-free resilient lines led by Mohawk's PureTech have broadened acceptance among sustainability-focused buyers.

In 2024, the resilient category also benefited from cost stabilization in calcium carbonate fillers, supporting aggressive promotional pricing during peak remodeling season. As a result, SPC click-lock planks featured prominently in direct-to-consumer bundles marketed through social platforms. Manufacturers augment margins through proprietary wear layers that qualify for extended warranties, a feature that resonates with homeowners concerned about long-term value.

The US Floor Covering Market Segments Into by Product Type (Carpet and Rugs, Resilient Flooring Luxury Vinyl Tile (LVT), and More), End-User (Residential, and Commercial Office), Distribution Channel (Specialty Flooring Retailers, Big-Box Home Centers, and More), Region (Northeast, Southeast, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Shaw Industries Group Inc.

- Tarkett S.A.

- Armstrong Flooring Inc.

- Interface Inc.

- Mannington Mills Inc.

- Gerflor Group

- Forbo Flooring Systems

- LG Hausys (Hanwha)

- Beaulieu International Group

- The Dixie Group Inc.

- Milliken & Company

- Engineered Floors LLC

- Karndean Designflooring

- Roppe Corporation

- Congoleum Corporation

- AHF Products (Bruce)

- Somerset Hardwood Flooring

- Quick-Step USA

- LL Flooring Holdings Inc.

- COREtec Floors

- Tandus Centiva (Tarkett)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

5 Market Overview

- 5.1 Market Drivers

- 5.1.1 IRA-Backed Commercial Retrofit Tax Incentives Accelerating Flooring Upgrades

- 5.1.2 Flexible Workspace Boom Driving Modular Flooring Demand in Offices & Co-working Hubs

- 5.1.3 Healthcare Construction Surge Requiring Low-VOC Resilient Surfaces

- 5.1.4 E-commerce Warehouse Expansion Increasing Durable Hard-Surface Installations

- 5.1.5 Growth in Residential Construction and Renovation Activity

- 5.1.6 Rising Consumer Preferences for Sustainability and Low Maintenance

- 5.2 Market Restraints

- 5.2.1 High Interest Rates Suppressing New Office & Retail Build-outs

- 5.2.2 Petrochemical Feedstock Volatility Compressing Vinyl & Rubber Margins

- 5.2.3 Skilled Installer Shortage Elevating Labor Costs & Project Delays

- 5.2.4 Landfill Diversion Mandates Raising Carpet End-of-Life Costs

- 5.3 Value / Supply-Chain Analysis

- 5.4 Regulatory Outlook

- 5.5 Technological Outlook

- 5.6 Porter's Five Forces

- 5.6.1 Bargaining Power of Suppliers

- 5.6.2 Bargaining Power of Buyers

- 5.6.3 Threat of New Entrants

- 5.6.4 Threat of Substitutes

- 5.6.5 Industry Rivalry

- 5.7 Pricing Analysis

6 Market Size & Growth Forecasts (Value)

- 6.1 By Product Type

- 6.1.1 Carpets & Rugs

- 6.1.1.1 Broadloom Carpet

- 6.1.1.2 Carpet Tiles

- 6.1.1.3 Area Rugs

- 6.1.2 Resilient Flooring

- 6.1.2.1 Luxury Vinyl Tile (LVT)

- 6.1.2.2 Vinyl Sheet & VCT

- 6.1.2.3 Rubber Flooring

- 6.1.2.4 Linoleum

- 6.1.3 Non-Resilient Hard Surface

- 6.1.3.1 Ceramic & Porcelain Tile

- 6.1.3.2 Natural Stone Tile

- 6.1.3.3 Solid Wood Flooring

- 6.1.3.4 Engineered Wood Flooring

- 6.1.3.5 Laminate Flooring

- 6.1.3.6 Bamboo & Cork Flooring

- 6.1.1 Carpets & Rugs

- 6.2 By End-User

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.2.1 Retail

- 6.2.2.2 Hospitality & Leisure

- 6.2.2.3 Healthcare

- 6.2.2.4 Education

- 6.2.2.5 Public & Institutional

- 6.2.2.6 Others

- 6.3 By Distribution Channel

- 6.3.1 Specialty Flooring Retailers

- 6.3.2 Big-Box Home Centers

- 6.3.3 Independent Contractors / Dealers

- 6.3.4 Direct-to-Consumer E-commerce

- 6.3.5 Wholesale / Distributors

- 6.4 By Region (U.S.)

- 6.4.1 Northeast

- 6.4.2 Southeast

- 6.4.3 Midwest

- 6.4.4 Southwest

- 6.4.5 West

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)Mohawk Industries Inc.

- 7.4.1 Shaw Industries Group Inc.

- 7.4.2 Tarkett S.A.

- 7.4.3 Armstrong Flooring Inc.

- 7.4.4 Interface Inc.

- 7.4.5 Mannington Mills Inc.

- 7.4.6 Gerflor Group

- 7.4.7 Forbo Flooring Systems

- 7.4.8 LG Hausys (Hanwha)

- 7.4.9 Beaulieu International Group

- 7.4.10 The Dixie Group Inc.

- 7.4.11 Milliken & Company

- 7.4.12 Engineered Floors LLC

- 7.4.13 Karndean Designflooring

- 7.4.14 Roppe Corporation

- 7.4.15 Congoleum Corporation

- 7.4.16 AHF Products (Bruce)

- 7.4.17 Somerset Hardwood Flooring

- 7.4.18 Quick-Step USA

- 7.4.19 LL Flooring Holdings Inc.

- 7.4.20 COREtec Floors

- 7.4.21 Tandus Centiva (Tarkett)

- 7.5 Market Opportunities & Future Outlook

- 7.5.1 White-Space & Unmet-Need Assessment

地板材料市场:2026-2032年全球市场预测(依产品类型、安装方式、销售管道及最终用户划分)

地板材料市场:2026-2032年全球市场预测(依产品类型、安装方式、销售管道及最终用户划分) 英国地板覆盖材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

英国地板覆盖材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球家居布置和地板覆盖材料市场报告地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

2026年全球家居布置和地板覆盖材料市场报告地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本地面铺装材料市场报告(按材料、配销通路、最终用户和地区划分,2026-2034年)

日本地面铺装材料市场报告(按材料、配销通路、最终用户和地区划分,2026-2034年) 地板覆盖市场-全球产业规模、份额、趋势、机会和预测,按材料(弹性、非弹性、软地板覆盖)、按应用(住宅、商业、工业)、按地区、按竞争细分,2020-2030 年预测弹性地板材料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)印尼地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)地板树脂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

地板覆盖市场-全球产业规模、份额、趋势、机会和预测,按材料(弹性、非弹性、软地板覆盖)、按应用(住宅、商业、工业)、按地区、按竞争细分,2020-2030 年预测弹性地板材料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)印尼地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)地板树脂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)