|

市场调查报告书

商品编码

1940645

英国地板覆盖材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United Kingdom Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

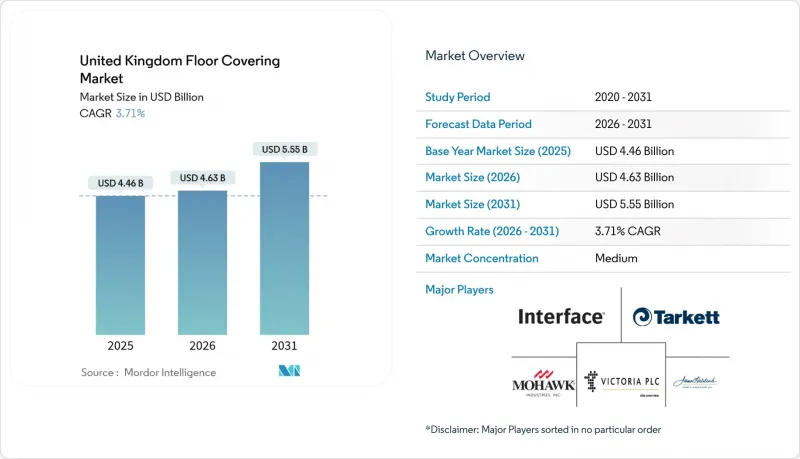

据估计,英国地板覆盖材料市场到 2026 年的价值将达到 46.3 亿美元,高于 2025 年的 44.6 亿美元。

预计到 2031 年将达到 55.5 亿美元,2026 年至 2031 年的复合年增长率为 3.71%。

这一稳步增长凸显了该行业已从疫情后的波动期过渡到稳步增长期,这主要得益于建设业的复工復产以及消费者对高端地面覆盖材料需求的转变。包括住宅维修、商业室内装修和政府主导的维修项目在内的广泛需求基础,支撑了市场的韧性。混合办公模式的兴起推动了模组化地毯砖的新订单增长,而以逼真纹理和低维护成本为特点的豪华乙烯基瓷砖(LVT)的需求在各个细分市场均加速增长。通路向线上和大型零售商的转移提高了产品认知度和价格透明度,加剧了竞争,同时也给利润率带来了压力,而原材料成本的波动和通货膨胀则进一步加剧了这种竞争。

英国地板覆盖材料市场趋势及分析

疫情后住宅维修热潮推动住宅需求

疫情后住宅维修活动的激增持续改变住宅地面覆盖材料的需求。住宅在兼具多种功能的空间中,更加重视舒适性和美观。这一趋势已从疫情初期的维修演变为对高端地面覆盖材料解决方案的持续投资,以提升视觉吸引力和功能性。地毯在2025年展现出復苏的迹象,设计师们偏好色彩丰富、图案大胆的地毯,尤其适用于卧室和客厅等注重舒适性的空间。同一空间内复合地面覆盖材料的普及,为製造商提供了机会,使其能够提供和谐统一的产品系列,实现不同区域之间的无缝过渡。这种行为转变反映了人们对住宅空间的构想和使用方式的根本性重新调整,从而推动了对各类地面覆盖材料材料的持续需求。

大规模公共部门维修计画会创造持续的需求。

政府在医疗、教育和公共基础设施领域的维修项目,透过多年计划週期创造对地板覆盖材料的持续需求,从而稳定市场。这些多年计划週期透过确保稳定的采购量来支撑市场稳定。诸如英国国家医疗服务体系(NHS)新建医院计画和全国学校重组计画等倡议,为供应商提供了可预测的商机。专注于医疗和教育领域地板覆盖材料的公司尤其能够从中受益。例如,James Halstead PLC旗下的Polyflor品牌在医疗和教育弹性地板覆盖材料领域创下了1.26亿英镑(1.6亿美元)的销售纪录。

高通膨会抑制消费者的购买力。

持续的通膨压力迫使消费者推迟非必要的住宅维修,儘管潜在需求强劲,但地板覆盖材料的非必需品购买却面临阻力。英国建筑材料价格指数持续波动,其对地板覆盖材料材料的具体影响波及整个计划的经济效益。注重预算的消费者越来越倾向于选择提案而非高端功能的产品,这可能会挤压高端製造商的利润空间。这一趋势对住宅维修市场的影响尤其显着,计划延期可能会波及整个供应链,并影响零售商的库存管理。然而,这一趋势也为那些能够提供既满足价格敏感型需求又能维持品质标准的高性价比解决方案的製造商创造了机会。

细分市场分析

在英国地板覆盖材料市场,弹性地板覆盖材料预计到2025年将以5.93%的复合年增长率成长,而非弹性地板覆盖材料将维持42.95%的市场份额。豪华乙烯基瓷砖(LVT)尤其引领市场成长,凭藉其逼真的纹理、对潮湿环境的适应性以及快速施工等优势,在住宅和商业场所都广受欢迎。捲材乙烯基和复合乙烯基地砖(VCT)在医疗保健和教育领域保持着领先地位,而软木和橡胶等小众材料也正在崛起,尤其是在註重环保的可持续发展计划中。地毯和地垫正在復兴,其大胆的图案和环保再生纱线迎合了消费者对美观和永续性的双重偏好。瓷砖和工程木地板等硬质地板覆盖材料依然保持着其奢华魅力,而中等价位的复合覆盖材料则因消费者越来越倾向于选择更耐用、设计更灵活的硬芯LVT而逐渐失去市场份额。

市场需求正变得日益两极化。一方面,高端专案提供客製化的天然材料,营造专属奢华感;另一方面,高性能合成材料迎合注重性价比的买家,兼具价值和耐用性。供应商同时提供这两种价位的产品,有助于降低市场波动风险,并在计划中占据更广泛的市场份额,从而增强其在竞争激烈的市场环境中的韧性。

预计到2031年,维修改造市场将以4.86%的复合年增长率成长,缩小与新建建筑市场的差距(2025年新建建筑市场占总销售额的53.78%)。这一增长主要由老旧住宅和商业物业的业主推动,他们致力于改善隔音和防潮性能,以提升空间的整体品质。快速安装也日益受到重视,免胶铺装和浮动系统因其便利性、高效性和对不同环境的适应性而备受青睐。同时,租赁型住宅(BTR)的租户周转率高、使用强度大,因此对耐用、易清洁且能经受高强度使用并长期保持功能性和美观性的饰面材料的需求也随之增长。

同时,开发商在新住宅计划和物流设施中指定使用耐用材料,但利率上升限制了这一发展速度,影响了计划的整体可行性和财务规划。为了解决维修的经济性问题,产品工程师正在开发针对现有地面直接施工优化的产品,这些产品只需极少的基层处理,从而确保维修计划经济高效且省时。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 疫情后住宅维修热潮

- 规划大规模公共部门维修计划

- 人们对豪华乙烯基瓷砖(LVT)的偏好日益增长

- 办公室对模组化地毯砖的需求不断增长

- 政府对再生木地板的激励措施

- 扩大租赁住宅计划

- 市场限制

- 高通膨抑制了可自由支配支出。

- 原油衍生原料价格波动

- 专业安装工人短缺

- 由于商业租赁期限延长,导致室内装修工程延误

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解市场近期发展动态(新产品发表、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模及成长预测(金额:美元)

- 依产品类型

- 地毯和毛毯

- 弹性地板覆盖材料

- 乙烯基片材和乙烯基复合磁砖

- 豪华乙烯基瓷砖(LVT)

- 油布

- 橡胶地板材料

- 软木地板材料

- 非弹性地板覆盖材料

- 陶瓷和陶瓷瓷砖

- 天然石材

- 硬木

- 工程木材

- 层压板

- 依建筑类型

- 新建工程

- 维修和更换

- 最终用户

- 住宅

- 商业

- 工业和公共基础设施

- 透过分销管道

- B2C/零售通路

- 家居建材商店

- 专卖店

- 在线的

- 其他分销管道

- B2B/承包商/经销商

- B2C/零售通路

- 按地区

- 英格兰

- 苏格兰

- 威尔斯

- 北爱尔兰

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Victoria PLC

- Interface Inc.

- Tarkett SA

- James Halstead PLC(Polyflor)

- Mohawk Industries

- Shaw Industries Group

- Forbo Flooring Systems

- Gerflor Group

- Milliken & Company

- Amtico International

- Karndean Designflooring

- Cormar Carpets

- Brintons Carpets

- Balta Group

- BerryAlloc(Beaulieu)

- Moduleo(IVC Group)

- Armstrong Flooring

- BSW Timber Group

- Junckers Flooring

- Johnson Tiles

第七章 市场机会与未来展望

United Kingdom floor covering market size in 2026 is estimated at USD 4.63 billion, growing from 2025 value of USD 4.46 billion with 2031 projections showing USD 5.55 billion, growing at 3.71% CAGR over 2026-2031.

This measured rise highlights a sector moving from post-pandemic volatility to steady growth as construction resumes and consumers trade up to premium surfaces. A broad demand base spanning residential renovation, commercial fit-outs, and government refurbishment programs underpins the market's resilience. Hybrid work patterns generate fresh orders for modular carpet tiles, while luxury vinyl tile (LVT) accelerates across segments due to realistic aesthetics and low upkeep requirements. Distribution shifts toward online and big-box retail channels are widening product visibility and price transparency, reinforcing competitive intensity even as raw-material cost swings and inflation challenge margins.

United Kingdom Floor Covering Market Trends and Insights

Post-pandemic home-improvement boom drives residential demand

The post-pandemic surge in home improvement activity continues to reshape residential flooring demand, with homeowners prioritizing comfort and aesthetics in spaces that now serve multiple functions. This trend extends beyond initial lockdown-driven renovations, evolving into sustained investment in premium flooring solutions that enhance both visual appeal and functional performance. Carpets are seeing a resurgence in 2025, with designers favoring rich colors and bold patterns for comfort-focused spaces such as bedrooms and living rooms. The shift toward mixed flooring materials within single spaces creates opportunities for manufacturers offering coordinated product lines that enable seamless transitions between different zones. This behavioral change reflects a fundamental recalibration of how residential spaces are conceived and utilized, driving sustained demand for diverse flooring categories.

Large-scale public-sector refurbishment pipeline creates sustained demand

Government refurbishment programs in healthcare, education, and public infrastructure create sustained flooring demand through multi-year project cycles that stabilize the market. These multi-year project cycles support market stability by ensuring steady procurement flows. Initiatives such as the NHS New Hospital Programme and national school rebuilding efforts provide predictable revenue opportunities for suppliers. Companies specializing in healthcare-compliant and education-grade flooring are particularly well-positioned to benefit. For example, James Halstead PLC's Polyflor brand reported record revenues of GBP 126 million (USD 160 million) from its healthcare and education resilient flooring segment.

High inflation constrains consumer spending power

Persistent inflation pressures force consumers to defer non-essential home improvements, creating headwinds for discretionary flooring purchases despite underlying demand strength. The United Kingdom construction material price indices show continued volatility, with specific impacts on flooring-adjacent materials affecting overall project economics. Budget-conscious consumers increasingly prioritize value propositions over premium features, potentially compressing margins for manufacturers positioned in higher-end segments. This dynamic particularly affects the residential renovation market, where project deferrals can cascade through the supply chain and impact retailer inventory management. However, the trend also creates opportunities for manufacturers offering cost-effective solutions that maintain quality standards while addressing price-sensitive demand.

Other drivers and restraints analyzed in the detailed report include:

- Growing preference for luxury vinyl tile transforms product mix

- Rising demand for modular carpet tiles reshapes commercial spaces

- Volatile raw-material prices pressure manufacturing economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the United Kingdom market for floor coverings is witnessing a 5.93% CAGR growth in resilient surfaces, while non-resilient options command a 42.95% market share. Leading the charge, LVT (Luxury Vinyl Tile) captivates with its lifelike visuals, adaptability to wet areas, and swift installation, making it a preferred choice for both residential and commercial applications. Sheet vinyl and VCT (Vinyl Composition Tile) maintain their foothold in healthcare and education sectors, alongside niche players like cork and rubber, especially in sustainability-driven projects where eco-conscious materials are prioritized. Carpets and rugs are making a comeback, spotlighting bold patterns and eco-friendly recycled yarns, which cater to evolving consumer preferences for both aesthetics and sustainability. While hard surfaces such as porcelain and engineered wood retain their premium appeal, mid-tier laminates are losing market share as consumers increasingly opt for rigid-core LVT, which offers enhanced durability and design versatility.

A bifurcated demand map is emerging. On one side, bespoke natural materials cater to luxury developments, offering exclusivity and high-end appeal; on the other, high-performance synthetics address value and durability, meeting the needs of cost-conscious buyers. Vendors positioned across both price ladders mitigate volatility and capture a broader wallet share within projects, ensuring resilience in a competitive market landscape.

By 2031, the replacement and retrofit market is projected to grow at a rate of 4.86%, narrowing the gap with the new-build segment, which commanded 53.78% of the revenue in 2025. This growth is primarily driven by the increasing focus of owners of aging residential and commercial properties on enhancing acoustic comfort and moisture control to improve the overall quality of their spaces. They are also prioritizing quicker installations, gravitating towards loose-lay formats and floating systems that offer convenience, efficiency, and adaptability to various environments. Meanwhile, build-to-rent schemes are driving a demand for durable, easy-to-clean finishes, which are essential for properties experiencing high tenant turnover and frequent use, ensuring these properties remain functional and visually appealing over time.

While developers are specifying high-capacity materials for new residential projects and logistics parks, the pace of these developments is tempered by rising interest rates, which impact overall project feasibility and financial planning. In response to renovation economics, product engineers are now crafting SKUs that are optimized for direct installation over existing floors and require less subfloor preparation, ensuring cost-effectiveness and time efficiency in retrofit projects.

The United Kingdom Floor Covering Market Report is Segmented by Product Type (Carpet and Rugs, Resilient Floor Covering, Non-Resilient Floor Covering), Construction Type (New Construction, Renovation & Replacement), End User (Residential, Commercial, Industrial & Public Infrastructure), Distribution Channel (B2C/Retail Channels, B2B/Contractors/Dealers), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Victoria PLC

- Interface Inc.

- Tarkett SA

- James Halstead PLC (Polyflor)

- Mohawk Industries

- Shaw Industries Group

- Forbo Flooring Systems

- Gerflor Group

- Milliken & Company

- Amtico International

- Karndean Designflooring

- Cormar Carpets

- Brintons Carpets

- Balta Group

- BerryAlloc (Beaulieu)

- Moduleo (IVC Group)

- Armstrong Flooring

- BSW Timber Group

- Junckers Flooring

- Johnson Tiles

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Pandemic Home-Improvement Boom

- 4.2.2 Large-Scale Public-Sector Refurbishment Pipeline

- 4.2.3 Growing Preference for Luxury Vinyl Tile (Lvt)

- 4.2.4 Rising Demand for Modular Carpet Tiles In Offices

- 4.2.5 Government Incentives For Recycled Content Flooring

- 4.2.6 Expansion of Build-To-Rent Housing Projects

- 4.3 Market Restraints

- 4.3.1 High Inflation Dampening Discretionary Spend

- 4.3.2 Volatile Crude-Derived Raw-Material Prices

- 4.3.3 Skills Shortage In Specialist Installation Labour

- 4.3.4 Extended Commercial Leasing Cycles Delaying Fit-Outs

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Carpet and Rugs

- 5.1.2 Resilient Floor Covering

- 5.1.2.1 Vinyl Sheets & VCT

- 5.1.2.2 Luxury Vinyl Tiles (LVT)

- 5.1.2.3 Linoleum

- 5.1.2.4 Rubber Flooring

- 5.1.2.5 Cork Flooring

- 5.1.3 Non-Resilient Floor Covering

- 5.1.3.1 Ceramic & Porcelain Tile

- 5.1.3.2 Natural Stone

- 5.1.3.3 Hardwood

- 5.1.3.4 Engineered Wood

- 5.1.3.5 Laminate

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation & Replacement

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial & Public Infrastructure

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail Channels

- 5.4.1.1 Home Centers

- 5.4.1.2 Specialty Stores

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B/Contractors/Dealers

- 5.4.1 B2C/Retail Channels

- 5.5 By Geography

- 5.5.1 England

- 5.5.2 Scotland

- 5.5.3 Wales

- 5.5.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Victoria PLC

- 6.4.2 Interface Inc.

- 6.4.3 Tarkett SA

- 6.4.4 James Halstead PLC (Polyflor)

- 6.4.5 Mohawk Industries

- 6.4.6 Shaw Industries Group

- 6.4.7 Forbo Flooring Systems

- 6.4.8 Gerflor Group

- 6.4.9 Milliken & Company

- 6.4.10 Amtico International

- 6.4.11 Karndean Designflooring

- 6.4.12 Cormar Carpets

- 6.4.13 Brintons Carpets

- 6.4.14 Balta Group

- 6.4.15 BerryAlloc (Beaulieu)

- 6.4.16 Moduleo (IVC Group)

- 6.4.17 Armstrong Flooring

- 6.4.18 BSW Timber Group

- 6.4.19 Junckers Flooring

- 6.4.20 Johnson Tiles

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Rising Preference for Underfloor Heating-Compatible Floors

- 7.3 Increased Adoption of Waterproof And Spill-Resistant Flooring

地板材料市场:2026-2032年全球市场预测(依产品类型、安装方式、销售管道及最终用户划分)

地板材料市场:2026-2032年全球市场预测(依产品类型、安装方式、销售管道及最终用户划分) 美国地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球家居布置和地板覆盖材料市场报告地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

2026年全球家居布置和地板覆盖材料市场报告地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本地面铺装材料市场报告(按材料、配销通路、最终用户和地区划分,2026-2034年)

日本地面铺装材料市场报告(按材料、配销通路、最终用户和地区划分,2026-2034年) 地板覆盖市场-全球产业规模、份额、趋势、机会和预测,按材料(弹性、非弹性、软地板覆盖)、按应用(住宅、商业、工业)、按地区、按竞争细分,2020-2030 年预测弹性地板材料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)印尼地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)地板树脂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

地板覆盖市场-全球产业规模、份额、趋势、机会和预测,按材料(弹性、非弹性、软地板覆盖)、按应用(住宅、商业、工业)、按地区、按竞争细分,2020-2030 年预测弹性地板材料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)印尼地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度地板树脂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)地板树脂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)