|

市场调查报告书

商品编码

1172495

职业中性增长在行业整合中放缓2022:年市场收入接近1000亿美元,对运营商行业的健康至关重要,但易受经济压力影响,私募股权公司崛起Carrier-neutral Growth Slows in 2022 Amid Consolidation: Market Approaches $100B in Annual Revenues, Still Central to Operator Industry Health, But Not Immune to Economic Pressures, Private Equity Players Ramp Up |

||||||

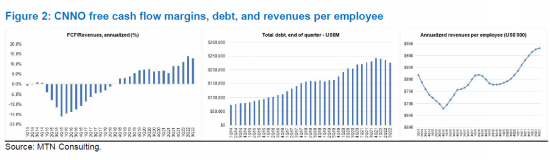

CNNO 收入在 2022 年第三季度达到约 239 亿美元(同比增长 3%),年化收入为 948 亿美元(同比增长 6%)。 这远低于 2021 年的年增长率 (12.5%) 和 2011-2021 年的平均年增长率 (16.6%)。 2021 年出现了一系列併购 (M&A) 和资本支出,但它们尚未对收入增长做出太大贡献。 因素包括销售週期的延长、重新谈判租赁协议的压力、随着市场成熟而加剧的价格竞争以及美元走强。 与此同时,CNNO 板块的盈利能力也越来越强。 在 2011-21 年的大部分时间里,平均自由现金流量利润率一直为负,但在过去三个季度中一直处于 11% 至 14% 的范围内。 随着利率上升,CNNO 不愿承担更多债务,而是专注于提高利润率。 CNNO建设网络是为了提高网络经济性,保持更多的网络流量,端到端地服务关键客户,跨基础设施类型进行交叉销售。我认为它会继续下去。

本报告审视了截至 2022 年第三季度 (2022 年第三季度) 全球运营商中立网络运营商 (CNNNO) 市场的最新发展。

文本中的图形

报告中提及的公司

|

|

内容

- 概览

- 分析运营商中立市场的独特挑战

- 市场总收入和增长率

- 主要公司概览

- 资本投资:未来两年有可能超过併购 (M&A) 和技术组件的扩展

- 综合业务模式:PE 行业推动的扩张趋势

- 附录

This short note provides a brief review of the development of the carrier-neutral network operator (CNNO) market through the third quarter of 2022 (3Q22).

VISUALS

CNNO revenues were approximately $23.9 billion (B) in 3Q22, up 3% YoY, and $94.8B for the annualized 3Q22 period (4Q21-3Q22), up 6% YoY. These growth rates are significantly less than the 12.5% growth seen in CY2021 and the average growth over the 2011-21 period of 16.6% per year. That's despite the acquisition spree the sector observed in 2021, when M&A spend of $42.1B easily outpaced capex of $31.4B. This M&A and capex spending have expanded the asset base of the sector, but not helped much with revenue growth, yet. Companies point to longer sales cycles, pressure to renegotiate leases, increased price competition as the market matures, and appreciation of the US dollar among the factors keeping a check on revenue growth. However, there are signs that the CNNO sector is becoming more profitable: average free cash flow margin has been in the 11-14% range for the last three quarters, while it was negative for most of the 2011-21 period. Debt remains high, totaling $225B in 3Q22, only slightly down from 3Q21; with higher interest rates, CNNOs are reluctant to take on more debt, instead focusing on margin growth. CNNOs will continue to build out their networks to improve network economics, keep more traffic on-net, provide key customers more of an end-to-end service, and cross sell across infrastructure types.

Private equity firms continue to invest heavily in the sector, and many have "digital infrastructure" funds aiming to combine assets across the three main infrastructure classes: towers, data centers, and fiber. As we argued in a July 2021 report, we continue to expect that "A new breed of integrated owners of infrastructure network assets will emerge over the next 2-3 years, converging towers, data centers, and fiber networks." PE firms' capital inflows are pushing this integration. A large group of well-funded PE firms are pursuing digital infrastructure opportunities. Some are explicitly aiming to assemble portfolios of integrated assets, and/or cobble them together into larger CNNOs able to address multi-sector opportunities from a position of massive scale. Ultimately most PEs do aim for liquidity events from these past investments, though some are content with the relatively steady cash flows spun off by CNNOs.

We will be formally updating our operator forecast soon. This update will include revised projections for the market, incorporating actual market data as reported through 3Q22.

Companies Mentioned:

|

|

Table of Contents

- Summary

- Measurement a unique challenge in carrier-neutral market

- Top line market growth

- Overview of key companies

- Capex likely to exceed M&A in next 2 years, and tech component will rise

- Integrated business models also to pick up, with boost from PE sector

- Appendix

List of Figures and Tables

- Figure 1: CNNO revenues, capex and M&A spending, annualized, 1Q14-3Q22

- Figure 2: CNNO free cash flow margins, debt, and revenues per employee

- Table 1: Overview of key CNNOs - recent financial metrics and M&A activity

全球网路规模网路营运商市场分析(2023 年第四季):

全球网路规模网路营运商市场分析(2023 年第四季): 虚拟网路营运商市场- 按服务(行动虚拟网路营运商(MVNO)、固定虚拟网路营运商(FVNO))、按产品(预付费、后付费)、按最终用户(消费者、企业)、2024 - 2032 年预测

虚拟网路营运商市场- 按服务(行动虚拟网路营运商(MVNO)、固定虚拟网路营运商(FVNO))、按产品(预付费、后付费)、按最终用户(消费者、企业)、2024 - 2032 年预测 网路营运商预测(~2028 年):资本支出将在 2023 年下降后恢復,并在 2028 年增长至约 6500 亿美元,生成式人工智慧推动资本支出和员工人数减少

网路营运商预测(~2028 年):资本支出将在 2023 年下降后恢復,并在 2028 年增长至约 6500 亿美元,生成式人工智慧推动资本支出和员工人数减少 营运商中立者希望搭乘 GenAI 浪潮 - 2023 年 1 月更新:CNNO 收入预计在 2023 年达到 100B 美元,资本密集度 >35%,因为行业抓住生成式 AI 和 5G 緻密化的机会

营运商中立者希望搭乘 GenAI 浪潮 - 2023 年 1 月更新:CNNO 收入预计在 2023 年达到 100B 美元,资本密集度 >35%,因为行业抓住生成式 AI 和 5G 緻密化的机会 运营商中立部门的2022年的OPEX电费及燃料费对剧增:对许多运营商中立部门经营者来说电费及燃料费是最大的运营成本,占OPEX (ex-D&A) 的最大80%

运营商中立部门的2022年的OPEX电费及燃料费对剧增:对许多运营商中立部门经营者来说电费及燃料费是最大的运营成本,占OPEX (ex-D&A) 的最大80% 运营商中立网络运营商(CNNO):市场分析(2022 Q4)CNNO将在2022投资超过450亿美元,通过资本支出和併购进行扩张,以支持运营商领域快速云端增长降低成本

运营商中立网络运营商(CNNO):市场分析(2022 Q4)CNNO将在2022投资超过450亿美元,通过资本支出和併购进行扩张,以支持运营商领域快速云端增长降低成本 网路经营者的电力使用数量:2021年

网路经营者的电力使用数量:2021年 22年前半期运营商中立市场的资料中心投资飙升

22年前半期运营商中立市场的资料中心投资飙升