|

市场调查报告书

商品编码

1266271

运营商中立部门的2022年的OPEX电费及燃料费对剧增:对许多运营商中立部门经营者来说电费及燃料费是最大的运营成本,占OPEX (ex-D&A) 的最大80%Energy Costs Spike 2022 Opex for Carrier-neutral Sector: For Many Carrier-neutral Operators, Energy is Largest Operational Expense and Can Account for Up to 80% of Opex (ex-D&A), Costs Surged in 2022 for Many |

||||||

电费及燃料费,占基础设施专门的运营商中立的网路运营商工作业者 (CNNO) 的运营成本用的大部分,OPEX (ex-D&A) 的30%以上,电费及燃料费花费最大80%。

本报告提供手机讯号塔,资料中心,光纤网路业者的能源支出相关资料,其资料的意义和关于今后方向性的论述。

图表

调查对像

刊载企业

|

|

目录

- 摘要

- CNNO:比其他业者类型更能源密集型

- 网路的永续性:需要从CNNO开始

- 影响

- 附录

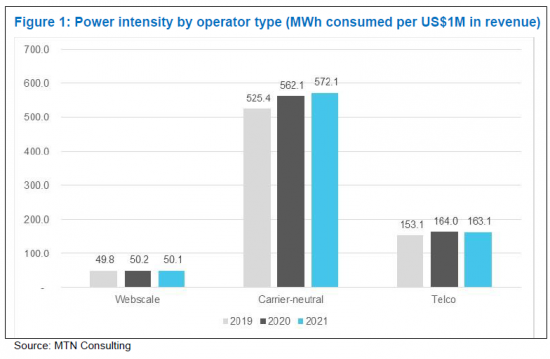

This brief presents data on energy spending by operators of cell towers, data centers, and fiber networks, and discusses the implications of the data and likely future directions. Utilities represent a large portion of operating expenses for these infrastructure-focused companies, which we track as "carrier-neutral network operators" (CNNOs). CNNOs also spend more than other types of operators. Webscale spending on power is miniscule relative to their size, less than 1% of opex (ex-D&A). Telcos spend a few % of opex (ex-D&A) on utilities. But CNNOs can spend more than 30% and up to 80% of opex (ex-D&A) on utilities.

VISUALS

Coverage

Companies mentioned:

|

|

Table of Contents

- Summary

- CNNOs are more energy-intensive than other operator types

- Sustainability in networks needs to start with CNNOs

- Implications

- Appendix

List of Figures

- Figure 1: Power intensity by operator type (MWh consumed per US$1M in revenue)

- Figure 2: Utilities spend as a % of opex (excluding depreciation & amortization), 2020-22

- Figure 3: Utilities vs. D&A costs as a percentage of total opex, 2022

关税情势如何影响美国再生能源成本

关税情势如何影响美国再生能源成本 关税情势对美国的再生能源成本带来的影响- 数据

关税情势对美国的再生能源成本带来的影响- 数据 通讯网路营运商市场回顾(2024年第三季):营收復苏,但持续的支出削减导致年度资本支出低于3,000亿美元大关

通讯网路营运商市场回顾(2024年第三季):营收復苏,但持续的支出削减导致年度资本支出低于3,000亿美元大关 网路营运商资本支出展望(2024 年第四季版):电信公司持平,但人工智慧驱动的生成式资料中心炒作将推动电信资本支出在 2024 年超过 6,000 亿美元,其中 Scalers 预计将引领市场

网路营运商资本支出展望(2024 年第四季版):电信公司持平,但人工智慧驱动的生成式资料中心炒作将推动电信资本支出在 2024 年超过 6,000 亿美元,其中 Scalers 预计将引领市场 网路营运商永续发展策略的全球市场:2024-2029

网路营运商永续发展策略的全球市场:2024-2029 Direct-to-Cell 全球市场:2024-2029

Direct-to-Cell 全球市场:2024-2029 Apps Run The World - 应用市场分析与买家洞察

Apps Run The World - 应用市场分析与买家洞察 虚拟网路营运商世界市场报告(2024 年)

虚拟网路营运商世界市场报告(2024 年) 营运商中立网路营运商(CNNO)-市场回顾(2023年第4季):

营运商中立网路营运商(CNNO)-市场回顾(2023年第4季): 虚拟网路营运商 (VNO) 的全球市场预测(截至 2030 年):按类型、目标客户、服务、技术、最终用户和地区进行分析

虚拟网路营运商 (VNO) 的全球市场预测(截至 2030 年):按类型、目标客户、服务、技术、最终用户和地区进行分析