|

市场调查报告书

商品编码

1740985

车辆到电网 (V2G) 技术市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Vehicle-to-Grid (V2G) Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

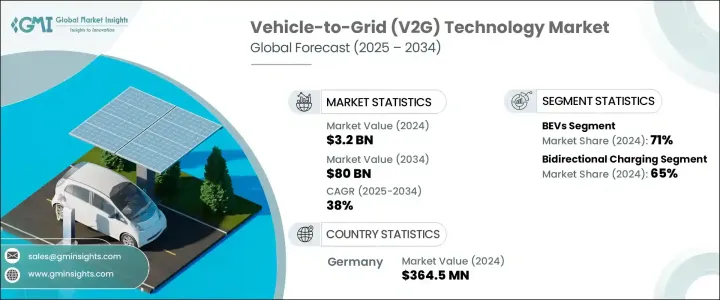

2024年,全球车辆到电网技术市场规模达32亿美元,预计2034年将以38%的复合年增长率成长,达到800亿美元。这得益于电动车的加速普及、智慧电网系统投资的不断增加以及全球气候目标对低碳基础设施的大力推动。随着全球转向更清洁的能源解决方案,V2G技术正成为未来能源格局的关键支柱。随着电动车成为主流,再生能源整合日益紧迫,V2G平台已成为实现能源弹性的关键推动因素。

汽车和能源产业的公司正在积极推动V2G系统的商业化,该系统能够支持尖峰负载管理、稳定电力供应并最大限度地减少对化石燃料的依赖。城镇化进程的加速、政府激励措施的出台、技术创新以及对储能解决方案日益增长的需求,为V2G网路的扩张创造了肥沃的土壤。分散式能源系统的趋势进一步增强了V2G在现代能源生态系统中的作用,为电动车车主、公用事业公司和技术供应商创造了新的收入来源。随着各国加强减少交通排放,V2G被视为协调国家能源议程与全球气候目标的关键策略。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 32亿美元 |

| 预测值 | 800亿美元 |

| 复合年增长率 | 38% |

各国政府正透过支持双向充电网络,使国家战略与国际气候目标保持一致,使电动车既能作为能源消费者,也能作为能源提供者与电网互动。公用事业公司利用电动车作为电网资产,管理再生能源的波动性,并缓解尖峰需求压力。在城市和工业区,支援V2G的电动车队越来越多地被用来在高需求时段取代传统电源。这些车辆透过释放储存的电能,有助于提高电网的弹性,从而最大限度地减少对化石燃料发电的依赖。技术供应商正在建立具有预测能源使用情况、即时电网通讯和能源交易等先进功能的平台,以促进价值创造。在一些地区,政府资金、激励措施和基础设施升级正在加速将标准电动车充电系统转换为支援V2G的系统。

2024年,纯电动车(BEV)占据了市场主导地位,占约71%的市场份额,预计其复合年增长率将达到38.3%。 BEV支援双向能量流动和零排放运行,使其与V2G系统高度相容。 BEV被广泛应用于商用车队和城市交通项目,包括公共交通和最后一英里配送。 BEV的普及率不断提高,加上相关政策的支持,正在提升其在V2G生态系统中的影响力。

车辆到电网 (V2G) 技术市场的双向充电部分在 2024 年占据 65% 的份额,预计到 2034 年将以 37.7% 的复合年增长率成长。这些充电器允许能量双向流动,使电动车不仅可以从电网充电,还可以在需要时返回电力。公用事业和车队营运商优先考虑这些系统,因为它们能够储存多余的再生能源并在需求高峰期间释放,从而优化电网效率并降低能源成本。

2024年,德国车辆到电网 (V2G) 技术市场占据39%的市场份额,产值达3.645亿美元。德国的领先地位源于其在汽车製造领域的深厚专业知识、广泛的电动车部署专案以及能够支持双向能源流动的发达电网。德国联邦政府支持能源转型和电气化的倡议,加上对电网现代化的大量投资,正在加速V2G基础设施的规模扩张。

全球主要汽车製造商和能源公司正在城市中心、工业园区和车队枢纽积极测试和部署V2G平台。全球车辆到电网 (V2G) 技术市场的主要参与者包括 ABB、三菱汽车、NRG Energy、电装、日立、AC Propulsion、日产汽车、Nuvve、本田汽车和 OVO Energy。为了扩大影响力,主要的 V2G 参与者正在大力投资研发更有效率、可扩展的双向充电技术。他们正在与汽车製造商和公用事业公司建立合作伙伴关係,以加速试点计画和大规模部署。许多公司专注于软体改进,包括电网优化、人工智慧驱动的负载管理和能源市场整合,以实现收益最大化。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 充电基础设施供应商

- 电网营运商

- V2G服务提供者

- 技术提供者

- 最终用途

- 川普政府关税的影响

- 贸易影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(客户成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 贸易影响

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 支持V2G部署的政府法规和财政激励措施

- 全球电动车的普及率不断提高

- 都市化和工业化进程加速

- V2G技术的持续进步

- 产业陷阱与挑战

- 升级现有充电基础设施的成本高昂

- 缺乏标准化的充电基础设施

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 纯电动车

- 插电式混合动力汽车

- 燃料电池汽车

第六章:市场估计与预测:按充电方式,2021 - 2034 年

- 主要趋势

- 单向充电

- 双向充电

第七章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 智慧电錶

- 电动车供电设备(EVSE)

- 家庭能源管理

- 软体解决方案

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 国内的

- 商业的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- ABB

- AC Propulsion

- Boulder Electric Vehicle

- Denso Corporation

- Edison International

- EnerDel

- Engie Group

- Fermata Energy

- Groupe Renault

- Hitachi

- Honda Motor

- Indra

- Mitsubishi Motors Corporation

- Nissan Motor Corporation

- NRG Energy

- Nuvve Corporation

- OVO Energy

- PG&E Corporation

- Toyota Shokki

- Wallbox

The Global Vehicle-To-Grid Technology Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 38% to reach USD 80 billion by 2034, driven by the accelerating adoption of electric vehicles, rising investment in smart grid systems, and global climate goals pushing for low-carbon infrastructure. As the world moves toward cleaner energy solutions, V2G technologies are becoming a key pillar of the future energy landscape. With electric vehicles becoming mainstream and renewable energy integration gaining urgency, V2G platforms are positioned as critical enablers of energy flexibility.

Companies across the automotive and energy sectors are working aggressively to commercialize V2G systems that can support peak load management, stabilize power supplies, and minimize dependence on fossil fuels. Growing urbanization, government incentives, technological innovations, and the increasing need for energy storage solutions are creating a fertile environment for the expansion of V2G networks. The trend toward decentralized energy systems is further amplifying the role of V2G in modern energy ecosystems, creating new revenue streams for EV owners, utilities, and technology providers alike. As countries intensify efforts to cut transportation emissions, V2G is seen as a key strategy for aligning national energy agendas with global climate targets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $80 Billion |

| CAGR | 38% |

Governments are aligning national strategies with international climate goals by supporting bidirectional charging networks, allowing EVs to interact with the grid as both energy consumers and energy providers. Utilities leverage EVs as grid assets to manage renewable energy variability and ease peak demand pressures. V2G-enabled EV fleets are increasingly used in cities and industrial areas to replace conventional power sources during high-demand periods. These vehicles contribute to grid resilience by discharging stored electricity, which minimizes reliance on fossil-fueled generation. Technology providers are building platforms with advanced features like predictive energy usage, real-time grid communication, and energy trading capabilities to boost value creation. In several regions, government funding, incentives, and infrastructure upgrades are accelerating the conversion of standard EV charging systems into V2G-capable ones.

Battery electric vehicles (BEVs) dominated the market by vehicle type in 2024, capturing about 71% share, and are forecasted to maintain their lead with a CAGR of 38.3%. Their ability to support bidirectional energy flows and zero-emission operation makes them highly compatible with V2G systems. BEVs are widely integrated into commercial fleets and urban mobility programs, including public transportation and last-mile delivery. Their expanding availability, coupled with supportive policies, is boosting their presence in the V2G ecosystem.

The bidirectional charging segment in the vehicle-to-grid (V2G) technology market held a 65% share in 2024 and is expected to grow at a CAGR of 37.7% through 2034. These chargers allow energy to move in both directions, enabling EVs to not only charge from the grid but also return power when needed. Utilities and fleet operators prioritize these systems for their ability to store surplus renewable energy and release it during demand peaks, optimizing grid efficiency and reducing energy costs.

The Germany Vehicle-To-Grid (V2G) Technology Market held a 39% share in 2024, generating USD 364.5 million. The country's leadership stems from its deep-rooted expertise in automotive manufacturing, extensive EV deployment programs, and a well-developed electric grid capable of supporting bidirectional energy flow. Germany's federal initiatives supporting energy transition and electrification, combined with significant investments in grid modernization, are accelerating the scale-up of V2G infrastructure.

Major automakers and energy companies worldwide are actively testing and implementing V2G platforms in urban centers, industrial zones, and fleet hubs. Key players in the Global Vehicle-To-Grid (V2G) Technology Market include ABB, Mitsubishi Motors, NRG Energy, Denso, Hitachi, AC Propulsion, Nissan Motor, Nuvve, Honda Motor, and OVO Energy. To strengthen their footprint, major V2G players are investing heavily in RandD to develop more efficient and scalable bidirectional charging technologies. They are forming partnerships with automotive manufacturers and utility companies to accelerate pilot projects and large-scale deployments. Many firms focus on software advancements, including grid optimization, AI-driven load management, and energy market integration to maximize returns.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Charging infrastructure providers

- 3.2.2 Grid operators

- 3.2.3 V2G service providers

- 3.2.4 Technology providers

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Supportive government regulations and financial incentives for V2G deployment

- 3.9.1.2 Growing adoption of electric vehicles across the globe

- 3.9.1.3 Rising urbanization and industrialization

- 3.9.1.4 Ongoing technological advancements in V2G technology

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost associated with upgrading existing charging infrastructure

- 3.9.2.2 Lack of standardized charging infrastructure

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 BEVs

- 5.3 PHEVs

- 5.4 FCVs

Chapter 6 Market Estimates & Forecast, By Charging, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Unidirectional charging

- 6.3 Bidirectional charging

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Smart meters

- 7.3 Electric vehicle supply equipment (EVSE)

- 7.4 Home energy management

- 7.5 Software solutions

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Domestic

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 AC Propulsion

- 10.3 Boulder Electric Vehicle

- 10.4 Denso Corporation

- 10.5 Edison International

- 10.6 EnerDel

- 10.7 Engie Group

- 10.8 Fermata Energy

- 10.9 Groupe Renault

- 10.10 Hitachi

- 10.11 Honda Motor

- 10.12 Indra

- 10.13 Mitsubishi Motors Corporation

- 10.14 Nissan Motor Corporation

- 10.15 NRG Energy

- 10.16 Nuvve Corporation

- 10.17 OVO Energy

- 10.18 PG&E Corporation

- 10.19 Toyota Shokki

- 10.20 Wallbox

2026年全球V2G(车辆到电网)技术市场报告

2026年全球V2G(车辆到电网)技术市场报告 车网互动(V2G)市场:依组件、技术(双向充电、单向充电)、应用和最终用户划分-全球预测至2036年

车网互动(V2G)市场:依组件、技术(双向充电、单向充电)、应用和最终用户划分-全球预测至2036年 全球V2G(车辆到电网)市场:按组件、车辆类型、应用、充电方式、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测全球车网互动(V2G)市场:按车辆类型、解决方案、应用、最终用户和地区划分 - 市场规模、行业趋势、机会分析和预测(2026-2035 年)Vehicle-to-Grid(V2G)的全球市场:车辆类型,解决方案,用途,各地区 - 市场规模,产业趋势,机会分析,预测(2025年~2033年)

全球V2G(车辆到电网)市场:按组件、车辆类型、应用、充电方式、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测全球车网互动(V2G)市场:按车辆类型、解决方案、应用、最终用户和地区划分 - 市场规模、行业趋势、机会分析和预测(2026-2035 年)Vehicle-to-Grid(V2G)的全球市场:车辆类型,解决方案,用途,各地区 - 市场规模,产业趋势,机会分析,预测(2025年~2033年) 全球车辆到电网 (V2G) 市场:预测至 2032 年 - 按组件、充电类型、车辆类型、功率输出、技术、最终用户和地区进行分析

全球车辆到电网 (V2G) 市场:预测至 2032 年 - 按组件、充电类型、车辆类型、功率输出、技术、最终用户和地区进行分析 2025 年至 2033 年车辆到电网市场规模、份额、趋势及预测(按解决方案类型、车辆类型、充电类型、应用和地区)

2025 年至 2033 年车辆到电网市场规模、份额、趋势及预测(按解决方案类型、车辆类型、充电类型、应用和地区) V2G(车辆到电网):全球市场

V2G(车辆到电网):全球市场 车辆到电网市场-全球产业规模、份额、趋势、机会和预测,按组件、技术、最终用途产业、地区和竞争细分,2020-2030 年预测车辆到电网 (V2G) 技术市场预测(至 2032 年):按类型、车辆类型、充电基础设施、组件、应用、最终用户和地区进行的全球分析

车辆到电网市场-全球产业规模、份额、趋势、机会和预测,按组件、技术、最终用途产业、地区和竞争细分,2020-2030 年预测车辆到电网 (V2G) 技术市场预测(至 2032 年):按类型、车辆类型、充电基础设施、组件、应用、最终用户和地区进行的全球分析