|

市场调查报告书

商品编码

1773385

宠物补品市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Pet Supplement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

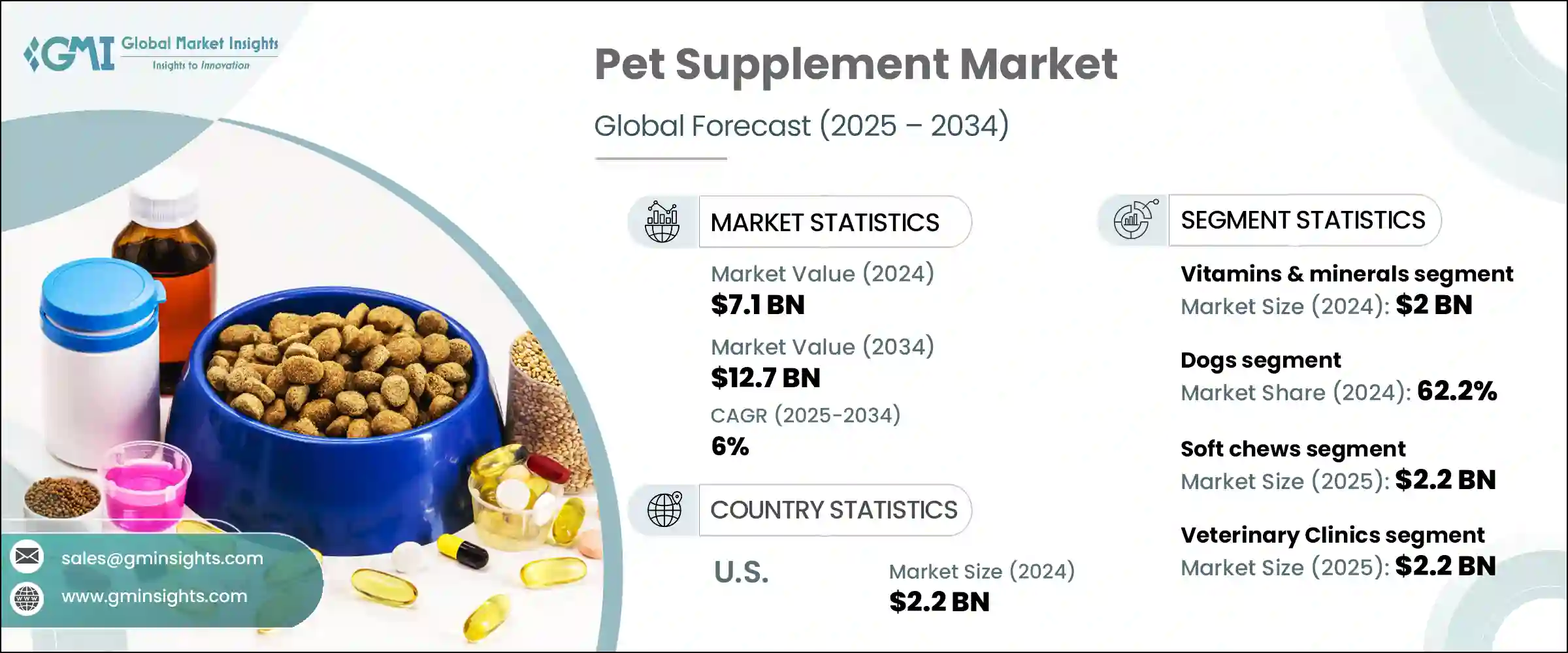

2024年,全球宠物补充剂市场规模达71亿美元,预计2034年将以6%的复合年增长率成长,达到127亿美元。这种需求的稳定成长与宠物主人不断变化的观念息息相关,他们越来越像对待家人一样对待宠物。消费者对预防性护理和健康的日益关注推动着市场的发展,他们寻求能够增强关节灵活性、免疫功能、消化功能、皮肤和毛髮健康的解决方案。这一趋势在城市环境中尤其明显,因为室内宠物需要营养护理。随着人们对特殊配方和健康益处的认识不断提高,符合宠物不同生命阶段、品种和特定健康需求的功能性宠物补充剂也越来越受欢迎。

随着宠物主人养犬数量的增加和生活方式的改变,对犬类补充剂的需求持续增长。同样,随着越来越多的家庭投资于为猫咪伴侣量身定制的护理,人们对猫咪健康产品的兴趣也在增长。富含多种维生素、益生菌、植物萃取物和欧米伽脂肪酸的补充剂,尤其是那些声称有机、非基因改造和无麸质的补充剂,正受到强烈追捧。宠物主人正在转向宠物年龄或品种的客製化解决方案,以改善其在各个生命阶段的生活品质。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 71亿美元 |

| 预测值 | 127亿美元 |

| 复合年增长率 | 6% |

2024年,维生素和矿物质细分市场贡献了可观的收入份额,价值达20亿美元。此细分市场涵盖B群维生素、钙和铁等必需营养素,以及富含葡萄糖胺、MSM、透明质酸和软骨素等广受欢迎的关节保健品。消化产品也蓬勃发展,尤其是那些透过益生元和益生菌来支持肠道菌丛的产品,这反映出消费者对内在健康认知的转变。

2024年,犬类保健品市占率达62.2%,预计2025-2034年复合年增长率为5.7%。随着北美和欧洲犬类饲养量的不断增长,对针对特定犬种配方的需求也日益增长。大型犬通常需要补充剂来维持活动能力和心血管功能,而小型犬则更适合补充皮肤、毛髮和镇静成分。随着宠物饲养量的不断增长以及家庭饲养多隻宠物,各大品牌纷纷推出差异化产品,以满足不同的健康需求。

2024年,美国宠物补充剂市场产值达22亿美元。在美国,宠物补充剂受动物食品法规的监管,製造商必须遵守美国兽医中心(CVM)根据21 CFR 507制定的指南。这些法规要求严格遵守标籤、成分定义、安全测试和现行良好生产规范(CGMP)等相关规定。 FDA与美国饲料管理协会(AAFCO)密切合作,确保各州标准统一。只有被归类为「公认安全」(GRAS)或透过食品添加剂申请核准的成分才允许用于宠物补充剂。

塑造全球宠物补充品产业的关键参与者包括硕腾公司 (Zoetis Inc.)、Zesty Paws、Nutramax Laboratories、玛氏宠物照护 (Mars Petcare) 和雀巢普瑞纳宠物照护 (Nestle Purina PetCare)。宠物补充剂行业的领先公司正在利用科学配方、监管透明度和数位化互动来巩固其市场地位。一项关键策略包括推出针对特定品种和年龄的产品线,旨在解决宠物各阶段常见的健康问题。各品牌也着重于清洁标籤生产,使用天然且可追溯的成分来满足消费者的偏好。对电商平台和订阅模式的投资可以提高客户留存率和访问量。与兽医和宠物健康影响者的合作可以提升信誉和知名度。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- Pestel 分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计资料(HS 编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 年至 2034 年

- 主要趋势

- 维生素和矿物质

- 复合维生素

- 维生素A

- 维生素D

- 维生素E

- B群维生素

- 钙

- 铁

- 其他矿物

- 关节健康补充品

- 葡萄糖胺

- 软骨素

- MSM(甲基磺酰甲烷)

- 玻尿酸

- 其他关节健康成分

- 消化健康补充剂

- 益生菌

- 益生元

- 消化酵素

- 纤维补充剂

- 皮肤和毛髮补充剂

- Omega-3脂肪酸

- Omega-6脂肪酸

- 生物素

- 锌

- 免疫支持补充剂

- 抗氧化剂

- 免疫增强剂

- 镇静和缓解焦虑的补充剂

- CBD补充剂

- 天然镇静剂

- 其他补充剂

- 心臟健康

- 肝臟支持

- 肾臟支持

- 认知健康

第六章:市场估计与预测:依宠物类型 2021 – 2034

- 主要趋势

- 狗

- 小的

- 中等的

- 大的

- 猫

- 室内猫

- 户外猫

- 鸟类

- 鱼

- 小动物

- 兔子

- 天竺鼠

- 仓鼠

- 其他小动物

- 爬虫类

- 其他的

第七章:市场估计与预测:依形式,2021 年至 2034 年

- 主要趋势

- 平板电脑

- 咀嚼片

- 普通平板电脑

- 软咀嚼物

- 粉末

- 液体

- 液滴

- 液体悬浮液

- 胶囊

- 点心

- 其他的

- 凝胶

- 喷雾剂

- 局部应用

第八章:市场估计与预测:按配销通路2021 – 2034

- 主要趋势

- 兽医诊所

- 宠物专卖店

- 网路零售

- 电子商务平台

- 直接面向消费者的网站

- 超市和大卖场

- 药局

- 其他的

- 农场和饲料商店

- 美容沙龙

- 宠物旅馆及寄宿

第九章:市场估计与预测:按年龄组,2021 年至 2034 年

- 主要趋势

- 小狗/小猫

- 成人

- 进阶的

第十章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- MEA 其余地区

第 11 章:公司简介

- Animal Essentials

- Ark Naturals

- Bayer Animal Health

- Boehringer Ingelheim Animal Health

- Ceva Sante Animale

- Dechra Pharmaceuticals

- Elanco Animal Health

- Hill's Pet Nutrition (Colgate-Palmolive)

- Innovet Pet Products

- Mars Petcare

- Nestle Purina PetCare

- NOW Foods (NOW Pets)

- Nutramax Laboratories

- Pet Naturals of Vermont

- PetHonesty

- Vetoquinol

- VetriScience Laboratories

- Virbac

- Zesty Paws

- Zoetis Inc.

The Global Pet Supplement Market was valued at USD 7.1 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 12.7 billion by 2034. This steady rise in demand is closely tied to the evolving mindset of pet owners who increasingly treat their pets like family members. The growing focus on preventative care and wellness is driving the market forward, as consumers seek solutions that support joint flexibility, immune function, digestion, skin, and coat health. This trend is particularly evident in urban settings, where indoor pets require nutritional care. Rising awareness of specialized formulations and health benefits has led to the growing popularity of functional pet supplements that match pets' life stages, breeds, and specific health needs.

Demand for dog supplements continues to expand in line with rising dog ownership and active lifestyle choices among pet owners. Likewise, interest in cat health products is climbing, as more households are investing in tailored care for feline companions. Supplements featuring multivitamins, probiotics, botanical extracts, and omega fatty acids-especially those carrying organic, non-GMO, and gluten-free claims-are seeing strong traction. Pet owners are turning to customized solutions with age- or breed-specific functions that improve the quality of life for their pets through every life stage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.1 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 6% |

In 2024, vitamins and minerals segment contributed a notable portion of revenue, valued at USD 2 billion. This segment includes essential nutrients like B-complex vitamins, calcium, and iron, along with popular joint health supplements that feature glucosamine, MSM, hyaluronic acid, and chondroitin. Digestive products are also thriving, particularly those that support the gut microbiome with prebiotics and probiotics, reflecting a shift in consumer understanding about internal wellness.

Dogs segment held 62.2% share in 2024 and is projected to grow at a CAGR of 5.7% during 2025-2034. With high dog ownership in North America and Europe, the demand for species-specific formulations is rising. Larger dogs often require supplements for mobility and cardiovascular support, while smaller breeds tend to benefit more from skin, coat, and calming formulations. As pet ownership expands and households adopt multiple pets, brands are working on differentiated offerings to meet various health demands.

U.S. Pet Supplement Market generated USD 2.2 billion in 2024. In the United States, pet supplements fall under animal food regulations, and manufacturers are required to follow the FDA's Center for Veterinary Medicine (CVM) guidelines under 21 CFR 507. These regulations enforce strict compliance related to labeling, ingredient definition, safety testing, and current good manufacturing practices (CGMPs). The FDA works closely with the Association of American Feed Control Officials (AAFCO) to ensure uniform standards across state lines. Only ingredients classified as Generally Recognized as Safe (GRAS) or approved through a food additive petition are permitted for use in pet supplements.

Key players shaping the Global Pet Supplement Industry include Zoetis Inc., Zesty Paws, Nutramax Laboratories, Mars Petcare, and Nestle Purina PetCare. Leading companies in the pet supplement industry are leveraging science-backed formulations, regulatory transparency, and digital engagement to strengthen their foothold. A key approach includes the launch of breed- and age-specific product lines designed to address common pet health issues at every stage. Brands are also focusing on clean-label production, using natural and traceable ingredients to align with consumer preferences. Investment in e-commerce platforms and subscription models enhances customer retention and access. Collaborations with veterinarians and pet wellness influencers drive credibility and awareness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Pet type

- 2.2.4 Form

- 2.2.5 Distribution channel

- 2.2.6 Age group

- 2.3 TAM analysis, 2025-2034

- 2.4 Cxo perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste Reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Vitamins & minerals

- 5.2.1 Multivitamins

- 5.2.2 Vitamin A

- 5.2.3 Vitamin D

- 5.2.4 Vitamin E

- 5.2.5 B- Complex vitamins

- 5.2.6 Calcium

- 5.2.7 Iron

- 5.2.8 Other minerals

- 5.3 Joint health supplements

- 5.3.1 Glucosamine

- 5.3.2 Chondroitin

- 5.3.3 MSM (methylsulfonylmethane)

- 5.3.4 Hyaluronic acid

- 5.3.5 Other joint health ingredients

- 5.4 Digestive health supplements

- 5.4.1 Probiotics

- 5.4.2 Prebiotics

- 5.4.3 Digestive enzymes

- 5.4.4 Fiber supplements

- 5.5 Skin & coat supplements

- 5.5.1 Omega-3 fatty acids

- 5.5.2 Omega-6 fatty acids

- 5.5.3 Biotin

- 5.5.4 Zinc

- 5.5.5 Immune support supplements

- 5.5.6 Antioxidants

- 5.5.7 Immune boosters

- 5.6 Calming & anxiety supplements

- 5.6.1 Cbd-based supplements

- 5.6.2 Natural calming agents

- 5.7 Other supplements

- 5.7.1 Heart health

- 5.7.2 Liver support

- 5.7.3 Kidney support

- 5.7.4 Cognitive health

Chapter 6 Market Estimates and Forecast, By Pet Type 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dogs

- 6.2.1 Small

- 6.2.2 Medium

- 6.2.3 Large

- 6.3 Cats

- 6.3.1 Indoor cats

- 6.3.2 Outdoor cats

- 6.4 Birds

- 6.5 Fish

- 6.6 Small animals

- 6.6.1 Rabbits

- 6.6.2 Guinea pigs

- 6.6.3 Hamsters

- 6.6.4 Other small animals

- 6.7 Reptiles

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Form, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Tablets

- 7.2.1 Chewable tablets

- 7.2.2 Regular tablets

- 7.3 Soft chews

- 7.4 Powders

- 7.5 Liquid

- 7.5.1 Liquid drops

- 7.5.2 Liquid suspensions

- 7.6 Capsules

- 7.7 Treats

- 7.8 Others

- 7.8.1 Gels

- 7.8.2 Sprays

- 7.8.3 Topical applications

Chapter 8 Market Estimates and Forecast, By Distribution Channel 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Veterinary clinics

- 8.3 Pet specialty stores

- 8.4 Online retail

- 8.4.1 E-commerce platforms

- 8.4.2 Direct-to-consumer websites

- 8.5 Supermarkets & hypermarkets

- 8.6 Pharmacies

- 8.7 Others

- 8.7.1 Farm & feed stores

- 8.7.2 Grooming salons

- 8.7.3 Pet hotels & boarding

Chapter 9 Market Estimates and Forecast, By Age Group, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Puppy/kitten

- 9.3 Adult

- 9.4 Senior

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Animal Essentials

- 11.2 Ark Naturals

- 11.3 Bayer Animal Health

- 11.4 Boehringer Ingelheim Animal Health

- 11.5 Ceva Sante Animale

- 11.6 Dechra Pharmaceuticals

- 11.7 Elanco Animal Health

- 11.8 Hill's Pet Nutrition (Colgate-Palmolive)

- 11.9 Innovet Pet Products

- 11.10 Mars Petcare

- 11.11 Nestle Purina PetCare

- 11.12 NOW Foods (NOW Pets)

- 11.13 Nutramax Laboratories

- 11.14 Pet Naturals of Vermont

- 11.15 PetHonesty

- 11.16 Vetoquinol

- 11.17 VetriScience Laboratories

- 11.18 Virbac

- 11.19 Zesty Paws

- 11.20 Zoetis Inc.

宠物营养补充品市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球宠物营养补充品市场规模、份额、趋势和成长分析报告(2026-2034年)

宠物营养补充品市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球宠物营养补充品市场规模、份额、趋势和成长分析报告(2026-2034年) 宠物草药补充剂市场-全球产业规模、份额、趋势、机会及预测(依产品类型、剂型、动物类型、通路、地区及竞争格局划分,2021-2031年)

宠物草药补充剂市场-全球产业规模、份额、趋势、机会及预测(依产品类型、剂型、动物类型、通路、地区及竞争格局划分,2021-2031年) 全球宠物活动及展览服务市场预测(至2032年):依活动类型、服务类型、宠物类型、收入模式、最终用户及地区划分

全球宠物活动及展览服务市场预测(至2032年):依活动类型、服务类型、宠物类型、收入模式、最终用户及地区划分 日本宠物营养品市场报告(按宠物类型、配销通路、来源、应用和地区划分,2026-2034年)

日本宠物营养品市场报告(按宠物类型、配销通路、来源、应用和地区划分,2026-2034年) 宠物营养补充品市场规模、份额和成长分析(按类型、宠物类型、剂型、应用、通路和地区划分)-2026-2033年产业预测2032 年宠物补充品和预防保健市场预测:按产品、动物类型、形态、预防保健类型、分销管道和地区进行的全球分析

宠物营养补充品市场规模、份额和成长分析(按类型、宠物类型、剂型、应用、通路和地区划分)-2026-2033年产业预测2032 年宠物补充品和预防保健市场预测:按产品、动物类型、形态、预防保健类型、分销管道和地区进行的全球分析 宠物用药草补充品市场,规模,占有率,趋势,产业分析报告:各产品类型,各用途,动物类别,各剂型,各流通管道,各地区,2025年~2034年的市场预测宠物益生菌补充品市场预测至 2030 年:按形式、功能、销售管道和地区进行的全球分析

宠物用药草补充品市场,规模,占有率,趋势,产业分析报告:各产品类型,各用途,动物类别,各剂型,各流通管道,各地区,2025年~2034年的市场预测宠物益生菌补充品市场预测至 2030 年:按形式、功能、销售管道和地区进行的全球分析 全球宠物补充品市场评估:依产品、依类型、依产品形式、依成分、依宠物类型、依应用、依价格范围、依最终用户、依分销渠道、依地区、机会、预测(2017) ~2031 )

全球宠物补充品市场评估:依产品、依类型、依产品形式、依成分、依宠物类型、依应用、依价格范围、依最终用户、依分销渠道、依地区、机会、预测(2017) ~2031 )