|

市场调查报告书

商品编码

1844305

汽车音频半导体市场机会、成长动力、产业趋势分析及2025-2034年预测Automotive Audio Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

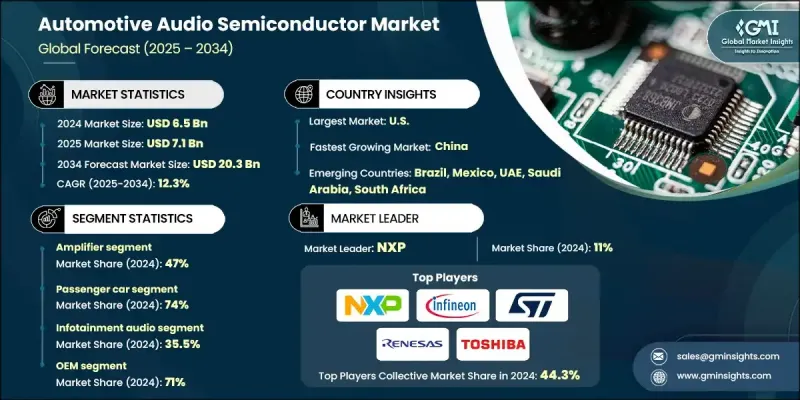

2024 年全球汽车音响半导体市场价值为 65 亿美元,预计将以 12.3% 的复合年增长率成长,到 2034 年达到 203 亿美元。

这一增长反映了汽车製造商对沉浸式用户体验的重视,对先进车载资讯娱乐系统的需求激增。现代消费者期待触控萤幕、语音互动和无缝音讯连接,半导体在支援高保真音讯处理和高效多通道设定方面发挥关键作用。随着电动和混合动力车强调座舱舒适性和先进的电子功能,对专用半导体的需求日益增长,以满足性能、能源效率和低噪音的标准。语音命令系统和人工智慧驱动的资讯娱乐平台也依赖先进的音讯晶片来解读命令并增强即时音质。向互联互动座舱环境的转变正直接影响所有汽车领域半导体整合度的提升。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 65亿美元 |

| 预测值 | 203亿美元 |

| 复合年增长率 | 12.3% |

2024年,扩大机市场占据47%的市场份额,预计到2034年将以13%的复合年增长率成长。先进的D类放大器正被广泛整合到汽车音频架构中,支援多声道音频,最大程度降低失真,同时优化功率效率。这一趋势主要源自于消费者对更高音效体验的需求,尤其是在中高阶汽车领域。

乘用车市场在2024年占了74%的市场份额,预计在2025年至2034年期间的复合年增长率将达到12.9%。该领域资讯娱乐技术(包括语音识别、音讯串流和互动式显示器)的日益普及,显着增加了对整合式半导体解决方案(例如功率放大器、DSP和连接晶片)的需求。如今,即使在入门级车型中,增强型音响功能也必不可少,这进一步增强了整个乘用车类别对音频半导体的需求。

美国汽车音频半导体市场占了90%的市场份额,2024年市场规模达16亿美元。美国在高端和豪华汽车的销售方面依然保持全球领先地位,而高端品牌音响系统是这些汽车的必备配置。这些汽车需要先进的半导体来实现环绕声处理、讯号调节和放大器性能。随着汽车製造商努力透过沉浸式音讯体验实现差异化,美国在汽车音讯晶片技术的采用和开发方面继续保持领先地位。

汽车音频半导体市场的主要参与者包括英飞凌科技、罗姆半导体、恩智浦半导体、亚德诺半导体、意法半导体、安森美半导体、高通、东芝电子装置公司、德州仪器和瑞萨电子。为了在竞争激烈的汽车音响半导体市场中保持强势地位,领先的公司正在大力投资下一代音讯技术,包括智慧放大器和整合人工智慧的DSP。各公司正专注于节能晶片设计,以满足电动车的需求,同时提高声学性能。与汽车原始设备製造商的策略联盟有助于加速产品的采用,而研发工作则致力于开发支援高级连接和语音介面的紧凑型多功能晶片。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 沉浸式车用音响的需求日益增长

- 电动车普及率不断提高

- 人工智慧与语音助理的整合

- 转向连网和软体定义的汽车

- 与音响品牌的优质OEM合作

- 产业陷阱与挑战

- 研发生产成本高

- 半导体供应链波动

- 严格的汽车可靠性标准

- 科技变革的快速步伐

- 市场机会

- 亚太地区电动车和混合动力汽车产量不断成长

- 采用主动降噪(ANC)技术

- 云端连线资讯娱乐系统

- 新兴市场高级汽车保有量的扩大

- 晶片製造商与一级原始设备製造商之间的合作

- 成长动力

- 成长潜力分析

- 主要市场趋势和中断

- 未来市场趋势

- 监管格局

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利分析

- 价格趋势

- 按地区

- 按产品

- 成本分解分析

- 生产统计

- 生产中心

- 进出口

- 主要进口国家

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

- 投资格局分析

- 半导体研发投资

- 汽车音响技术融资

- 音频创新领域的创投

- 企业投资模式

- 政府研究经费

- 音频半导体领域的併购活动

- 汽车音讯架构的演变

- ADAS 音讯集成

- 多区域和个性化音频系统

- 软体定义汽车 (SDV) 的影响

- 音讯品质和性能基准化分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依组件划分,2021 - 2034 年

- 主要趋势

- 扩大机

- 数位讯号处理器

- 麦克风

- 调谐器

第六章:市场估计与预测:以推进方式,2021 - 2034 年

- 主要趋势

- 汽油

- 柴油引擎

- 全电动

- 油电混合车

- 插电式混合动力

- 燃料电池电动车

第七章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 资讯娱乐音讯

- 车内语音

- 主动降噪

- ADAS 音讯提示

- 远端资讯处理和呼叫音讯

- 其他的

第 8 章:市场估计与预测:按安装量,2021 年至 2034 年

- 主要趋势

- OEM

- 售后市场

第九章:市场估计与预测:依车型,2021 - 2034

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车

- 轻型

- 中型

- 重负

第 10 章:市场估计与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- 全球参与者

- Analog Devices

- Cirrus Logic

- Infineon Technologies

- NXP

- ON Semiconductor

- Qualcomm

- Renesas Electronics

- ROHM Semiconductor

- STMicroelectronics

- Texas Instruments

- Toshiba Electronic Devices

- Regional Champions

- MediaTek

- Realtek

- ESS Technology

- Synaptics

- Dialog Semiconductor

- Wolfson Microelectronics

- AKM Semiconductor

- Yamaha

- Nuvoton Technology

- Silicon Labs

- 新兴企业和服务提供者

- Cadence Design Systems

- CEVA

- Dolby Laboratories

- DSP Group

- DTS

- Fortemedia

- Imagination Technologies

- Knowles

- Tempo Semiconductor

- Waves Audio

The Global Automotive Audio Semiconductor Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 12.3% to reach USD 20.3 billion by 2034.

This growth reflects the surge in demand for advanced in-vehicle infotainment systems, as automakers prioritize immersive user experiences. With modern consumers expecting touchscreens, voice interaction, and seamless audio connectivity, semiconductors play a key role in powering high-fidelity sound processing and efficient multi-channel setups. As electric and hybrid vehicles emphasize cabin comfort and advanced electronic features, specialized semiconductors are increasingly required to meet performance, energy efficiency, and low-noise standards. Voice-command systems and AI-driven infotainment platforms also rely on sophisticated audio chips to interpret commands and enhance real-time sound quality. The shift toward connected, interactive cabin environments is directly influencing the rise in semiconductor integration across all vehicle segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 12.3% |

In 2024, the amplifiers segment held a 47% share and is forecast to grow at a CAGR of 13% through 2034. Advanced Class-D amplifiers are being widely integrated into vehicle audio architectures, supporting multi-channel audio with minimal distortion while optimizing power efficiency. This trend is primarily driven by consumer demand for elevated sound experiences, particularly in mid-range and high-end vehicle segments.

The passenger cars segment held a 74% share in 2024 and is anticipated to grow at a CAGR of 12.9% between 2025 and 2034. The rising use of infotainment technologies in this segment, including voice recognition, audio streaming, and interactive displays, has significantly increased the need for integrated semiconductor solutions like power amplifiers, DSPs, and connectivity chips. Enhanced sound features are now essential even in entry-level models, reinforcing the demand for audio-focused semiconductors throughout the passenger vehicle category.

US Automotive Audio Semiconductor Market held a 90% share and generated USD 1.6 billion in 2024. The country remains a global leader in the sale of premium and luxury vehicles, where high-end branded sound systems are essential features. These vehicles require advanced semiconductors for surround sound processing, signal conditioning, and amplifier performance. As carmakers strive to differentiate with immersive audio experiences, the US continues to lead in the adoption and development of automotive audio chip technologies.

Key players in the Automotive Audio Semiconductor Market include Infineon Technologies, ROHM Semiconductor, NXP, Analog Devices, STMicroelectronics, ON Semiconductor, Qualcomm, Toshiba Electronic Devices, Texas Instruments, and Renesas Electronics. To maintain a strong position in the competitive automotive audio semiconductor market, leading companies are investing heavily in next-gen audio technologies, including smart amplifiers and AI-integrated DSPs. Firms are focusing on energy-efficient chip designs that meet the demands of electric vehicles while enhancing acoustic performance. Strategic alliances with automotive OEMs help accelerate product adoption, while R&D efforts are geared toward developing compact, multifunctional chips that support advanced connectivity and voice interfaces.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 Installation

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for immersive in-car audio

- 3.2.1.2 Increasing EV adoption

- 3.2.1.3 Integration of AI and voice assistants

- 3.2.1.4 Shift toward connected and software-defined vehicles

- 3.2.1.5 Premium OEM collaborations with audio brands

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High R&D and production costs

- 3.2.2.2 Semiconductor supply chain volatility

- 3.2.2.3 Stringent automotive reliability standards

- 3.2.2.4 Rapid pace of tech change

- 3.2.3 Market opportunities

- 3.2.3.1 Growing EV and hybrid production in APAC

- 3.2.3.2 Adoption of active noise cancellation (ANC)

- 3.2.3.3 Cloud-connected infotainment systems

- 3.2.3.4 Expansion of premium car ownership in emerging markets

- 3.2.3.5 Collaboration between chipmakers and Tier-1 OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent analysis

- 3.11 Price trends

- 3.11.1 By region

- 3.11.2 By product

- 3.12 Cost breakdown analysis

- 3.13 Production statistics

- 3.13.1 Production hubs

- 3.13.2 Import and export

- 3.13.3 Major import countries

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Investment Landscape Analysis

- 3.15.1 Semiconductor R&D Investment

- 3.15.2 Automotive Audio Technology Funding

- 3.15.3 Venture Capital in Audio Innovation

- 3.15.4 Corporate Investment Patterns

- 3.15.5 Government Research Funding

- 3.15.6 M&A Activity in Audio Semiconductors

- 3.16 Automotive Audio Architecture Evolution

- 3.17 ADAS Audio Integration

- 3.18 Multi-Zone and Personalized Audio Systems

- 3.19 Software-Defined Vehicle (SDV) Impact

- 3.20 Audio Quality and Performance Benchmarking

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn) (Units)

- 5.1 Key trends

- 5.2 Amplifier

- 5.3 DSP

- 5.4 Microphone

- 5.5 Tuner

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn) (Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 All-electric

- 6.5 HEV

- 6.6 PHEV

- 6.7 FCEV

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn) (Units)

- 7.1 Key trends

- 7.2 Infotainment audio

- 7.3 In-car Voice

- 7.4 Active noise cancellation

- 7.5 ADAS audio cues

- 7.6 Telematics & call audio

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Installation, 2021 - 2034 ($Bn) (Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn) (Units)

- 9.1 Key trends

- 9.2 Passenger car

- 9.2.1 Hatchback

- 9.2.2 Sedan

- 9.2.3 SUV

- 9.3 Commercial Vehicle

- 9.3.1 Light duty

- 9.3.2 Medium duty

- 9.3.3 Heavy-duty

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 ($Bn) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Analog Devices

- 11.1.2 Cirrus Logic

- 11.1.3 Infineon Technologies

- 11.1.4 NXP

- 11.1.5 ON Semiconductor

- 11.1.6 Qualcomm

- 11.1.7 Renesas Electronics

- 11.1.8 ROHM Semiconductor

- 11.1.9 STMicroelectronics

- 11.1.10 Texas Instruments

- 11.1.11 Toshiba Electronic Devices

- 11.2 Regional Champions

- 11.2.1 MediaTek

- 11.2.2 Realtek

- 11.2.3 ESS Technology

- 11.2.4 Synaptics

- 11.2.5 Dialog Semiconductor

- 11.2.6 Wolfson Microelectronics

- 11.2.7 AKM Semiconductor

- 11.2.8 Yamaha

- 11.2.9 Nuvoton Technology

- 11.2.10 Silicon Labs

- 11.3 Emerging Players & Service Providers

- 11.3.1 Cadence Design Systems

- 11.3.2 CEVA

- 11.3.3 Dolby Laboratories

- 11.3.4 DSP Group

- 11.3.5 DTS

- 11.3.6 Fortemedia

- 11.3.7 Imagination Technologies

- 11.3.8 Knowles

- 11.3.9 Tempo Semiconductor

- 11.3.10 Waves Audio

汽车半导体市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、装置、最终使用者、功能及安装类型划分

汽车半导体市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、装置、最终使用者、功能及安装类型划分 2026年全球汽车半导体市场报告

2026年全球汽车半导体市场报告 汽车用碳化硅元件市场:2026-2032年全球预测(依元件类型、应用、额定电压和封装类型划分)汽车用碳化硅功率元件市场:2026-2032年全球预测(依元件类型、车辆型态、电压等级、额定功率、销售管道和应用划分)汽车用碳化硅功率模组市场:按车辆类型、配置、额定功率、冷却方式和应用划分,全球预测(2026-2032年)

汽车用碳化硅元件市场:2026-2032年全球预测(依元件类型、应用、额定电压和封装类型划分)汽车用碳化硅功率元件市场:2026-2032年全球预测(依元件类型、车辆型态、电压等级、额定功率、销售管道和应用划分)汽车用碳化硅功率模组市场:按车辆类型、配置、额定功率、冷却方式和应用划分,全球预测(2026-2032年) 汽车半导体市场:驱动智慧(2025)

汽车半导体市场:驱动智慧(2025) 乘用车半导体市场-全球产业规模、份额、趋势、机会和预测,按组件类型、应用类型、地区和竞争格局划分,2020-2030年预测

乘用车半导体市场-全球产业规模、份额、趋势、机会和预测,按组件类型、应用类型、地区和竞争格局划分,2020-2030年预测 汽车功率半导体及模组(SiC、GaN)产业(2025)

汽车功率半导体及模组(SiC、GaN)产业(2025) 汽车全像显示半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

汽车全像显示半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球汽车半导体市场按组件、车辆类型、动力系统、材料、应用和地区划分-预测至2030年

全球汽车半导体市场按组件、车辆类型、动力系统、材料、应用和地区划分-预测至2030年