|

市场调查报告书

商品编码

1636491

德国电动车电池电解:市场占有率分析、产业趋势、成长预测(2025-2030)Germany Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

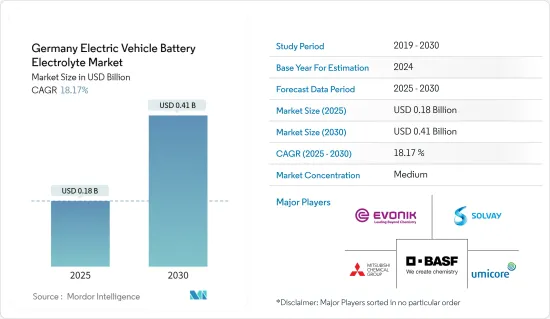

德国电动车电池电解市场规模预计2025年为1.8亿美元,2030年将达4.1亿美元,预测期间(2025-2030年)复合年增长率为18.17%。

主要亮点

- 从中期来看,预计全部区域电动车普及率的提高以及政府对电池製造的支持措施和投资将推动预测期内对德国电动车电池电解市场的需求。

- 另一方面,电解生产所用关键原料对其他国家的依赖预计将抑制德国电动车电池电解市场的成长。

- 电解配方的创新可提高电池性能、安全性和寿命,特别是高性能或远距电动车,将在不久的将来为德国电动车电池电解市场创造重大成长机会。

德国电动车电池电解市场趋势

锂离子电池预计将占较大份额

- 德国是欧洲领先的电动车 (EV) 市场。该国对电动车的承诺是由政府倡议推动的,包括补贴、税收优惠和严格的法规(例如减排目标)。随着持有中电动车数量的增加,对锂离子电池和对其功能至关重要的电解的需求也在增加。

- 此外,随着锂离子电池材料价格的下降,製造商正在增加对电动车电池生产的投资。产量的增加自然会增加对包括电解在内的基本电池组件的需求。

- 例如,2023年锂离子电池组的成本将比前一年下降14%,稳定在139美元/kWh。电池价格的下降将导致电动车价格更加实惠,从而刺激电动车的采用并增加电动车的市场占有率。这种不断增长的需求不仅是由电池组件(特别是电解质)消耗的增加所推动的,也是由旨在提高电池性能的技术进步所推动的。

- 此外,德国正积极努力缩小供应链缺口,旨在减少对锂离子电池进口材料(包括正极、负极和电解液)的依赖。随着电动车电池製造和锂生产方面雄心勃勃的投资计画正在进行,预计对锂离子电池组件(特别是电解)的需求将很大。

- 例如,2024年5月,Rock Tech Lithium Inc.获得批准在德国古本建立锂精製。该精製预计产能约为 24,000 吨氢氧化锂,这是电动车电池和能源储存系统的重要组成部分。

- 另一项倡议是,2024 年 2 月,汽车电池公司 (ACC) 筹集了 47 亿美元资金,在法国、德国和义大利建立三个锂离子电池超级工厂。 ACC预测,到2030年,锂离子电池产量将超过200万颗。此类战略投资预计将增加未来几年对锂离子电池电解的需求。

- 鑑于这些动态,锂离子电池电解细分市场预计在预测期内将大幅成长。

电池製造投资预计将推动市场

- 德国是大众、宝马和戴姆勒(梅赛德斯-奔驰)等汽车巨头的所在地,在电动车(EV)开发方面正在取得长足进步。这些製造商计划持有大部分车队提供电气化,因此对电动车电池及其基本电解的需求迅速增加。

- 为了加强对电动车领域的投资,德国政府正在推出一系列奖励和补贴。随着电动车销量持续上升,预计政府将宣布更多措施,进一步加强国内电池製造。国际能源总署的资料凸显了这个趋势。 2023年德国纯电动车(BEV)销量达到52万辆,较2022年的47万辆大幅成长。

- 同时,多家电池製造商正在德国伙伴关係生产不仅效率更高、整体性能也提高的电动车电池。这些进步的核心是先进的电池电解配方。这些尖端配方不仅可以延长电池寿命和安全性,还可以提高能量密度,在产业未来创新中发挥关键作用。

- 2024 年 5 月,着名电池製造商 VARTA主导了一个由 15 家公司和大学组成的联盟。此次合作以 ENTISE计划为中心,致力于利用钠离子技术的潜力,生产用于工业应用的高性能、环保电池。该联盟获得德国联邦研究和教育部约 750 万欧元的津贴,并计划在 2027 年中期完成计划的最后阶段。

- 随着产业转向提供更高能量密度和安全性的固态电池,电解要求预计会发生变化。近年来,企业之间达成了多项协议,凸显了业界为满足汽车领域固态电池快速成长的需求所做的努力。

- 例如,2024年7月,大众集团电池部门Powerco与QuantumScape签署协议,将QuantumScape开创性的固体锂金属电池技术推向业界尖端。这些合作关係不仅显示对固态电池的需求不断增长,也凸显了电动车电池生产中对电解稳定供应的需求。

- 考虑到此类新兴市场的发展和资本的涌入,旨在提高电动车电池产能的预期投资预计将重振市场。

德国电动汽车电池电解液产业概况

德国电动车电池电解市场温和。市场的主要企业包括(排名不分先后)赢创工业公司、BASF公司、索尔维公司、优美科公司和三菱化学集团公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车的扩张

- 政府对电池製造的支持措施和投资

- 抑制因素

- 电解生产中使用的关键原料对其他国家的依赖

- 促进因素

- 供应链分析

- PESTLE分析

- 投资分析

第五章市场区隔

- 电池类型

- 锂离子

- 铅酸

- 其他电池类型

- 电解质类型

- 液体电解质

- 凝胶电解质

- 固体电解质

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Evonik Industries AG

- BASF SE

- Solvay SA

- Mitsubishi Chemical Group.

- Umicore SA

- Targray Industries Inc.

- 3M Company

- NEI Corporation

- Cabot Corporation

- Samsung SDI

- 其他知名公司名单

- 市场排名分析

第七章 市场机会及未来趋势

- 电解液配方的创新

简介目录

Product Code: 50003760

The Germany Electric Vehicle Battery Electrolyte Market size is estimated at USD 0.18 billion in 2025, and is expected to reach USD 0.41 billion by 2030, at a CAGR of 18.17% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the growing adoption of electric vehicles and supportive government policies and investments towards battery manufacturing across the region are expected to drive the demand for the Germany electric vehicle battery electrolyte market during the forecast period.

- On the other hand, the dependence on other countries for key raw materials used in the production of electrolytes is expected to restrain the growth of the Germany electric vehicle battery electrolyte market.

- Nevertheless, the innovation in electrolyte formulations that improve battery performance, safety, and lifespan, particularly for high-performance or long-range EVs, creates significant growth opportunities in the Germany electric vehicle battery electrolyte market in the near future.

Germany Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery is Expected to Have a Major Share

- Germany stands as one of Europe's foremost markets for electric vehicles (EVs). The nation's push towards electric mobility is bolstered by government initiatives, including subsidies, tax incentives, and stringent regulations like emission reduction targets. As the fleet of EVs expands, so does the demand for lithium-ion batteries, and by extension, the electrolytes integral to their function.

- Moreover, as the prices of materials for lithium-ion batteries decline, manufacturers are ramping up investments in EV battery production. This uptick in production naturally amplifies the demand for essential battery components, notably electrolytes.

- For example, in 2023, the cost of lithium-ion battery packs saw a 14% drop from the previous year, settling at USD 139/kWh. This decline in battery prices translates to more affordable EVs, spurring adoption and expanding the market share for electric vehicles. Such heightened demand not only signals increased consumption of battery components, especially electrolytes but also propels technological advancements aimed at enhancing battery performance.

- Additionally, Germany is actively working to bridge supply chain gaps, aiming to lessen its dependence on imported materials for lithium-ion batteries, including cathodes, anodes, and electrolytes. With ambitious investment plans on the horizon for both EV battery manufacturing and lithium production, a pronounced demand for lithium-ion battery components, particularly electrolytes, is anticipated.

- For instance, in May 2024, Rock Tech Lithium Inc. secured approval to set up a lithium refinery in Guben, Germany. This refinery is projected to boast a capacity of approximately 24,000 tonnes of lithium-hydroxide, a crucial ingredient for electric car batteries and energy storage systems.

- In another move, February 2024 saw Automotive Cells Company (ACC) amass USD 4.7 billion in funding to establish three lithium-ion battery gigafactories spread across France, Germany, and Italy. ACC projects that by 2030, its production will exceed 2 million lithium-ion batteries. Such strategic investments are poised to amplify the demand for lithium-ion battery electrolytes in the coming years.

- Given these dynamics, the lithium-ion battery electrolyte segment is set for a significant upswing in the forecast period.

Investments Towards Battery Manufacturing is Expected to Drive the Market

- Germany, home to automotive titans like Volkswagen, BMW, and Daimler (Mercedes-Benz), is witnessing these giants make substantial strides in electric vehicle (EV) development. With plans to electrify a significant portion of their fleets, these manufacturers are fueling a burgeoning demand for EV batteries and their essential electrolytes.

- To bolster investments in the EV sector, the German government has rolled out a suite of incentives and subsidies. As electric vehicle sales continue to rise, it's anticipated that the government will unveil additional policies to further bolster domestic battery manufacturing. Data from the International Energy Agency highlights this trend: in 2023, Germany's battery electric vehicle (BEV) sales reached 0.52 million units, a notable increase from 0.47 million in 2022.

- In tandem, several battery manufacturers are forging partnerships in Germany, aiming to produce EV batteries that are not only more efficient but also enhance overall performance. At the heart of these advancements are advanced battery electrolyte formulations. These cutting-edge formulations not only extend battery life and safety but also elevate energy density, marking them as key players in the industry's future innovations.

- Highlighting the collaborative spirit, in May 2024, VARTA, a prominent battery manufacturer, spearheaded a consortium of 15 companies and universities. This alliance, centered around the project ENTISE, is dedicated to crafting high-performance, eco-friendly cells for industrial applications, harnessing the potential of sodium-ion technology. With a financial backing of approximately EUR 7.5 million in grants from Germany's Federal Ministry of Research and Education, the consortium aims to wrap up the project's final phase by mid-2027.

- As the industry pivots towards solid-state batteries, heralded for their superior energy density and safety, there's an anticipation of a shift in electrolyte requirements. Recent years have seen a flurry of agreements among companies, underscoring the industry's commitment to meeting the surging demand for solid-state batteries in the automotive realm.

- For instance, in July 2024, Volkswagen Group's battery arm, Powerco, inked a deal with QuantumScape to bring QuantumScape's pioneering solid-state lithium-metal battery technology to the industrial forefront. Such collaborations not only signal a rising demand for solid-state batteries but also underscore the need for a consistent supply of electrolytes in EV battery production.

- Given these developments and the influx of funding, the anticipated investments aimed at bolstering EV battery production capacity are set to invigorate the market.

Germany Electric Vehicle Battery Electrolyte Industry Overview

The Germany electric vehicle battery electrolyte market is moderate. Some of the major players in the market (in no particular order) include Evonik Industries AG, BASF SE, Solvay SA, Umicore SA, and Mitsubishi Chemical Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Supportive Government Policies and Investments Towards Battery Manufacturing

- 4.5.2 Restraints

- 4.5.2.1 The Dependence on Other Countries for Key Raw Materials Used in the Production of Electrolytes

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Evonik Industries AG

- 6.3.2 BASF SE

- 6.3.3 Solvay SA

- 6.3.4 Mitsubishi Chemical Group.

- 6.3.5 Umicore SA

- 6.3.6 Targray Industries Inc.

- 6.3.7 3M Company

- 6.3.8 NEI Corporation

- 6.3.9 Cabot Corporation

- 6.3.10 Samsung SDI

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Innovation in Electrolyte Formulations

02-2729-4219

+886-2-2729-4219

电动车电池电解质市场-全球产业规模、份额、趋势、机会和预测,按电池类型、电解质类型、应用、地区和竞争情况细分,2020-2030 年

电动车电池电解质市场-全球产业规模、份额、趋势、机会和预测,按电池类型、电解质类型、应用、地区和竞争情况细分,2020-2030 年 东协国家电动车电池电解:市场占有率分析、产业趋势、成长预测(2025-2030)中东和非洲电动汽车电池电解市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)中国电动汽车电池电解:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利电动汽车电池电解:市场占有率分析、产业趋势与成长预测(2025-2030)亚太地区电动汽车电池电解:市场占有率分析、产业趋势和成长预测(2025-2030 年)北美电动车电池电解:市场占有率分析、产业趋势与成长预测(2025-2030)南美洲电动车电池电解:市场占有率分析、产业趋势、成长预测(2025-2030)印度电动车电池电解:市场占有率分析、产业趋势与统计、成长预测(2025-2030)欧洲电动车电池电解:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

东协国家电动车电池电解:市场占有率分析、产业趋势、成长预测(2025-2030)中东和非洲电动汽车电池电解市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)中国电动汽车电池电解:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利电动汽车电池电解:市场占有率分析、产业趋势与成长预测(2025-2030)亚太地区电动汽车电池电解:市场占有率分析、产业趋势和成长预测(2025-2030 年)北美电动车电池电解:市场占有率分析、产业趋势与成长预测(2025-2030)南美洲电动车电池电解:市场占有率分析、产业趋势、成长预测(2025-2030)印度电动车电池电解:市场占有率分析、产业趋势与统计、成长预测(2025-2030)欧洲电动车电池电解:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

▼