|

市场调查报告书

商品编码

1683949

室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Indoor LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

室内 LED 照明市场规模预计在 2025 年为 280.7 亿美元,预计到 2030 年将达到 363.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.31%。

工业生产需求的不断增长、储存空间需求的不断增长以及办公空间可用性的增加,正在推动该地区室内 LED 照明市场的需求。

- 就金额份额而言,工业和仓储(I&W)将在 2023 年占据大部分份额(49.2%),其次是商业(31.1%)、住宅(17.5%)和农业。未来几年,我们预计工业和农业照明的份额将会增加,而其余部分的份额将略有下降。在新冠肺炎疫情期间,全球各地的产业都面临许多内部和外部阻力。 2021年,许多国家都维持了工业生产。 2021年,美国工业生产额为2,4,971亿美元,较2020年成长11.55%。同期,英国工业生产额为2,748.7亿美元,较2020年成长16.57%。因此,工业生产的上升导致对仓库的需求增加,从而导致未来几年对室内照明的需求增加。

- 在许多国家,政府补贴和住宅计画在引进新住宅发挥着重要作用。在印度,政府已经推出了多项节能计划。例如,中央政府雄心勃勃的 Pradhan Mantri Awas Yojana (PMAY) 计划旨在到 2022 年在全国建造 2000 万套经济适用住宅。加拿大卡加利在 2022 年开工建设了 17,306 个多单元住宅计划。

- 物流建设是一个越来越重要的领域,电子商务和出口热潮推动了对新仓库和其他物流基础设施的需求。 2022年7月,百胜中国控股公司在上海嘉定区开始兴建占地61,000平方公尺的百胜中国供应链管理中心。预计这些案例将推动全球室内 LED 市场的成长。

全球范围内电子商务、住宅所有权和智慧城市发展的兴起可能会促进 LED 照明的销售。

- 无论从金额份额或数量份额来看,亚太地区都占据室内 LED 照明市场的主导地位。从金额份额来看,2023年亚太地区将仅次于北美,位居第二,其次是欧洲、中东和非洲以及南美。 2021年,在亚太地区,中国产值为4,865.8亿美元,较2020年成长26.04%。 2022年,工业产值成长3.6%。 2023年3月份,中国工业生产与前一年同期比较增3.9%。因此,疫情过后工业产量的成长将转化为未来几年对室内照明的需求。

- 此外,在北美,到 2022 年,预计大多数美国新兴企业将以零售为重点(15.05%),其中包括一家实体店和一家电子商务公司。其次是餐饮等食品业务,占13.71%。新兴企业的崛起预计将推动该地区对室内 LED 的需求。

- 此外,在欧洲,德国的房屋自有率在2017年至2020年间略有下降。 2021年,约有49.1%的人口将住在公寓里,2022年,约有46.7%的人口将住在公寓里。因此,德国是欧洲住房自有率最低的国家,同时也是最大的租赁公寓市场之一。通货膨胀和高利率导致住宅出现16年来最大以季度为基础跌幅。都市区住宅和公寓价格平均下跌3.6%。预计明年住宅量将会下降。总体而言,LED照明需求的成长率可能随着住宅销售需求而波动,但租赁住宅的增加可能会加速该国的LED采用。

全球室内 LED 照明市场趋势

人口成长、绿色建筑和政府推广 LED 应用的计划正在推动市场

- 2023年世界人口将达80亿,高于2020年的77.9亿。人口最多的国家包括中国(14.5亿)、印度(14.2亿)和美国(3.368亿)。而且,全球就业人数将从2015年的31.6亿增加到2022年的33.2亿,增加近1.3亿人。随着就业和人口成长带来公民知识的增加,LED 的使用可能会增加。

- 儘管受到新冠疫情影响,全球在节能建筑方面的支出仍异常增长了 11.4%,从 2019 年的 1,650 亿美元增至 2020 年的 1,840 多亿美元。自 2015 年以来,能源效率投资的年增长率首次超过 3%。随着更多节能建筑的开发以及住宅需要拥有更多房间来满足不断增长的人口的住宅需求,对 LED 的需求将会增加。

- 在全球范围内,住宅数量不断增加,照明需求推动了 LED 的采用。例如,在印度,孟买大都会区 (MMR) 的新楼盘数量从前一年的 56,883 套增加了一倍多,达到 2022 年的 1,24,652 套。巴西的经济适用住宅计画也已重启。巴西总统宣布,计划于 2023 年 2 月重启针对低收入者的全国性联邦住宅计画。总统于 2009 年创建了该计划,名为“Minha Casa, Minha Vida”(字面意思是“我的家,我的生活”)。此类案例预计将进一步推动该国对 LED 照明的需求。

智慧城市、绿建筑发展和政府措施推动市场成长

- 北美政府正在支持智慧城市和住宅的发展,并在住宅和商业领域采用新技术。例如,美国的绿色建筑预计将在2021年大幅增加,目前已超过830亿美元。这标誌着绿色建筑领域的扩张,这对于减少建筑和房地产行业的碳足迹至关重要。由于 LED 节能,建设活动的增加和绿色建筑的采用将推动其使用。因此,该地区的 LED 市场正在扩大。

- 商业用电每天持续10至12小时。工业部门全天电力消耗24小时,住宅部门全天用电5.5-7小时。由于印度的 UJALA 计划和 SLNP 计划等政府倡议分别以较低的价格提供 LED 并实施 LED 路灯计划,促进各个行业的应用,预计亚太地区对节能照明解决方案的需求将会上升。

- 自从政府开始参与并支持有益措施以来,人们开始认识到对节能照明系统日益增长的需求。全球许多国家的政府正采取性能要求、标籤和奖励计画等各种倡议,迅速逐步淘汰低效光源。例如,欧盟修改了《生态设计指令》和《限制有害物质指令》的要求,将在 2023 年有效禁止欧洲使用所有萤光,而欧洲十多年前就开始向 LED 过渡。

室内 LED 照明产业概况

室内LED照明市场较为分散,前五大企业占比为36.84%。该市场的主要企业是:ACUITY BRANDS, INC.、LEDVANCE GmbH (MLS)、OPPLE Lighting、松下控股公司和 Signify (飞利浦)(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 人口

- 人均收入

- LED进口总量

- 照明电力消耗量

- 家庭数量

- LED渗透率

- 园艺区

- 法律规范

- 阿根廷

- 巴西

- 中国

- 法国

- 德国

- 波湾合作理事会

- 印度

- 日本

- 南非

- 英国

- 美国

- 价值链与通路分析

第五章 市场区隔

- 室内照明

- 农业照明

- 商业照明

- 办公室

- 零售

- 其他的

- 工业/仓库

- 住宅

- 地区

- 亚太地区

- 欧洲

- 中东和非洲

- 北美洲

- 南美洲

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ACUITY BRANDS, INC.

- ams-OSRAM AG

- Current Lighting Solutions, LLC.

- EGLO Leuchten GmbH

- LEDVANCE GmbH(MLS Co Ltd)

- Nichia Corporation

- OPPLE Lighting Co., Ltd

- Panasonic Holdings Corporation

- Signify(Philips)

- Thorn Lighting Ltd.(Zumtobel Group)

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001647

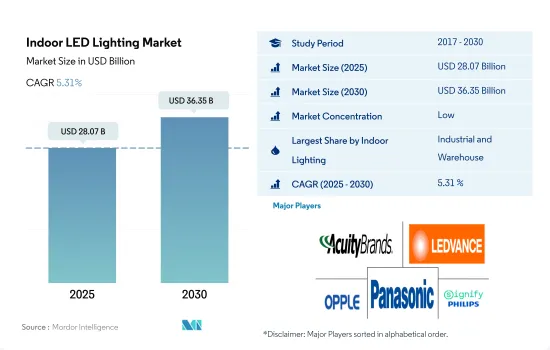

The Indoor LED Lighting Market size is estimated at 28.07 billion USD in 2025, and is expected to reach 36.35 billion USD by 2030, growing at a CAGR of 5.31% during the forecast period (2025-2030).

The increasing demand for industrial production, rising need for storage space, and increasing availability of office space drive the demand for indoor LED lighting market in the region

- In terms of value share, in 2023, industrial and warehouse (I&W) accounted for the majority of the share (49.2%), followed by commercial (31.1%), residential (17.5%), and agricultural. The market share is expected to gain in (I&W) and agricultural lighting in coming years and a small reduction in the remaining divisions. Across the globe, industries faced several internal and external headwinds during COVID-19. A large number of countries sustained their industrial production in 2021. In 2021, the United States produced a total of USD 2,497.1 billion, an increase of 11.55% compared to 2020. During the same period, the UK produced a total of USD 274.87 billion, an increase of 16.57% compared to 2020. Thus, the growing industrial production resulted in creating more need for warehouses and increasing the demand for indoor lighting in coming years.

- Government subsidies and housing schemes play a key role in the adoption of new houses in many nations. In India, the government has introduced several energy-saving programs. For example, the central government's ambitious Pradhan Mantri Awas Yojana (PMAY) program aimed to build 20 million affordable metropolitan housing units nationwide by 2022. In Calgary, Canada, under multi-units, home projects fueled 17,306 starts in 2022.

- E-commerce and the export boom have led to demand for new warehouses and other logistics infrastructure, and logistics-related building is becoming an increasingly important sector. In July 2022, Yum China Holdings Inc. commenced the construction of the Yum China Supply Chain Management Center in Shanghai's Jiading district, with an area of 61,000 square meters. Such instances are expected to drive the growth of the global indoor LED market.

Rising e-commerce, home ownership, and smart city development across the world would boost LED light sales

- In terms of value and volume share, Asia-Pacific has the majority share in indoor LED lighting. In terms of value share, in 2023, APAC stood second after North America, followed by Europe, the Middle East & Africa, and South America. In 2021, in APAC, China's output value totaled USD 486.58 billion, an increase of 26.04% compared to 2020. In 2022, industrial production increased by 3.6%. In March 2023, China's industrial production increased by 3.9% year-on-year. Thus, post-pandemic increases in industrial output will lead to demand for indoor lighting in the coming years.

- Furthermore, in North America, by 2022, most US startups were expected to be retail-focused (15.05%), including both brick-and-mortar stores and one e-commerce company. Restaurants and other food businesses followed, accounting for 13.71% of new businesses. An increase in the number of startups is expected to increase the demand for indoor LEDs in the region.

- Additionally, in Europe, between 2017 and 2020, the German homeownership rate declined slightly. About 49.1% of the population lived in apartments in 2021 and 46.7% in 2022. As a result, Germany has the lowest homeownership rate in Europe and one of the largest rental apartment markets. Inflation and high-interest rates have pushed home prices to their steepest quarterly decline in 16 years. Urban and rural homes and apartments fell an average of 3.6%. New home construction is expected to decline next year. Overall, the growth rate of demand for LED lighting may fluctuate depending on home sales demand, but growth in rental housing could accelerate LED adoption in the country.

Global Indoor LED Lighting Market Trends

The market is driven by increasing population, green buildings, and government programs to promote LED adoption

- The world's population reached 8 billion people in 2023, up from 7.79 billion in 2020. The largest countries by population included China (1.45 billion), India (1.42 billion), and the US (336.8 million). Furthermore, global employment increased to 3.32 billion people in 2022 from 3.16 billion in 2015, an increase of almost 0.13 billion people. The use of LEDs will increase as more knowledge is spread throughout the population as a result of the rise in the number of employed individuals and population growth.

- Despite the COVID-19 pandemic, worldwide spending on energy-efficient construction increased by an exceptional 11.4% in 2020 to over USD 184 billion, up from USD 165 billion in 2019. The yearly growth rate for investments in energy efficiency surpassed 3% for the first time since 2015. The requirement for additional rooms in a house will result in increased demand for LEDs due to the rise in the development of energy-efficient buildings and to meet the residential needs of the expanding population.

- Globally, launches of new houses have been rising, creating more LED penetration due to the need for illumination. For instance, in India, new launches in the Mumbai Metropolitan Region (MMR) increased over two-fold to 1,24,652 units in 2022 from 56,883 units in the previous year. Brazil's affordable housing program also restarted. The Brazilian President announced plans to restart the nationwide federal housing program for low-income individuals in February 2023. The President created the program, named "Minha Casa, Minha Vida," which translates to "My Home, My Life," in 2009. Such instances are further expected to raise the demand for LED lighting in the country.

Development of smart cities, green buildings, and government initiatives to drive the growth of the market

- The development of smart cities and homes is being supported by governments in North America, which are also adopting new technology in the residential and commercial sectors. As an illustration, green buildings in the US increased dramatically in 2021 and now exceed USD 83 billion dollars. This demonstrates the expansion of the green building sector, which is crucial for lowering the carbon footprint of the building and real estate industries. As LED is energy efficient, increased construction activity and the adoption of green building practices will encourage its use. As a result, the LED market in the area is expanding.

- Commercial electricity use lasts between 10 and 12 hours every day. Electricity consumption in the industrial sector accounts for 24 hours a day, while in the residential sector, it varies from 5.5 to 7 hours. The demand for energy-efficient lighting solutions is expected to rise in Asia-Pacific, in part because of government initiatives like India's UJALA and SLNP programs, which offer LEDs at reduced prices and LED installation projects for streetlights, respectively, and promote their use in a variety of industries.

- After governments began taking part in and supporting beneficial efforts, the growing need for energy-efficient lighting systems was mainly realized. Numerous governments all over the world are moving swiftly to phase out inefficient light sources through a variety of efforts like performance requirements, labeling, and incentive schemes. For instance, the EU modified requirements under the Ecodesign Directive and the Restriction of Hazardous Substances Directive, which essentially prohibited all fluorescent lighting in 2023 in Europe, where the transition to LED began more than ten years ago.

Indoor LED Lighting Industry Overview

The Indoor LED Lighting Market is fragmented, with the top five companies occupying 36.84%. The major players in this market are ACUITY BRANDS, INC., LEDVANCE GmbH (MLS Co Ltd), OPPLE Lighting Co., Ltd, Panasonic Holdings Corporation and Signify (Philips) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 Per Capita Income

- 4.3 Total Import Of Leds

- 4.4 Lighting Electricity Consumption

- 4.5 # Of Households

- 4.6 Led Penetration

- 4.7 Horticulture Area

- 4.8 Regulatory Framework

- 4.8.1 Argentina

- 4.8.2 Brazil

- 4.8.3 China

- 4.8.4 France

- 4.8.5 Germany

- 4.8.6 Gulf Cooperation Council

- 4.8.7 India

- 4.8.8 Japan

- 4.8.9 South Africa

- 4.8.10 United Kingdom

- 4.8.11 United States

- 4.9 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Indoor Lighting

- 5.1.1 Agricultural Lighting

- 5.1.2 Commercial

- 5.1.2.1 Office

- 5.1.2.2 Retail

- 5.1.2.3 Others

- 5.1.3 Industrial and Warehouse

- 5.1.4 Residential

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.2 Europe

- 5.2.3 Middle East and Africa

- 5.2.4 North America

- 5.2.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ACUITY BRANDS, INC.

- 6.4.2 ams-OSRAM AG

- 6.4.3 Current Lighting Solutions, LLC.

- 6.4.4 EGLO Leuchten GmbH

- 6.4.5 LEDVANCE GmbH (MLS Co Ltd)

- 6.4.6 Nichia Corporation

- 6.4.7 OPPLE Lighting Co., Ltd

- 6.4.8 Panasonic Holdings Corporation

- 6.4.9 Signify (Philips)

- 6.4.10 Thorn Lighting Ltd. (Zumtobel Group)

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

可调光LED轨道灯具市场按类型、光源、安装方式、功率、应用和最终用户划分-全球预测,2026-2032年

可调光LED轨道灯具市场按类型、光源、安装方式、功率、应用和最终用户划分-全球预测,2026-2032年 中东和非洲室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)南美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)德国室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)日本室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)欧洲室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中东和非洲室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)南美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)德国室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)日本室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)欧洲室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

▼