|

市场调查报告书

商品编码

1683950

印度汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)India Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

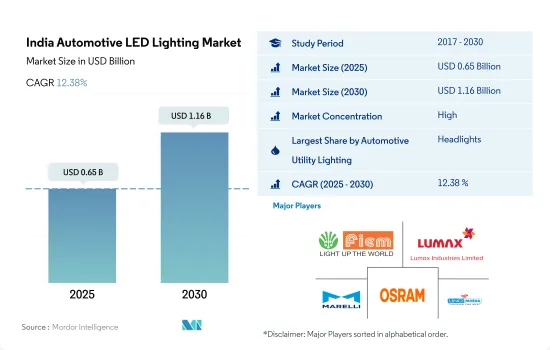

印度汽车 LED 照明市场规模预计在 2025 年为 6.5 亿美元,预计到 2030 年将达到 11.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 12.38%。

就金额而言,头灯预计将占据最大的市场份额

- 从2017年的金额份额来看,头灯占了大部分,其次是方向灯和日间行车灯。预计头灯和日间行车灯的市场占有率将保持不变,而转向信号灯的市场份额预计在预测期内将略有下降。印度汽车照明市场的最大趋势是在头灯中增加带有投影灯的DRL(日行灯)。塔塔、现代和马恆达是几个将在其即将推出的汽车中整合 LED 投影灯的知名例子。随着事故趋势的增加, LED灯的渗透率预计也会上升。 2021年,雨、雾、冰雹、雨夹雪等恶劣天气条件下发生的事故占所有交通事故的16.8%,与前一年同期比较增加了12.6%。

- 从出货量份额来看,2017年方向灯占最大份额,其次是头灯和煞车灯。这些灯的市场占有率保持稳定,预计未来不会发生变化。转向信号灯是任何车辆的主要部件,在发生轻微至重大事故时都可能受到影响并需要更换。 2017年总合发生道路交通事故464910起,到2021年下降到412432起,这也说明转向信号灯的数量在逐年减少。

- 在扩张和创新方面,2022年9月,马瑞利将在印度南部班加罗尔开设一个新的技术研发中心,以增强公司在电子机械设计模拟和汽车照明产品方面的创新能力。

印度汽车 LED 照明市场趋势

自主品牌大力推广经济型乘用车和商用车

- 印度汽车产量预计2022年将达2,747万辆,2023年将达2,906万辆。新冠肺炎疫情影响了整个汽车产业的运作。 2020年4月,汽车产业全面停滞,没有销售纪录。销售于 2020 年 5 月开始,但仍远低于 2019 年的水准。印度汽车工业协会 (SIAM) 计算出,暂停营运的决定导致每天的生产损失为 2,300 亿印度卢比(2.7707 亿美元)。然而,预计市场将在 2021 年復苏,并在整个预测期内实现正成长。

- TATA Motors、Mahindra &Mahindra、Ashok Leyland Ltd、Maruti Suzuki、Bajaj Auto Ltd 等是印度顶级汽车製造商。印度汽车工业正在扩张,并非常重视替代燃料以及利用环保燃料来提高汽车经济性。例如,塔塔汽车推出了Starbus电动巴士,这是一款以替代燃料为动力的乘用车,以满足智慧城市当前和未来的客运需求。 LED 照明的节能性能和高流明输出使得其在车辆中广泛应用。

- 汽车照明仍然是关键因素。照明不仅可以增强车辆内部和外部的美观度,还可以提高车辆的安全。例如,2021年9月,印度有50多家公司提交了与LED和其他产品生产挂钩的奖励申请,提案投资6,000亿印度卢比(7.22亿美元)。企业和政府的此类投资预计将推动印度全面采用 LED 照明。

政府政策协助扩大充电站网络

- 目前,印度正处于发展阶段。到2023年3月,全国将有6,586个公共充电站(PCS)投入运作。印度政府一直致力于透过推出电动车倡议,将印度打造为电动车产业的主要参与者之一。

- 随着印度的发展,电动车产业蓬勃发展,允许 100% 直接投资、建立新製造工厂并推动充电基础设施建设。政府透过提供资本补贴(如 FAME-II、PLI SCHEME、电池更换政策、电动车区域和电动车税收减免)来鼓励安装电动车充电站。 2019 年 4 月,FAME II 计画启动,预算为 12.0465 亿美元,用于支援 50 万辆电动三轮车、7,000 辆电动公车、5.5 万辆电动二轮车。其目的是促进电动车在印度的普及。该计划原定于 2022 年完成。 2021 年 9 月,内阁批准了针对汽车产业的生产连结奖励计画计画 (PLI 计画),以增加电动车和氢燃料电池汽车的产量。

- 此外,作为 PLI 计划的增值部分,预计对 LED 照明市场的投资将达到 40% 至 75% 左右。这也将见证原本不在印度生产的零件和子组件的製造。预计此类政府投资将推动印度整体 LED 照明市场的发展,包括汽车 LED。此外,印度对电动车的需求进一步扩大,预计将推动对电动车充电基础设施的需求,从而在预测期内产生对汽车 LED 的需求。

印度汽车LED照明产业概况

印度汽车LED照明市场相当集中,前五大厂商占80.99%的市占率。市场的主要企业有:汽车LED照明Fiem Industries Ltd.、Lumax Industries、Marelli Holdings、OSRAM GmbH。以及 Uno Minda Limited(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 汽车产量

- 人口

- 人均收入

- 汽车贷款利率

- 充电站数量

- 汽车持有量

- LED进口总量

- 家庭数量

- 道路网络

- 渗透率

- 法律规范

- 印度

- 价值链与通路分析

第五章 市场区隔

- 汽车实用照明

- 日间行车灯 (DRL)

- 转向指示灯

- 头灯

- 倒车灯

- 红绿灯

- 尾灯

- 其他的

- 汽车照明

- 二轮车

- 商用车

- 搭乘用车

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- Fiem Industries Ltd.

- HELLA GmbH & Co. KGaA

- HYUNDAI MOBIS

- Lumax Industries

- Marelli Holdings Co., Ltd.

- Neolite ZKW Lightings Pvt. Ltd

- OSRAM GmbH.

- Uno Minda Limited

- Valeo

- Varroc Group

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001648

The India Automotive LED Lighting Market size is estimated at 0.65 billion USD in 2025, and is expected to reach 1.16 billion USD by 2030, growing at a CAGR of 12.38% during the forecast period (2025-2030).

Headlights are expected to hold the highest share by market value

- In terms of value share, in 2017, headlights accounted for the majority, followed by directional signal lights and DRL. The market share is expected to remain the same for headlights and DRL during the forecast period, with a small reduction in directional signal lights. The biggest trend in India's automotive lighting market is the addition of DRLs (daytime running lamps) with projector lights in frontal lighting. Tata, Hyundai, and Mahindra are among the few popular examples of integrating LED projector lights in upcoming vehicles. The fog LED lamp penetration rate is expected to increase with increasing accident trends. Accidents under adverse weather conditions such as rainy, foggy, and hail/sleet accounted for 16.8% of total road accidents in 2021, an increase of 12.6% from the prior year.

- In terms of volume share, in 2017, directional signal lights accounted for the majority, followed by headlights and stoplights. The market share is expected to remain the same with less fluctuation for these lights. Directional signal lights are the prime part with a high probability of getting affected in minor to major accidents in all types of vehicles and require replacement. In 2017, a total of 4,64,910 road accidents occurred, while in 2021, it decreased to 4,12,432. This also indicated the decrease in the volume of directional signal light every year.

- In terms of expansion and innovations, in September 2022, Marelli inaugurated its new Technical R&D Center in Bangalore, South India, boosting the company's innovation capability in Mechanical Design Simulations for Electronics and moving forward for automotive lighting products.

India Automotive LED Lighting Market Trends

Homegrown automotive brands are promoting economical passenger and commercial vehicles

- The total automobile vehicle production in India stood at 27.47 million units in 2022, and it was expected to reach 29.06 million units in 2023. The COVID-19 outbreak impacted the auto industry's entire operations. In April 2020, the auto industry was completely shut down, and no sales were recorded. Sales started in May 2020, but even then, they were far lower than they had been at the same point in 2019. According to a calculation by the Society of Indian Automobile Manufacturers (SIAM), the shutdown decision caused a daily output loss of INR 2,300 crore (USD 277.07 million). However, the market rebounded in 2021, and it is projected to witness positive growth throughout the forecast period.

- TATA Motors, Mahindra & Mahindra, Ashok Leyland Ltd, Maruti Suzuki, and Bajaj Auto Ltd, among others, are the country's top automakers. India's automotive industry is expanding, with businesses emphasizing alternative fuels and improving the vehicle economy with eco-friendly fuels. For instance, Tata Motors introduced the Starbus Electric Bus, a passenger vehicle driven by alternative fuels, to satisfy the present and future passenger transportation needs in smart cities. Due to the energy-saving capabilities and high-lumen output of LED lights, they are being increasingly adopted in vehicles.

- Vehicle lighting is still a crucial component. Lighting enhances the aesthetic appeal of a vehicle's interior and exterior while contributing to vehicle safety. For instance, in September 2021, more than 50 companies in India submitted applications for production-linked incentives for LEDs and other products, with a proposed investment of INR 6,000 crores (USD 722 million). Such investments by companies and the government are expected to drive the overall adoption of LED lighting in India.

Government policies are helping extend the network of charging stations

- Currently, India is in its developing phase. By March 2023, there were 6,586 public charging stations (PCS) operational in the country. The Government of India consistently demonstrates its commitment to establishing India as one of the significant players in the EV industry by introducing initiatives for electric vehicles.

- As India is developing, the electric vehicle industry is also picking pace, with the possibility of 100% FDI, new manufacturing plants, and an increased push to improve charging infrastructure. The government is promoting the installation of EV charging stations by providing capital subsidies, including FAME-II, PLI SCHEME, Battery Switching Policy, Special Electric Mobility Zone, and tax reduction on EVs. In April 2019, the FAME II plan was introduced with an USD 1204.65 million budget to support 500,000 e-three-wheelers, 7,000 e-buses, 55,000 e-passenger vehicles, and a million e-two-wheelers. The purpose was to encourage electric vehicle adoption in India. The plan was supposed to end in 2022. In September 2021, a PLI Scheme, or Production-Linked Incentive Scheme, for the automotive sector was approved by the Cabinet to increase the manufacturing of electric and hydrogen fuel cell vehicles.

- Additionally, as a value addition under the PLI scheme, investments in the LED lighting market are expected to be around 40% to 75%. This would also result in the manufacturing of components or sub-assemblies that were originally not manufactured in India. Such investments by the government are expected to drive the overall LED lighting market in India, including automotive LEDs. Further growing demand for EVs in India is expected to boost the demand for EV charging infrastructure, which would also create the need for automotive LEDs during the forecast period.

India Automotive LED Lighting Industry Overview

The India Automotive LED Lighting Market is fairly consolidated, with the top five companies occupying 80.99%. The major players in this market are Fiem Industries Ltd., Lumax Industries, Marelli Holdings Co., Ltd., OSRAM GmbH. and Uno Minda Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 India

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Fiem Industries Ltd.

- 6.4.2 HELLA GmbH & Co. KGaA

- 6.4.3 HYUNDAI MOBIS

- 6.4.4 Lumax Industries

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Neolite ZKW Lightings Pvt. Ltd

- 6.4.7 OSRAM GmbH.

- 6.4.8 Uno Minda Limited

- 6.4.9 Valeo

- 6.4.10 Varroc Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2026年全球汽车LED照明市场报告

2026年全球汽车LED照明市场报告 汽车LED照明市场-全球产业规模、份额、趋势、机会、预测:按位置、车辆类型、自适应照明、地区和竞争格局划分,2021-2031年

汽车LED照明市场-全球产业规模、份额、趋势、机会、预测:按位置、车辆类型、自适应照明、地区和竞争格局划分,2021-2031年 汽车LED照明市场规模、份额和成长分析(按技术类型、车辆类型、类型和地区划分)-产业预测(2026-2033年)

汽车LED照明市场规模、份额和成长分析(按技术类型、车辆类型、类型和地区划分)-产业预测(2026-2033年) 汽车LED照明市场(按车型、产品类型、技术和销售管道)——2025-2032年全球预测

汽车LED照明市场(按车型、产品类型、技术和销售管道)——2025-2032年全球预测 汽车用LED的世界市场趋势:照明和显示器预测

汽车用LED的世界市场趋势:照明和显示器预测 汽车LED照明市场:2025年至2030年预测

汽车LED照明市场:2025年至2030年预测 全球汽车LED市场(2025年)- 照明与显示产品趋势全球汽车LED尾灯市场:未来预测(2025-2030)

全球汽车LED市场(2025年)- 照明与显示产品趋势全球汽车LED尾灯市场:未来预测(2025-2030) 汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年

汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年 中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

▼