|

市场调查报告书

商品编码

1686575

英国作物保护化学品:市场占有率分析、行业趋势和成长预测(2025-2030 年)UK Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

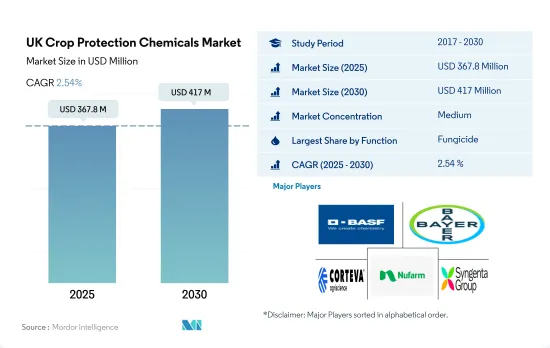

英国作物保护化学品市场规模预计在 2025 年为 3.678 亿美元,预计到 2030 年将达到 4.17 亿美元,预测期内(2025-2030 年)的复合年增长率为 2.54%。

该国的病虫害侵扰日益严重,导致严重的产量损失,并推动了各种作物保护化学品市场的需求。

- 2022 年英国杀菌剂市值为 1.829 亿美元,同年市场占有率为 53.2%,成为消费量最大的作物保护化学品。

- 英国使用最广泛的杀菌剂包括Chlorothalonil、Epoxiconazole、Prothioconazole和Tebuconazole。小麦叶枯病是英国最具破坏性的小麦叶部病害,在高压时期会造成 30-50% 的产量损失。许多小麦种植者正在增加杀菌剂的使用以减少产量损失。

- 这种杂草影响英国的棉花和冬小麦等作物。对于主要纤维作物棉花而言,这已造成30%的产量损失。黑草(Alopecurus myosuroides)是一种本土杂草,在英国农场中猖獗生长。严重的虫害迫使农民放弃主要粮食作物冬小麦。杂草争夺资源,阻碍作物生长,降低产量,造成经济损失,并导致使用除草剂。 2022 年,除草剂占英国作物保护化学品市场的 38.2%。

- 气候变迁和气温升高导致害虫数量增加,摄食习惯也随之改变。一项研究预测,随着作物受到的热应力加剧,英国气温上升 2°C 可能会导致粮食产量减少约 10%。结果,该国农民被迫使用杀虫剂来应对虫害压力。

- 该国病虫害的侵扰日益严重,导致严重的产量损失,因此市场需要一系列基于农民需求的作物保护剂。预计预测期内(2023-2029 年)市场复合年增长率为 2.4%。

英国作物保护化学品市场趋势

在英国,农药消费量正在下降,原因有很多,包括农民采用非化学替代品。

- 英国的杀虫剂消费量正在下降。 2017年至2022年间,由于种植面积转向畜牧业生产、某些活性物质的撤出、天气对病虫害水平的影响以及农民采用非化学替代品,每公顷消费量减少了243,800吨。

- 英国减少农药使用的压力越来越大,可能会影响未来几年的农药消费。政府已采取多项倡议减少农药的使用。例如,2018年1月,英国政府发布了《绿色未来:我们的25年计画》,旨在改善环境并增加综合虫害管理(IPM)和永续作物保护的采用。

- 2020 年,儘管草甘膦可能与癌症有关,但英国农业中Glyphosate的使用量在四年内增加了 16%,包括重量、处理面积和每公顷施用率。政府计划透过增加收穫前干燥(使用Glyphosate人工干燥作物)或增加犁地农业来减少对传统化学物质的依赖,免耕农业倾向于依靠Glyphosate和其他除草剂来处理杂草,而不会透过耕作从土壤中释放碳。同样,杀菌剂IMAZALIL)的使用量增加了53%,而同期用该化学品处理的土地面积增加了63%,达到81,000多公顷。

- 植物病虫害对农业生产有重大影响,因此气候变迁、病虫害和产量损失可能会增加农药消耗,以保护作物,减少因病虫害造成的产量损失。

监管变化和政府对减少农药的关注可能会影响作物保护化学品的价格。

- Cypermethrin和Emamectin benzoate是目前大规模使用的重要杀虫剂成分。 2022年,这些零件的价格分别为每吨21,100美元和每吨17,300美元。

- Metalaxyl2022 年的价格为每吨 8,700 美元,是一种系统性苯酰胺杀菌剂,以其保护和治疗作用而闻名。它透过抑制孢子囊的形成、菌丝的生长和新感染的建立来发挥作用。它抑制真菌核酸合成(RNA聚合酵素1)。该杀菌剂建议用作热带和亚热带作物的叶面喷布、用于控制土壤传播病原体的土壤处理剂以及用于管理霜霉病的种子处理剂。

- Glyphosate被农民广泛用作除草剂来控制杂草并作为耕作的替代品,但据观察,它会破坏土壤生态系统并释放碳。在英国,由于再生农业实践鼓励减少耕作,截至 2020 年的四年间,Glyphosate在农业中的使用量增加了 16%。农药喷洒面积增加9%(23万公顷)。小麦种植者主要使用Glyphosate在收穫前干燥作物。 2022年Glyphosate价格与前一年同期比较去年同期上涨2.2%。

- 选择性除草剂二甲戊灵属于Dinitroanilines除草剂。它用于控制各种园艺作物、草坪和林业中的多种杂草,包括一年生植物、多年生植物、阔叶树和木本植物。 2022年,二甲戊灵的价格为每吨3,300美元。

英国作物保护化学品产业概况

英国作物保护化学品市场适度整合,前五大公司占 63.61% 的市场。市场的主要企业包括BASF公司、拜耳公司、科迪华农业科技、纽髮姆有限公司和先正达集团(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告发布

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 英国

- 价值炼和通路分析

第五章市场区隔

- 按功能

- 杀菌剂

- 除草剂

- 杀虫剂

- 杀软体动物剂

- 杀线虫剂

- 按应用

- 化学处理

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 按作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 52786

The UK Crop Protection Chemicals Market size is estimated at 367.8 million USD in 2025, and is expected to reach 417 million USD by 2030, growing at a CAGR of 2.54% during the forecast period (2025-2030).

Increasing pests and disease infestations in the country are leading to severe yield losses and driving the market for different crop protection chemicals

- The UK fungicide market was valued at USD 182.9 million in 2022. It was the most consumed among crop protection chemicals, with a market share of 53.2% in the same year.

- The most extensively used fungicide formulations in the United Kingdom include chlorothalonil, epoxiconazole, prothioconazole, and tebuconazole. Septoria tritici is UK wheat's most damaging foliar disease, causing yield losses that range from 30% to 50% in high-pressure seasons. Many wheat growers have increased the use of fungicides in their crops to mitigate yield loss.

- Weeds impact UK crops like cotton and winter wheat. They cause a 30% yield loss in cotton, the main fiber crop. Black grass (Alopecurus myosuroides), a native weed, frequently infests UK farms. Severe infestations force farmers to abandon winter wheat, the main cereal crop. Weeds compete for resources, hinder crop growth, and reduce yields, causing economic losses and leading to the adoption of herbicides. Herbicides accounted for 38.2% of the UK crop protection chemicals market in 2022.

- The changing climate and rising temperatures are causing an increase in the population and feeding habits of insect pests. A study reveals that as heat stress on crops intensifies, cereal yields in the United Kingdom are projected to decline by approximately 10% with a 2 °C increase in temperature. Consequently, these circumstances are prompting farmers in the country to rely on insecticides to manage pest pressures.

- Increasing pests and disease infestations in the country have led to severe yield losses, thus driving the market for different crop protection chemicals based on farmers' needs. The market is estimated to register a CAGR of 2.4% during the forecast period (2023-2029).

UK Crop Protection Chemicals Market Trends

The United Kingdom is experiencing a decline in the consumption of pesticides due to various factors, including the adoption of non-chemical alternatives by farmers

- The United Kingdom is experiencing a decline in the consumption of pesticides. From 2017 to 2022, the consumption per hectare decreased by 243.8 thousand metric ton due to changes in the area of cultivation to livestock farming, withdrawal of certain active substances, the impact of the weather on pest and disease levels, and the adoption of non-chemical alternatives by farmers.

- The rising pressure on the United Kingdom to reduce the use of pesticides could impact the consumption of pesticides in the coming years. The government is taking several initiatives to reduce the use of pesticides. For instance, in January 2018, the UK government launched "A Green Future: Our 25-Year Plan" to improve the environment and increase the uptake of integrated pest management (IPM) and sustainable crop protection.

- In 2020, the use of glyphosate in UK farming grew by 16% over four years in terms of weight, the area treated, and application rate per hectare despite being linked to causing cancer and the government plans to reduce reliance on conventional chemicals due to rising pre-harvest desiccation (where crops are artificially dried using glyphosate) and/or an increase in no-till agriculture, which tends to rely upon glyphosate and other herbicides to deal with weeds without releasing carbon from the soil via plowing. Similarly, the use of the fungicide imazalil increased by 53%, while the land area treated with the chemical rose by 63% to more than 81,000 ha during the same period.

- Changing climate, pests and diseases, and harvest losses could drive the consumption of pesticides to protect crops and reduce pest yield losses, as plant diseases and pests can have a significant impact on agriculture production.

Regulatory changes and the government's focus on reducing pesticides may influence the prices of crop protection chemicals

- Cypermethrin and emmamectin benzoate are significant insecticide ingredients used on a large scale. In 2022, these ingredients were priced at USD 21.1 thousand per metric ton and USD 17.3 thousand per metric ton, respectively.

- Metalaxyl, valued at USD 8.7 thousand per metric ton in 2022, is a systemic phenylamide fungicide known for its protective and curative mode of action. It works by suppressing sporangial formation, mycelial growth, and the establishment of new infections. It disrupts fungal nucleic acid synthesis - RNA polymerase 1. This fungicide is recommended for foliar spray on tropical and sub-tropical crops, as a soil treatment for controlling soil-borne pathogens, and as a seed treatment to manage downy mildew.

- Glyphosate, widely used by farmers as a herbicide for weed control and as an alternative to plowing, has been observed to disrupt the soil ecosystem and release carbon. In the United Kingdom, its usage in farming witnessed a growth of 16% over four years till 2020, with regenerative farming practices encouraging reduced plowing. The area of land sprayed with pesticides expanded by 9% (230,000 ha). Wheat farms are notable users of glyphosate for crop desiccation before harvest. In 2022, the price of glyphosate experienced a 2.2% increase compared to the previous year.

- Pendimethalin, a selective herbicide, belongs to the dinitroaniline herbicide family. It is used to control a broad range of weeds, including annual and perennial grasses, broadleaf species, and woody species in various horticultural crops, turf, and forestry. In 2022, pendimethalin was priced at USD 3.3 thousand per metric ton.

UK Crop Protection Chemicals Industry Overview

The UK Crop Protection Chemicals Market is moderately consolidated, with the top five companies occupying 63.61%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

日本作物保护化学品市场报告(按产地、类型、应用和地区)2025-2033

日本作物保护化学品市场报告(按产地、类型、应用和地区)2025-2033 农作物保护化学品市场 - 全球产业规模、份额、趋势、机会和预测,按类型、来源、应用方式、地区和竞争细分,2020-2030 年预测

农作物保护化学品市场 - 全球产业规模、份额、趋势、机会和预测,按类型、来源、应用方式、地区和竞争细分,2020-2030 年预测 中国作物保护化学品市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太地区作物保护化学品:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)作物保护化学品-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美作物保护化学品-市场占有率分析、产业趋势与统计、成长预测(2025-2030)南美作物保护化学品:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印尼作物保护化学品市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)印度作物保护化学品-市场占有率分析、产业趋势与统计、2025-2030年成长预测德国作物保护化学品-市场占有率分析、产业趋势与统计、成长预测(2025-2030)

中国作物保护化学品市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太地区作物保护化学品:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)作物保护化学品-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美作物保护化学品-市场占有率分析、产业趋势与统计、成长预测(2025-2030)南美作物保护化学品:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印尼作物保护化学品市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)印度作物保护化学品-市场占有率分析、产业趋势与统计、2025-2030年成长预测德国作物保护化学品-市场占有率分析、产业趋势与统计、成长预测(2025-2030)

▼