|

市场调查报告书

商品编码

1693384

泰国黏合剂:市场占有率分析、行业趋势和成长预测(2025-2030 年)Thailand Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

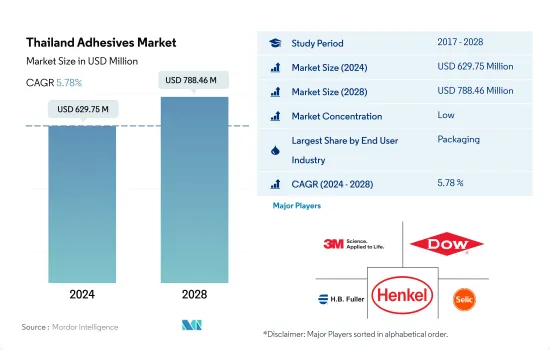

泰国黏合剂市场规模预计在 2024 年为 6.2975 亿美元,预计到 2028 年将达到 7.8846 亿美元,预测期内(2024-2028 年)的复合年增长率为 5.78%。

泰国的汽车工业在该国黏合剂需求的整体成长中发挥关键作用。

- 受新冠疫情影响,2020 年黏合剂消费量较 2019 年下降约 11.6%。疫情导致製造地关闭、需求减少,严重影响了泰国的黏合剂消费量。泰国的停工持续了近三个月,扰乱了供应链并导致劳动力短缺。但由于製造业需求稳定,2021年消费量达到10%左右的正成长。

- 黏合剂主要用于国内包装产业,因为它们在包装应用中黏合塑胶、金属、纸张和纸板方面发挥着至关重要的作用。由于成本低、黏合强度高,这些应用需要使用水性黏合剂,并且该行业大量使用水性黏合剂。 2021 年,泰国包装产业消耗了约 26,000 吨水性黏合剂。溶剂型黏合剂是包装产业成长最快的技术,预计 2022 年至 2028 年该领域的复合年增长率为 2.37%。

- 汽车业是泰国第二大黏合剂消费产业。该国汽车产能达168万辆,与前一年同期比较增18%,带动2021年汽车胶合剂市场成长16.62%。预计国际市场对泰国汽车出口需求的成长将推动未来几年对汽车胶合剂的需求。 2021年汽车出口额将达414.3亿美元。

泰国黏合剂市场趋势

食品、化妆品等产业对塑胶包装的需求不断增加,推动包装产业

- 预计2022年泰国人均GDP将达7,450美元,与前一年同期比较增3.3%。包装产业对该国GDP的贡献约为1.91%。贸易外汇、就业、人事费用、政府政策支持等都会影响泰国的包装产业。

- 2020年,受新冠疫情影响,泰国经济放缓。当年的产量与 2019 年相比下降了 4.74%。这是由于供应链中断、劳动力短缺以及近三个月的全国封锁造成的。然而,2021年国际边界开放后国内经济復苏,导致生产所需原料供应正常,2021年增加了7,900吨。

- 泰国是全球塑胶包装市场领先的製造国之一。塑胶包装产业每年的价值为 50 亿美元,是所有类型包装中最高的。该国约有28%的塑胶产量用于塑胶包装产品。这种包装主要用于食品、医疗、化妆品和许多其他类型的产品。

- 泰国包装产业对生质塑胶的使用正在增加。政府也透过《塑胶废弃物管理蓝图(2018-2030)》等措施优先发展生质塑胶产业。 GC 和嘉吉是跨国生物聚合物公司,已宣布计划投资 200 亿美元在泰国建造新的生质塑胶工厂。

泰国汽车工业预计将占据东南亚国协汽车产量的近50.1%,处于领先地位。

- 过去50年来,泰国汽车工业经历了令人瞩目的成长。该国正在不断向下一代汽车产业迈进,该产业遵循S曲线,具有更高的附加价值生产,并致力于使其汽车产业政策与环境保护政策保持一致。泰国是东协地区最大的汽车生产国。 2020年产量为1,427,074辆,占东协总产量的50.1%。其次是印尼(691,150辆,约24.2%)和马来西亚(485,186辆,约17.0%)。

- 2019年汽车产量约2,013,710辆,但2020年受新冠疫情影响,产量骤降至1,427,074辆,下降约29%。因此,2019年至2021年汽车产量波动幅度约为-16%,2020年至2021年汽车产量波动幅度约为-1%。

- 泰国是世界第11大汽车生产国,也是东协第一大汽车生产国,凭藉着成熟的价值链,有望成为东协的电动车中心。为满足当地需求,泰国的电动车库存正稳定成长。更重要的是,几家泰国知名公司正在积极投资该国的电动车充电基础设施,显示对未来需求成长的信心日益增强。政府和私人机构为增加充电站等电动车基础设施所做的努力表明泰国的电动车生态系统正在快速发展。

泰国胶黏剂产业概况

泰国胶合剂市场较为分散,前五大企业占29.77%的市占率。该市场的主要企业包括 3M、陶氏、HB Fuller Company、汉高股份公司、Selic Corp Public Company Limited 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑与施工

- 鞋类皮革

- 包装

- 木製品和配件

- 法律规范

- 泰国

- 价值炼和通路分析

第五章市场区隔

- 最终用户产业

- 航太

- 车

- 建筑与施工

- 鞋类和皮革

- 医疗保健

- 包装

- 木製品和配件

- 其他的

- 科技

- 热熔胶

- 反应性

- 溶剂型

- 紫外线固化胶合剂

- 水性

- 树脂

- 丙烯酸纤维

- 氰基丙烯酸酯

- 环氧树脂

- 聚氨酯

- 硅胶

- VAE・EVA

- 其他的

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- 3M

- Arkema Group

- Dow

- DUNLOP ADHESIVES(THAILAND)CO., LTD.

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Selic Corp Public Company Limited.

- Sika AG

- Star Bond (Thailand) Company Limited

第七章:CEO面临的关键策略问题

第 8 章 附录

- 全球黏合剂和密封剂产业概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 驱动因素、限制因素和机会

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 92439

The Thailand Adhesives Market size is estimated at 629.75 million USD in 2024, and is expected to reach 788.46 million USD by 2028, growing at a CAGR of 5.78% during the forecast period (2024-2028).

Thailand's Automotive industry having a significant role in the overall growth of adhesive's demand in the country

- The consumption of adhesives declined in 2020 by about 11.6% compared to 2019 due to the COVID-19 pandemic, which severely affected the consumption of adhesives in Thailand owing to the closedown of the manufacturing sites and reduction in demand. The lockdown in the country for nearly three months resulted in supply chain disruptions and labor shortages. However, consumption registered growth in 2021 with a positive growth rate of about 10% due to steady demand from the manufacturing sector.

- Adhesives are majorly consumed in the packaging industry in the country owing to their importance in bonding plastics, metals, and paper and cardboard packaging applications. Water-borne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength, which is required in these applications. Nearly 26 thousand tons of water-borne adhesives were consumed in the Thai packaging industry in 2021. Solvent-borne adhesives are the fastest-growing technology in the packaging industry, and the segment is expected to register a CAGR of 2.37% from 2022 to 2028.

- The automotive industry is the second-largest consumer of adhesives in Thailand. The automotive adhesives market grew by 16.62% in 2021, as the country's total vehicle manufacturing capacity reached 1.68 million units, up by 18% from the previous year. The rising demand for Thailand's automotive exports in the international market is expected to drive the demand for automotive adhesives over the coming years. The automotive export value reached USD 41.43 billion in 2021.

Thailand Adhesives Market Trends

Growing demand for plastic packaging in food, cosmetics, and other industries will propel the packaging industry

- Thailand registered a GDP of USD 7,450 per capita with a growth rate of 3.3% Y-O-Y in 2022. The packaging industry contributes a share of around 1.91 of the country's GDP. Trade exchange, employment, labor charges, government policy support, etc., affect the Thai packaging industry.

- The country observed an economic slowdown in 2020 because of the COVID-19 pandemic. Production volume declined by 4.74% in the same year compared to 2019. This happened due to supply chain disruptions, labor shortages, and a lockdown in the country for nearly three months. However, because of economic recovery in the country in line with international borders being opened in 2021, the regular supply of raw materials began for production, which increased by 7,900 ton in 2021.

- Thailand is one of the major manufacturing countries in the global plastic packaging market. The plastic packaging industry reaches USD 5 billion annually, the highest among other types of packaging. Around 28% of the country's plastic production is used in plastic packaging products. This packaging is majorly used in food, healthcare, cosmetics, and many other types of products in Thailand.

- The usage of bioplastics in the packaging industry of Thailand is increasing. The government has also prioritized the bioplastic industry's development through policies such as the Plastic Waste Management Roadmap (2018-2030). GC and Cargill are two multinational biopolymer companies that have announced plans to invest USD 20 billion in establishing new bioplastic plants in Thailand.

Nearly 50.1% share of the overall automotive production among the ASEAN countries is likely to drive the industry in Thailand

- The Thai automobile sector has grown tremendously over the last 50 years. The country is constantly advancing its next-generation automotive industry to follow the S-Curve promotion with better value-added production, and it also aims for the automotive industrial policy to be aligned with the environmental protection policy. Thailand is the largest auto producer in the ASEAN region. In 2020, production totaled 1,427,074 units, accounting for 50.1% of total ASEAN production. This was followed by Indonesia (690,150 units, or approximately 24.2%) and Malaysia (485,186 units, or approximately 17.0%).

- In 2019, the country recorded about 20.13,710 units of vehicles produced, which drastically reduced to 14,27,074 units in 2020, accounting for a decline of about 29% owing to the COVID-19 pandemic. As a result, the variation in automotive production between 2019 and 2021 amounted to about -16%, whereas between 2020 and 2021, the variation was recorded at about -1%.

- Thailand, ranked as the 11th largest automotive producer in the world and the first in ASEAN, is poised to become ASEAN's EV center, owing to its well-established value chain, which provides the industry with top-notch quality products at a competitive price. Thailand's EV stock has been steadily increasing in response to local demand. More importantly, several well-known Thai corporations have been actively investing in EV charging infrastructure around the country, indicating rising confidence in future demand increases. Efforts by governmental and private sector institutions to increase EV infrastructure, such as charging stations, suggest that Thailand's EV ecosystem is developing rapidly.

Thailand Adhesives Industry Overview

The Thailand Adhesives Market is fragmented, with the top five companies occupying 29.77%. The major players in this market are 3M, Dow, H.B. Fuller Company, Henkel AG & Co. KGaA and Selic Corp Public Company Limited. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 DUNLOP ADHESIVES (THAILAND) CO., LTD.

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 Selic Corp Public Company Limited.

- 6.4.9 Sika AG

- 6.4.10 Star Bond (Thailand) Company Limited

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

纺织黏合剂市场:黏合剂类型、形态、功能、织物类型、最终用户和分销管道划分-全球预测,2026-2032年黏合剂机器类型、聚合物类型、速度、黏度、应用、最终用途产业和销售管道,全球预测,2026-2032年有机热连接件市场:依产品类型、应用、终端用户产业及通路划分,全球预测(2026-2032年)橡皮筋黏合剂市场按类型、形式、分销管道、应用和最终用户划分,全球预测(2026-2032年)橡胶基材黏合剂市场按配方技术、树脂类型、基材类型、最终用途产业和应用划分-全球预测,2026-2032年

纺织黏合剂市场:黏合剂类型、形态、功能、织物类型、最终用户和分销管道划分-全球预测,2026-2032年黏合剂机器类型、聚合物类型、速度、黏度、应用、最终用途产业和销售管道,全球预测,2026-2032年有机热连接件市场:依产品类型、应用、终端用户产业及通路划分,全球预测(2026-2032年)橡皮筋黏合剂市场按类型、形式、分销管道、应用和最终用户划分,全球预测(2026-2032年)橡胶基材黏合剂市场按配方技术、树脂类型、基材类型、最终用途产业和应用划分-全球预测,2026-2032年 2025-2032年全球涂料、黏合剂和密封剂添加剂(CAS)市场

2025-2032年全球涂料、黏合剂和密封剂添加剂(CAS)市场 全球黏合剂市场:机会与策略展望(至2034年)

全球黏合剂市场:机会与策略展望(至2034年) 卫生黏合剂市场分析及预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、形态、组成、功能、工艺整体包装解决方案市场分析及预测(至2035年):依类型、产品类型、服务、技术、材料类型、应用、製程、最终用户、功能、解决方案划分智慧黏合剂技术市场分析及预测(至2035年):依类型、产品、技术、应用、材料类型、最终用户、功能、製程、形式及解决方案划分

卫生黏合剂市场分析及预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、形态、组成、功能、工艺整体包装解决方案市场分析及预测(至2035年):依类型、产品类型、服务、技术、材料类型、应用、製程、最终用户、功能、解决方案划分智慧黏合剂技术市场分析及预测(至2035年):依类型、产品、技术、应用、材料类型、最终用户、功能、製程、形式及解决方案划分

▼