|

市场调查报告书

商品编码

1693575

义大利营运服务咨询:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Italy Operations Service Consulting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

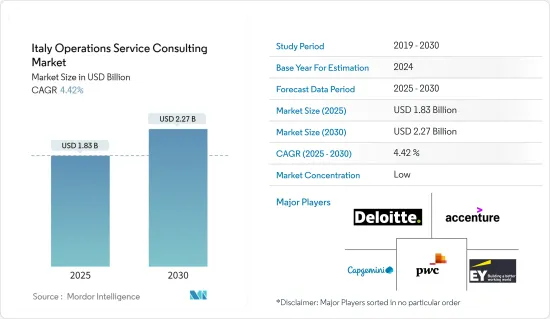

义大利营运服务咨询市场规模预计在 2025 年为 18.3 亿美元,预计到 2030 年将达到 22.7 亿美元,在市场估计和预测期(2025-2030 年)内复合年增长率为 4.42%。

营运管理(有时也称为营运咨询)提供建议和实施服务,以改善公司的内部营运和整个价值链的绩效。

主要亮点

- 由于科技的不断创新和社会的数位化,义大利正处于快速成长时期。为了迎接变化、发现机会、制定新策略、明确计划并执行计划以实现目标,企业需要以营运顾问公司的形式寻求策略合作伙伴。

- 根据最终用户,市场细分为金融服务、製造业、能源和公共产业、公共部门、零售和其他最终用户。 2021年市场占有率为26.91%,其中金融业占据主导地位。 1990 年代,透过合併、收购、资产转移、清算和银行转换,义大利的银行数量大幅减少,这些银行占该国银行资产的 60%。义大利约有1000家银行。义大利政府正在透过多项计画推动银行业整合,以提高其国际竞争力。

- 随着数位化进程,拥有独特经营模式和策略的新企业将不断涌现,对市场产生巨大影响。新的自由职业网站、虚拟网路和专业团队的不断涌现增加了客户可用的选择。大企业与小企业竞争。独立承包商和鬆散的专业网络给小型企业带来了压力。海外人才的涌入甚至迫使独立承包商进入市场。

- 在预测期内,义大利公共部门预计将以健康的速度采用营运服务咨询。透过利用数位技术的颠覆性潜力,公共部门将公民、社区、工人和企业置于进步的核心,为该国的市场供应商创造机会。

- 在 COVID-19 疫情爆发期间,义大利各地的组织采取了一切必要的预防措施,以确保社区和工人的安全。许多组织已经完成了数位转型,并选择了完全远端工作或结合数位和办公室工作的混合模式。此外,新冠疫情的出现使得供应链更加脆弱。对于大多数 IT 公司来说,生态系统很薄弱,由关键业务咨询和服务提供者组成。此外,鼓励远距工作的法规要求服务供应商确保其关键任务企业客户能够使用所需的工具和技术,以确保其所提供服务的速度、安全性、品质和整体效率。

义大利营运服务咨询市场趋势

金融服务业占很大份额

- 影响金融机构的技术的快速进步将越来越要求金融服务公司进行创新、降低营运风险、降低成本、提高客户忠诚度、提高业务绩效、降低营运风险、降低成本并为客户创造引人注目的价值提案。

- 技术和消费行为的改善继续推动义大利付款产业的发展。金融服务公司正在迅速采用营运服务咨询来适应不断变化的付款环境并抓住机会。这将影响零售付款服务、现金管理和付款技术。

- 随着义大利金融服务数位化的提高,来自全球市场的供应商正成为金融改革、重组、转亏为盈和交易的客户。例如,国际顾问公司 FTI Consulting 于 2022 年 6 月扩大了在义大利的企业融资和重组服务范围。几家在义大利营运的市场供应商正在寻求合併和业务,以更好地服务寻求金融服务的客户。

- 此外,新冠疫情也成为义大利银行业进一步数位化的推手。例如,数位管道的使用增加正在改变客户对一站式商店的偏好,即在单一平台上提供他们所需的所有金融服务。例如数位付款、线上保险、网路购物线上付款等。

- Parva Consulting 等提供金融领域咨询服务的区域顾问公司凭藉其创新服务吸引了银行、资产管理和保险业的极大兴趣。 Parva Consulting 分析分销网络并重新设计业务流程,以提高银行业的客户体验和营运效率,从而腾出时间来提高业务品质。

- 根据 Accuris Global 的一项调查,摩根大通是 2021 年义大利最大的併购(M&A) 交易财务顾问公司。该公司总交易额接近 970 亿美元,已成为该国顶级的併购交易顾问。高盛以 910 亿美元的交易量位居第二。

新兴科技投资激增

- 义大利政府正在努力建立新兴企业模式并吸引其他欧洲国家的注意。儘管近期经济环境不佳,但对企业家的支持氛围逐渐增强。义大利曾以高税收闻名。因此,许多义大利人经常离开该国,到更自由和灵活的地方创业。政府致力于透过加强对创新和技术的支持并授权其促进研究和技术转移来结束这种循环。

- 为了促进该地区的新兴企业生态系统,义大利政府推出了一项 10 亿欧元(10.4 亿美元)的投资计划,并成立了一个名为 CDP 创业投资 的新创投机构。 CDP 创业投资管理七种类型的基金,包括加速器基金、创投母基金和「A/B 轮匹配」基金。它还启动了两个加速计划,为小型企业和企业家提供指导、网路和支援服务。

- 新的国家过渡计画4.0是义大利復苏基金的基石。约 240 亿欧元(246 亿美元)将投资于结构性改革,以加强所有扣除率并大幅提高利用率。目的是增加私人投资并为企业提供稳定性和可预测性。

- 义大利于2021年设立了「人工智慧」国家博士学位,这是世界上规模最大、最全面的人工智慧博士学位之一。义大利研究人员是世界上所有主要人工智慧研究网络的成员,包括CLAIRE和ELLIS等最负盛名的欧盟网路。它也是全球人工智慧伙伴关係(GPAI)的创始成员之一。

- 根据义大利经济发展部统计,2021年第一季,义大利商业服务业新创公司9377家,製造业、能源和采矿业新创公司2138家。相较之下,商业服务业的新创企业数量最多,而运输和物流的新创企业数量最少。

义大利营运服务顾问业概况

义大利营运服务咨询市场竞争激烈,由许多全球性和地区性公司组成。这些公司占有相当大的市场占有率,并致力于扩大其全球基本客群。此外,该公司还专注于研发活动、策略联盟和其他有机和无机成长策略,以保持更强的市场地位。

- 2022 年 10 月:安永正式在全球推出面向金融服务的 EY Nexus,这是一项为期三年、投资 100 亿美元的技术、策略和人才计画。随着 EY Nexus 的推出,该公司推出了一个业务转型平台,旨在快速部署金融服务的新产品和解决方案,扩大其技术生态系统的规模。

- 2022 年 9 月:Accenture宣布计画收购世界领先的製造、培训和顾问公司 Stellantis。此次收购将使Accenture能够将世界级製造(WCM)方法融入其客户解决方案中,以帮助提高生产和供应链网路的有效性、永续性和弹性。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 产业影响评估

第五章市场动态

- 市场驱动因素

- 增加对新兴技术的投资

- 采用BI和先进的资料管理策略

- 市场限制

- 咨询市场的变化

- 案例研究: VIS-A-VIS 营运咨询

第六章市场区隔

- 按最终用户

- 金融服务

- 製造业

- 能源与公共产业

- 公共部门

- 零售

- 其他最终用户产业

第七章竞争格局

- 公司简介

- Deloitte Touche Tohmatsu Limited

- Accenture PLC

- PricewaterhouseCoopers LLP

- Ernst & Young ITALY Limited

- Capgemini SE

- KPMG International

- Boston Consulting Group Inc.

- AT Kearney Inc.(Kearney)

- Mckinsey & Company Inc.

- Bain & Company Inc.

- Roland Berger GmbH

- Simon-Kucher & Partners

- OC&C Strategy Consultants

第八章投资分析

第九章:市场的未来

The Italy Operations Service Consulting Market size is estimated at USD 1.83 billion in 2025, and is expected to reach USD 2.27 billion by 2030, at a CAGR of 4.42% during the forecast period (2025-2030).

Operations management sometimes referred to as operations consulting, provides advice and implementation services to improve a company's internal operations and performance across the value chain.

Key Highlights

- Due to continued technological breakthroughs and the digitization of society, Italy is undergoing a rapid growth period. To embrace change, discover opportunities, develop new strategies, articulate a plan, and implement plans to achieve their goals, businesses need strategic partners in the form of operations consulting firms.

- By end-user, the market is divided into financial services, manufacturing, energy and utilities, the public sector, retail, and other end users. With a share of 26.91%, the financial industry controlled most of the market in 2021. Due to bank mergers, acquisitions, asset transfers, liquidations, and conversions that accounted for 60% of all banking assets in the nation throughout the 1990s, the number of banks in Italy has drastically declined. There are about a thousand banks in Italy. The government is promoting consolidation through several programs to make the Italian banking sector more competitive abroad.

- The market is greatly impacted by increased digitization since it makes it possible for new businesses to emerge with unique business models and strategies. The ongoing appearance of new freelancing websites, virtual networks, and specialty teams has increased the options available to clients. Greater firms compete with smaller ones. Independent contractors and loosely established expert networks put a strain on smaller enterprises. Due to the influx of overseas talent, even independent contractors are under pressure to enter the market.

- Over the forecast period, the public sector in Italy is anticipated to adopt operations consulting services at a healthy rate. Public sector organizations are keeping citizens, communities, workers, and businesses at the center of progress by utilizing the disruptive potential of digital technologies, which opens up opportunities for market vendors in the nation.

- Organizations around Italy took all required precautions to safeguard the safety of communities and workers due to the COVID-19 outbreak. Many organizations finished their digital transformation and have chosen to operate entirely remotely or in a hybrid model that combines digital and in-office work. In addition, the emergence of COVID-19 has made supply chains more vulnerable. For the majority of IT firms, the ecosystem is fragile and comprises important operations consulting service providers. Mandates encouraging remote work have also prompted service providers to guarantee that mission-critical corporate clients have access to the tools and technology required to allow the speed, security, quality, and overall effectiveness of services offered.

Italy Operations Service Consulting Market Trends

Financial Service Sector to Hold Significant Share

- Due to the quick technological advancements affecting financial institutions, financial services companies will increasingly need to innovate, reduce operational risk, cut costs, increase customer loyalty, improve business performance, reduce operational risk, reduce costs, and create compelling value propositions for their clients.

- Improvements in technology and consumer behavior continue to propel the development of the payments sector in Italy. Financial services companies are quickly introducing operations consulting services to stay up with the changing payment landscape and seize the possibilities. This has ramifications for retail payments services, cash management, and payments technology.

- Global market vendors are customers for financial transformations, restructurings, turnarounds, and transactions in Italy because of the country's growing digitalization of financial services. For instance, the international consulting company FTI Consulting extended its corporate finance and restructuring service offerings in Italy in June 2022. Several market vendors operating in Italy are engaging in merger and collaboration operations to offer better services to their clients who want financial services.

- Furthermore, the COVID-19 pandemic has driven the banking sector in Italy to undergo significant digital transformation. For instance, the usage of digital channels has increased, along with changing customer preferences toward a one-stop shop with a single platform for obtaining all necessary financial services. Examples include digital payments, online insurance, online payments for online shopping, etc.

- Regional consulting companies like Parva Consulting, which provides consulting services in the financial sector, are attracting much interest from the banking, asset management, and insurance industries with their creative services. To improve customer experience and sales effectiveness in banking, the organization analyses distribution networks and redesigns operational procedures to free up commercial quality time.

- As per research by Acuris Global, JPMorgan was Italy's top financial advisory company for merger and acquisition (M&A) agreements in 2021. With a total deal value close to USD 97 billion, the company became the top advisor to M&A deals in the nation. Goldman Sachs & Co. is placed second in the leaderboard with a deal value of USD 91 billion.

Surged Investment Trends in Emerging Technologies

- The Italian government is working hard to build up its start-up model and draw the rest of Europe's attention to it. Despite the unfavorable recent economic climate, the atmosphere is evolving to support entrepreneurs. Italy used to be known for having high taxes. Hence, many Italians would regularly leave the nation to start their enterprises in places with more freedom and flexibility. The government has been focusing on ending this cycle by increasing its support for innovation and technology and granting greater power to advance research and tech transfer.

- To boost the regional start-up ecosystem, the Italian government introduced a EUR 1 billion (USD 1.04 billion) investment program and established a new venture arm named CDP Venture Capital. This manages seven different funds, including an accelerator fund, a VC fund-of-funds, and "Series A/B matching" funds. It also launched two acceleration programs to provide SMEs and entrepreneurs mentorship, networking, and support services.

- The new National Transition Plan 4.0 serves as the foundation for the Italian Recovery Fund. About EUR 24 billion (USD 24.6 billion) is being invested in a structural change that strengthens all deduction rates and significantly increases usage. It aims to increase private investment and provide businesses with stability and predictability.

- One of the world's biggest and most comprehensive artificial intelligence doctorates, the National Doctorate in "Artificial Intelligence" was launched in Italy in 2021. Italian academics are participating in all key worldwide AI research networks, including the most prestigious EU networks, such as CLAIRE and ELLIS. It is also one of the founding members of the Global Partnership on Artificial Intelligence (GPAI).

- According to the Ministry of Economics Development, the number of business services start-ups in Italy for 1Q 2021 was 9,377. There were 2,138 new start-ups in the manufacturing activities, energy, and mining sector. Business services had the highest number of start-ups, in contrast to transportation and logistics, which had the lowest.

Italy Operations Service Consulting Industry Overview

The Italian operations service consulting market is highly competitive and consists of many global and regional players. These players account for a considerable market share and focus on expanding their global client base. They focus on research and development activities, strategic alliances, and other organic and inorganic growth strategies to stay stronger in the market.

- October 2022: Ernst & Young unveiled the worldwide official launch of EY Nexus for financial services, a three-year, USD 10 billion investment in technology, strategy, and people. With the launch of EY Nexus, the company has expanded the amount of its technological ecosystem by introducing a business transformation platform intended to deploy new products and solutions quickly for financial services.

- September 2022: Accenture announced its plan to acquire Stellantis, a world-class manufacturing, training, and consulting business. By way of this takeover, Accenture could include the World Class Manufacturing (WCM) approach into its solutions for customers, assisting them in improving the effectiveness, sustainability, and resilience of their production and supply chain networks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Investment in Emerging Technologies

- 5.1.2 Adoption of BI and Advanced Data Management Strategies

- 5.2 Market Restraints

- 5.2.1 Shift in the Consulting Marketplace

- 5.3 Case Studies VIS-A-VIS Operations Consultancy

6 MARKET SEGMENTATION

- 6.1 By End-user

- 6.1.1 Financial Services

- 6.1.2 Manufacturing

- 6.1.3 Energy and Utilities

- 6.1.4 Public Sector

- 6.1.5 Retail

- 6.1.6 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Deloitte Touche Tohmatsu Limited

- 7.1.2 Accenture PLC

- 7.1.3 PricewaterhouseCoopers LLP

- 7.1.4 Ernst & Young ITALY Limited

- 7.1.5 Capgemini SE

- 7.1.6 KPMG International

- 7.1.7 Boston Consulting Group Inc.

- 7.1.8 A. T. Kearney Inc. (Kearney)

- 7.1.9 Mckinsey & Company Inc.

- 7.1.10 Bain & Company Inc.

- 7.1.11 Roland Berger GmbH

- 7.1.12 Simon-Kucher & Partners

- 7.1.13 OC&C Strategy Consultants