|

市场调查报告书

商品编码

1850011

语音分析:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Speech Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

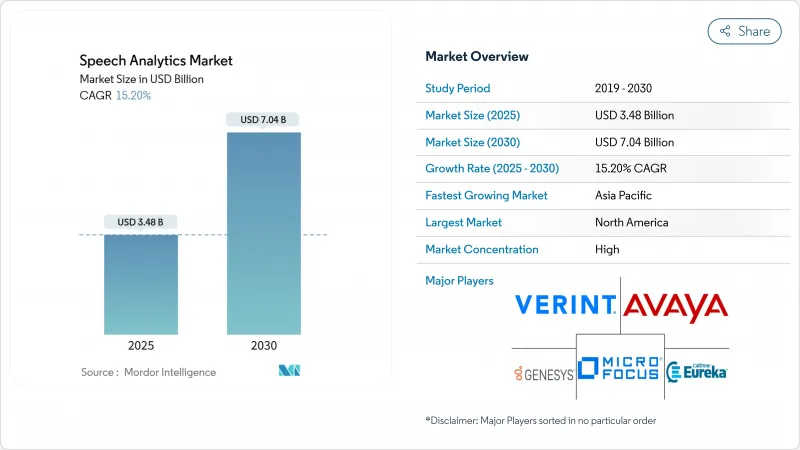

预计语音分析市场规模到 2025 年将达到 34.8 亿美元,到 2030 年将达到 70.4 亿美元,复合年增长率为 15.20%。

云端优先的客户经验计划、超过 95% 的人工智慧转录准确率,以及将语音资料列为董事会优先事项的端到端合规性要求,正在蓬勃发展。领先的供应商持续将语音分析嵌入更广泛的客户经验套件中,包括销售、合规和经营团队决策职能,以及品质保证团队。随着大型科技公司将分析嵌入其云端生态系,而专业的新兴企业则优先考虑即时座席协助和产业就绪的语言模型,竞争格局正在加剧。这种转变正在加速云端的采用,并增加对实施服务的需求,惠及越来越多先前缺乏投资资源的中小型企业。

全球语音分析市场趋势与洞察

云端优先 CX 转型加速分析采用

将客服中心工作负载迁移到云端的公司不再只是分析敷衍的呼叫样本,而是会审查每一次互动,创建用于模式识别和主动服务改进的大型资料集。资本支出障碍正在消退,这使得中型企业无需漫长的采购週期即可采用高级分析技术。供应商正在将语音分析捆绑到整合的客户体验 (CX) 套件中,从而简化工作流程整合并加快部署时间。这种转变也推动了基于消费的定价,为那些更重视营运预算而非资本预算的小型团队开启了语音分析市场。随着云端生态系的成熟,与意图预测和情绪评分等相关人工智慧服务的整合将成为承包,从而加速了整个企业的采用。

人工智慧驱动的转录准确性解锁了整个企业的用例

低于 4% 的单字错误率已将语音分析从品质保证工具转变为策略性业务系统。更高的准确率支持情绪检测、即时座席指导以及高度监管行业的自动化合规性检查。深度学习模型现在只需极少的调整即可处理方言、嘈杂环境和特定领域的术语,从而降低营运成本。企业正在将语音分析扩展到销售支援和高阶主管级沟通分析,从而提升价值获取。这项技术飞跃将语音分析定位为对话智慧平台的基础,该平台将语音、文字和视讯资料整合到单一分析层。

实施成本是采用的障碍

许可成本、语言模型训练和整合服务持续对中端市场预算造成压力,导致计划延期并限制其发展范围。许多公司低估了产品词彙不断发展变化过程中持续优化所需的人工时长。云端订阅减轻了资本投入,但并不能消除对熟练分析师将洞察转化为流程变革的需求。儘管基础设施价格下降,但由于语音分析在 CRM、劳动力管理和合规性归檔等多个系统中的应用,对专业服务的需求仍然高涨。供应商正在透过打包加速器和自动配置嚮导来弥补这一缺口,但总体拥有成本仍然是初期采用的障碍。

細項分析

2024年,组件解决方案市场规模为21.3亿美元,占61.20%。然而,随着企业意识到精准洞察依赖专家整合、客製化模型训练和工作流程重新设计,服务正在缩小这一差距。从2025年到2030年,由于企业更重视可操作的成果而非功能清单,服务收入预计将达到19.50%的复合年增长率,并超过产品收入。

顾问公司和託管服务提供者正在将分析结果与关键绩效指标 (KPI) 相结合,这进一步推动了语音分析市场从以工具为中心转向以价值为中心的销售模式。随着云端技术应用的加速,客户正在寻求合作伙伴来迁移历史语音檔案、配置安全控制并提供变更管理支援。这些因素共同作用,将服务从可选的附加元件转变为关键的采购驱动因素,尤其对于缺乏内部资料科学人才的公司。

受传统投资以及金融和医疗保健领域严格的资料主权法规的推动,本地部署架构在2024年将维持60.40%的份额。然而,云端订阅量将以21.00%的复合年增长率成长,这表明企业将向弹性、频繁的功能更新和简化的整合转变。

随着供应商将即时分析、储存和 AI 模型更新捆绑到计量收费定价模式中,云端语音分析的市场规模正在不断扩大。资本预算有限的中型企业欢迎这种转变,而跨国企业则青睐能够在无需重复基础设施的情况下实现跨区域标准化的能力。超大规模提供者提供的合规认证缓解了监管阻力,进一步推动了这一转变。

语音分析技术市场按组件(解决方案、服务)、部署(本地部署、云端/SaaS)、组织规模(中小企业、大型企业)、应用(客户体验管理、通话监控和品管等)、最终用户行业(BFSI、IT 和通讯、医疗保健等)和地区细分。市场预测以美元计算。

区域分析

到2024年,北美将以45.00%的语音分析市场份额位居第一,这得益于其成熟的云端生态系、较高的数位服务采用率以及金融和医疗保健领域严格的合规要求。持续的投资重点是全通路旅程分析和即时座席辅助工具,这两者都依赖低延迟转录和情绪评分。尤其是美国公司,他们正在投入更多预算,将其传统的客服中心转型为支援人工智慧的互动中心,以巩固其在该地区的领导地位。

亚太地区是成长最快的地区,以中国、日本和印度主导,预计到2030年的复合年增长率将达到19.00%。政府支持的人工智慧专案和服务业外包的快速扩张为云端原生部署创造了肥沃的土壤。中国的银行正在将语音分析技术融入其超级应用,日本的保险公司正在利用它来应对劳动力的萎缩,而印度的BPO公司则正在采用语音分析技术来监控多语言队列中的代理品质。随着本地供应商与全球合作伙伴合作实现语言模型的在地化,高成长产业的应用正在加速。

欧洲位于两者之间,严格的资料保护法规限制了重要的商业机会。 GDPR合规性正在推动对自动化同意管理、重新导向和区域资料驻留的解决方案的需求。英国在语音分析方面的应用处于领先地位,其次是德国和法国,这两个国家都应用语音分析来区分拥挤的零售和通讯市场的客户服务。西班牙语音广告支出的激增凸显了人们对语音管道智慧日益增长的商业性兴趣,并预示着其将在欧洲大陆的企业中广泛应用。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 客服中心的云端优先 CX 转型

- AI即时转录准确率:95%以上

- 监管要求100%遵守通话记录

- 全通路分析套件(语音+文字+影片)

- CCaaS 市场上销售的「代理辅助」微应用激增

- 通讯业者的 5G 网路公共 API,实现低延迟边缘分析

- 市场限制

- 实施和客製化调整成本高

- 资料隐私问题(GDPR、CPRA、PCI-DSS)

- 低资源语言中缺乏註释的特定领域语音

- 使用合成语音重新训练大规模 LLM 时模型崩坏的风险

- 监管格局

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模与成长预测(价值)

- 按组件

- 解决方案

- 服务

- 按部署模型

- 本地部署

- 云/SaaS

- 按组织规模

- 大公司

- 小型企业

- 按用途

- 客户经验管理

- 通话监控和品管

- 风险与合规管理

- 销售和行销情报

- 按最终用户产业

- BFSI

- 通讯/IT

- 卫生保健

- 零售与电子商务

- 政府和公共部门

- 旅游与饭店

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- NICE Ltd.

- Verint Systems Inc.

- Avaya Inc.

- Genesys Telecommunications Laboratories Inc.

- Micro Focus International PLC

- CallMiner Inc.

- Calabrio Inc.

- OpenText Corp.

- Talkdesk Inc.

- AWS(Amazon Transcribe/Contact Lens)

- Google Cloud(Contact Center AI and Speech-to-Text)

- IBM(Watson Speech Services)

- Uniphore

- Clarabridge(Qualtrics)

- Observe.AI

- LiveVox Holdings Inc.

- Cogito Corp.

- VoiceBase Inc.(LivePerson Inc.)

- Raytheon BBN Technologies

- CallRail Inc.

第七章 市场机会与未来展望

The speech analytics market is valued at USD 3.48 billion in 2025 and is projected to reach USD 7.04 billion by 2030, advancing at a 15.20% CAGR.

Momentum is building around cloud-first customer-experience programs, AI transcription accuracy above 95%, and end-to-end compliance demands that now make voice data a board-level priority. Leading vendors continue to embed speech analytics in broader customer-experience suites, pushing adoption beyond quality-assurance teams into sales, compliance, and executive decision-making functions. Competitive intensity is rising as technology giants fold analytics into their cloud ecosystems, while specialist start-ups emphasise real-time agent assist and industry-ready language models. These shifts are accelerating cloud deployments, fuelling demand for implementation services, and widening the addressable base of small and mid-sized enterprises that previously lacked the resources to invest.

Global Speech Analytics Market Trends and Insights

Cloud-First CX Transformation Accelerates Analytics Adoption

Organisations migrating contact-centre workloads to the cloud are no longer analysing a token sample of calls; they now review every interaction, creating larger datasets for pattern recognition and proactive service improvements. Capital-expense barriers have receded, enabling mid-market firms to deploy advanced analytics without long procurement cycles. Vendors are bundling speech analytics into unified CX suites, smoothing workflow integration and cutting implementation timelines. This shift also promotes consumption-based pricing, opening the speech analytics market to smaller teams that prefer operational over capital budgets. As cloud ecosystems mature, integration with adjacent AI services such as intent prediction and sentiment scoring becomes turnkey, accelerating enterprise-wide adoption.

AI-Powered Transcription Accuracy Unlocks Enterprise-Wide Use Cases

Word-error rates below 4% have turned speech analytics from a quality-assurance tool into a strategic business system. Higher accuracy supports sentiment detection, real-time agent coaching, and automated compliance checks in heavily regulated industries. Deep-learning models now handle dialects, noisy environments, and domain-specific terminology with minimal human tuning, reducing operational costs. Enterprises extend speech analytics to sales enablement and executive-level communication analysis, broadening value capture. This technical leap positions speech analytics as a foundation for conversational intelligence platforms that fuse voice, text, and video data into a single analytic layer.

Implementation Costs Create Adoption Barriers

Licensing fees, language-model training, and integration services still strain mid-market budgets, delaying projects and limiting scope. Many firms underestimated the staff hours required for continuous optimisation as product vocabularies evolve. Cloud subscriptions ease capital commitments but do not eliminate the need for skilled analysts who translate insights into process changes. Despite falling infrastructure prices, professional-services demand remains high because speech analytics deployments touch multiple systems, including CRM, workforce management, and compliance archives. Vendors address the gap with packaged accelerators and automated configuration wizards, yet total cost of ownership remains a gating factor for first-time adopters.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Compliance Drives Comprehensive Call Recording

- Omnichannel Analytics Creates Unified Journey Insights

- Data-Privacy Regulations Complicate Implementation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The speech analytics market size for component solutions stood at USD 2.13 billion in 2024, reflecting a 61.20% share that underscores the centrality of core technology to adoption cycles. Services, however, are closing the gap as organisations recognise that accurate insights depend on specialised integration, custom model training, and workflow redesign. Between 2025 and 2030, service revenue is expected to log a 19.50% CAGR, outpacing product sales as enterprises prioritise actionable outcomes over feature checklists.

Consultancies and managed-service providers align analytics outputs with key performance indicators, reinforcing the speech analytics market's shift from tool-centric to value-centric selling. As cloud deployments accelerate, customers lean on partners to migrate historical audio archives, configure security controls, and provide change-management support. These factors collectively elevate services from an optional add-on to a decisive purchase driver, especially among firms lacking in-house data science talent.

On-premise architectures retained a 60.40% speech analytics market share in 2024, supported by legacy investments and stringent data-sovereignty rules in finance and healthcare. Yet cloud subscriptions are growing at a 21.00% CAGR, signalling a decisive pivot toward elasticity, frequent feature updates, and simplified integrations.

The speech analytics market size for cloud deployments is swelling as vendors bundle real-time analytics, storage, and AI model updates into pay-as-you-go tiers. Mid-market organisations with limited capital budgets welcome the shift, while global enterprises favour the ability to standardise across regions without duplicating infrastructure. Regulatory resistance is easing as hyperscale providers earn compliance certifications, further boosting migration momentum.

Speech Analytics Technology Market is Segmented by Component (Solutions, Services), Deployment (On-Premise, Cloud/SaaS), Organization Size (Small and Medium Enterprises, Large Enterprises), Application (Customer Experience Management, Call Monitoring and Quality Management and More), End-User Industry (BFSI, Telecommunications and IT, Healthcare and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America ranked first with 45.00% speech analytics market share in 2024, anchored by mature cloud ecosystems, high digital-service penetration, and strict compliance mandates in finance and healthcare. Ongoing investments focus on omnichannel journey analytics and real-time agent-assist tools, both of which rely on low-latency transcription and sentiment scoring. United States enterprises, in particular, allocate larger budgets to transform legacy contact centres into AI-enabled engagement hubs, extending the region's leadership position.

APAC is the fastest-growing territory with a projected 19.00% CAGR to 2030, led by China, Japan, and India. Government-backed AI programmes and rapid expansion of service-sector outsourcing create fertile ground for cloud-native deployments. Chinese banks embed voice analytics into super-apps, Japanese insurers use it to counter shrinking workforces, and Indian BPOs adopt it to monitor agent quality across multilingual queues F5. Local vendors collaborate with global partners to localise language models, accelerating adoption across high-growth industries.

Europe sits between the two, with substantial opportunity tempered by data-protection stringency. GDPR compliance drives demand for solutions that automate consent management, redaction, and regional data residency. The United Kingdom leads adoption, followed by Germany and France, each applying speech analytics to differentiate customer service in crowded retail and telecom markets. Spain's surge in voice-ad-spend underscores growing commercial interest in voice-channel intelligence, foreshadowing broader uptake across continental enterprises.

- NICE Ltd.

- Verint Systems Inc.

- Avaya Inc.

- Genesys Telecommunications Laboratories Inc.

- Micro Focus International PLC

- CallMiner Inc.

- Calabrio Inc.

- OpenText Corp.

- Talkdesk Inc.

- AWS (Amazon Transcribe / Contact Lens)

- Google Cloud (Contact Center AI and Speech-to-Text)

- IBM (Watson Speech Services)

- Uniphore

- Clarabridge (Qualtrics)

- Observe.AI

- LiveVox Holdings Inc.

- Cogito Corp.

- VoiceBase Inc. (LivePerson Inc.)

- Raytheon BBN Technologies

- CallRail Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first CX transformation in contact centers

- 4.2.2 AI-powered real-time transcription accuracy ?95 %

- 4.2.3 Regulatory demand for 100 % call?record compliance

- 4.2.4 Omnichannel analytics bundling (speech + text + video)

- 4.2.5 Surge in "agent assist" micro-apps sold via CCaaS marketplaces

- 4.2.6 Telco 5G network-exposed APIs enabling low-latency edge analytics

- 4.3 Market Restraints

- 4.3.1 High implementation and custom-tuning costs

- 4.3.2 Data-privacy concerns (GDPR, CPRA, PCI-DSS)

- 4.3.3 Scarcity of annotated domain-specific audio in low-resource languages

- 4.3.4 Model collapse risks when large LLMs retrain on synthetic speech

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud / SaaS

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Application

- 5.4.1 Customer Experience Management

- 5.4.2 Call Monitoring and Quality Management

- 5.4.3 Risk and Compliance Management

- 5.4.4 Sales and Marketing Intelligence

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Telecommunications and IT

- 5.5.3 Healthcare

- 5.5.4 Retail and E-commerce

- 5.5.5 Government and Public Sector

- 5.5.6 Travel and Hospitality

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Israel

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NICE Ltd.

- 6.4.2 Verint Systems Inc.

- 6.4.3 Avaya Inc.

- 6.4.4 Genesys Telecommunications Laboratories Inc.

- 6.4.5 Micro Focus International PLC

- 6.4.6 CallMiner Inc.

- 6.4.7 Calabrio Inc.

- 6.4.8 OpenText Corp.

- 6.4.9 Talkdesk Inc.

- 6.4.10 AWS (Amazon Transcribe / Contact Lens)

- 6.4.11 Google Cloud (Contact Center AI and Speech-to-Text)

- 6.4.12 IBM (Watson Speech Services)

- 6.4.13 Uniphore

- 6.4.14 Clarabridge (Qualtrics)

- 6.4.15 Observe.AI

- 6.4.16 LiveVox Holdings Inc.

- 6.4.17 Cogito Corp.

- 6.4.18 VoiceBase Inc. (LivePerson Inc.)

- 6.4.19 Raytheon BBN Technologies

- 6.4.20 CallRail Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2025年全球语音分析市场报告

2025年全球语音分析市场报告 2025 年至 2033 年语音分析市场报告(按类型、部署、企业规模、最终用途和地区)日本语音分析市场报告(按类型、部署模式、企业规模、最终用户和地区)2025 年至 2033 年

2025 年至 2033 年语音分析市场报告(按类型、部署、企业规模、最终用途和地区)日本语音分析市场报告(按类型、部署模式、企业规模、最终用户和地区)2025 年至 2033 年 语音分析市场规模、份额和成长分析(按组件、企业规模、部署模式、应用、最终用户和地区)- 产业预测 2025-2032

语音分析市场规模、份额和成长分析(按组件、企业规模、部署模式、应用、最终用户和地区)- 产业预测 2025-2032 市场占有率与预测:语音分析,2023~2028年,世界规模(2份报告套装)

市场占有率与预测:语音分析,2023~2028年,世界规模(2份报告套装) 北美语音分析:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲语音分析:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

北美语音分析:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲语音分析:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 全球语音分析市场规模、份额和趋势分析:按部署类型、组件、应用程式、公司规模、行业和地区分類的展望和预测(2024-2031)

全球语音分析市场规模、份额和趋势分析:按部署类型、组件、应用程式、公司规模、行业和地区分類的展望和预测(2024-2031) 语音分析市场:按组件、类型、通路、组织规模、部署、最终用户 - 2025-2030 年全球预测

语音分析市场:按组件、类型、通路、组织规模、部署、最终用户 - 2025-2030 年全球预测 语音分析市场规模、份额和趋势分析报告:2024-2030 年按组件、部署、公司规模、行业、地区和细分市场进行的预测

语音分析市场规模、份额和趋势分析报告:2024-2030 年按组件、部署、公司规模、行业、地区和细分市场进行的预测