|

市场调查报告书

商品编码

1851217

印度金融科技:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)India Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

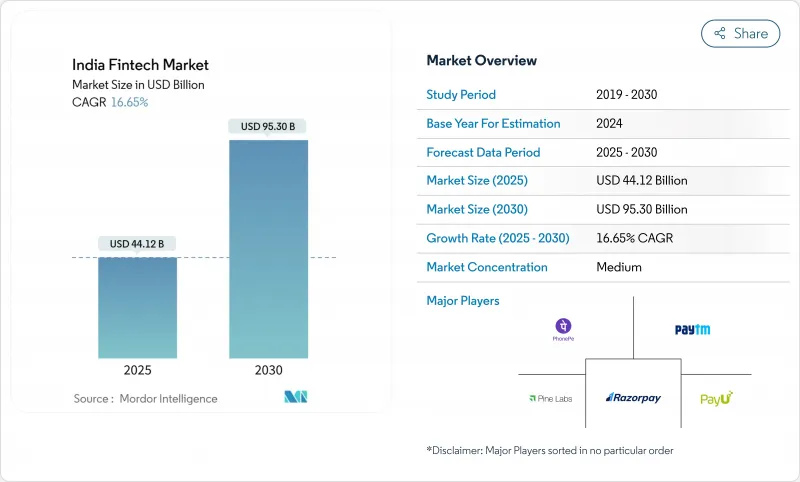

印度金融科技市场预计到 2025 年将达到 441.2 亿美元,到 2030 年将扩大到 953 亿美元,从 2025 年到 2030 年的复合年增长率将达到 16.65%。

政府的持续支持、价格合理的行动数据以及诸如UPI和Aadhaar等无缝衔接的公共数位基础设施,正在扩大服务覆盖范围、降低交付成本并促进产品创新。智慧型手机的快速普及持续扩大着潜在用户群体,而千禧世代和Z世代的财富累积则推动了对数位投资和信贷产品的需求。随着以支付为主导的超级应用拓展至贷款、保险和财富管理领域,竞争依然激烈;同时,专业企业也在高端信贷、零工经济和跨境支付等领域开闢了盈利的细分市场。来自二、三线城市的竞争者不断涌入,以及国际UPI整合的日益普及,正在从根本上拓展各个客户群和地区的成长机会。

印度金融科技市场趋势与洞察

政府建设的数位公共基础设施加速了大众市场的普及。

到2024年11月,UPI月交易量将超过150亿笔,交易额达2,800亿美元。基于Aadhaar的电子身分验证(eKYC)已将註册成本从15-20美元降至0.5美元,使服务提供者能够为低收入用户提供更多服务。目前,超过5.08亿印度人透过JAM三者(支付、贷款和保险)获得正规金融服务,扩大了印度在支付、贷款和保险领域的金融科技市场。超过4,270亿美元的直接福利转移已为日常交易搭建了数位化轨道。开放且可互通的架构降低了私人企业的整合阻力,进而促进了产品发布和跨产业合作。

帐户聚合框架释放资料主导的信任

自2021年推出以来,AA系统实现了基于用户同意的检验财务记录共用,使贷款机构能够对没有正式信用记录的借款人进行信用评分。预计到2025年,该系统将为小型企业和零售客户提供近3000亿美元的信贷额度。取得公用事业收费帐单和交易资料的能力缩短了核准时间并降低了违约风险。政策制定者将AA视为未来数位信贷体系的基石,该体系旨在平衡创新与消费者保护。

印度储备银行收紧数位贷款和外国贷款开发许可(FLDG)规则将增加合规成本。

2022年颁布、2023年更新的法规强制要求借款人与受监管实体之间进行直接资金流动,详细揭露年利率,并将贷款组合的贷款损失保障上限设定为5%。合规支出增加了15%至20%,给中小型金融机构带来了压力。强制性的冷静期和资料保留要求促使企业重新评估短期产品,延缓了扩张计划,并降低了印度金融科技市场的盈利。

细分市场分析

到2024年,数位支付将占印度金融科技市场份额的42.9%,这主要得益于2024财年1,310亿笔UPI交易的强劲成长。随着智慧型手机普及率的不断提高和商家接受度的提升,即使收入模式转向附加价值服务,该领域预计仍将保持高速成长。产业巨头正透过整合信贷、保险和财富管理产品来加深客户互动,从而延长客户生命週期并提高每位客户的利润率。随着全球科技巨头、银行和本土企业竞相争夺每日交易流量,竞争日益激烈。

预计到2030年,在所有提案中,新银行的复合年增长率将达到19.62%,成为成长最快的领域。纯数位银行正与持牌银行合作,为自由工作者和小型企业提供全端式行动帐户、自动化预算和另类贷款服务。随着法律规范的完善和应用程式介面(API)的标准化,新银行的服务对象将不再局限于都市区精英,而是扩展到更广泛的群体,提供本地化的介面和针对特定细分市场的服务。新银行不断扩大的基本客群,加上其较低的营运成本,正稳步提升对印度金融科技市场规模的贡献。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府兴建的数位公共基础设施(UPI、Aadhaar、OCEN)将加速大众市场的普及。

- 帐户聚合框架:解锁资料主导的信用承销

- 电子商务与零工经济平台嵌入式的金融需求

- 消费税实施后,中小企业正规化将催生新的中小企业金融科技需求池。

- 千禧世代和Z世代的财富累积推动了低成本智能投顾的发展

- 跨境UPI合作(新加坡、阿联酋等)开闢了新的汇款收入来源。

- 市场限制

- 印度储备银行收紧数位借贷和外国贷款开发许可证(FLDG)监管,导致合规成本上升。

- 零商家折扣率政策将压缩付款闸道的利润池。

- 网路诈骗案件的不断增加削弱了消费者信心

- 从2022年起,冬季资金短缺将限制规模化资金的资金筹措。

- 价值/供应链分析

- 监理与技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 投资/基金趋势分析

第五章 市场规模与成长预测

- 按服务方案

- 数位支付

- 数位借贷

- 数位投资

- 保险科技

- 新银行

- 最终用户

- 零售

- 商业

- 透过使用者介面

- 行动应用

- 网页/浏览器

- POS/物联网设备

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Paytm(One97 Communications Ltd)

- PhonePe Pvt Ltd

- Razorpay Software Pvt Ltd

- Pine Labs Pvt Ltd

- PayU Payments Pvt Ltd

- BharatPe(Resilient Innovations Pvt Ltd)

- MobiKwik(One MobiKwik Systems Ltd)

- PolicyBazaar(PB Fintech Ltd)

- Zerodha Broking Ltd

- Upstox(RKSV Securities India Pvt Ltd)

- Groww(Nextbillion Technology Pvt Ltd)

- Cred Financial Technologies Pvt Ltd

- Slice(GaragePreneurs Internet Pvt Ltd)

- KreditBee(Finnov Pvt Ltd)

- Lendingkart Finance Ltd

- Capital Float(Axio Digital)

- NeoGrowth Credit Pvt Ltd

- Navi Technologies Ltd

- Jupiter(Amica Finance Pvt Ltd)

- NIYO Solutions Pvt Ltd

第七章 市场机会与未来展望

The India fintech market is valued at USD 44.12 billion in 2025 and is forecasted to advance to USD 95.30 billion by 2030, translating into a solid 16.65% CAGR during 2025-2030.

Consistent government backing, inexpensive mobile data, and seamless digital public infrastructure such as UPI and Aadhaar are widening access, compressing delivery costs, and encouraging product innovation. Rapid gains in smartphone penetration continue to expand the total addressable population, while millennial and Gen-Z wealth creation fuels demand for investment and credit products that are digital first. Competition remains intense as payments-led super-apps move laterally into lending, insurance, and wealth, and as specialist challengers carve profitable niches in premium credit, gig-worker finance, and cross-border payments. Rising participation from Tier II and Tier III cities, together with international UPI linkages, signals a structural broadening of growth opportunities across customer segments and geographies.

India Fintech Market Trends and Insights

Government-Built Digital Public Infrastructure Accelerating Mass-Market Adoption

Monthly UPI volumes exceeded 15 billion in November 2024, moving USD 280 billion in value. Aadhaar-enabled eKYC has cut onboarding costs from USD 15-20 to USD 0.5, allowing providers to serve low-income users profitably. More than 508 million Indians now access formal financial services through the JAM trinity, enlarging the India fintech market pool for payments, lending, and insurance. Direct benefit transfers delivered over USD 427 billion have entrenched digital rails in everyday transactions. The open, interoperable architecture reduces integration friction for private players, which in turn spurs product launches and cross-sector collaborations.

Account Aggregator Framework Unlocking Data-Driven Credit

Since its launch in 2021, the AA system has enabled consent-based sharing of verified financial records, allowing lenders to score borrowers who lack formal histories. By 2025, it is set to channel credit flows nearing USD 300 billion to MSMEs and retail customers. The ability to pull utility-bill and transaction data cuts approval times and lowers default risk, underpinning the expansion of digital lending platforms within the India fintech market. Policy makers view AA as a cornerstone for future digital credit rails that balance innovation with consumer protection.

RBI's Stricter Digital-Lending & FLDG Norms Raising Compliance Cost

Regulations issued in 2022 and updated in 2023 require direct fund flows between borrowers and regulated entities, detailed APR disclosures, and caps on default-loss guarantees at 5% of loan portfolios. Compliance spending has climbed 15-20%, squeezing smaller lenders. Cooling-off windows and data-storage mandates have prompted revisions to short-term products, slowing expansion plans and trimming profitability in the India fintech market.

Other drivers and restraints analyzed in the detailed report include:

- Embedded-Finance Demand from E-commerce and the Gig Economy

- Formalization of MSMEs Post-GST: Creating New Demand Pools

- Zero-MDR Policy Compressing Payment-Gateway Profit Pools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital payments accounted for 42.9% of India's fintech market share in 2024, underpinned by 131 billion UPI transactions in FY24. Continued smartphone adoption and merchant acceptance are expected to keep the segment on a high-growth track, even as revenue models shift toward value-added services. Industry incumbents deepen engagement by layering credit, insurance, and wealth products, thereby lengthening user lifecycles and raising per-customer margins. Competitive intensity remains elevated as global tech giants, banks, and home-grown players fight for daily transaction flow.

Neobanking is projected to post a 19.62% CAGR through 2030, the fastest among all propositions. Digital-only challengers partner with licensed banks to offer full-stack mobile accounts, automated budgeting, and alternative lending for freelancers and MSMEs. As regulatory frameworks mature and APIs standardize, neobanks expand beyond urban elites into vernacular interfaces and segment-specific offerings. The widening customer base, combined with low overheads, positions neobanks to steadily lift their contribution to the India fintech market size.

The India Fintech Market is Segmented by Service Proposition (Digital Payments, Digital Lending and Financing, Digital Investments, Insurtech, and Neobanking), by End-User (Retail and Businesses), and by User Interface (Mobile Applications, Web / Browser, and POS / IoT Devices). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Paytm (One97 Communications Ltd)

- PhonePe Pvt Ltd

- Razorpay Software Pvt Ltd

- Pine Labs Pvt Ltd

- PayU Payments Pvt Ltd

- BharatPe (Resilient Innovations Pvt Ltd)

- MobiKwik (One MobiKwik Systems Ltd)

- PolicyBazaar (PB Fintech Ltd)

- Zerodha Broking Ltd

- Upstox (RKSV Securities India Pvt Ltd)

- Groww (Nextbillion Technology Pvt Ltd)

- Cred Financial Technologies Pvt Ltd

- Slice (GaragePreneurs Internet Pvt Ltd)

- KreditBee (Finnov Pvt Ltd)

- Lendingkart Finance Ltd

- Capital Float (Axio Digital)

- NeoGrowth Credit Pvt Ltd

- Navi Technologies Ltd

- Jupiter (Amica Finance Pvt Ltd)

- NIYO Solutions Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Built Digital Public Infrastructure (UPI, Aadhaar, OCEN) Accelerating Mass-Market Adoption

- 4.2.2 Account Aggregator Framework Unlocking Data-Driven Credit Underwriting

- 4.2.3 Embedded-Finance Demand from E-commerce & Gig-Economy Platforms

- 4.2.4 Formalization of MSMEs post-GST Creating New SME Fintech Demand Pools

- 4.2.5 Millennial & Gen-Z Wealth Creation Driving Low-Cost Robo-Advisory Uptake

- 4.2.6 Cross-Border UPI Linkages (e.g., Singapore, UAE) Opening New Remittance Revenues

- 4.3 Market Restraints

- 4.3.1 RBI's Stricter Digital-Lending & FLDG Norms Raising Compliance Cost

- 4.3.2 Zero-MDR Policy Compressing Payment-Gateway Profit Pools

- 4.3.3 Escalating Cyber-Fraud Incidents Undermining Consumer Trust

- 4.3.4 Post-2022 Funding Winter Constraining Scale-Up Capital

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment & Funding Trend Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending and Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Paytm (One97 Communications Ltd)

- 6.4.2 PhonePe Pvt Ltd

- 6.4.3 Razorpay Software Pvt Ltd

- 6.4.4 Pine Labs Pvt Ltd

- 6.4.5 PayU Payments Pvt Ltd

- 6.4.6 BharatPe (Resilient Innovations Pvt Ltd)

- 6.4.7 MobiKwik (One MobiKwik Systems Ltd)

- 6.4.8 PolicyBazaar (PB Fintech Ltd)

- 6.4.9 Zerodha Broking Ltd

- 6.4.10 Upstox (RKSV Securities India Pvt Ltd)

- 6.4.11 Groww (Nextbillion Technology Pvt Ltd)

- 6.4.12 Cred Financial Technologies Pvt Ltd

- 6.4.13 Slice (GaragePreneurs Internet Pvt Ltd)

- 6.4.14 KreditBee (Finnov Pvt Ltd)

- 6.4.15 Lendingkart Finance Ltd

- 6.4.16 Capital Float (Axio Digital)

- 6.4.17 NeoGrowth Credit Pvt Ltd

- 6.4.18 Navi Technologies Ltd

- 6.4.19 Jupiter (Amica Finance Pvt Ltd)

- 6.4.20 NIYO Solutions Pvt Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

金融科技市场商业分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案

金融科技市场商业分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案 2026-2030年全球金融科技市场金融科技市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分

2026-2030年全球金融科技市场金融科技市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分 美国金融科技市场:市场占有率分析、产业趋势与统计及成长预测(2026-2031年)英国金融科技:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国金融科技市场:市场占有率分析、产业趋势与统计及成长预测(2026-2031年)英国金融科技:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球金融科技即服务 (FaaS) 市场规模、份额、趋势和成长分析报告,2026-2034 年金融科技市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

全球金融科技即服务 (FaaS) 市场规模、份额、趋势和成长分析报告,2026-2034 年金融科技市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 日本金融科技市场报告:依采用类型、技术、应用、最终用户和地区划分(2026-2034年)

日本金融科技市场报告:依采用类型、技术、应用、最终用户和地区划分(2026-2034年) 金融科技领域生成式人工智慧市场-全球产业规模、份额、趋势、机会及预测(按组件、部署、应用、地区和竞争格局划分,2021-2031年)中东和北非金融科技市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

金融科技领域生成式人工智慧市场-全球产业规模、份额、趋势、机会及预测(按组件、部署、应用、地区和竞争格局划分,2021-2031年)中东和北非金融科技市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)