|

市场调查报告书

商品编码

1906971

马来西亚油气:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031)Malaysia Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

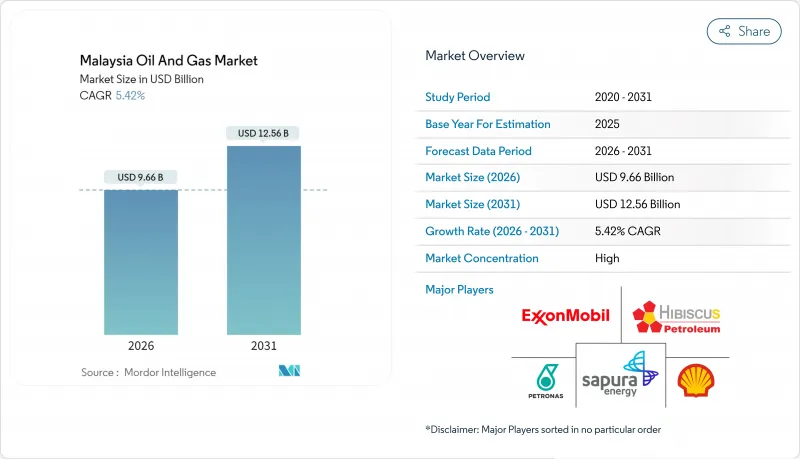

预计到 2026 年,马来西亚的石油和天然气市场规模将达到 96.6 亿美元,高于 2025 年的 91.6 亿美元。

预计到 2031 年将达到 125.6 亿美元,2026 年至 2031 年的复合年增长率为 5.42%。

马来西亚油气市场强劲的成长前景得益于对深水探勘、下游石化一体化以及不断扩大的碳管理项目的大规模投资。马来西亚国家石油公司(PETRONAS)的一体化价值链开发确保了原料供应的稳定,而产品分成合约(PSC)的审查持续吸引国际合作伙伴。预计沙捞越和沙巴的近海盆地将提高产量,新的液化天然气(LNG)供应协议将巩固马来西亚作为区域天然气枢纽的地位。同时,马来西亚半岛有利的财政环境和计划的基础设施正在加速石化产能的扩张,进一步巩固马来西亚作为东南亚能源中心的位置。

马来西亚油气市场趋势及展望

对精炼石油产品的需求迅速成长

东南亚地区燃料消费的復苏和新的出行趋势正在推动炼油厂的运转率。边佳兰综合炼油厂计划于2024年11月投入商业运营,日产能达30万桶,将为马来西亚半岛向印尼、越南和菲律宾等供应供不应求的市场供应原油奠定基础。马来西亚国家石油公司(Petronas)旗下的化学公司正在建造一座年产能3.3万吨的化学品回收工厂,预计将于2026年竣工,并将循环经济理念融入其下游业务。这些计划将保障上游生产商的原油供应,并将马来西亚定位为加工中心,而不仅仅是原油出口国。

沙捞越和沙巴未开发的深水蕴藏量

兰卡苏卡和拉央拉央丛集的前缘区域蕴藏着巨大的天然气和冷凝油潜力,需要高规格的钻井平台、海底回接系统和浮体式液化天然气(LNG)解决方案。在2025年马来西亚竞标中,五个勘探区域和三个开发及风险分担丛集被选为投资促进项目。康菲石油和壳牌正将其投资组合资本转向以天然气为中心的开发项目,以确保LNG原料的稳定供应。稳定的产品分成合约(PSC)框架以及马来西亚国家石油公司(Petronas)作为资源管理者的角色,缩短了从发现到首次产气的前置作业时间,从而增强了马来西亚油气市场的长期竞争力。

原油价格波动

2024-2025年布兰特原油价格每桶70-90美元的波动已扰乱了现金流规划,推迟了一些最终投资决策,并增加了借贷成本。获利能力较弱的油田的经济效益仍然对价格下跌十分敏感,尤其是那些需要高成本的气举或化学注入来提高产量的油田。马来西亚石油、天然气和能源服务理事会提出的财政援助请求凸显了市场波动所带来的风险。虽然避险和成本优化可能有效,但持续的波动可能会减缓深水油田开发和退役工作的进度。

细分市场分析

2025年,上游业务将占马来西亚油气市场总量的74.85%,主要得益于强劲的产量分成合约(PSC)活动和马来西亚国家石油公司(PETRONAS)的计划储备。 Jerung、Kasawari和Geumsut Kakap油田的重建计划有助于维持产量,同时抵消自然减产的影响。上游业务在马来西亚油气市场的主导地位反映了该国得天独厚的地理条件(蕴藏着丰富的天然气和冷凝油蕴藏量)以及有利于油田商业化的财政政策。

预计上游投资动能将持续到2031年,国际业者将陆续获得深水井区块和边际油气田改造计划。同时,随着沙巴-砂拉越天然气管道于2027年退役,中游企业将面临为东马天然气寻找替代运输路线的挑战。下游企业将受惠于新的原料来源,上游产能提升带来的冷凝油增加将为边佳兰重整装置提供原料。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对精炼石油产品的需求激增

- 未开发的深水蕴藏量(砂拉越和沙巴)

- 基于奖励的生产分成合约(PSC)修订及财务条款

- 亚洲液化天然气需求成长提振马来西亚出口

- CCUS和蓝氢计划储备库

- 下游石化一体化趋势

- 市场限制

- 原油价格波动加剧

- 投资方向随全球能源转型而改变

- 基于环境、社会和治理(ESG)的融资限制

- 老化的海洋基础设施和不断上涨的营运成本

- 供应链分析

- 监管环境

- 技术展望

- 原油产量和消费量预测

- 天然气生产与消费预测

- 已安装管道容量分析

- 非传统资源资本支出展望(緻密油、油砂、深水)

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- PESTEL 分析

第五章 市场规模与成长预测

- 按行业

- 上游部门

- 中游产业

- 下游产业

- 按地区

- 陆上

- 离岸

- 透过服务

- 建造

- 维护和检修

- 退休

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、伙伴关係、购电协议)

- 市场占有率分析(主要企业的市场排名和份额)

- 公司简介

- Petroliam Nasional Berhad(Petronas)

- Shell plc

- Exxon Mobil Corp.

- Chevron Corp.

- BP plc

- Hibiscus Petroleum Bhd

- Sapura Energy Bhd

- Dialog Group Bhd

- MISC Berhad

- Yinson Holdings Bhd

- PTTEP(Malaysia assets)

- Repsol Exploration(Malaysia)SA

- Lundin Energy Malaysia

- Murphy Oil Corporation(Malaysia)

- Serba Dinamik Holdings

- Velesto Energy Bhd

- Malaysia Marine & Heavy Engineering

- Altus Oil & Gas Malaysia Sdn Bhd

- Petro-Excel Sdn Bhd

- Petro Teguh(M)Sdn Bhd

第七章 市场机会与未来展望

Malaysia Oil And Gas Market size in 2026 is estimated at USD 9.66 billion, growing from 2025 value of USD 9.16 billion with 2031 projections showing USD 12.56 billion, growing at 5.42% CAGR over 2026-2031.

The strong growth outlook for the Malaysia oil and gas market stems from sizable investments in deep-water exploration, downstream petrochemical integration, and an expanding carbon management pipeline. Petronas' integrated value-chain footprint secures feedstock reliability, while Production Sharing Contract (PSC) revisions continue to attract international partners. Offshore basins in Sarawak and Sabah are set to deliver incremental volumes, and new LNG supply deals preserve Malaysia's role as a regional gas hub. Meanwhile, constructive fiscal terms and project-ready infrastructure in Peninsular Malaysia accelerate petrochemical capacity additions and reinforce the Malaysia oil and gas market as a Southeast Asian energy pivot.

Malaysia Oil And Gas Market Trends and Insights

Surging Demand for Refined Petroleum Products

Regional fuel consumption recovery and new mobility trends stimulate refinery utilization rates across Southeast Asia. The Pengerang Integrated Complex entered commercial service in November 2024 with 300,000 barrels-per-day capacity, underpinning Peninsular Malaysia's aspiration to supply deficit markets in Indonesia, Vietnam, and the Philippines. Petronas Chemicals is constructing a 33,000-tonnes-per-annum chemical recycling plant due in 2026, embedding circular-economy practices into the downstream landscape. These projects lock in crude intake for upstream producers and frame Malaysia as a processing hub rather than a pure exporter of crude.

Untapped Deep-Water Reserves in Sarawak & Sabah

Frontier acreage in the Langkasuka and Layang-Layang clusters offers sizable gas and condensate potential that requires high-spec rigs, subsea tie-backs, and floating LNG solutions. The Malaysia Bid Round 2025 listed five exploration blocks and three Development and Risk-sharing Option clusters to catalyze investment. ConocoPhillips and Shell have shifted portfolio capital toward gas-weighted developments to maximize LNG feedstock security. The stable PSC framework and Petronas' role as resource custodian shorten lead times from discovery to first gas, enhancing the long-term competitiveness of the Malaysia oil and gas market.

High Crude-Price Volatility

Brent fluctuations between USD 70-90 per barrel in 2024-2025 disrupted cash-flow planning, deferred some final investment decisions, and raised borrowing costs. Marginal field economics remain sensitive to price dips, particularly where enhanced recovery requires costly gas lift or chemical injection. The Malaysian Oil, Gas and Energy Services Council's appeal for fiscal relief underscores exposure to market swings. While hedging and cost optimization help, sustained volatility may temper the pace of deep-water and decommissioning commitments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Asian LNG Demand Lifting Malaysian Exports

- Downstream Petrochemical Integration Momentum

- Global Energy-Transition Investment Shift

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The upstream segment captured 74.85% of the Malaysia oil and gas market size in 2025, buoyed by robust PSC activity and Petronas' project pipeline. Jerun, Kasawari, and Gumusut-Kakap Redevelopment sustain plateau output while offsetting natural decline rates. The Malaysian oil and gas market share leadership in upstream activities reflects a geology rich in gas-condensate plays and a supportive fiscal regime that accelerates field monetization.

Upstream investment momentum will likely continue through 2031 as international operators secure acreage in deep-water wells and marginal redevelopments. Concurrently, midstream operators face rerouting challenges once the Sabah-Sarawak Gas Pipeline retires in 2027, requiring alternative evacuation for East Malaysian gas. Downstream players benefit from new feedstock when upstream debottlenecking releases incremental condensate volumes that feed into Pengerang's reformers.

The Malaysia Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Petroliam Nasional Berhad (Petronas)

- Shell plc

- Exxon Mobil Corp.

- Chevron Corp.

- BP plc

- Hibiscus Petroleum Bhd

- Sapura Energy Bhd

- Dialog Group Bhd

- MISC Berhad

- Yinson Holdings Bhd

- PTTEP (Malaysia assets)

- Repsol Exploration (Malaysia) S.A.

- Lundin Energy Malaysia

- Murphy Oil Corporation (Malaysia)

- Serba Dinamik Holdings

- Velesto Energy Bhd

- Malaysia Marine & Heavy Engineering

- Altus Oil & Gas Malaysia Sdn Bhd

- Petro-Excel Sdn Bhd

- Petro Teguh (M) Sdn Bhd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for refined petroleum products

- 4.2.2 Untapped deep-water reserves (Sarawak & Sabah)

- 4.2.3 Incentive-driven PSC revisions & fiscal terms

- 4.2.4 Rising Asian LNG demand lifting Malaysian exports

- 4.2.5 CCUS & blue-hydrogen project pipeline

- 4.2.6 Downstream petrochemical integration momentum

- 4.3 Market Restraints

- 4.3.1 High crude-price volatility

- 4.3.2 Global energy-transition investment shift

- 4.3.3 ESG-driven capital access constraints

- 4.3.4 Aging offshore infrastructure & OPEX escalation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power - Suppliers

- 4.11.2 Bargaining Power - Buyers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Petroliam Nasional Berhad (Petronas)

- 6.4.2 Shell plc

- 6.4.3 Exxon Mobil Corp.

- 6.4.4 Chevron Corp.

- 6.4.5 BP plc

- 6.4.6 Hibiscus Petroleum Bhd

- 6.4.7 Sapura Energy Bhd

- 6.4.8 Dialog Group Bhd

- 6.4.9 MISC Berhad

- 6.4.10 Yinson Holdings Bhd

- 6.4.11 PTTEP (Malaysia assets)

- 6.4.12 Repsol Exploration (Malaysia) S.A.

- 6.4.13 Lundin Energy Malaysia

- 6.4.14 Murphy Oil Corporation (Malaysia)

- 6.4.15 Serba Dinamik Holdings

- 6.4.16 Velesto Energy Bhd

- 6.4.17 Malaysia Marine & Heavy Engineering

- 6.4.18 Altus Oil & Gas Malaysia Sdn Bhd

- 6.4.19 Petro-Excel Sdn Bhd

- 6.4.20 Petro Teguh (M) Sdn Bhd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026年全球油气管道及相关结构建设市场报告

2026年全球油气管道及相关结构建设市场报告 石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测

石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测 美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)英国石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)英国石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 日本油气市场报告:按类型、应用和地区划分(2026-2034年)2026年全球油气市场报告

日本油气市场报告:按类型、应用和地区划分(2026-2034年)2026年全球油气市场报告 石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析

2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析