|

市场调查报告书

商品编码

1939095

英国石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United Kingdom Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

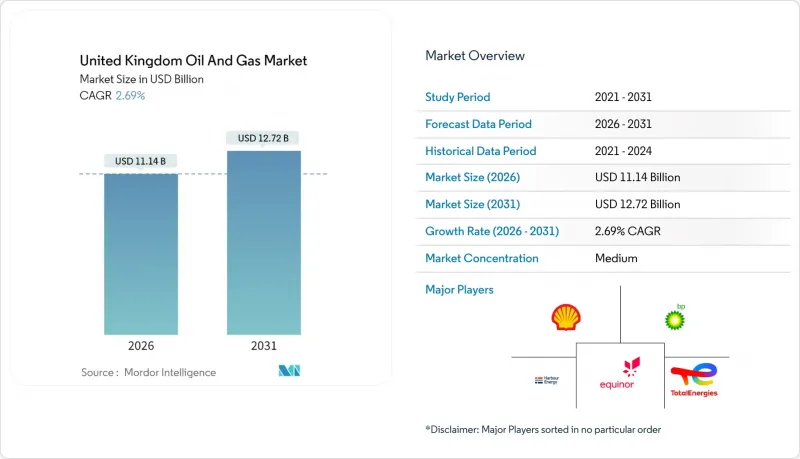

英国石油和天然气市场预计将从 2025 年的 108.5 亿美元成长到 2026 年的 111.4 亿美元,到 2031 年达到 127.2 亿美元,2026 年至 2031 年的复合年增长率为 2.69%。

这项稳定扩张得益于策略转型,旨在最大限度地释放北海成熟油田的价值,并有意放缓新勘探活动。自2020年以来,营运商已将钻井成本降低了15%至20%,在财务负担日益加重的情况下仍保持了盈利。 2024年的投资金额超过60亿英镑,是监管机构预期的1.5倍,主要用于延长油田寿命计画和支援碳捕获基础设施的中游升级改造。独立公司之间的整合加速,促成了两项总额超过20亿美元的重大收购,实现了成本协同效应和退役效率的提升。同时,离岸风力发电试验和平台电气化降低了柴油消耗,显示排放合规和生产稳定性可以兼得。

英国油气市场趋势与洞察

降低北海采矿成本可提高营运效率

北海钻井成本大幅下降,使英国营运商在全球能源市场挑战中拥有了竞争优势。自2020年以来,海底系统的技术突破和钻井技术的改进已使每桶生产成本降低了15-20%,从而在日益增长的财务压力下维持了生产的永续性。这种成本降低的趋势使英国油田在与国际竞争对手的较量中占据优势,尤其是在能源安全问题日益突出、国内石油产量价值不断提升的情况下。效率的提高得益于先进的储存管理系统和优化的生产计划,从而在最大限度地提高采收率的同时,最大限度地降低了营运成本。营运商正利用这些成本优势,为继续投资那些可能因获利能力下降而提前退役的成熟资产以及延长油田寿命提供理由。

英国北海转型协议奖励重塑投资重点

英国北海转型协议为在实现净零排放目标方面取得显着进展的营运商提供系统性的财政奖励,从根本上改变了整个产业的资本配置决策。投资补贴和更高的折旧免税额率鼓励企业将碳捕获、利用与储存(CCUS)技术整合到其营运中,符合条件的计划可获得高达合格支出40%的加速税收合格。该政策框架已承诺从2024年起投入超过20亿英镑用于CCUS投资,将先前无利可图的计划转变为可行的开发机会。该协议为在排放展现技术领先优势的营运商提供了竞争优势,有效支持了向低碳油气生产的转型。 ISO 14001环境管理系统认证对于获得这些激励措施的重要性日益凸显,营运商正大力投资合规流程。

加速征收CCS课税给企业现金流带来压力

英国大陆棚上游业者加速征收捕碳封存(CCS)附加税,正给整个区域带来即时的财务压力。主要生产商的合规成本估计每年高达1.5亿至2亿英镑。法规结构要求营运商无论是否参与具体计划,都必须为国家CCS基础设施建设做出贡献,这实际上是透过产业课税补贴更广泛的能源转型目标。这种征税结构对缺乏规模来承担额外成本的中小型独立运营商造成了不成比例的影响,可能加速边缘运营商寻求更大的合作伙伴或彻底退出市场。遵守征税规定需要加强监测和报告能力,这增加了营运的复杂性,并进一步加剧了资源紧张。

细分市场分析

2025年上游业务71.65%的市占率占主导地位,显示开采活动仍是英国油气业务的核心。然而,中游业务到2031年的复合年增长率(CAGR)为4.18%,预示着该业务将发生根本性转变,转向基础设施和加工投资。上游业务受益于提高采收率技术和油田延寿计划,这些措施最大限度地提高了现有北海资产的价值。像Harbour Energy这样的业者在2024年投资超过13亿美元用于资产收购,以整合产能。中游业务的加速成长是由碳捕获、利用和封存(CCUS)计划所需的关键基础设施所驱动的,这些项目需要对管道网路和加工设施进行重大升级,以满足二氧化碳运输和氢气生产的需求。由于对成品油的需求,下游业务保持稳定,但长期来看,电气化趋势和可再生燃料强制令将对其构成挑战。

中游基础设施投资尤其集中在东海岸丛集,其中Kerath Midstream的H2NorthEast工厂拥有1吉瓦的蓝氢生产能力,这将需要大规模的管道维修和新建压缩站。预计到2025年,英国中游市场规模将达到21.9亿美元,年成长率将比产业平均高出1.5个百分点。英国天然气输送系统由超过7,600公里的高压管道组成,国家电网每年投资25亿英镑用于网路维护和升级计划,以支援传统的天然气输送和新兴的氢能应用。浮式生产储油卸油设备)的引入正在扩大处理能力,并使以前难以开发的蕴藏量得以开发。同时,战略石油储备的要求以及平滑季节性需求的需求也促进了储能基础设施的发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 北海采矿成本呈下降趋势。

- 英国北海过渡协议的奖励

- 浮动式风力发电平台快速增加(降低勘探和生产成本)

- 蒂斯河畔和亨伯河畔地区的再工业化(蓝氢需求)

- 基于人工智慧的探勘影像处理的成功率

- 市场限制

- 加快对上游企业课税碳捕获与封存税。

- 併网离岸风力发电可望取代天然气尖峰时段需求。

- 加强退役保证金要求

- 供应链分析

- 监管环境

- 技术展望

- 原油产量和消费量预测

- 天然气生产与消费预测

- 已安装管道容量分析

- 非传统资源资本支出展望(緻密油、油砂、深水)

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- PESTEL 分析

第五章 市场规模与成长预测

- 按行业

- 上游部门

- 中游产业

- 下游产业

- 按安装位置

- 陆上

- 离岸

- 透过服务

- 建造

- 维护和检修

- 退休

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、联盟、购电协议)

- 市场占有率分析(主要企业的市场排名和份额)

- 公司简介

- Shell plc

- BP plc

- Harbour Energy plc

- TotalEnergies SE

- Equinor ASA

- Chevron Corp.

- Centrica plc

- Valaris plc

- INEOS Group Ltd

- ConocoPhillips UK Ltd

- EnQuest plc

- Ithaca Energy plc

- Neptune Energy Group

- Cadent Gas Ltd

- Dana Petroleum Ltd

- ESSO UK Ltd

- BG Group Ltd

- Premier Oil(Chrysaor)

- Wood plc

- Subsea 7 SA

第七章 市场机会与未来展望

The United Kingdom Oil And Gas market is expected to grow from USD 10.85 billion in 2025 to USD 11.14 billion in 2026 and is forecast to reach USD 12.72 billion by 2031 at 2.69% CAGR over 2026-2031.

A strategic shift toward squeezing maximum value from mature North Sea reservoirs, paired with a deliberate slowdown in greenfield exploration, underpins this measured expansion. Operators have reduced lifting costs by 15-20% since 2020, thereby protecting profitability even as fiscal burdens increase. The 2024 investment outlay of more than £6 billion, half again above regulator expectations, flowed mainly into life-extension programs and midstream upgrades that support carbon-capture infrastructure. Consolidation among independents accelerated, with two headline acquisitions totaling more than USD 2 billion, unlocking cost synergies and decommissioning efficiencies. At the same time, floating-wind pilots and on-platform electrification cut diesel burn, proving that emissions compliance and production stability can coexist.

United Kingdom Oil And Gas Market Trends and Insights

Declining North Sea Lifting Costs Drive Operational Efficiency

North Sea lifting costs have decreased substantially, creating competitive advantages for UK operators amid global energy market challenges. Technological breakthroughs in subsea systems and enhanced drilling techniques have cut per-barrel extraction costs by 15-20% since 2020, sustaining production viability despite heightened fiscal pressures. This cost reduction trajectory positions UK fields favorably against international alternatives, particularly as energy security concerns elevate domestic production value. The efficiency gains result from advanced reservoir management systems and optimized production scheduling, which maximize recovery rates while minimizing operational expenses. Operators leverage these cost improvements to extend field life and justify continued investment in mature assets that might otherwise face early decommissioning.

UK North Sea Transition Deal Incentives Reshape Investment Priorities

The UK North Sea Transition Deal offers structured fiscal incentives to operators demonstrating measurable progress toward net-zero emissions targets, thereby fundamentally altering capital allocation decisions across the sector. Investment allowances and enhanced depletion rates reward companies that integrate carbon capture, utilization, and storage technologies into their operations, with qualifying projects receiving accelerated tax relief worth up to 40% of eligible expenditures. This policy framework has catalyzed over £2 billion in committed CCUS investments since 2024, transforming previously uneconomical projects into viable development opportunities. The deal creates competitive advantages for operators demonstrating technological leadership in emissions reduction, effectively subsidizing the transition toward lower-carbon hydrocarbon production. ISO 14001 environmental management certification has become increasingly critical for accessing these incentives, with operators investing heavily in compliance processes.

Accelerated CCS Levy Strains Operator Cash Flows

The introduction of accelerated carbon capture and storage levies on upstream operators has created immediate financial pressure across the UK Continental Shelf, with compliance costs estimated at £150-200 million annually for major producers. This regulatory framework requires operators to contribute to national CCS infrastructure development regardless of their individual project participation, effectively subsidizing broader energy transition objectives through sector-specific taxation. The levy structure disproportionately impacts smaller independents who lack the scale to absorb these additional costs, potentially accelerating consolidation as marginal operators seek larger partners or exit the market entirely. Compliance with the levy requirements demands enhanced monitoring and reporting capabilities, which add operational complexity and further strain resources.

Other drivers and restraints analyzed in the detailed report include:

- Floating Wind Platform Integration Reduces Operational Carbon Intensity

- Teesside and Humber Industrial Clusters Create Blue Hydrogen Demand

- Offshore Wind Grid Integration Reduces Peak Gas Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The upstream segment's commanding 71.65% market share in 2025 reflects the continued centrality of extraction activities to UK oil and gas operations, yet the midstream segment's 4.18% CAGR through 2031 signals a fundamental shift toward infrastructure and processing investments. Upstream activities benefit from enhanced recovery techniques and extended field life programs that maximize value from existing North Sea assets. Operators like Harbour Energy have invested over USD 1.3 billion in asset acquisitions during 2024 to consolidate production capabilities. The midstream segment's accelerated growth stems from critical infrastructure requirements for carbon capture, utilization, and storage projects, with pipeline networks and processing facilities requiring substantial upgrades to handle CO2 transport and hydrogen production. Downstream operations maintain steady performance through refined product demand, though the segment faces long-term headwinds from electrification trends and renewable fuel mandates.

Midstream infrastructure investments are particularly concentrated in the East Coast Cluster, where Kellas Midstream's H2NorthEast facility represents a 1 GW blue hydrogen production capability that necessitates extensive pipeline modifications and the installation of new compression stations. The UK oil and gas market size for midstream operations reached USD 2.19 billion in 2025, with annual growth rates exceeding the sector average by 1.5 percentage points. The UK's gas transmission system spans over 7,600 km of high-pressure pipelines, with National Grid investing £2.5 billion annually in network maintenance and enhancement projects that support both traditional gas transport and emerging hydrogen applications. Processing capabilities are expanding through the deployment of floating production, storage, and offloading vessels, which enable the development of previously stranded reserves. Meanwhile, storage infrastructure benefits from strategic petroleum reserve requirements and seasonal demand balancing needs.

The United Kingdom Oil and Gas Market is Segmented by Sector (Upstream, Downstream, and Midstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Shell plc

- BP plc

- Harbour Energy plc

- TotalEnergies SE

- Equinor ASA

- Chevron Corp.

- Centrica plc

- Valaris plc

- INEOS Group Ltd

- ConocoPhillips UK Ltd

- EnQuest plc

- Ithaca Energy plc

- Neptune Energy Group

- Cadent Gas Ltd

- Dana Petroleum Ltd

- ESSO UK Ltd

- BG Group Ltd

- Premier Oil (Chrysaor)

- Wood plc

- Subsea 7 SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining North Sea lifting costs

- 4.2.2 UK "North Sea Transition Deal" incentives

- 4.2.3 Surge in floating-wind-powered platforms (E&P cost cuts)

- 4.2.4 Re-industrialisation of Teesside & Humber (blue hydrogen demand)

- 4.2.5 AI-enabled seismic imaging success rates

- 4.3 Market Restraints

- 4.3.1 Accelerated CCS levy on upstream operators

- 4.3.2 Grid-connected offshore wind cannibalising peak-time gas demand

- 4.3.3 Heightened decommissioning bond requirements

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Intensity of Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Shell plc

- 6.4.2 BP plc

- 6.4.3 Harbour Energy plc

- 6.4.4 TotalEnergies SE

- 6.4.5 Equinor ASA

- 6.4.6 Chevron Corp.

- 6.4.7 Centrica plc

- 6.4.8 Valaris plc

- 6.4.9 INEOS Group Ltd

- 6.4.10 ConocoPhillips UK Ltd

- 6.4.11 EnQuest plc

- 6.4.12 Ithaca Energy plc

- 6.4.13 Neptune Energy Group

- 6.4.14 Cadent Gas Ltd

- 6.4.15 Dana Petroleum Ltd

- 6.4.16 ESSO UK Ltd

- 6.4.17 BG Group Ltd

- 6.4.18 Premier Oil (Chrysaor)

- 6.4.19 Wood plc

- 6.4.20 Subsea 7 SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026年全球油气管道及相关结构建设市场报告

2026年全球油气管道及相关结构建设市场报告 石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测

石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测 美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)越南石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)越南石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 日本油气市场报告:按类型、应用和地区划分(2026-2034年)2026年全球油气市场报告

日本油气市场报告:按类型、应用和地区划分(2026-2034年)2026年全球油气市场报告 石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚油气:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031)

石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚油气:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031) 2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析

2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析