|

市场调查报告书

商品编码

1934642

越南石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)Vietnam Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

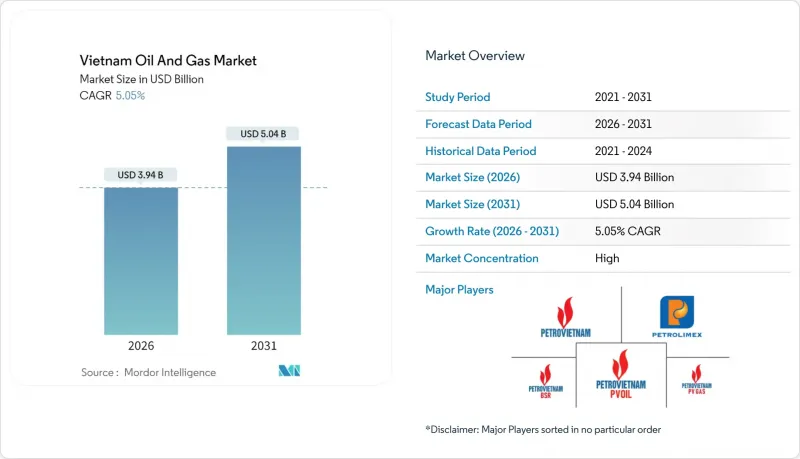

预计到 2026 年,越南石油和天然气市场规模将达到 39.4 亿美元,高于 2025 年的 37.5 亿美元。

预计到 2031 年将达到 50.4 亿美元,2026 年至 2031 年的复合年增长率为 5.05%。

这项成长轨迹源自于越南在国内天然气产量下降的情况下,为保障能源安全而采取的策略性倡议,以及在第八个国家电力发展计画下加速推进液化天然气(LNG)发电投资。以储量超过1700亿立方公尺的BO Mon区块开发为代表的大规模上游投资,与不断扩大的进口合作伙伴关係相辅相成,确保了新建燃气电厂的燃料柔软性。成功的海上探勘、更深层的储存目标以及国内钻机製造技术的进步,都进一步增强了资本投资动能。同时,下游数位化、更严格的ESG(环境、社会和治理)监管以及外商直接投资(FDI)园区内工业天然气基本客群的不断增长,正在提升中下游现金流,并引导营运商转向利润丰厚的维护和检修服务。这些因素共同作用,推动了以资产优化而非单纯新增产能为中心的中期发展机会。

越南油气市场趋势与洞察

基于PDP-8的LNG发电推广

越南第八个电力发展计画(PDP-8)规定,2030年,液化天然气(LNG)发电装置容量将达22,524兆瓦,约占全国总发电量的10%。自2013年以来,越南国内天然气产量以每年约5%的速度下降,但天然气需求预计将从2020年的130亿立方公尺增加到2030年的340亿立方公尺以上。新增供给能力,例如2025年3月将Thi Vai终端的日处理能力扩建至700万立方米,正在为此转型提供支援。 PV Gas和Excelerate Energy已签署谅解备忘录,将从2026年起向越南供应美国液化天然气,这将加强越南首个完全一体化LNG发电项目-非卡车机组3号和4号机组的原料多元化。这些开创性的措施确立了液化天然气作为电力产业脱碳基础的地位。

国内产量下降推动了勘探与生产支出。

随着白虎油田和白虎油田等成熟油田面临水位上升和压力下降的困境,营运商正在探勘新的储存以稳定国内供应。墨菲石油公司决定在2025年前投资1.1亿美元(占其全球预算的9%),用于钻探拉克达旺油田并评估海苏旺油田。在海苏旺油田,1X井在两个储存中实现了370英尺的净产量。越南石油公司提前20天完成了大雄三期项目,展现了其在国内加快加密井计划以应对产量下降的能力。计划在15-1/05区块和15-2/17区块进行的股权转让旨在透过将产量分成条款与成熟的服务基础设施相结合,吸引更多风险资本。这些项目将近期现金流分配给高效益油井,同时透过提高采收率延长油田寿命。

成熟油田和高额的水裂解成本

像白虎油田这样的历史性高产量油田目前含水率高达80%以上,导致分离和加工成本上升,利润空间受到挤压。虽然技术进步已将自升式钻井平台的维修週期缩短至五天,但储存衰减仍在持续,导致产量下降和退役责任增加。资本密集的增产技术仅能部分弥补产量下降,凸显了进行新探勘的必要性。

细分市场分析

预计到2025年,上游油气业务将占越南油气市场的74.25%,并在2031年之前保持5.38%的年均增长率,这主要得益于BO Mon区块和墨菲石油公司Lac Da Vang项目等深水计划的投资。投资的激增将促使越南进行评估钻井,目标是开采超过1亿桶油当量(boe)的可采储量,从而巩固越南在油气探勘和生产领域的主导地位。 White Tiger油田和Dai Hung三期专案的持续储存管理,体现了从一次采油技术向二次采油技术的过渡,这将延长油田寿命并维持课税产量。

中游海底管线和液化天然气接收设施将海上油气源与都市区需求中心连接起来,而位于宜山和榕桔的下游炼油厂正将閒置产能从每年650万吨提高到近750万吨。利用数位双胞胎和人工智慧进行产量优化,降低了能源消耗,减少了不合格产品的数量,从而提高了每桶利润,儘管2020年《环境保护法》收紧了环境法规。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 基于PDP-8的LNG发电推广

- 国内产量下降推动勘探和开发投资

- 外商直接投资园区内燃气发电产业的发展

- B区块和蓝鲸钻井平台数量激增

- 燃油零售快速数位化(PVOIL Easy)

- 美越液化天然气供应伙伴关係

- 市场限制

- 成熟油田和高额的水裂解成本

- 液化天然气电力价格上限

- 产品分成合约(PSC)和液化天然气(LNG)接收站审批延误

- 南海地缘政治风险

- 供应链分析

- 监管环境

- 技术展望

- 原油产量和消费量预测

- 天然气生产与消费预测

- 已安装管道容量分析

- 非传统资源资本支出展望(緻密油、油砂、深水)

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- PESTEL 分析

第五章 市场规模与成长预测

- 按行业

- 上游部门

- 中游产业

- 下游产业

- 按地区

- 陆上

- 离岸

- 透过服务

- 建造

- 维护和检修

- 退休

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、伙伴关係、购电协议)

- 市场占有率分析(主要企业的市场排名和份额)

- 公司简介

- Vietnam Oil & Gas Group(PetroVietnam)

- Petrolimex Group

- PetroVietnam Gas(JSC)

- Binh Son Refining & Petrochemical(BSR)

- PetroVietnam Oil(PVOIL)

- PetroVietnam Power(PV Power)

- PetroVietnam Exploration & Production(PVEP)

- PetroVietnam Drilling(PVD)

- PetroVietnam Technical Services(PTSC)

- PetroVietnam Transportation(PV Trans)

- ExxonMobil Corp.

- TotalEnergies SE

- Chevron Corp.

- Idemitsu Kosan Co. Ltd

- Mitsui Oil Exploration

- Excelerate Energy Inc.

- Jadestone Energy plc

- Rosneft PJSC

- Japan Drilling Co. Ltd

- KS Energy Services Ltd

第七章 市场机会与未来展望

Vietnam Oil And Gas Market size in 2026 is estimated at USD 3.94 billion, growing from 2025 value of USD 3.75 billion with 2031 projections showing USD 5.04 billion, growing at 5.05% CAGR over 2026-2031.

This trajectory is rooted in Vietnam's deliberate shift toward energy security as domestic production declines and LNG-to-power investment accelerates under the National Power Development Plan VIII. Substantial upstream commitments-exemplified by the Block B - O Mon development with recoverable gas exceeding 170 billion m3-harmonize with rising import alliances that secure fuel flexibility for new gas-fired generation. Offshore exploration success, deeper reservoir targets, and indigenous rig fabrication collectively reinforce capital expenditure momentum. At the same time, downstream digitalization, stricter ESG rules, and a widening industrial gas customer base in foreign direct investment (FDI) parks are expanding mid- and downstream cash flows while nudging operators toward higher-margin maintenance and turnaround services. Together, these forces cultivate a medium-term opportunity set centered on asset optimization rather than pure greenfield capacity.

Vietnam Oil And Gas Market Trends and Insights

LNG-to-Power Push Under PDP-8

Vietnam's Power Development Plan VIII stipulates 22,524 MW of LNG-fired capacity by 2030, equal to roughly 10% of the national fleet.VN. Domestic gas output has been declining at a rate of approximately 5% annually since 2013, yet gas demand is forecast to increase from 13 billion m3 in 2020 to exceed 34 billion m3 by 2030. Capacity additions such as the Thi Vai terminal expansion to 7 million m3 per day in March 2025 underpin that pivot. PV Gas and Excelerate Energy have signed supply memoranda that lock in U.S. cargoes from 2026, bolstering feedstock diversity for Nhon Trach 3 and 4-the country's first fully integrated LNG-to-power chain. Together, these milestones embed LNG as a cornerstone of power-sector decarbonization.

Declining Domestic Output Spurs E&P Spend

Mature fields, such as Bach Ho and White Tiger, face rising water cuts and falling pressure, prompting operators to explore new reservoirs to stabilize the national supply. Murphy Oil committed USD 110 million for 2025-9% of its global budget-to drill Lac Da Vang and appraise Hai Su Vang, where the 1X well logged 370 ft of net pay over two reservoirs. PetroVietnam delivered Dai Hung Phase 3 twenty days ahead of schedule, demonstrating its domestic capacity to fast-track infill plans that counteract decline. Upcoming farm-outs in Blocks 15-1/05 and 15-2/17 aim to attract more risk capital by pairing production sharing terms with proven service infrastructure. Together, these programs allocate near-term cash flow to high-impact wells while extending field life through enhanced recovery.

Mature Fields & High Water-Cut Costs

Historic producers like Bach Ho now record water-cut levels above 80%, inflating separation expenses and squeezing margins. Engineering tweaks have trimmed jack-up repair cycles to five days, yet reservoir decline continues to erode volumes and elevate decommissioning liabilities. Capital-intensive enhanced recovery only partially offsets drop-offs, underscoring the need for new exploration.

Other drivers and restraints analyzed in the detailed report include:

- Gas-Fired Industrial Growth in FDI Parks

- Surge in Rigs for Block B & Blue Whale

- Price-Capped LNG-Power Tariffs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The upstream segment accounted for 74.25% of Vietnam's oil and gas market in 2025 and is forecast to compound at a 5.38% CAGR to 2031, driven by deepwater spending on projects such as Block B - O Mon and Murphy Oil's Lac Da Vang program. This spending surge underwrites appraisal drilling that targets recoverable volumes exceeding 100 million barrels of oil equivalent (boe) and consolidates Vietnam's lead in the oil and gas market for exploration and production. Ongoing reservoir management at White Tiger and Phase 3 of Dai Hung exemplify the shift from primary recovery to secondary techniques, which prolong field life and sustain taxable output.

While midstream subsea pipelines and LNG reception facilities link offshore flows to urban demand centers, downstream refiners at Nghi Son and Dung Quat add capacity headroom from 6.5 million t/y to nearly 7.5 million t/y. Digital twins and AI-driven yield optimization reduce energy intensity and curtail off-spec volumes, thereby increasing profit per barrel despite stricter environmental regulations under the 2020 Environmental Protection Law.

The Vietnam Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vietnam Oil & Gas Group (PetroVietnam)

- Petrolimex Group

- PetroVietnam Gas (JSC)

- Binh Son Refining & Petrochemical (BSR)

- PetroVietnam Oil (PVOIL)

- PetroVietnam Power (PV Power)

- PetroVietnam Exploration & Production (PVEP)

- PetroVietnam Drilling (PVD)

- PetroVietnam Technical Services (PTSC)

- PetroVietnam Transportation (PV Trans)

- ExxonMobil Corp.

- TotalEnergies SE

- Chevron Corp.

- Idemitsu Kosan Co. Ltd

- Mitsui Oil Exploration

- Excelerate Energy Inc.

- Jadestone Energy plc

- Rosneft PJSC

- Japan Drilling Co. Ltd

- KS Energy Services Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LNG-to-Power Push Under PDP-8

- 4.2.2 Declining Domestic Output Spurs E&P Spend

- 4.2.3 Gas-Fired Industrial Growth in FDI Parks

- 4.2.4 Surge in Rigs for Block B & Blue Whale

- 4.2.5 Rapid Fuel-Retail Digitisation (PVOIL Easy)

- 4.2.6 U.S.-Vietnam LNG Supply Alliances

- 4.3 Market Restraints

- 4.3.1 Mature Fields & High Water-Cut Costs

- 4.3.2 Price-Capped LNG-Power Tariffs

- 4.3.3 Slow PSC & LNG Terminal Approvals

- 4.3.4 South China Sea Geopolitical Risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Suppliers

- 4.11.3 Bargaining Power of Buyers

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Vietnam Oil & Gas Group (PetroVietnam)

- 6.4.2 Petrolimex Group

- 6.4.3 PetroVietnam Gas (JSC)

- 6.4.4 Binh Son Refining & Petrochemical (BSR)

- 6.4.5 PetroVietnam Oil (PVOIL)

- 6.4.6 PetroVietnam Power (PV Power)

- 6.4.7 PetroVietnam Exploration & Production (PVEP)

- 6.4.8 PetroVietnam Drilling (PVD)

- 6.4.9 PetroVietnam Technical Services (PTSC)

- 6.4.10 PetroVietnam Transportation (PV Trans)

- 6.4.11 ExxonMobil Corp.

- 6.4.12 TotalEnergies SE

- 6.4.13 Chevron Corp.

- 6.4.14 Idemitsu Kosan Co. Ltd

- 6.4.15 Mitsui Oil Exploration

- 6.4.16 Excelerate Energy Inc.

- 6.4.17 Jadestone Energy plc

- 6.4.18 Rosneft PJSC

- 6.4.19 Japan Drilling Co. Ltd

- 6.4.20 KS Energy Services Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

2026年全球油气管道及相关结构建设市场报告

2026年全球油气管道及相关结构建设市场报告 石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测

石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测 美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)英国石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)英国石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本油气市场报告:按类型、应用和地区划分(2026-2034年)2026年全球油气市场报告

日本油气市场报告:按类型、应用和地区划分(2026-2034年)2026年全球油气市场报告 石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚油气:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031)

石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚油气:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031) 2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析

2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析