|

市场调查报告书

商品编码

1907244

北美建筑化学品市场-份额分析、产业趋势与统计、成长预测(2026-2031)North America Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

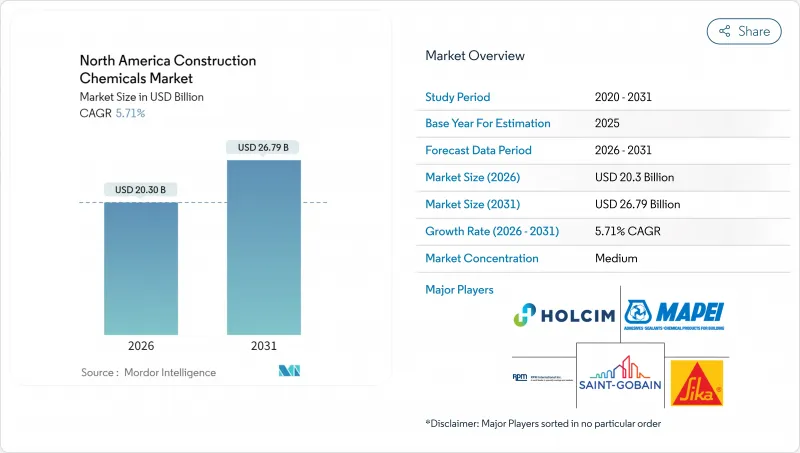

预计到 2025 年,北美建筑化学品市场价值将达到 192 亿美元,到 2026 年将成长至 203 亿美元,到 2031 年将成长至 267.9 亿美元,预测期(2026-2031 年)的复合年增长率为 5.71%。

基础设施现代化专案、清洁采购法规以及人工智慧驱动的混合料设计平台的兴起,正共同推动产品需求成长,并重新定义产品规格的製定路径。由《基础设施投资与就业法案》(IIJA)资助的公路、桥樑和水利基础设施维修,为大批量混凝土应用创造了稳定的需求基础,这就需要高效的混凝土外加剂,以延长使用寿命并抵消不断上涨的原材料价格。各州的碳含量法规促使买家更倾向于低全球暖化潜势(GWP)的防水卷材和水泥基增强外加剂,从而为经认证的永续化学品创造了高端市场。资料中心和半导体大型企划正在推动防火涂料、精密密封剂和快速固化剂的快速应用。同时,日益严格的能源效率标准也推动了对先进外墙系统的高性能黏合剂的需求。儘管石油基树脂价格波动和技术纯熟劳工短缺仍然是成本方面的阻力,但垂直整合的供应商和拥有简化施工技术的公司正在降低利润风险。

北美建筑化学品市场趋势与洞察

对基础建设计划的大规模投资

由《基础设施投资与就业法案》(IIJA)资金筹措的众多交通基础设施改善和桥樑维修项目,对防护涂料、修补砂浆和水处理化学品的需求持续旺盛。成本上涨(例如2022年公路建设指数的上涨)降低了购买力,促使各机构转向以性能为导向、强调全生命週期耐久性的规范。加拿大联邦和省级计画与美国的发展趋势相符,尤其是在设计用于承受冻融循环的防水系统方面。能够证明其产品在加速老化测试通讯协定下可延长资产使用寿命的供应商,将获得多年期框架合约。原物料采购的垂直整合正逐渐成为应对竞标价格波动的一种手段,使生产商能够在原物料价格波动的情况下履行固定价格承诺。

严格的节能标准推动了高性能外加剂的发展

加州建筑规范第24条、IECC和各州能源规范的融合提高了墙体和屋顶的最低保温要求,推动了先进密封剂和黏合剂系统在连续保温结构中的应用。同时,这些计划也要求减少碳排放,从而对既能降低水泥用量又不牺牲强度的蕴藏量提出了双重要求。混凝土生产商越来越多地指定使用高效减水剂,以提高飞灰和矿渣的替代率,并在某些情况下添加奈米二氧化硅混合物以达到更高的模量目标。在公共部门竞标中,提供从摇篮到大门的环境产品声明(EPD)和技术建模支援的化学品供应商正在取代大宗商品供应商。在商业建筑中,能源建模工具将热性能和结构性能模拟相结合,从而在更薄的楼板截面中实现更严格的化学性能容差。

石油基树脂价格波动

美国国际贸易委员会(USITC)启动反倾销调查后,环氧树脂现货价格飙升,挤压了依赖高纯度双酚A原料的特种涂料的利润空间。在墨西哥湾沿岸设有工厂的製造商享有运输成本优势,但仍面临飓风导致停产的风险。避险策略包括从亚洲双重采购以及建造本地仓储设施以平抑供应衝击。终端用户正在尝试使用混合系统,以生物基环氧树脂取代石油基成分,但这些混合产品仍然价格较高,且规格核准有限。多年期供应合约通常包含动态定价条款,以将原物料价格波动的影响转嫁给用户。

细分市场分析

至2025年,防水解决方案将占北美建设化学品市场的32.62%,预计2031年将以6.09%的复合年增长率成长。这反映出,由于日益严格的防潮标准,人们对建筑围护结构的完整性越来越重视。由于液态防水膜的广泛应用,预计该细分市场的成长速度将高于整体市场。液态防水膜可缩短施工时间,并能适应复杂的几何形状,取代传统的片材系统。为了在节能建筑中实现双重性能目标,製造商正在将聚合物改质沥青与反应性硅烷混合,以在保持蒸气渗透性的同时提高延展性。采用地工织物增强液态防水膜的混合系统价格高于标准产品。表面处理剂和固化剂正着重于改善脱模和水化控制,这与预製构件生产商的趋势类似,旨在提高工厂的生产效率。同时,混凝土外加剂生产商正在将收缩控製剂纳入综合防水方案中,使承包商能够在单一保固范围内获得多功能解决方案。

混凝土外加剂仍然是重要的产品类别,这主要得益于高效减水剂,其在以50%的波特兰水泥替代率下即可达到25 MPa的强度,这对于低碳竞标是一项关键性能指标。由于老旧桥樑存量不断增加,包括纤维包裹环氧树脂和超快凝砂浆在内的修復和加固化学品的需求日益增长,许多联邦计划已指定使用这些系统进行桥面覆盖。对黏合剂、密封剂和地板树脂的需求保持稳定,这主要得益于商业建筑幕墙维修和高客流量零售场所的整修。持续的VOC法规和NFPA 285合规要求正迫使复合材料生产商转向低溶剂或水性化学品,从而调整其原材料组合和利润结构。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对基础建设计划的大规模投资

- 严格的节能标准推动了对高性能外加剂的需求。

- 预拌混凝土和预製构件施工方法的快速普及

- 循环经济政策促进低碳建筑材料的使用。

- 人工智慧驱动的混合设计平台,可提高化学品计量精度

- 市场限制

- 石油基树脂价格波动

- 由于劳动力短缺,新计画启动延迟

- 消防法规的变更限制了溶剂型化学品的使用。

- 价值链分析

- 监管环境

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 产业间竞争

第五章 市场规模与成长预测

- 副产品

- 黏合剂

- 热熔胶

- 反应性

- 溶剂型

- 水溶液

- 锚栓和水泥浆

- 水泥基固定材料

- 树脂固定

- 混凝土外加剂

- 加速器

- 空气引射器

- 高效减水剂

- 缓速器

- 收缩抑制剂

- 黏度调节剂

- 塑化剂

- 其他的

- 混凝土保护涂层

- 丙烯酸纤维

- 醇酸树脂

- 环氧树脂

- 聚氨酯

- 其他树脂

- 地板树脂

- 丙烯酸纤维

- 环氧树脂

- 聚天门冬胺酸树脂

- 聚氨酯

- 其他树脂

- 维修和维修化学品

- 纤维缠绕系统

- 压浆

- 微型混凝土砂浆

- 改质砂浆

- 钢筋保护材料

- 密封剂

- 丙烯酸纤维

- 环氧树脂

- 聚氨酯

- 硅酮

- 其他树脂

- 表面处理化学品

- 固化剂

- 释放剂

- 其他的

- 防水解决方案

- 化学品

- 防水膜

- 黏合剂

- 按最终用户类别

- 商业的

- 工业和公共设施

- 基础设施

- 住宅

- 按地区

- 美国

- 加拿大

- 墨西哥

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- ARDEX Americas

- Arkema(Bostik)

- Ashland

- Dow

- Henkel AG & Co. KGaA

- Holcim Group

- Kingspan Group

- LATICRETE International, Inc

- MAPEI SpA

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Xypex USA

第七章 市场机会与未来展望

第八章:执行长面临的关键策略挑战

The North America Construction Chemicals Market was valued at USD 19.20 billion in 2025 and estimated to grow from USD 20.3 billion in 2026 to reach USD 26.79 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

Infrastructure modernization programs, buy-clean procurement rules, and the rise of AI-enabled mix-design platforms are simultaneously expanding product demand and redefining specification pathways. Highway, bridge, and water-infrastructure upgrades funded by the Infrastructure Investment and Jobs Act (IIJA) fuel a steady pipeline of large-volume concrete applications that require high-efficiency admixtures capable of extending service life while offsetting raw material inflation. State-level embodied-carbon mandates are steering buyers toward low-GWP waterproofing membranes and supplementary-cementitious-material-compatible admixtures, creating premium pricing niches for verified sustainable chemistries. Data-center and semiconductor megaprojects drive the rapid adoption of fire-resistant coatings, precision sealants, and quick-turn curing compounds, while energy-efficiency codes increase demand for high-performance adhesives within advanced envelope systems. Petro-derived resin price swings and skilled-labor shortages remain cost headwinds; however, suppliers with vertically integrated feedstock positions and simplified application technologies are mitigating margin risk.

North America Construction Chemicals Market Trends and Insights

Substantial investments in infrastructure projects

Many transportation improvements and bridge repairs, financed by the IIJA, are translating into consistent, high-volume demand for protective coatings, repair mortars, and water treatment chemicals. Cost inflation-characterized by growth in highway-construction indices during 2022-has eroded purchasing power, prompting agencies to shift toward performance-based specifications that emphasize lifecycle durability. Canadian federal and provincial programs mirror the U.S. momentum, particularly for waterproofing systems engineered to withstand freeze-thaw cycles. Suppliers that can document extended asset life under accelerated-aging protocols are winning multi-year framework contracts. Vertical integration in raw material sourcing is emerging as a hedge against bid volatility, allowing producers to honor fixed-price commitments despite fluctuations in feedstock prices.

Stringent energy-efficiency codes spurring high-performance admixtures

Convergence of Title 24, IECC, and provincial energy codes has elevated the minimum thermal performance required of walls and roofs, driving adoption of advanced sealants and adhesive systems that support continuous-insulation assemblies. The same projects must now also demonstrate lower embodied carbon, creating dual pressure for admixtures that reduce cement content without compromising strength. Concrete producers increasingly specify superplasticizers that allow higher fly-ash or slag substitution ratios, and some are integrating nano-silica blends to meet stringent modulus targets. Chemical suppliers offering cradle-to-gate EPDs and technical modeling support are displacing commodity providers in public-sector bids. In commercial buildings, energy modeling tools are linking thermal and structural simulations, further tightening tolerances on chemical performance at thinner slab profiles.

Volatility in petro-derived resin prices

Epoxy resin spot prices spiked after USITC launched an antidumping inquiry, squeezing margins in specialty coatings that rely on high-purity bisphenol-A feedstock. Manufacturers with Gulf-Coast plants enjoy freight advantages but remain vulnerable to hurricane-related outages. Hedging strategies include dual-sourcing from Asia and building on-site tank storage to smooth supply shocks. End-users are trialing hybrid systems that replace petro content with bio-based epoxies, but these blends still command price premiums and face limited code approvals. Dynamic pricing clauses have become standard in multi-year supply contracts to pass through feedstock price fluctuations.

Other drivers and restraints analyzed in the detailed report include:

- Rapid adoption of ready-mix and precast methods

- Circular economy mandates favoring low-carbon construction materials

- Labor shortages slowing new project starts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing Solutions accounted for 32.62% of the North America construction chemicals market in 2025 and is projected to grow at a 6.09% CAGR through 2031, reflecting heightened focus on building-envelope integrity under stricter moisture-management codes. The segment outpaces overall market expansion as liquid-applied membranes replace sheet systems to cut labor hours and accommodate complex geometries. Manufacturers are blending polymer-modified asphalt with reactive silanes to achieve elongation while maintaining vapor permeability, meeting dual performance targets in energy-efficient assemblies. Hybrid systems that reinforce fluid membranes with geo-textile fabrics command premiums over standard products. Surface-treatment chemicals and curing compounds follow the same trend as precast producers, who emphasize release cleanliness and hydration control to accelerate plant throughput. Meanwhile, concrete-admixture suppliers are incorporating shrinkage-reducing additives into integrated waterproofing packages, enabling contractors to source multi-functional solutions under a single warranty.

Concrete Admixtures remain a significant product group, driven by superplasticizers that deliver 25 MPa strength at 50% replacement levels of portland cement-a critical capability for low-carbon bids. Repair and rehabilitation chemicals, including fiber-wrapping epoxies and ultra-rapid-setting mortars, benefit from the aging bridge stock, with many federal projects already specifying these systems for deck overlays. Adhesives, sealants, and flooring resins maintain steady demand tied to commercial facade upgrades and high-traffic retail refurbishments. VOC restrictions and NFPA 285 compliance continue to push formulators toward low-solvent or water-borne chemistries, reshaping raw-material portfolios and margin profiles.

The North America Construction Chemicals Market Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, and More), End-User Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- ARDEX Americas

- Arkema (Bostik)

- Ashland

- Dow

- Henkel AG & Co. KGaA

- Holcim Group

- Kingspan Group

- LATICRETE International, Inc

- MAPEI S.p.A.

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Xypex USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Substantial investments in infrastructure projects

- 4.2.2 Stringent energy-efficiency codes spurring high-performance admixtures

- 4.2.3 Rapid adoption of ready-mix and precast methods

- 4.2.4 Circular economy mandates favouring low-carbon construction materials

- 4.2.5 AI-enabled mix-design platforms boosting chemical dosage accuracy

- 4.3 Market Restraints

- 4.3.1 Volatility in petro-derived resin prices

- 4.3.2 Labor shortages slowing new project starts

- 4.3.3 Fire-safety rule changes curbing solvent-borne chemistries

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-User Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 ARDEX Americas

- 6.4.3 Arkema (Bostik)

- 6.4.4 Ashland

- 6.4.5 Dow

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Holcim Group

- 6.4.8 Kingspan Group

- 6.4.9 LATICRETE International, Inc

- 6.4.10 MAPEI S.p.A.

- 6.4.11 RPM International Inc.

- 6.4.12 Saint-Gobain

- 6.4.13 Sika AG

- 6.4.14 Xypex USA

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

建筑化学品市场:2026-2032年全球市场预测(依产品类型、技术、剂型、建筑类型、应用、最终用户和通路划分)固定式机械锚栓市场:依产品类型、材料、应用、终端用户产业及通路划分,全球预测,2026-2032年

建筑化学品市场:2026-2032年全球市场预测(依产品类型、技术、剂型、建筑类型、应用、最终用户和通路划分)固定式机械锚栓市场:依产品类型、材料、应用、终端用户产业及通路划分,全球预测,2026-2032年 建筑化学品市场分析及预测(至2035年):类型、产品、应用、形态、材质类型、技术、最终用户、功能、安装类型、解决方案

建筑化学品市场分析及预测(至2035年):类型、产品、应用、形态、材质类型、技术、最终用户、功能、安装类型、解决方案 建筑化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

建筑化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球建筑化学品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球建筑化学品市场规模、份额、趋势和成长分析报告(2026-2034年) 建筑化学品市场规模、份额、趋势及预测(按类型、应用和地区划分)(2026-2034 年)

建筑化学品市场规模、份额、趋势及预测(按类型、应用和地区划分)(2026-2034 年) 2026年全球建筑化学品市场报告

2026年全球建筑化学品市场报告