|

市场调查报告书

商品编码

1911820

马来西亚建筑化学品市场-份额分析、产业趋势与统计、成长预测(2026-2031)Malaysia Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

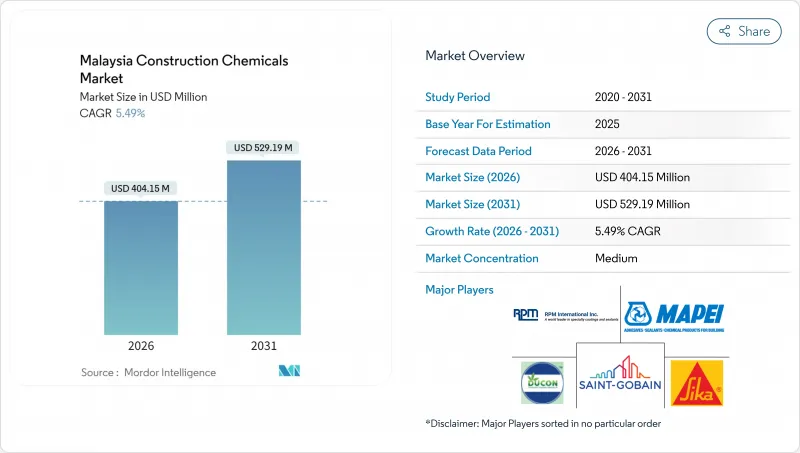

预计马来西亚建筑化学品市场将从 2025 年的 3.8312 亿美元成长到 2026 年的 4.0415 亿美元,到 2031 年将达到 5.2919 亿美元,2026 年至 2031 年的复合年增长率为 5.49%。

持续的基础设施投资势头,包括2024年1月至11月期间授予的1837亿元人民币计划,正支撑着市场销量的稳步增长,因为开发商指定使用高性能外加剂、防水卷材和防护涂料。诸如2025年1月签署的柔佛-新加坡经济特区等大型企划,预计将加速对适用于海洋和高湿度环境的耐用化学品的需求。马来西亚建筑化学品市场也受惠于政府强制要求公共工程中90%采用BIM(建筑资讯模型)的政策,这有利于能够与自动化施工流程无缝整合的精密工程产品。同时,绿建筑认证的推进也推动了低VOC(挥发性有机化合物)和可回收配方的应用,使製造商能够在抓住永续性机会的同时,获得更高的溢价。

马来西亚建筑化学品市场趋势与洞察

加速永续的公共和私人基础设施投资

马来西亚强劲的基础设施发展计画(2024年合约总额:人民币1837亿元)推动了桥樑、隧道和城市轨道交通系统专用防水卷材、聚合物改性水泥浆和防腐蚀涂料的需求成长。光是柔佛-新加坡经济特区就计划在五年内完成50个跨境计划,这将带动对耐咸水环境的海洋密封剂和碳酸盐阻隔剂的需求。包括特斯拉和英特尔等製造巨头公私合营,进一步提高了性能标准,并促进了静电耗散型地板树脂和耐化学腐蚀墙面涂料规范的发展。道路、港口和数位化管道的改善吸引了更多配套商业计划,从而在马来西亚建筑化学品市场中形成良性循环,促进产品需求成长。

低收入住宅政策推动了住宅化学品消耗

国家住宅计画加速推进补贴住宅,规范了预拌混凝土和预製墙板的使用,扩大了外加剂的使用范围,并提高了品质标准。低收入住宅开发商自愿采用绿色建筑标准,推动了对水性丙烯酸密封剂和低VOC瓷砖黏合剂的需求,这些产品符合绿色建筑指数设定的碳减排目标。该计划扩展到怡保和古晋等区域城市,扩大了分销网络,促使供应商采用小包装并配备行动技术服务团队。对成本敏感的计划正在采用耐用且价格具有竞争力的化学品,而本地製造商正在扩大自动化生产线规模,以确保批次品质的稳定性。

原物料价格波动限制了市场扩张。

进口聚合物、特殊溶剂和高性能添加剂占高端配方原料成本的60%之多,使得製造商极易受到外汇波动和油价飙升的影响。儘管马来西亚国家石油公司(Petronas)已签订了到2026年的远期供应协议,但规模较小的企业通常以现货方式采购,这在原材料成本上涨时会为其息EBITDA获利率)带来压力。位于边佳兰(Pengerang)的价值35亿美元的石化综合体自2025年中期开始建设,将进一步整合本地供应,但预计要到2028年才能达到设计产能。在此之前,市场波动可能会加速产业整合,因为资金短缺的企业会将市场占有率拱手让给一体化跨国公司。

细分市场分析

到2025年,防水解决方案将占据马来西亚建筑化学品市场48.42%的份额,这主要得益于吉隆坡和新山高层建筑计划对屋顶和裙楼平台防水的强制性规范。虽然沥青改质防水卷材在销售方面仍保持领先地位,但聚合物-水泥混合产品因其在地下工程中快速固化的特性而日益受到青睐。随着交通导向开发项目、港口、资料中心和需要在潮湿环境中长期使用的地下设施的建设,马来西亚防水领域建筑化学品市场的规模预计将持续扩大。

预计到2031年,表面处理化学品将以6.78%的复合年增长率实现最高增长,这主要得益于先进的固化剂和专为预製外墙板优化的脱模乳液的推动。防涂鸦密封剂和疏水性硅烷凝胶预计将受到市政基础设施项目的青睐,这些项目旨在降低维护成本。创新正朝着奈米工程颗粒的方向发展,这些颗粒能够在不增加VOC含量的情况下提高耐磨性,同时满足绿建筑认证标准。

其他福利

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 基础建设计划中可持续的公私合作投资

- 透过推广低成本住宅来增加住宅开工量

- 绿建筑认证推动对低挥发性有机化合物、耐用化学品的需求

- 预拌混凝土快速摊舖及预製外加剂渗透性提高

- 透过经济特区(SEZ)的税收优惠实现特种化学品生产的本地化

- 市场限制

- 原材料价格波动会对生产商的利润率带来压力。

- 遵守环境、健康和安全 (EHS) 法规(禁止使用挥发性有机化合物 (VOC) 和有害溶剂)的成本不断上升

- 能够操作先进化学技术的熟练工人短缺

- 价值链分析

- 监管环境

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 副产品

- 黏合剂

- 热熔胶

- 反应性

- 溶剂型

- 水溶液

- 锚栓和水泥浆

- 水泥基固定剂

- 树脂固定

- 混凝土外加剂

- 加速器

- 空气引射器

- 高效减水剂

- 缓速器

- 收缩抑制剂

- 黏度调节剂

- 塑化剂

- 其他的

- 混凝土保护涂层

- 丙烯酸纤维

- 醇酸树脂

- 环氧树脂

- 聚氨酯

- 其他的

- 地板树脂

- 丙烯酸纤维

- 环氧树脂

- 聚天门冬胺酸

- 聚氨酯

- 其他的

- 修復和修復化学产品

- 纤维缠绕系统

- 压浆

- 微型混凝土砂浆

- 改质砂浆

- 钢筋保护材料

- 密封剂

- 丙烯酸纤维

- 环氧树脂

- 聚氨酯

- 硅

- 其他的

- 表面处理化学品

- 固化剂

- 释放剂

- 其他的

- 防水解决方案

- 化学品

- 防水膜

- 黏合剂

- 透过使用

- 商业的

- 工业和公共设施

- 基础设施

- 住宅

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- ARDEX-QUICSEAL SINGAPORE

- Arkema(Bostik)

- Cementaid International

- Dribond Construction Chemicals

- Ducon Construction Chemicals

- Henkel AG & Co. KGaA

- MAPEI SpA

- MC-Bauchemie

- PENETRON MALAYSIA SDN BHD.

- RPM International

- Saint-Gobain

- Sika AG

- Terraco Holdings Ltd.

第七章 市场机会与未来展望

The Malaysia Construction Chemicals Market is expected to grow from USD 383.12 million in 2025 to USD 404.15 million in 2026 and is forecast to reach USD 529.19 million by 2031 at 5.49% CAGR over 2026-2031.

Sustained infrastructure momentum, including RMB 183.7 billion in projects awarded during the first 11 months of 2024, underpins steady volume growth as developers specify higher-performance admixtures, waterproofing membranes, and protective coatings. Mega-projects, such as the Johor-Singapore Special Economic Zone, signed in January 2025, are expected to accelerate demand for durable chemistries suited to marine and high-humidity environments. The Malaysia construction chemicals market also benefits from the government's 90% BIM adoption mandate for public works, which favors precision-engineered products that integrate seamlessly with automated construction workflows. In parallel, the momentum for green-building certification stimulates the uptake of low-VOC and recyclable formulations, enabling manufacturers to command premium price points while capturing sustainability-driven opportunities.

Malaysia Construction Chemicals Market Trends and Insights

Sustainable Public and Private Infrastructure Investment Acceleration

Malaysia's robust infrastructure pipeline, valued at RMB 183.7 billion in contracts awarded during 2024, sustains growth for specialty waterproofing membranes, polymer-modified grouts, and corrosion-inhibiting coatings used in bridges, tunnels, and urban rail systems. The Johor-Singapore Special Economic Zone alone aims to target 50 cross-border projects within five years, thereby amplifying demand for marine-grade sealants and anti-carbonate admixtures that can withstand brackish conditions. Public-private partnerships that include manufacturing giants such as Tesla and Intel further elevate performance benchmarks, driving the development of specifications for electrostatic-dissipative flooring resins and chemical-resistant wall coatings. Upgraded roads, ports, and digital pathways attract secondary commercial projects, reinforcing a virtuous cycle of product demand across the Malaysian construction chemicals market.

Affordable Housing Programs Driving Residential Chemical Consumption

The National Housing Policy's accelerated rollout of subsidized units standardizes the use of ready-mix concrete and prefabricated wall panels, expanding admixture volumes while tightening quality tolerances. Developers engaged in low-income housing voluntarily adopt green building criteria, fueling demand for water-based acrylic sealants and low-VOC tile adhesives that align with carbon reduction goals outlined by the Green Building Index. The policy's geographic spread into secondary cities, such as Ipoh and Kuching, enlarges distribution networks, prompting suppliers to introduce small-pack formulations and mobile technical service teams. Cost-sensitive projects rely on high-durability yet price-competitive chemistries, incentivizing local manufacturers to scale automated production lines for consistent batch quality.

Feedstock Price Volatility Constraining Market Expansion

Imported polymers, specialty solvents, and performance additives account for up to 60% of the raw material cost in premium formulations, exposing manufacturers to currency fluctuations and crude oil price spikes. PETRONAS has locked in forward supply contracts through 2026, but small and mid-sized players purchase on spot terms, eroding EBITDA margins when feedstock costs rise. The Pengerang-based USD 3.5 billion petrochemical complex, under construction since mid-2025, will enhance local supply integration but is not expected to reach nameplate output before 2028. Until then, volatility may accelerate consolidation as under-capitalized firms cede share to integrated multinationals.

Other drivers and restraints analyzed in the detailed report include:

- Green Building Certification Momentum Reshaping Chemical Specifications

- Ready-Mix Concrete and Prefabrication Technology Integration

- Environmental Health and Safety Compliance Cost Escalation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions captured 48.42% of the Malaysian construction chemicals market share in 2025, driven by mandatory rooftop and podium deck specifications in high-rise developments across Kuala Lumpur and Johor Bahru. Bitumen-modified membranes retain their leadership in volume, while polymer-cementitious hybrids gain favor for their rapid-setting underground applications. The Malaysian construction chemicals market size for waterproofing is projected to expand in lockstep with transit-oriented developments, ports, and data center basements that require a long service life in humid conditions.

Surface-treatment chemicals are expected to register the fastest 6.78% CAGR through 2031, driven by advanced curing agents and mold-release emulsions optimized for precast facade panels. Anti-graffiti sealers and hydrophobic silane gels enjoy rising demand from municipal infrastructure programs aimed at reducing maintenance costs. Innovation is pivoting toward nano-engineered particles that enhance abrasion resistance without increasing VOC levels, aligning with green-building credits.

The Malaysia Construction Chemicals Market Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, and Waterproofing Solutions) and End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, Residential). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ARDEX-QUICSEAL SINGAPORE

- Arkema (Bostik)

- Cementaid International

- Dribond Construction Chemicals

- Ducon Construction Chemicals

- Henkel AG & Co. KGaA

- MAPEI S.p.A.

- MC-Bauchemie

- PENETRON MALAYSIA SDN BHD.

- RPM International

- Saint-Gobain

- Sika AG

- Terraco Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainable public and private investments in infrastructure projects

- 4.2.2 Affordable-housing push expanding residential starts

- 4.2.3 Green-building certification fueling demand for low-VOC and durable chemistries

- 4.2.4 Rapid adoption of ready-mix concrete and prefab raising admixture penetration

- 4.2.5 SEZ tax breaks localising specialty-chemical production

- 4.3 Market Restraints

- 4.3.1 Feedstock price volatility squeezing producer margins

- 4.3.2 Rising EHS compliance costs (VOC, hazardous solvent bans)

- 4.3.3 Shortage of trained applicators for advanced chemistries

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ARDEX-QUICSEAL SINGAPORE

- 6.4.2 Arkema (Bostik)

- 6.4.3 Cementaid International

- 6.4.4 Dribond Construction Chemicals

- 6.4.5 Ducon Construction Chemicals

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 MAPEI S.p.A.

- 6.4.8 MC-Bauchemie

- 6.4.9 PENETRON MALAYSIA SDN BHD.

- 6.4.10 RPM International

- 6.4.11 Saint-Gobain

- 6.4.12 Sika AG

- 6.4.13 Terraco Holdings Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

建筑化学品市场分析及预测(至2035年):类型、产品、应用、形态、材质类型、技术、最终用户、功能、安装类型、解决方案

建筑化学品市场分析及预测(至2035年):类型、产品、应用、形态、材质类型、技术、最终用户、功能、安装类型、解决方案 建筑化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

建筑化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 建筑化学品市场规模、份额、趋势及预测(按类型、应用和地区划分)(2026-2034 年)

建筑化学品市场规模、份额、趋势及预测(按类型、应用和地区划分)(2026-2034 年) 2026年全球建筑化学品市场报告

2026年全球建筑化学品市场报告 建筑化学品市场-全球产业规模、份额、趋势、机会及预测(2021-2031 年)(依产品类型、应用、地区及竞争格局划分)中东建筑化学品市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)北美建筑化学品市场-份额分析、产业趋势与统计、成长预测(2026-2031)

建筑化学品市场-全球产业规模、份额、趋势、机会及预测(2021-2031 年)(依产品类型、应用、地区及竞争格局划分)中东建筑化学品市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)北美建筑化学品市场-份额分析、产业趋势与统计、成长预测(2026-2031)