|

市场调查报告书

商品编码

1910901

日本资料中心市场-份额分析、产业趋势、统计和成长预测(2026-2031)Japan Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

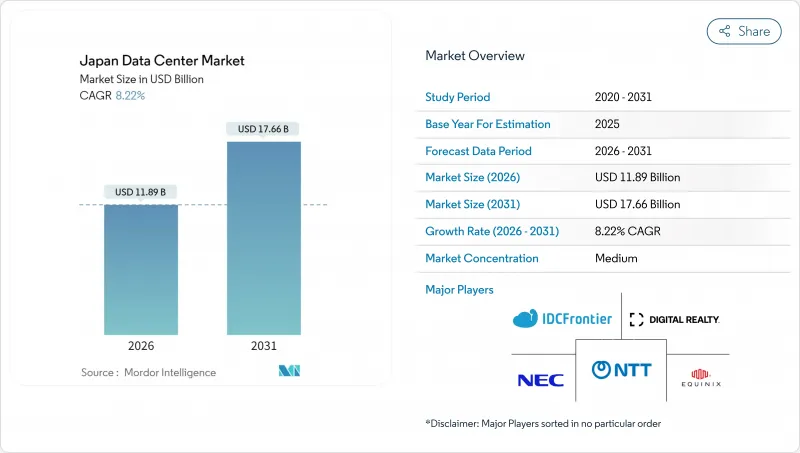

日本资料中心市场预计将从 2025 年的 109.9 亿美元成长到 2026 年的 118.9 亿美元,到 2031 年达到 176.6 亿美元,2026 年至 2031 年的复合年增长率为 8.22%。

就IT负载容量而言,市场预计将从2025年的3,340兆瓦成长到2030年的6,460兆瓦,在预测期(2025-2030年)内复合年增长率(CAGR)为14.12%。市场占有率和估计值均以兆瓦(MW)为单位计算和报告。在公共部门云端政策、超大规模资本支出以及人工智慧工作负载激增的推动下,丛集(目前已是亚太地区最大的集群)预计将巩固主导地位。国内营运商正受益于优先发展自主云端的政策,而全球云端供应商则正在将容量本地化以满足资料居住法规的要求。 5G的持续部署和物联网(IoT)的日益普及正在推动边缘运算的需求,促使中等规模的配置靠近人口中心和製造地。同时,土地短缺、电价上涨和抗震设计成本迫使开发商优化设施选址、创新冷却技术并向郊区走廊多元化发展,以维持日本资料中心市场的成长动能。

日本资料中心市场趋势与洞察

政府数位转型计画加速云端迁移

日本数位局已设定目标,计划在2025年前将中央政府的工作负载全面迁移到云端平台,并有望成为国内新增资料中心容量的主要租户,以维护资料主权。为满足这项激增的需求,亚马逊云端服务(AWS)计划在2027年前投资2.26兆日圆(约152.4亿美元)扩建其位于东京和大阪的资料中心。地方政府和国有企业类似的现代化趋势也推动了对地方政府需求的成长,确保了新建设计划的早期预订率。国内供应商在公共采购中享有优先权,而全球超大规模资料中心业者正在加快合资策略,以满足采购法规的要求。最终,政府工作负载源源不绝地涌入,为日本资料中心市场未来多年的运转率提供了支撑。

超大规模投资激增,以应对人工智慧和OTT流量成长。

人工智慧模型的训练已将每个机架的功率密度提升至30kW以上,微软承诺投资29亿美元,为日本客户打造配备丰富GPU的资料中心园区。谷歌斥资10亿美元建造的「Proa」和「Taihei」海底光缆正在提升跨太平洋的传输能力,并将东京和大阪定位为重要的整合中心。日本国内主要企业Softbank Corporation与英伟达合作,共同打造一座人工智慧优化型资料中心,这进一步印证了高密度运算已成为一项策略资产。这些倡议缩短了供需週期,加快了审批速度,并加剧了对有限兆瓦级配额的竞争,所有这些都在推动日本资料中心市场的扩张。

主要热点地区土地稀缺且高成本

预计到2024年,东京市中心地价将上涨69%,将推高资料中心开发预算,并挤压内部报酬率。江东区居民的反对凸显了社会接受度方面的障碍,迫使业者将业务拓展至印西市等郊区,这些地区拥有更广阔的土地资源,且地方政府的激励措施能够改善计划的计划。虽然搬迁可以降低土地成本,但需要同时投资建造暗纤和冗余变电站,这将延长专案建设週期,并限制日本资料中心市场的短期供应。

细分市场分析

预计到2031年,容量在5兆瓦至20兆瓦之间的中型资料中心将以12.02%的复合年增长率成长,超过日本整体资料中心市场的成长速度。这种规模的资料中心既能实现冷却和保全方面的规模经济效益,又能保持位置的柔软性,从而避免大型资料中心园区面临的土地和电力限制。大型资料中心仍占据38.10%的市场份额,因为像亚马逊网路服务(AWS)这样的超大规模资料中心业者营运商会购置连片土地来建造100兆瓦以上的丛集。然而,这些计划面临的监管和社区障碍会延长开发週期,使中型资料中心在上市速度上更具优势。由经济产业省支持的福岛人工智慧资料中心项目,就体现了政府对可在不同地区复製的15兆瓦分散式资料中心的支持政策。

开发人员倾向于采用模组化设计,以便逐步启动,从而使资本投资与合约授予保持一致,同时最大限度地减少閒置容量。对于考虑迁移传统设备的公司而言,中型资料中心是整合多个本地部署地点的理想选择。此外,支援 5G 和物联网的边缘运算节点通常也适用于此规模范围,从而增强运转率的弹性。因此,即使超大规模资料中心正在兴起,预计中型机房仍将主导日本资料中心市场未来的成长。

截至2025年,三级资料中心将占日本资料中心市场的66.05%,年复合成长率达15.28%。其99.982%的运转率满足大多数审核标准和灾害復原要求,无需像四级资料中心那样配备双电源或并行维护冗余。营运商整合隔震轴承、阻尼器和加固框架,以确保这些设施能够承受7级地震并维持服务水准。这种方法强调风险与成本的平衡。一级和二级资料中心用于开发和测试环境以及非关键储存应用场景,特别适用于电力预算紧张的农村地区。四级资料中心由于资本投入高昂,仅限于延迟要求极低的交易平台和核心营运商交换器。

标准化正在加速三级资料中心的发展。预製电气和机械撬装设备减少了现场施工,将工期从24个月缩短至18个月。此外,由于已有预先已通过核准的抗震和节能计算模板,此模式也简化了监理申报流程。因此,三级资料中心可望进一步扩大其优势,并推动日本资料中心市场架构的演进。

日本资料中心市场报告按资料中心规模(大型、超大型、中型、巨型、小规模)、等级(Tier 1、Tier 2、Tier 3、Tier 4)、资料中心类型(超大规模/自建、企业/边缘、託管)、最终用户(银行、金融服务和保险 (BFSI)、IT 及 ITES、电子商务、政府、製造业、媒体和电信市场预测以 IT 负载容量(兆瓦,MW)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场驱动因素

- 政府数位转型计画加速云端迁移

- 超大规模投资激增,以适应人工智慧和OTT流量成长

- 5G赋能的物联网的普及将推动边缘配置。

- 数据本地化规则将鼓励国内产能扩张

- 老旧企业办公室的退役推动了託管需求。

- 大阪和东京城市余热回收奖励措施。

- 市场限制

- 主要热点地区土地稀缺且高成本

- 与其他本地公司相比,电费较高

- 地震和灾害抵御能力成本溢价

- 併网核准流程前置作业时间较长

- 市场展望

- IT负载能力

- 高架地板面积

- 託管收入

- 预装机架

- 机架空间利用率

- 海底电缆

- 主要行业趋势

- 智慧型手机用户数量

- 每部智慧型手机的数据流量

- 行动资料通讯速度

- 宽频资料传输速度

- 光纤连接网路

- 法律规范

- 价值炼和通路分析

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按资料中心规模

- 大规模

- 巨大的

- 中号

- 百万

- 小规模

- 依层级类型

- 一级和二级

- 三级

- 第四级

- 依资料中心类型

- 超大规模/内部建设

- 企业/边缘运算

- 搭配

- 未使用的

- 运作中

- 零售共址

- 批发託管

- 最终用户

- BFSI

- 资讯科技/资讯科技服务

- 电子商务

- 政府机构

- 製造业

- 媒体与娱乐

- 沟通

- 其他最终用户

- 透过热点

- 大阪市

- 高松

- 东京

- 其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Equinix Inc.

- MC Digital Realty(Digital Realty Trust Inc. and Mitsubishi Corporation JV)

- AT TOKYO Corporation

- Amazon Web Services Inc.

- NTT Global Data Centers(NTT Ltd.)

- netXDC(SCSK Corporation)

- IDC Frontier Inc.(Yahoo Japan subsidiary)

- AirTrunk Operating Pty Ltd.

- NEC Corporation

- IBM Japan Ltd.

- Colt Data Centre Services Holdings Ltd.

- Alibaba Cloud(Alibaba Group Holding Ltd.)

- Microsoft Corporation

- Telehouse(KDDI Corporation)

- Additional regional and niche operators

第七章 市场机会与未来展望

The Japan Data Center Market is expected to grow from USD 10.99 billion in 2025 to USD 11.89 billion in 2026 and is forecast to reach USD 17.66 billion by 2031 at 8.22% CAGR over 2026-2031.

In terms of IT load capacity, the market is expected to grow from 3.34 thousand megawatt in 2025 to 6.46 thousand megawatt by 2030, at a CAGR of 14.12% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Fueled by public-sector cloud mandates, hyperscale capital outlays, and proliferating artificial-intelligence workloads, the cluster is already the largest in Asia-Pacific and is on course to consolidate regional primacy. Domestic operators benefit from policy preferences for sovereign cloud while global cloud providers localize capacity to satisfy data-residency rules. Sustained 5G rollout and Internet-of-Things (IoT) adoption intensify edge-computing needs, encouraging medium-scale deployments near population and manufacturing centers. Simultaneously, land scarcity, electricity tariffs and seismic engineering premiums compel developers to optimize facility footprints, innovate in cooling and diversify toward suburban corridors to keep the Japan data center market growth momentum intact.

Japan Data Center Market Trends and Insights

Government Digital Transformation Programs Accelerating Cloud Migration

The Digital Agency targets complete migration of central-government workloads to cloud platforms by 2025, creating an anchor tenant for new capacity located inside Japan to preserve data sovereignty. Amazon Web Services has earmarked JPY 2.26 trillion (USD 15.24 billion) through 2027 to scale facilities in Tokyo and Osaka to meet this surge. Similar modernization waves in municipalities and state-owned corporations extend demand into regional prefectures, ensuring that new builds achieve rapid pre-commit rates. Domestic providers gain selection preference in public tenders, while global hyperscalers accelerate joint-venture strategies to satisfy procurement rules. The outcome is a steady pipeline of government workloads that underpins multi-year utilization visibility for the Japan data center market.

Surge in Hyperscale Investments to Meet AI and OTT Traffic Growth

Artificial-intelligence model training pushes power density above 30 kW per rack, prompting Microsoft to pledge USD 2.9 billion for GPU-rich campuses serving Japanese customers. Google's USD 1 billion Proa and Taihei subsea cables improve trans-Pacific throughput, positioning Tokyo and Osaka as primary aggregation nodes. Domestic champion SoftBank collaborates with NVIDIA on AI-optimized halls, reinforcing that high-density compute has become a strategic asset. These commitments shorten supply-demand cycles, compress permitting windows, and intensify competition for scarce megawatt allocations, all of which add tailwinds to Japan data center market expansion.

Scarcity and High Cost of Land in Prime Hotspots

Average land prices in central Tokyo rose 69% during 2024, inflating facility-development budgets and squeezing internal rates of return. Community pushback in Koto ward underscores social-license barriers, forcing operators to scout suburban areas such as Inzai, where larger parcels exist and municipal incentives improve project economics. While relocation mitigates land cost, it demands parallel investment in dark-fiber routes and redundant sub-stations, elongating project timelines and tempering near-term Japan data center market supply.

Other drivers and restraints analyzed in the detailed report include:

- 5G-Enabled IoT Proliferation Driving Edge Deployments

- Decommissioning of Ageing Enterprise Sites Boosting Colocation Demand

- Long Grid-Connection Approval Lead Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-sized halls between 5 MW and 20 MW are on track for a 12.02% CAGR to 2031, outpacing the overall Japan data center market. These footprints deliver economies of scale in cooling and security while retaining siting flexibility that circumvents the land and power constraints dogging mega-campuses. Large-scale sites retain 38.10% share because hyperscalers like Amazon Web Services reserve contiguous land for clusters exceeding 100 MW. Yet the regulatory and community hurdles tied to such projects prolong gestation periods, giving medium builds a speed-to-market edge. The Fukushima AI facility, backed by the Ministry of Economy and Trade illustrates policy support for distributed 15-MW blocks that can be replicated across regions.

Developers favor modular designs that allow phased power rollouts, letting them match capital deployment to contract wins while limiting stranded capacity. Enterprises migrating legacy rooms find the medium footprint ideal for consolidating multiple on-premise sites under one roof. Moreover, edge-compute nodes supporting 5G and IoT often scale within this band, enhancing utilization resilience. Consequently, medium halls are expected to become the volume engine for future Japan data center market size additions, even as hyperscale complexes command headlines.

Tier 3 facilities hold 66.05% share of Japan data center market size in 2025 and are expanding at 15.28% CAGR. Their 99.982% uptime rating meets most audit and disaster-recovery thresholds without incurring the dual utility feeds and concurrent-maintenance redundancy of Tier 4. Operators integrate base-isolation bearings, dampers, and reinforced frames so these halls withstand magnitude-7 quakes while maintaining service levels, a design approach that balances risk and cost. Tier 1 and Tier 2 footprints serve dev-test and non-critical storage use cases, especially in regional sites where power budgets are tighter. Tier 4 remains confined to latency-sensitive trading platforms and core switching sites for telecom carriers due to capex intensity.

Standardization accelerates Tier 3 development. Prefabricated electrical and mechanical skids reduce field labor, compressing build schedules from 24 to 18 months. The model also simplifies regulatory submissions because templates have pre-approved seismic and energy-efficiency calculations. Accordingly, Tier 3 is likely to deepen its lead, anchoring how the Japan data center market architecturally evolves.

The Japan Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Equinix Inc.

- MC Digital Realty (Digital Realty Trust Inc. and Mitsubishi Corporation JV)

- AT TOKYO Corporation

- Amazon Web Services Inc.

- NTT Global Data Centers (NTT Ltd.)

- netXDC (SCSK Corporation)

- IDC Frontier Inc. (Yahoo Japan subsidiary)

- AirTrunk Operating Pty Ltd.

- NEC Corporation

- IBM Japan Ltd.

- Colt Data Centre Services Holdings Ltd.

- Alibaba Cloud (Alibaba Group Holding Ltd.)

- Microsoft Corporation

- Telehouse (KDDI Corporation)

- Additional regional and niche operators

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Government digital transformation programs accelerating cloud migration

- 4.1.2 Surge in hyperscale investments to meet AI and OTT traffic growth

- 4.1.3 5G-enabled IoT proliferation driving edge deployments

- 4.1.4 Data localisation rules favour domestic capacity additions

- 4.1.5 Decommissioning of ageing enterprise sites boosting colocation demand

- 4.1.6 Municipal waste-heat reuse incentives in Osaka and Tokyo

- 4.2 Market Restraints

- 4.2.1 Scarcity and high cost of land in prime hotspots

- 4.2.2 Elevated electricity tariffs versus regional peers

- 4.2.3 Earthquake and disaster-resilience cost premium

- 4.2.4 Long grid-connection approval lead times

- 4.3 Market Outlook

- 4.3.1 IT Load Capacity

- 4.3.2 Raised Floor Space

- 4.3.3 Colocation Revenue

- 4.3.4 Installed Racks

- 4.3.5 Rack Space Utilization

- 4.3.6 Submarine Cable

- 4.4 Key Industry Trends

- 4.4.1 Smartphone Users

- 4.4.2 Data Traffic Per Smartphone

- 4.4.3 Mobile Data Speed

- 4.4.4 Broadband Data Speed

- 4.4.5 Fiber Connectivity Network

- 4.4.6 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale / Self-built

- 5.3.2 Enterprise / Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Osaka City

- 5.5.2 Takamatsu

- 5.5.3 Tokyo

- 5.5.4 Rest of Japan

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Equinix Inc.

- 6.4.2 MC Digital Realty (Digital Realty Trust Inc. and Mitsubishi Corporation JV)

- 6.4.3 AT TOKYO Corporation

- 6.4.4 Amazon Web Services Inc.

- 6.4.5 NTT Global Data Centers (NTT Ltd.)

- 6.4.6 netXDC (SCSK Corporation)

- 6.4.7 IDC Frontier Inc. (Yahoo Japan subsidiary)

- 6.4.8 AirTrunk Operating Pty Ltd.

- 6.4.9 NEC Corporation

- 6.4.10 IBM Japan Ltd.

- 6.4.11 Colt Data Centre Services Holdings Ltd.

- 6.4.12 Alibaba Cloud (Alibaba Group Holding Ltd.)

- 6.4.13 Microsoft Corporation

- 6.4.14 Telehouse (KDDI Corporation)

- 6.4.15 Additional regional and niche operators

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

中东资料中心:市场占有率分析、产业趋势与统计、成长预测(2026-2031)义大利资料中心:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)印尼资料中心市场占有率分析、产业趋势与统计、成长预测(2026-2031)印度资料中心市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)德国资料中心市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚资料中心:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

中东资料中心:市场占有率分析、产业趋势与统计、成长预测(2026-2031)义大利资料中心:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)印尼资料中心市场占有率分析、产业趋势与统计、成长预测(2026-2031)印度资料中心市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)德国资料中心市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚资料中心:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本资料中心市场报告(按组件、类型、企业规模、最终用户和地区划分,2026-2034 年)

日本资料中心市场报告(按组件、类型、企业规模、最终用户和地区划分,2026-2034 年) 资料中心乙太网路切换器市场规模、份额和成长分析(按产品、交换连接埠、应用、最终用户、类型和地区划分)-2026-2033年产业预测

资料中心乙太网路切换器市场规模、份额和成长分析(按产品、交换连接埠、应用、最终用户、类型和地区划分)-2026-2033年产业预测 资料中心市场规模、份额和趋势分析报告:按组件、类型、伺服器机架密度、冗余、PUE、设计、层级、企业规模、最终用途、地区和细分市场预测(2026-2033 年)

资料中心市场规模、份额和趋势分析报告:按组件、类型、伺服器机架密度、冗余、PUE、设计、层级、企业规模、最终用途、地区和细分市场预测(2026-2033 年) 小型资料中心市场按产品类型、功率容量、部署应用、冷却技术和地区划分

小型资料中心市场按产品类型、功率容量、部署应用、冷却技术和地区划分